Global Edge Data Center Market

Market Size in USD Billion

USD

42.50 Billion

USD

131.82 Billion

2025

2033

USD

42.50 Billion

USD

131.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 42.50 Billion | |

| USD 131.82 Billion | |

| % | |

|

What is the Edge Data Center Market Size and Overview?

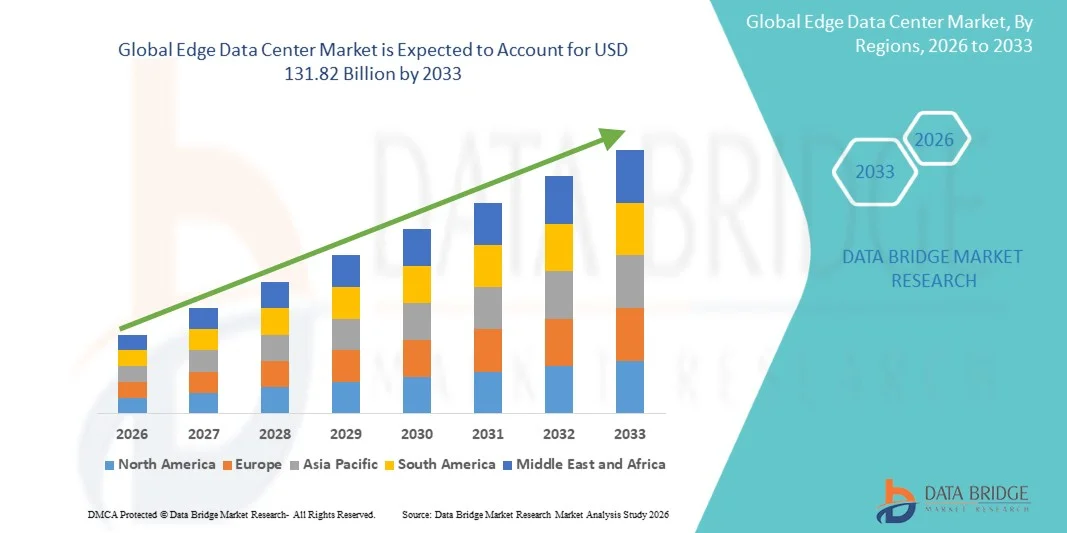

As per Data Bridge Market Research Analysis the Edge Data Center Market was valued at USD 42.5 Billion in 2025 and is projected to reach USD 131.82 Billion by 2033, growing at a CAGR of 15.20% from 2026 to 2033. The market is experiencing consistent growth driven by increasing deployment of 5G networks, rising adoption of IoT and AI enabled applications, and growing demand for low latency real time data processing across industries. Expanding investments in distributed computing infrastructure and increasing adoption of cloud edge architectures are further supporting market expansion across developed and emerging economies.

The increasing global focus on digital transformation and decentralized data processing, combined with rising demand for high speed connectivity and localized computing capabilities, is compelling enterprises to deploy edge data center infrastructure closer to end users and devices. Edge computing solutions are increasingly being utilized to support autonomous systems, smart manufacturing, cloud gaming, telemedicine, and real time analytics applications while improving operational efficiency and reducing network congestion. Continuous advancements in modular edge facilities, energy efficient cooling systems, and AI optimized infrastructure are further accelerating market growth globally.

Market Size & Forecast

- Global Market Value (2025): USD 42.5 Billion

- Expected Market Value (2033): USD 131.82 Billion

- Forecast CAGR (2026–2033): 15.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Edge Data Center Market with the largest revenue share of 36% in 2025, supported by strong adoption of edge computing infrastructure, rapid deployment of 5G networks, and increasing demand for low latency data processing across enterprises

- The solution segment led the market with 87.5% share in 2025, driven by increasing deployment of edge computing infrastructure, modular data center systems, edge servers, and intelligent cooling technologies across distributed enterprise environments

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 17.8% from 2026 to 2033, fueled by rapid urbanization, expanding internet penetration, and increasing adoption of digital services across emerging economies

- Services are the fastest-growing component type, projected to register a CAGR of 16% from 2026 to 2033, supported by rising demand for managed services, consulting, deployment, and maintenance support for distributed edge environments

- The large facility segment dominated the facility size category with a 61% revenue share in 2025, led by strong investments from hyperscale cloud providers, telecom operators, and large enterprises deploying high-capacity edge infrastructure

- IT and Telecom accounted for 34% of the market in 2025, preferred by rapid deployment of 5G networks, increasing internet traffic, and growing demand for ultra-low latency computing infrastructure

- The small and medium-sized facility segment is the fastest-growing category, with a CAGR of 14% from 2026 to 2033, driven by increasing adoption of localized edge infrastructure among small enterprises, retail operators, healthcare facilities, and remote industrial sites

Report Scope and Edge Data Center Market Segmentation

|

Attributes |

Edge Data Center Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

What is the Key Trend in the Edge Data Center Market?

Trend: Rising AI and 5G Edge Integration

The rapid expansion of AI powered applications and 5G connectivity is significantly accelerating deployment of edge data center infrastructure across global markets. Enterprises are increasingly investing in distributed edge computing systems to support real time analytics, autonomous technologies, cloud gaming, video streaming, and industrial IoT applications requiring ultra low latency processing. The growing rollout of 5G networks is further increasing demand for localized data processing and decentralized storage capabilities to reduce network congestion and improve application responsiveness. Advancements in modular edge facilities, AI optimized servers, and edge orchestration platforms are also strengthening infrastructure scalability and operational efficiency.

Companies such as Cisco Systems introduced its Unified Edge platform in November 2025 to integrate compute, storage, and networking capabilities into a single AI ready edge infrastructure platform, supporting real time AI inferencing and distributed edge deployments across enterprise and telecom environments.

Edge Data Center Market Dynamics

Key Market Driver: Growing Demand for Low Latency Processing

The increasing need for real time data processing and ultra low latency connectivity is significantly driving demand for edge data center infrastructure across industries. Enterprises are increasingly deploying localized computing facilities closer to end users and connected devices to support AI applications, industrial automation, autonomous mobility, telemedicine, and immersive digital experiences. Growing adoption of IoT ecosystems and expansion of 5G networks are further accelerating investments in decentralized computing environments capable of processing high volumes of data efficiently. Rising dependence on cloud gaming, video analytics, and smart manufacturing applications is also strengthening the requirement for edge computing capabilities globally.

Major companies such as Amazon Web Services, Equinix, and Digital Realty are expanding edge infrastructure investments to support enterprise demand for real time cloud services, low latency connectivity, and distributed digital operations across telecom, healthcare, and industrial sectors.

Key Restraint/Challenge: High Infrastructure Deployment and Operational Costs

A major challenge in the Edge Data Center market is the high capital investment required for deploying and maintaining distributed edge infrastructure across multiple geographic locations. Edge facilities require substantial expenditure on advanced networking equipment, modular data center systems, cooling infrastructure, edge servers, cybersecurity technologies, and power management solutions. Complex deployment environments, rising energy consumption, and increasing operational maintenance costs further add to infrastructure management challenges for enterprises and service providers. In addition, ensuring data security, scalability, and seamless connectivity across decentralized edge networks significantly increases implementation complexity and operational expenditure.

The expansion of AI focused edge infrastructure projects by major operators such as Dell Technologies and Schneider Electric in 2025 highlights the significant investment requirements associated with deploying scalable and energy efficient edge computing facilities capable of supporting high density AI workloads.

Key Market Opportunity: Growing Adoption of Edge AI in Industrial Automation

The increasing adoption of Edge AI technologies across industrial automation and smart manufacturing environments is creating significant growth opportunities for the Edge Data Center market. Manufacturers are increasingly deploying AI enabled edge infrastructure to support predictive maintenance, machine vision, robotics, real time analytics, and connected production systems requiring instant data processing capabilities. The integration of edge computing with industrial IoT and private 5G networks is improving operational efficiency, reducing downtime, and enabling intelligent factory automation across manufacturing facilities. Advancements in AI accelerated edge servers and compact modular data center solutions are also improving deployment flexibility and scalability for industrial applications.

Companies such as Veea and Vapor IO announced a strategic collaboration in February 2025 to deliver AI as a Service and federated learning solutions through private 5G enabled edge infrastructure designed for smart manufacturing and multi site enterprise environments, accelerating adoption of industrial edge AI ecosystems globally.

Edge Data Center Market Scope

The edge data center market is segmented on the basis of component, facility size, and end use.

- By Component

On the basis of component, the Edge Data Center Market is segmented into solution and services. The Solution segment dominated the market with the largest share of 87.5% in 2025, driven by increasing deployment of edge computing infrastructure, modular data center systems, edge servers, and intelligent cooling technologies across distributed enterprise environments. Organizations are heavily investing in edge solutions to support low-latency data processing, real-time analytics, and localized workload management for IoT, AI, and 5G applications. Rising adoption of smart city infrastructure and industrial automation is further accelerating demand for integrated edge hardware and software platforms. The segment also benefits from growing investments in hyperscale edge expansion by cloud and telecom providers. Continuous advancements in edge security, power management, and network optimization technologies are strengthening market dominance across major industries.

The Services segment is projected to register the fastest growth at a CAGR of 16% from 2026 to 2033, driven by rising demand for managed services, consulting, deployment, and maintenance support for distributed edge environments. Enterprises increasingly require specialized expertise to handle complex edge infrastructure integration, cybersecurity management, and remote monitoring operations. Growing adoption of hybrid cloud-edge architectures is further increasing the need for professional support services to ensure operational efficiency and scalability. Service providers are expanding offerings focused on predictive maintenance, edge orchestration, and lifecycle management to address evolving enterprise requirements. Increasing focus on minimizing downtime and improving edge network reliability is significantly accelerating service adoption across telecom, manufacturing, and retail sectors.

- By Facility Size

On the basis of facility size, the Edge Data Center Market is segmented into large facility and small and medium-sized facility. The Large Facility segment dominated the market with a share of 61% in 2025, supported by strong investments from hyperscale cloud providers, telecom operators, and large enterprises deploying high-capacity edge infrastructure. These facilities offer advanced computing capabilities, enhanced storage capacity, and high-performance connectivity required to process massive volumes of real-time data. Large facilities are increasingly utilized for AI workloads, content delivery, and enterprise edge applications requiring scalable and secure infrastructure. Their ability to support multi-tenant operations and regional edge distribution strengthens adoption across urban and industrial hubs. Expansion of 5G infrastructure and rising demand for high-density computing environments are further reinforcing segment dominance.

The Small and Medium-Sized Facility segment is projected to register the fastest growth at a CAGR of 14% from 2026 to 2033, driven by increasing adoption of localized edge infrastructure among small enterprises, retail operators, healthcare facilities, and remote industrial sites. These facilities provide cost-effective and flexible deployment models suitable for low-latency applications and decentralized computing requirements. Growing demand for compact modular data centers and micro edge facilities is enabling rapid deployment in underserved and rural areas. Advancements in energy-efficient cooling systems and prefabricated edge solutions are improving operational efficiency and scalability for smaller facilities. Rising emphasis on real-time processing and localized digital transformation initiatives is accelerating growth across emerging markets and regional enterprises.

- By End Use

On the basis of end use, the Edge Data Center Market is segmented into IT and telecom, BFSI, healthcare and lifesciences, manufacturing & automotive, government, gaming and entertainment, retail and e-commerce, and others. The IT and Telecom segment dominated the market with the largest share of 34% in 2025, driven by rapid deployment of 5G networks, increasing internet traffic, and growing demand for ultra-low latency computing infrastructure. Telecom operators are heavily investing in edge data centers to support real-time communication, cloud gaming, video streaming, and AI-driven network optimization. Rising adoption of distributed cloud architecture and network virtualization technologies is further strengthening edge infrastructure expansion across telecom ecosystems. The segment also benefits from increasing demand for localized content delivery and faster data processing capabilities. Continuous expansion of connected devices and IoT applications is reinforcing the leadership position of the IT and telecom sector.

The Healthcare and Lifesciences segment is projected to register the fastest growth at a CAGR of 13% from 2026 to 2033, driven by increasing adoption of real-time patient monitoring, telemedicine platforms, AI-assisted diagnostics, and connected medical devices. Healthcare providers are deploying edge data centers to process sensitive patient data locally while ensuring low latency and regulatory compliance. Rising demand for rapid clinical data analysis and remote healthcare delivery is accelerating adoption of decentralized computing infrastructure across hospitals and research institutions. Advancements in medical IoT, wearable technologies, and edge-enabled imaging systems are further improving operational efficiency and patient outcomes. Growing investments in digital healthcare transformation and smart hospital infrastructure are significantly supporting segment expansion globally.

Edge Data Center Market Regional Analysis

North America dominated the edge data center market and accounted for the largest revenue share of 36% in 2025, driven by strong adoption of edge computing infrastructure, rapid deployment of 5G networks, and increasing demand for low latency data processing across enterprises. The region benefits from advanced cloud infrastructure, high concentration of hyperscale data center operators, and growing investments in AI, IoT, and real time analytics technologies. Enterprises across telecom, healthcare, retail, and manufacturing sectors are increasingly deploying edge facilities to support decentralized workloads and improve operational efficiency. In addition, strong investments in smart city development and autonomous technologies continue to reinforce North America’s leadership position in the global market.

U.S. Edge Data Center Market Insight

The U.S. Edge Data Center market is experiencing strong growth driven by rising deployment of 5G infrastructure, increasing adoption of AI enabled applications, and growing demand for real time data processing capabilities. Enterprises are heavily investing in localized edge infrastructure to support cloud gaming, connected devices, autonomous systems, and digital transformation initiatives across industries. The country’s strong hyperscale cloud ecosystem and presence of leading technology providers are enabling rapid deployment of advanced edge computing solutions. In addition, increasing investments in smart manufacturing, healthcare digitization, and edge AI platforms are further accelerating market expansion across the U.S.

Canada Edge Data Center Market Insight

The Canada Edge Data Center market is witnessing steady growth supported by increasing investments in digital infrastructure and rising adoption of cloud and edge computing technologies across enterprises. Businesses across telecom, retail, and financial services sectors are increasingly deploying edge facilities to improve data processing speed and reduce network latency. The country’s growing focus on smart city projects and connected infrastructure is further encouraging adoption of decentralized data center solutions. In addition, rising demand for secure and energy efficient edge facilities is contributing to market growth in Canada.

Europe Edge Data Center Market Insight

The Europe Edge Data Center market is expanding steadily due to increasing digital transformation initiatives, strong focus on data sovereignty, and rising deployment of edge computing infrastructure across industries. The region benefits from advanced telecommunications networks, growing adoption of Industry 4.0 technologies, and increasing demand for low latency cloud services. Enterprises across automotive, manufacturing, healthcare, and retail sectors are actively investing in edge facilities to support real time analytics and connected operations. Rising emphasis on energy efficient data center solutions and sustainable digital infrastructure continues to support regional market growth

U.K. Edge Data Center Market Insight

The U.K. Edge Data Center market is growing steadily, driven by rapid expansion of 5G connectivity, increasing cloud adoption, and strong demand for low latency digital services. Enterprises are increasingly deploying edge facilities to support financial services, e commerce, media streaming, and AI driven applications. The presence of a mature digital ecosystem and rising investments in smart infrastructure projects are further supporting market expansion. In addition, growing adoption of edge enabled IoT and real time analytics platforms is strengthening demand across the U.K.

Germany Edge Data Center Market Insight

The Germany Edge Data Center market is expanding due to strong industrial automation, increasing deployment of connected manufacturing systems, and rising adoption of Industry 4.0 technologies. Enterprises across automotive, industrial, and logistics sectors are increasingly leveraging edge infrastructure to enable real time monitoring and operational efficiency. The country’s strong emphasis on data security and advanced engineering capabilities is driving adoption of localized and highly secure edge facilities. In addition, growing investments in AI powered industrial applications and smart factory infrastructure are further accelerating market development in Germany.

Asia-Pacific Edge Data Center Market Insight

The Asia-Pacific Edge Data Center market is expected to register the fastest growth with a CAGR of 17.8% from 2026 to 2033, driven by rapid urbanization, expanding internet penetration, and increasing adoption of digital services across emerging economies. Growing deployment of 5G networks and rising demand for cloud gaming, video streaming, and IoT applications are significantly boosting edge infrastructure investments. Countries such as China, India, Japan, and South Korea are witnessing strong expansion of smart city initiatives and digital transformation programs. In addition, increasing investments by hyperscale cloud providers and telecom companies are further accelerating regional market growth.

Japan Edge Data Center Market Insight

The Japan Edge Data Center market is witnessing steady growth supported by strong technology adoption, increasing deployment of connected infrastructure, and rising demand for real time data processing solutions. Enterprises are investing in edge facilities to support AI applications, industrial automation, autonomous mobility, and advanced telecommunications services. The country’s highly developed digital infrastructure and focus on automation technologies are further supporting market expansion. In addition, growing adoption of smart manufacturing and edge enabled robotics is strengthening demand in Japan.

China Edge Data Center Market Insight

The China Edge Data Center market is growing rapidly due to large scale 5G deployment, rising cloud computing adoption, and strong expansion of AI and IoT ecosystems. Enterprises are actively investing in edge infrastructure to support smart manufacturing, digital commerce, autonomous systems, and real time analytics applications. The country’s strong digital economy and extensive investments in data infrastructure are enabling rapid deployment of distributed edge facilities. In addition, increasing focus on smart city development and localized data processing capabilities is further driving market growth in China.

Which are the Top Companies in Edge Data Center Market?

The edge data center industry is primarily led by well-established companies, including:

- Equinix, Inc. (U.S.)

- Fujitsu Limited (Japan)

- American Tower Corporation (U.S.)

- Lenovo Group Limited (China)

- Cisco Systems, Inc. (U.S.)

- NTT Ltd. (Japan)

- Dell Inc. (U.S.)

- AtlasEdge Data Centres (U.K.)

- Schneider Electric SE (France)

- Digital Realty Trust, Inc. (U.S.)

- Amazon Web Services (AWS) (U.S.)

- Vapor IO, Inc. (U.S.)

- Google LLC (U.S.)

- Vertiv Holdings Co. (U.S.)

- DartPoints (U.S.)

- Huawei Technologies Co., Ltd. (China)

- 365 Data Centers (U.S.)

- Hewlett Packard Enterprise Company (U.S.)

- Flexential Corporation (U.S.)

- EdgeConneX Inc. (U.S.)

Latest Developments in Edge Data Center Market

- In November 2025, Cisco Systems Inc. launched its Unified Edge platform to extend data center capabilities to edge environments, enabling real-time applications and AI inferencing at the point of data generation. Positioned as a first-to-market solution, it integrates compute, networking, and storage into a single system supported by a broad partner ecosystem, delivering modular, AI-ready performance. The platform also streamlines large-scale deployments, offers end-to-end observability, and embeds security across all layers to safeguard distributed edge infrastructure. This development is strengthening the Edge Data Center market by improving operational scalability, enhancing distributed workload management, and enabling enterprises to deploy secure and intelligent edge infrastructure more efficiently

- In June 2025, Schneider Electric introduced advanced EcoStruxure modular edge and AI data center solutions designed to support high density AI workloads and accelerated computing environments. The launch included prefabricated modular pod infrastructure, liquid cooling integration, and AI optimized rack systems that improve scalability, deployment speed, and energy efficiency for distributed edge facilities. This development is strengthening the Edge Data Center market by enabling enterprises to deploy compact and sustainable edge infrastructure capable of handling real time AI processing and decentralized computing requirements. It is also accelerating adoption of next generation edge architectures across telecom, hyperscale cloud, and industrial sectors

- In June 2025, Schneider Electric expanded its strategic collaboration with NVIDIA to develop AI ready edge and data center infrastructure solutions focused on advanced cooling, power distribution, and high density rack systems. The partnership introduced new reference architectures and NVIDIA enabled rack solutions aimed at supporting scalable AI factories and distributed edge computing deployments. This development is significantly impacting the Edge Data Center market by improving infrastructure efficiency, reducing deployment complexity, and supporting rapid expansion of AI workloads at the edge. The collaboration is also encouraging wider enterprise investments in energy efficient and sustainable edge computing ecosystems

- In May 2025, Dell unveiled its AI Factory and expanded PowerEdge and PowerScale hardware portfolio to support AI workloads across both core and edge environments. The company also announced partnerships with Google Gemini for on-prem AI deployment and Cohere for secure AI integration, emphasizing decentralized computing and sustainable infrastructure innovation. This development is accelerating growth in the Edge Data Center market by enabling enterprises to process AI workloads closer to end users while improving infrastructure flexibility, energy efficiency, and real time analytics capabilities across distributed environments

- In February 2025, Veea and Vapor IO launched a strategic collaboration to deliver turnkey AI-as-a-Service and federated learning solutions leveraging Vapor IO’s Zero Gap AI platform and private 5G infrastructure for smart manufacturing, municipal projects, and multi-site enterprises. The collaboration focuses on enabling low latency AI processing and decentralized intelligence at the network edge. This development is positively impacting the Edge Data Center market by expanding adoption of edge AI platforms, strengthening private 5G enabled infrastructure deployment, and supporting real time industrial and smart city applications across distributed enterprise environments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.