Global Edge Ai Enabled Diagnostic Imaging Devices Market

Market Size in USD Billion

USD

1.61 Billion

USD

6.13 Billion

2025

2033

USD

1.61 Billion

USD

6.13 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.61 Billion | |

| USD 6.13 Billion | |

| % | |

|

Edge-AI Enabled Diagnostic Imaging Devices Market Size

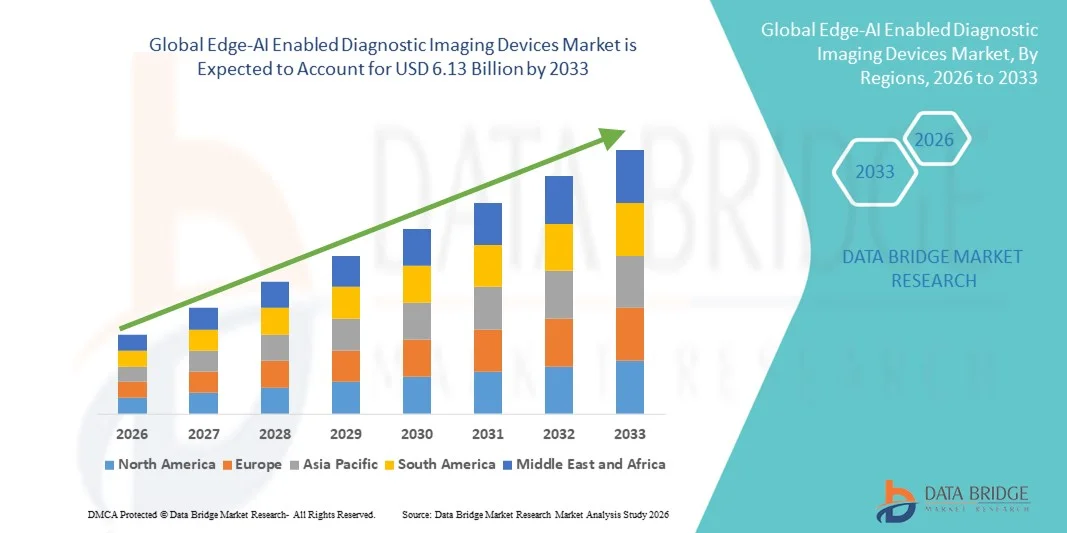

- The global edge-AI enabled diagnostic imaging devices market size was valued at USD 1.61 billion in 2025 and is expected to reach USD 6.13 billion by 2033, at a CAGR of 18.20% during the forecast period

- The market growth is largely fueled by the increasing integration of artificial intelligence and edge computing technologies in medical imaging systems, enabling faster image processing, real-time diagnostics, and improved clinical decision-making across hospitals and diagnostic centers

- Furthermore, rising demand for efficient, accurate, and real-time diagnostic solutions in healthcare facilities is establishing Edge-AI Enabled Diagnostic Imaging Devices as an important component of modern medical imaging infrastructure. These converging factors are accelerating the uptake of Edge-AI Enabled Diagnostic Imaging Devices solutions, thereby significantly boosting the industry's growth

Edge-AI Enabled Diagnostic Imaging Devices Market Analysis

- Edge-AI Enabled Diagnostic Imaging Devices, which integrate artificial intelligence directly within imaging equipment to enable real-time data processing and faster clinical decision-making, are becoming increasingly important in modern healthcare systems across hospitals and diagnostic imaging centers due to their ability to enhance diagnostic accuracy, reduce latency, and improve workflow efficiency

- The escalating demand for Edge-AI Enabled Diagnostic Imaging Devices is primarily fueled by the rapid adoption of artificial intelligence in healthcare, increasing demand for faster and more accurate diagnostic imaging, and the growing need for real-time data processing directly at the device level without reliance on centralized cloud infrastructure

- North America dominated the edge-AI enabled diagnostic imaging devices market with the largest revenue share of 38.6% in 2025, characterized by advanced healthcare infrastructure, high adoption of AI-driven medical technologies, and the strong presence of leading medical imaging device manufacturers, with the U.S. experiencing significant growth in AI-integrated imaging systems across hospitals and diagnostic centers

- Asia-Pacific is expected to be the fastest growing region in the edge-AI enabled diagnostic imaging devices market during the forecast period with a projected CAGR of 10.4%, due to increasing healthcare investments, growing adoption of AI-based healthcare technologies, and expanding diagnostic imaging infrastructure across emerging economies

- The portable devices segment dominated the largest market revenue share of 38.7% in 2025, driven by their widespread adoption in hospitals and diagnostic centers due to the convenience of mobility and ease of use

Report Scope and Edge-AI Enabled Diagnostic Imaging Devices Market Segmentation

|

Attributes |

Edge-AI Enabled Diagnostic Imaging Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Edge-AI Enabled Diagnostic Imaging Devices Market Trends

Enhanced Convenience Through AI and Voice Integration

- A significant and accelerating trend in the global edge-AI enabled diagnostic imaging devices market is the integration of edge computing and AI-based imaging algorithms directly into diagnostic equipment. This development is significantly enhancing the speed, accuracy, and efficiency of medical imaging, enabling real-time decision-making at the point of care

- For instance, in 2025, Siemens Healthineers launched edge-AI enabled MRI systems capable of automatically optimizing scan parameters based on patient anatomy, reducing the need for repeat imaging and improving diagnostic confidence. Similarly, Philips Healthcare introduced portable CT scanners with edge-AI features that allow immediate image reconstruction and analysis, supporting rapid diagnosis in emergency and critical care settings

- AI integration in these devices enables intelligent image processing, automated anomaly detection, and predictive analytics. For example, some edge-AI enabled ultrasound systems can detect subtle cardiovascular or obstetric abnormalities and provide real-time alerts to clinicians, improving patient outcomes. In addition, automated workflows reduce operator dependency and increase the throughput of diagnostic imaging centers

- The integration of edge-AI with diagnostic imaging platforms allows seamless connectivity with hospital information systems (HIS) and picture archiving and communication systems (PACS), enabling centralized storage, analysis, and retrieval of patient imaging data. This interoperability streamlines clinical workflows and enhances the overall efficiency of healthcare delivery

- This trend towards smarter, faster, and more connected diagnostic imaging devices is reshaping expectations for healthcare providers worldwide. Consequently, companies such as Canon Medical Systems and GE Healthcare are developing edge-AI enabled devices with enhanced real-time processing, automated imaging protocols, and improved diagnostic reliability

- The demand for edge-AI enabled diagnostic imaging devices is growing rapidly across hospitals, outpatient centers, and specialty clinics, as healthcare providers increasingly prioritize faster diagnosis, higher imaging accuracy, and improved operational efficiency

Edge-AI Enabled Diagnostic Imaging Devices Market Dynamics

Driver

Rising Need for Rapid and Accurate Diagnostics

- The global increase in chronic diseases, aging populations, and complex medical conditions is driving the adoption of edge-AI enabled imaging devices. Hospitals require faster and more precise diagnostics to improve treatment outcomes and patient satisfaction

- For instance, in 2025, Canon Medical Systems deployed edge-AI enabled CT scanners in several U.S. hospitals to accelerate cardiac imaging and reduce patient wait times, demonstrating real-world adoption of AI-powered diagnostic solutions

- The growing trend toward minimally invasive procedures also supports edge-AI imaging adoption, as surgeons rely on highly detailed imaging to plan and execute complex interventions

- Furthermore, increasing investment by private and public healthcare providers in modern imaging infrastructure is fueling market growth, especially in regions with rising healthcare expenditure

- Enhanced patient throughput and reduced imaging times are key benefits driving adoption, as edge-AI imaging devices allow multiple scans to be completed with higher accuracy and lower chances of errors, improving operational efficiency in busy hospital environments

- Edge-AI enabled devices are increasingly being used in specialized departments such as oncology and neurology, where precise imaging is critical for early detection, treatment planning, and monitoring disease progression, ultimately improving patient prognosis

- The ability to perform on-site, real-time diagnostics in emergency and critical care settings is also promoting adoption, as hospitals seek to reduce reliance on centralized imaging centers and provide immediate, actionable insights for urgent patient care

Restraint/Challenge

High Costs and Regulatory Complexity

- Edge-AI enabled diagnostic imaging devices are often expensive due to advanced hardware, software licensing, and continuous maintenance costs, limiting adoption in smaller clinics and low-resource settings

- For instance, high-end GE Healthcare edge-AI CT scanners can cost hundreds of thousands of dollars, which has delayed adoption in many hospitals in Southeast Asia and Latin America, highlighting the barrier of high capital expenditure

- Regulatory approval and compliance with international standards, such as FDA and CE marks, can slow the introduction of AI-based imaging devices. Ensuring that AI algorithms meet stringent clinical validation criteria adds complexity and delays time-to-market

- Healthcare providers may face challenges in staff training and workflow integration, as new devices require radiologists and technicians to adapt to AI-assisted imaging systems

- Interoperability issues with legacy hospital systems can hinder the full potential of edge-AI devices, requiring additional investments in IT infrastructure and software integration

- Addressing these barriers through cost-effective device models, simplified regulatory pathways, and clinician training programs will be critical for achieving widespread market adoption and sustainable growth

Edge-AI Enabled Diagnostic Imaging Devices Market Scope

The market is segmented on the basis of product type and application.

- By Product Type

On the basis of product type, the Edge-AI Enabled Diagnostic Imaging Devices market is segmented into wearable devices, portable devices, handheld devices, and other devices. The portable devices segment dominated the largest market revenue share of 38.7% in 2025, driven by their widespread adoption in hospitals and diagnostic centers due to the convenience of mobility and ease of use. Portable imaging devices allow clinicians to perform diagnostics at the point of care, significantly reducing patient wait times and enabling faster clinical decisions. Hospitals and specialty clinics increasingly deploy portable devices for cardiac, neurological, and oncology diagnostics due to their high accuracy and flexibility. The integration of Edge-AI enhances image processing, anomaly detection, and real-time decision support, further boosting adoption. Portable devices are often designed to be compatible with multiple imaging modalities such as ultrasound, X-ray, and CT, increasing their utility. Advancements in battery life, lightweight design, and connectivity with hospital IT systems support their popularity. Growing demand for telemedicine and remote diagnostics also drives segment expansion. Manufacturers are continuously innovating with improved image resolution, AI-assisted analytics, and cloud integration. The increasing prevalence of chronic diseases and the need for early diagnosis fuel market growth. The segment also benefits from supportive reimbursement policies in developed regions. Overall, portable devices remain the most widely adopted product type, dominating revenue in the market.

The wearable devices segment is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by rising demand for continuous patient monitoring and personalized diagnostics. Wearable imaging devices integrated with Edge-AI allow real-time monitoring of physiological parameters such as cardiac activity and neurological signals. The growing popularity of home-based diagnostics and remote patient monitoring is boosting adoption of wearable devices. Technological advancements in miniaturized imaging sensors and AI-assisted data processing improve usability and accuracy. Wearable devices are increasingly used in cardiology, neurology, and oncology for early detection and continuous monitoring. The rising prevalence of chronic diseases and the focus on preventive healthcare further support market expansion. Increasing patient awareness about personal health management encourages wearable device usage. Hospitals and specialty clinics are adopting these devices for outpatient care and follow-up diagnostics. Digital health platforms and telemedicine services integrate wearable imaging data for enhanced clinical insights. Pharmaceutical and medical device companies are investing in R&D to develop innovative, comfortable, and reliable wearable imaging devices. Supportive government initiatives for remote monitoring technologies in developed and emerging markets strengthen growth. The combination of mobility, AI-enhanced analytics, and patient-centered care makes wearable devices the fastest-growing product segment in this market.

- By Application

On the basis of application, the market is segmented into cardiology, oncology, neurology, radiology, pathology, and others. The cardiology segment accounted for the largest market revenue share of 29.4% in 2025, driven by the high prevalence of cardiovascular diseases worldwide and the critical need for early and accurate diagnostics. Edge-AI enabled devices allow real-time monitoring of heart function, early detection of arrhythmias, and improved diagnostic accuracy for heart-related conditions. Hospitals and cardiac care centers extensively adopt AI-integrated imaging solutions for point-of-care diagnostics and in-patient monitoring. The integration of AI enhances predictive analytics and automates interpretation of imaging results, reducing clinical workload and improving patient outcomes. Growing awareness of heart health, government initiatives for cardiovascular disease management, and rising healthcare expenditure drive the adoption of cardiac imaging devices. The segment also benefits from improved reimbursement policies in developed markets. Technological advances in portable and handheld cardiac imaging devices further support growth. The increasing focus on personalized medicine and preventive care reinforces demand. Edge-AI solutions provide real-time alerts, aiding clinicians in rapid decision-making. Collaboration between medical device manufacturers and healthcare providers expands the reach of cardiac diagnostics. Overall, cardiology remains the largest application segment, accounting for the highest revenue in the market.

The oncology segment is expected to witness the fastest CAGR of 11.9% from 2026 to 2033, driven by the increasing global cancer burden and the demand for early detection and precise monitoring of tumors. Edge-AI enabled imaging devices provide enhanced tumor detection, volumetric analysis, and treatment response assessment with improved accuracy and speed. Hospitals and oncology centers increasingly use portable and handheld imaging solutions for tumor monitoring, biopsy guidance, and therapy planning. The growing emphasis on personalized cancer care and precision medicine is boosting adoption of AI-integrated diagnostic imaging devices. Technological advancements in AI algorithms and imaging modalities enhance diagnostic reliability and reduce false positives. Rising government initiatives and healthcare investments in cancer screening programs support market expansion. Integration of devices with telemedicine platforms allows remote monitoring and consultation, particularly in underserved regions. Early detection and continuous monitoring improve patient survival rates, further driving demand. Oncology-focused Edge-AI devices are increasingly incorporated into multi-modal imaging workflows for comprehensive cancer care. Increasing collaborations between AI companies and healthcare providers accelerate innovation and adoption. Growing patient awareness and proactive health management contribute to market growth. The oncology segment is expected to grow rapidly and emerge as the fastest-growing application area in the Edge-AI enabled diagnostic imaging devices market.

Edge-AI Enabled Diagnostic Imaging Devices Market Regional Analysis

- North America dominated the edge-AI enabled diagnostic imaging devices market with the largest revenue share of 38.6% in 2025

- Characterized by advanced healthcare infrastructure, high adoption of AI-driven medical technologies, and the strong presence of leading medical imaging device manufacturers

- The market experienced significant growth in AI-integrated imaging systems across hospitals, diagnostic centers, and specialty clinics, driven by increasing demand for faster, more accurate diagnostics and improved patient outcomes

U.S. Edge-AI Enabled Diagnostic Imaging Devices Market Insight

The U.S. edge-AI enabled diagnostic imaging devices market accounted for the largest share within North America, driven by the rapid adoption of AI-powered imaging modalities, including MRI, CT, and ultrasound systems. Hospitals and diagnostic centers are increasingly integrating AI algorithms to enhance image accuracy, automate workflow, and reduce diagnostic time. Leading manufacturers such as GE Healthcare, Siemens Healthineers, and Philips Healthcare are investing heavily in AI-enabled solutions, which is further boosting market expansion. The focus on early disease detection, precision medicine, and improving patient care quality is propelling the demand for advanced imaging technologies.

Canada Edge-AI Enabled Diagnostic Imaging Devices Market Insight

Canada’s edge-AI enabled diagnostic imaging devices market is witnessing robust growth in AI-driven diagnostic imaging adoption, fueled by government healthcare investments, increasing diagnostic imaging volumes, and expanding AI research in healthcare institutions. Hospitals and imaging centers are progressively deploying AI-integrated systems to improve workflow efficiency, reduce radiologist workload, and enhance diagnostic accuracy. The growing emphasis on precision medicine and early detection of chronic and acute conditions is expected to support sustained market growth throughout the forecast period.

Europe Edge-AI Enabled Diagnostic Imaging Devices Market Insight

Europe edge-AI enabled diagnostic imaging devices market held a significant share in 2025, supported by a well-established healthcare system, high adoption of AI-enabled imaging technologies, and the strong presence of leading medical device manufacturers. Hospitals and diagnostic centers across Germany, France, and other EU countries are integrating AI solutions for faster, more precise diagnostics. The region’s emphasis on innovation, regulatory support for advanced medical technologies, and growing demand for digital healthcare solutions are fueling market growth.

U.K. Edge-AI Enabled Diagnostic Imaging Devices Market Insight

The U.K. edge-AI enabled diagnostic imaging devices market dominated the European market with the largest revenue share of 28.7% in 2025, driven by a robust healthcare infrastructure, widespread adoption of AI-powered imaging modalities, and the presence of specialized diagnostic centers. Hospitals and private diagnostic facilities are increasingly deploying AI-integrated MRI, CT, and X-ray systems to enhance imaging accuracy, workflow efficiency, and patient outcomes. The government’s initiatives promoting AI in healthcare and digital health programs further support market expansion.

Germany Edge-AI Enabled Diagnostic Imaging Devices Market Insight

Germany is expected to be the fastest growing country in Europe, with a projected CAGR of 9.2% during the forecast period. This growth is fueled by increasing healthcare expenditure, rising adoption of AI-based imaging systems across hospitals and diagnostic clinics, and strong support for innovative medical technologies. German healthcare providers prioritize precision, automation, and efficiency in imaging workflows, which drives the demand for advanced Edge-AI-enabled diagnostic imaging devices.

Asia-Pacific Edge-AI Enabled Diagnostic Imaging Devices Market Insight

The Asia-Pacific edge-AI enabled diagnostic imaging devices market is projected to register the fastest growth, driven by rising healthcare expenditure, urbanization, and the expansion of diagnostic imaging infrastructure in emerging economies. Countries like China, India, and Japan are investing heavily in AI-enabled medical devices to address increasing patient loads and improve diagnostic efficiency. In addition, initiatives promoting digital health and smart hospital technologies are accelerating the adoption of AI-based imaging solutions, particularly in hospitals, diagnostic centers, and specialty clinics.

China Edge-AI Enabled Diagnostic Imaging Devices Market Insight

China edge-AI enabled diagnostic imaging devices market dominated the APAC region in 2025, driven by rapid urbanization, expanding hospital networks, and growing adoption of AI-assisted imaging modalities. The strong presence of domestic manufacturers offering affordable AI-powered imaging solutions and government initiatives promoting smart hospitals and AI in healthcare are key factors contributing to the market’s growth.

India Edge-AI Enabled Diagnostic Imaging Devices Market Insight

India edge-AI enabled diagnostic imaging devices market is expected to be the fastest growing country in APAC, with hospitals and diagnostic centers increasingly adopting AI-based imaging systems to improve diagnostic accuracy and workflow efficiency. Growing awareness of advanced healthcare technologies, rising prevalence of chronic diseases, and investments in modern diagnostic infrastructure are driving the rapid uptake of Edge-AI Enabled Diagnostic Imaging Devices.

Edge-AI Enabled Diagnostic Imaging Devices Market Share

The Edge-AI Enabled Diagnostic Imaging Devices industry is primarily led by well-established companies, including:

- Assa Abloy (Sweden)

- GE Healthcare (U.S.)

- Siemens Healthineers (Germany)

- Philips Healthcare (Netherlands)

- Canon Medical Systems (Japan)

- Fujifilm Healthcare (Japan)

- Hologic (U.S.)

- Samsung Medison (South Korea)

- Mindray Medical (China)

- Hitachi Medical Systems (Japan)

- Shimadzu Corporation (Japan)

- Carestream Health (U.S.)

- Konica Minolta Healthcare (Japan)

- Esaote (Italy)

- Neusoft Medical Systems (China)

- Sectra AB (Sweden)

- PerkinElmer (U.S.)

- Agfa-Gevaert Group (Belgium)

- Varian Medical Systems (U.S.)

- Toshiba Medical (Japan)

- Kanghua Healthcare (China)

Latest Developments in Global Edge-AI Enabled Diagnostic Imaging Devices Market

- In October 2024, MedCognetics, Inc. introduced the first embedded AI cancer detection system for mammography imaging that integrates an NVIDIA IGX Orin medical‑grade edge AI platform with its CogNet AI‑MT software. This system enables real‑time image analysis and cancer detection directly within the mammography device, eliminating latency from external workstations and improving diagnostic speed and accuracy in breast imaging

- In March 2025, Siemens Healthineers launched AI‑powered MRI acceleration software designed to enhance image reconstruction speed and clarity, marking a notable advancement in integrated AI for clinical diagnostic imaging workflows. This technology is part of the broader AI‑centric product expansion improving diagnostic decision‑making in real time

- In May 2025, GE HealthCare launched CleaRecon DL, an AI‑enabled imaging enhancement platform for cone‑beam computed tomography (CBCT) that received both FDA 510(k) clearance and CE mark, highlighting regulatory acceptance for advanced AI diagnostic tools designed to improve image quality and diagnostic precision

- In July 2025, Philips Healthcare introduced the AI‑enabled CT 5300 system, part of its next‑generation imaging portfolio designed with integrated AI features to accelerate diagnosis and enhance imaging insight across multiple modalities, reinforcing the market’s shift toward embedded AI capabilities in diagnostic devices

- In July 2025, Quibim raised USD 50 million in a Series A funding round to accelerate its development of advanced imaging biomarker technologies that incorporate AI analysis and support diagnostic workflows across MRI and CT applications — reinforcing investment activity in edge‑AI diagnostic platforms

- In July 2025, Aidoc received a Breakthrough Device Designation from the U.S. FDA for its new multi‑triage AI solution (CARE1) that covers multiple acute findings in CT scans, indicating clinical validation for advanced AI algorithms integrated into real‑time imaging interpretation workflows

- In August 2025, Samsung India launched a new portfolio of mobile CT products (including AI‑powered mobile CT systems such as CereTom Elite and OmniTom Elite), designed to improve access to advanced diagnostic imaging with embedded AI and edge processing features for emergency departments, ICUs, and remote settings

- In November 2025, Samsung launched the next‑generation R20 ultrasound system with cutting‑edge artificial intelligence tools and enhanced image clarity to support general imaging diagnostics, emphasizing improved clinician experience and real‑time image analysis capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.