Global Ehrlichiosis Treatment Market

Market Size in USD Billion

USD

85.50 Billion

USD

139.39 Billion

2025

2033

USD

85.50 Billion

USD

139.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 85.50 Billion | |

| USD 139.39 Billion | |

| % | |

|

Ehrlichiosis Treatment Market Size

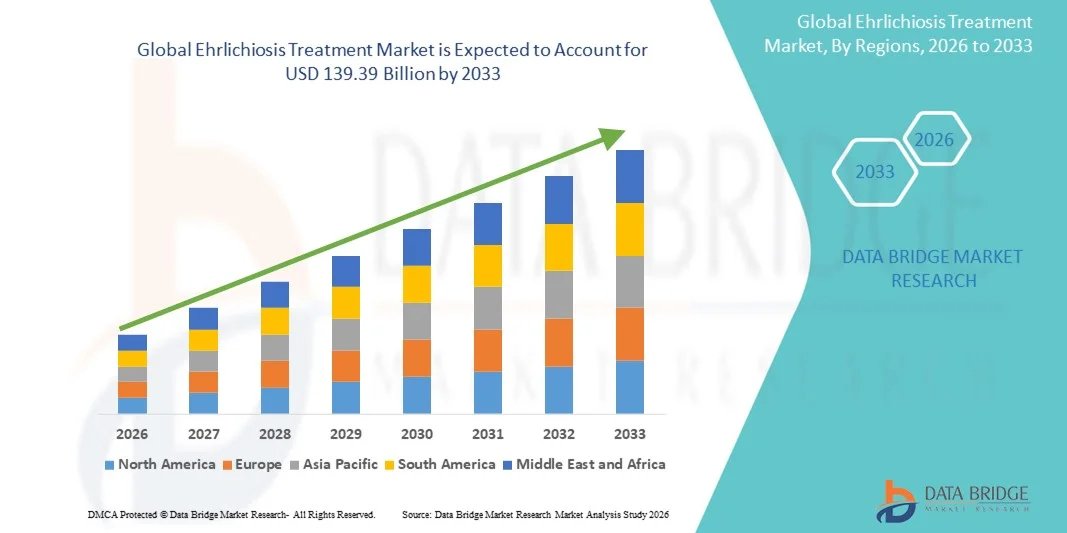

- The global Ehrlichiosis Treatment market size was valued at USD 85.50 billion in 2025 and is expected to reach USD 139.39 billion by 2033, at a CAGR of 6.30% during the forecast period

- The market growth is largely fueled by increasing awareness of tick-borne diseases, advancements in diagnostic technologies, and expansion of healthcare infrastructure in both urban and rural settings

- Furthermore, rising demand for effective, accessible, and timely treatment options is establishing Ehrlichiosis therapies as a critical component of infectious disease management. These converging factors are accelerating the uptake of Ehrlichiosis Treatment solutions, thereby significantly boosting the industry's growth

Ehrlichiosis Treatment Market Analysis

- Ehrlichiosis treatments, including antibiotics and supportive care, are increasingly vital components of modern healthcare for both children and adults due to their effectiveness, accessibility, and integration with advanced diagnostic and treatment protocols

- The escalating demand for ehrlichiosis treatments is primarily fueled by rising disease awareness, improved healthcare access, and a growing preference for early detection and standardized treatment regimens, ensuring better patient outcomes and reducing complications

- North America dominated the ehrlichiosis treatment market with the largest revenue share of 39% in 2025, supported by robust healthcare infrastructure, high disease awareness, widespread access to antibiotics, and specialized treatment centers. The U.S. leads the region due to early detection programs, extensive diagnostic capabilities, and strong healthcare spending

- Asia-Pacific is expected to be the fastest growing region in the ehrlichiosis treatment market during the forecast period, projected to grow at a CAGR of 8.5% from 2026 to 2033, driven by increasing incidence of the disease, expansion of healthcare access, development of diagnostic and treatment facilities, and government initiatives promoting early detection and prevention in countries such as China, India, Japan, and South Korea

- The Tick Bites segment dominated the largest market revenue share of 62.1% in 2025, reflecting the high prevalence of Ehrlichiosis transmission through vectors in endemic regions

Report Scope and Ehrlichiosis Treatment Market Segmentation

|

Attributes |

Ehrlichiosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ehrlichiosis Treatment Market Trends

Growing Awareness and Early Diagnosis Initiatives

- A significant and accelerating trend in the global ehrlichiosis treatment market is the increasing focus on early detection and awareness campaigns, especially in endemic regions. Government and non-government health organizations are actively promoting education about tick-borne infections, including symptoms, risk factors, and prevention measures

- For instance, public health initiatives in the United States and parts of Europe have implemented tick surveillance programs and awareness drives, helping healthcare providers identify suspected Ehrlichiosis cases sooner

- Advancements in diagnostic methods, such as PCR testing and serological assays, are supporting timely identification and improving patient outcomes

- Healthcare providers are increasingly integrating early screening protocols in routine check-ups for at-risk populations, including forestry workers, farmers, and outdoor enthusiasts

- Enhanced physician awareness and patient education are leading to faster reporting and reduced complications from delayed treatment

- Awareness campaigns coupled with digital platforms, mobile health apps, and teleconsultation services are helping patients seek care promptly

- This trend is fostering the adoption of effective treatment regimens, strengthening the overall market growth trajectory

Ehrlichiosis Treatment Market Dynamics

Driver

Rising Prevalence and Improved Access to Targeted Therapies

- The growing prevalence of Ehrlichiosis, driven by expanding tick habitats and climate change, is a significant driver of market growth. Areas with rising tick populations are witnessing increased infection rates, emphasizing the need for effective treatment solutions

- For instance, in 2023, several U.S. states reported a 15% increase in reported Ehrlichiosis cases compared to 2021, highlighting an urgent need for antibiotic therapies and supportive care

- Increased healthcare accessibility, particularly in rural and endemic regions, allows timely administration of standard antibiotics such as doxycycline, improving patient outcomes

- Healthcare initiatives supporting prophylactic and therapeutic interventions contribute to higher treatment adoption rates. Rising awareness among clinicians regarding best practices for managing moderate to severe Ehrlichiosis cases is further promoting the use of approved therapeutic regimens

- The combination of epidemiological growth and enhanced therapy accessibility continues to drive sustained market expansion

Restraint/Challenge

Diagnostic Challenges and High Treatment Costs

- Challenges in accurate and timely diagnosis remain a significant restraint in the Ehrlichiosis Treatment market. The non-specific nature of early symptoms, such as fever, headache, and malaise, often leads to misdiagnosis or delayed treatment

- For instance, a 2022 report from a regional hospital highlighted several cases initially misdiagnosed as influenza, which led to delayed antibiotic therapy and increased complication rates

- The relatively high cost of some advanced diagnostics, such as PCR and multiplex assays, can limit adoption, particularly in low-resource settings

- Although doxycycline remains affordable, supportive care for severe cases, including hospitalization or intravenous therapy, can be expensive, affecting overall treatment accessibility

- Healthcare systems are working to mitigate these challenges through training programs for physicians, subsidized diagnostics, and awareness campaigns to ensure timely identification and management of Ehrlichiosis

- Overcoming these diagnostic and cost-related barriers is crucial to improving patient outcomes and supporting long-term market growth

Ehrlichiosis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, transmission, dosage, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Ehrlichiosis Treatment market is segmented into Doxycycline, Rifampin, and Others. The Doxycycline segment dominated the largest market revenue share of 57.4% in 2025, driven by its long-standing recognition as the first-line therapy for Ehrlichiosis. Doxycycline is widely used due to its effectiveness against a broad range of Ehrlichia species, safety in adult and pediatric patients, and ease of oral administration. Hospitals, clinics, and endemic region healthcare centers adopt Doxycycline as part of standard treatment protocols. It is included in WHO and CDC guidelines, further solidifying its market dominance. High patient compliance, favorable pharmacokinetics, and well-established dosing regimens contribute to sustained adoption. The availability of generic formulations ensures affordability, while government programs and NGO campaigns promote awareness and timely treatment. Its efficacy in both prophylactic and acute treatment, combined with minimal adverse effects, reinforces preference. Doxycycline’s role in reducing complications, hospitalizations, and severe cases strengthens its position. Physician familiarity, clinical trial evidence, and regional guideline incorporation all support the segment’s continued leadership. Awareness campaigns in rural areas, training for healthcare professionals, and inclusion in treatment bundles further expand market penetration. Community outreach and public health monitoring also drive widespread adoption in high-risk zones.

The Rifampin segment is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, driven by increasing demand in doxycycline-resistant cases, severe infections, and immunocompromised patients. Rifampin’s adoption is growing due to its complementary use in combination therapy and its effectiveness in hospital and clinic settings. Rising awareness of alternative treatment options and clinical guideline updates contribute to accelerating market penetration. Specialty hospitals and infectious disease centers are increasingly integrating Rifampin into treatment protocols. Its efficacy in co-infections, favorable clinical outcomes, and inclusion in treatment algorithms enhance demand. Emerging research, government approvals, and expanded availability in developed and emerging countries support growth. Pharmaceutical companies are introducing optimized formulations for faster administration and better patient adherence. Hospitals prioritize intravenous Rifampin for severe cases, while outpatient use is growing in controlled programs. Awareness campaigns targeting high-risk populations further drive adoption. Global and regional conferences on tick-borne diseases highlight Rifampin’s role, increasing physician knowledge and recommendation rates.

- By Diagnosis

On the basis of diagnosis, the market is segmented into Serology, Blood Tests, Complete Blood Count (CBC), Indirect Immunofluorescent Assay (IFA), Polymerase Chain Reaction (PCR), and Others. The PCR segment dominated the largest market revenue share of 45.8% in 2025, due to its ability to detect Ehrlichia DNA rapidly with high specificity and sensitivity. PCR enables early detection, reduces misdiagnosis, and allows timely initiation of treatment, which is critical for preventing severe complications. Hospital laboratories, reference centers, and research institutions widely adopt PCR, further consolidating dominance. The test is essential in outbreak investigations, epidemiological studies, and surveillance programs, enhancing its credibility. Its automation, high throughput, and multiplexing capabilities support large-scale testing in endemic regions. National guidelines and physician training programs recommend PCR as the gold standard for confirmation. The integration of PCR into routine diagnostic protocols increases reliability and patient trust. Cost reductions, standardized kits, and international support programs strengthen accessibility. Adoption is particularly high in urban hospitals and centers with advanced laboratory infrastructure. Clinical evidence supporting rapid symptom resolution encourages continuous use. Point-of-care PCR testing in mobile labs is expanding, reinforcing the segment’s market leadership.

The IFA segment is expected to witness the fastest CAGR of 18.2% from 2026 to 2033, fueled by increased use in epidemiological studies, seroprevalence surveys, and confirmatory testing. IFA is particularly useful in field diagnostics and mobile healthcare units, allowing early identification and management. Government initiatives, NGO programs, and awareness campaigns are promoting IFA adoption in remote and rural areas. Standardized IFA kits, combined with training for laboratory technicians, improve testing accuracy and consistency. Hospitals and clinics are increasingly integrating IFA into secondary diagnostic workflows. Its cost-effectiveness, reliability, and compatibility with existing lab infrastructure contribute to fast adoption. Clinical guidelines and physician familiarity accelerate integration into routine practice. IFA is being promoted for both surveillance and diagnostic purposes in endemic regions. Community outreach and public health programs highlight its rapid utility, driving awareness. Increased laboratory capacity, improved reporting systems, and NGO support enhance penetration. IFA adoption complements PCR and serology, providing a robust diagnostic toolkit.

- By Transmission

On the basis of transmission, the market is segmented into Tick Bites, Blood Transfusion, and Organ Transplant. The Tick Bites segment dominated the largest market revenue share of 62.1% in 2025, reflecting the high prevalence of Ehrlichiosis transmission through vectors in endemic regions. Rural populations, agricultural workers, and forest laborers are most exposed, driving demand for early treatment and prophylaxis. Tick awareness campaigns, government preventive programs, and public education initiatives reinforce market dominance. Hospitals and clinics prioritize early intervention following tick bites, which supports rapid diagnosis and treatment initiation. Tick-borne transmission remains a primary focus of national surveillance and disease control programs. Seasonal outbreak management strategies further drive awareness and treatment adoption. Physician guidelines emphasize prophylactic and early therapeutic measures for exposed individuals. Rapid diagnosis and immediate access to antibiotics contribute to the segment’s strength. Research on tick ecology, control programs, and environmental monitoring supports preventive healthcare measures. Regional programs targeting endemic hot spots enhance patient access to effective treatment. Public health policies and educational outreach encourage early medical consultation, reinforcing sustained adoption.

The Blood Transfusion segment is expected to witness the fastest CAGR of 14.7% from 2026 to 2033, driven by increased awareness of transfusion-transmitted Ehrlichiosis, adoption of stringent screening protocols, and regulatory mandates. Blood banks, hospitals, and specialized clinics are implementing enhanced testing protocols to prevent infection spread. Government guidelines and hospital policies promote monitoring of blood products. Clinician education programs highlight transfusion-associated risks and drive early intervention. Standardized testing and inclusion in hospital workflows accelerate adoption. Research and reporting of transfusion-related cases enhance clinical awareness. Regional regulations in Europe, North America, and Asia-Pacific increase compliance. Awareness campaigns and professional training programs support growth. Continuous monitoring of donor blood and reporting mechanisms drive trust in transfusion safety. Expansion of hospital-based blood services and adoption of advanced testing kits contribute to faster market growth.

- By Dosage

On the basis of dosage, the market is segmented into Injection, Tablet, and Others. The Tablet segment dominated the largest market revenue share of 51.3% in 2025, driven by patient convenience, easy administration, and suitability for outpatient treatment. Tablets reduce the need for hospitalization and support adherence in long-term therapy, particularly in endemic regions. National eradication programs, physician recommendations, and community awareness campaigns reinforce market dominance. Tablets are widely distributed in retail pharmacies, clinics, and public health programs. Cost-effectiveness, oral bioavailability, and inclusion in guideline-based therapy enhance adoption. Patient compliance, minimal invasiveness, and widespread availability further strengthen the segment. Clinical studies confirming efficacy and safety boost confidence among healthcare providers. Tablets facilitate early treatment initiation and reduce the burden on hospitals. Endemic regions benefit from community-based distribution of oral therapy. Pharmaceutical companies are expanding production and distribution, ensuring consistent supply. Integration with public health campaigns and awareness drives reinforces widespread adoption.

The Injection segment is expected to witness the fastest CAGR of 15.8% from 2026 to 2033, driven by hospital-based treatment for severe cases and intravenous therapy protocols. Injection therapy is critical for patients with acute, complicated, or immunocompromised presentations. Hospitals are expanding infusion infrastructure, training staff, and integrating protocols into standard care. Severe case prevalence, guideline updates, and physician preference support faster adoption. Insurance coverage, hospital readiness, and clinical trial evidence strengthen growth. The need for rapid therapeutic delivery in high-risk patients accelerates market penetration. Intravenous therapy ensures precise dosing and treatment monitoring. Research supporting injection efficacy reinforces clinical confidence. Hospital protocols emphasize injections for severe or refractory infections. Increased awareness of severe Ehrlichiosis manifestations drives demand. Multi-center adoption and national guideline inclusion further enhance expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into Intravenous, Oral, and Others. The Oral route dominated the largest market revenue share of 53.9% in 2025, due to convenience, accessibility, and outpatient suitability. Oral administration reduces hospitalization needs and increases patient adherence. Community-based programs, public awareness, and guideline integration strengthen dominance. Oral therapy is the standard for mild to moderate infections and for continuation of therapy post-hospitalization. Physician recommendation, patient preference, and cost-effectiveness support adoption. Availability in rural pharmacies and healthcare centers improves access. Clinical evidence confirms efficacy and safety for oral administration. Treatment adherence programs and patient education enhance usage. Health systems promote oral therapy to reduce healthcare costs. Standardized dosing, widespread availability, and integration into public health campaigns drive continued dominance. Pharmaceutical supply chains ensure consistent distribution in endemic areas.

The Intravenous route is expected to witness the fastest CAGR of 16.2% from 2026 to 2033, fueled by the treatment of severe cases requiring hospital supervision. Hospitals adopt IV therapy protocols for acute infections, ensuring rapid response and monitoring. Increased severe case prevalence, guideline inclusion, and ICU readiness support growth. Infusion infrastructure expansion, staff training, and clinical evidence reinforce adoption. National programs and outbreak management strategies highlight IV therapy. Insurance coverage, emergency care readiness, and hospital capacity enhance implementation. Adoption in urban and tertiary care hospitals is expanding. Critical care protocols, high patient compliance, and standardized treatment guidelines further accelerate growth. Pharmaceutical companies are improving IV formulations for stability and efficacy. Research studies confirm IV therapy benefits for severe cases, supporting clinical adoption.

- By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. Hospitals dominated the largest market revenue share of 56.5% in 2025, due to availability of trained staff, diagnostic infrastructure, ICU facilities, and management of severe cases. Hospitals integrate national reporting programs, eradication initiatives, and standardized patient care. Acute case management, IV therapy, and monitoring of eradication therapy strengthen dominance. Insurance coverage, guideline adherence, and centralized care enhance adoption. Hospitals serve as referral centers, emergency care hubs, and diagnostic leaders. Training programs, staff expertise, and clinical protocol integration reinforce position. High patient volume, infrastructure, and specialty services drive continued leadership. Regional hospitals in endemic areas contribute heavily to market share. Public health monitoring and hospital-based awareness campaigns further strengthen adoption.

The Clinics segment is expected to witness the fastest CAGR of 17.4% from 2026 to 2033, driven by the expansion of outpatient care, patient follow-up, rapid diagnostics, and early-stage treatment. Clinics are increasingly administering oral therapy, conducting awareness campaigns, and supporting adherence programs. Community health initiatives and NGO collaborations support adoption. Clinics facilitate access in semi-urban and rural areas, expanding reach. Physician training, rapid testing integration, and patient education enhance effectiveness. Expansion of private clinic networks in endemic regions drives growth. Telemedicine integration and mobile healthcare services increase adoption. Clinics are key in early detection, monitoring, and preventive care. Increased patient awareness and outreach programs promote clinic visits. Local pharmacies and healthcare partnerships reinforce service delivery.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Retail Pharmacy segment dominated the largest market revenue share of 48.2% in 2025, due to accessibility, local presence, patient familiarity, and consistent availability of antibiotics. Retail pharmacies improve adherence through counseling, refill programs, and trusted local services. Urban and semi-urban penetration strengthens dominance. Integration with national programs, insurance, and public health campaigns enhance usage. Consistent supply chains, community trust, and availability of generics support adoption. Retail pharmacies serve as primary access points in endemic regions. Awareness campaigns and pharmacist-led guidance reinforce preference. Pharmaceutical distribution networks strengthen presence. Accessibility in remote and suburban areas enhances patient reach. Endemic hotspots rely on retail pharmacies for early treatment access. Community engagement, loyalty programs, and local partnerships further drive market leadership.

The Online Pharmacy segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, fueled by digital health adoption, home delivery, telemedicine integration, and patient preference for remote access. Mobile apps, e-commerce platforms, and increased internet penetration accelerate adoption. Online pharmacies provide discreet access, subscription services, and timely delivery, especially in underserved areas. Integration with telemedicine and electronic prescriptions enhances efficiency. E-commerce expansion, logistics optimization, and digital payment adoption further drive growth. Awareness campaigns and marketing initiatives increase penetration. Online pharmacies are gaining trust through certifications, reviews, and customer support. Endemic regions benefit from doorstep delivery. Digital platforms improve patient adherence and access to generics. Integration with public health programs ensures remote patient care. Online pharmacies support chronic and follow-up treatments efficiently.

Ehrlichiosis Treatment Market Regional Analysis

- North America dominated the ehrlichiosis treatment market with the largest revenue share of 39% in 2025, supported by robust healthcare infrastructure, high disease awareness, widespread access to antibiotics, and specialized treatment centers

- Consumers in the region highly value advanced diagnostic capabilities, early detection programs, and the availability of effective treatment options

- This widespread adoption is further supported by strong healthcare spending, technologically advanced medical facilities, and an emphasis on preventive care, establishing Ehrlichiosis treatment as a critical solution for both residential and clinical healthcare settings

U.S. Ehrlichiosis Treatment Market Insight

The U.S. ehrlichiosis treatment market captured the largest revenue share within North America in 2025, fueled by extensive diagnostic capabilities, early detection programs, and a high prevalence of specialized treatment centers. Patients and healthcare providers are increasingly prioritizing timely and effective interventions, while government-led awareness and disease management programs further drive market growth.

Europe Ehrlichiosis Treatment Market Insight

The Europe ehrlichiosis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising disease awareness, increasing incidence rates in certain countries, and the availability of advanced healthcare infrastructure. European healthcare systems emphasize early detection, timely treatment, and patient education, which together boost adoption rates.

U.K. Ehrlichiosis Treatment Market Insight

The U.K. ehrlichiosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by national health programs promoting disease awareness, robust healthcare infrastructure, and widespread access to effective antibiotic therapies. The country’s proactive surveillance and treatment initiatives are expected to continue stimulating market growth.

Germany Ehrlichiosis Treatment Market Insight

The Germany ehrlichiosis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, the presence of specialized infectious disease centers, and increasing awareness of the disease among clinicians and patients. Germany’s focus on research and development in infectious disease management also supports market expansion.

Asia-Pacific Ehrlichiosis Treatment Market Insight

The Asia-Pacific ehrlichiosis treatment market is poised to grow at the fastest CAGR of 8.5% during the forecast period from 2026 to 2033, driven by increasing incidence of the disease, expansion of healthcare access, and development of diagnostic and treatment facilities in countries such as China, India, Japan, and South Korea. Government initiatives promoting early detection, preventive measures, and access to effective antibiotics are further accelerating market adoption.

Japan Ehrlichiosis Treatment Market Insight

The Japan ehrlichiosis treatment market is gaining momentum due to rising disease awareness, increasing diagnostic capabilities, and government health programs aimed at early detection and treatment. The country’s advanced healthcare system and growing focus on infectious disease management are fueling market growth.

China Ehrlichiosis Treatment Market Insight

The China ehrlichiosis treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing disease prevalence, expansion of healthcare infrastructure, and government initiatives promoting early detection and treatment. The availability of affordable diagnostic and therapeutic solutions, along with strong domestic healthcare programs, are key factors propelling market growth in China.

Ehrlichiosis Treatment Market Share

The Ehrlichiosis Treatment industry is primarily led by well-established companies, including:

• Cephalon, Inc. (U.S.)

• Novartis AG (Switzerland)

• Pfizer Inc. (U.S.)

• GlaxoSmithKline (U.K.)

• Merck & Co., Inc. (U.S.)

• Sanofi (France)

• Cipla Ltd. (India)

• Aurobindo Pharma (India)

• Dr. Reddy’s Laboratories (India)

• Bayer AG (Germany)

• Roche Holding AG (Switzerland)

• Takeda Pharmaceutical Company (Japan)

• Eli Lilly and Company (U.S.)

• Janssen Pharmaceuticals (U.S.)

• Mylan N.V. (U.S.)

• Boehringer Ingelheim (Germany)

• AbbVie Inc. (U.S.)

• Teva Pharmaceutical Industries Ltd. (Israel)

• Shionogi & Co., Ltd. (Japan)

• Sun Pharmaceutical Industries Ltd. (India)

Latest Developments in Global Ehrlichiosis Treatment Market

- In January 2023, researchers at The Ohio State University and collaborators reported the development of cell‑permeable macrocyclic peptides that target the type IV secretion effector Etf‑1 of Ehrlichia chaffeensis. These peptides (such as “B7” and its derivatives) bind Etf‑1 with high affinity, block its interaction with host Beclin‑1, inhibit its localization to inclusion membranes, and significantly reduce E. chaffeensis infection in cultured human THP‑1 monocytes

- In July 2024, a study published in BMC Infectious Diseases documented that about 9.1% of patients with confirmed or probable ehrlichiosis in a U.S. cohort developed neurological symptoms, such as confusion, seizures, focal deficits, or cranial nerve palsy — often with normal neuroimaging. This finding raises awareness of “neuro‑ehrlichiosis” and underlines the need for early diagnosis and appropriate treatment, even in atypical cases

- In August 2024, scientists published in Vaccines (MDPI) that a genetically modified live-attenuated vaccine (MLAV) for Ehrlichia chaffeensis, tested in dogs, conferred at least one year of protective immunity. Vaccinated dogs challenged (both via tick transmission and by direct injection) cleared the pathogen much more effectively than unvaccinated controls; they also maintained specific IgG and CD4+ T‑cell immune responses throughout the year

- In January 2025, a follow-up study further confirmed the durability of immunity induced by the MLAV: dogs vaccinated with the attenuated strain were exposed to E. chaffeensis via tick bite up to 12 months after vaccination, and they showed significantly lower systemic infection rates compared to controls

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.