Global Electric Vehicle Charging Cables Market

Market Size in USD Billion

USD

1.02 Billion

USD

10.01 Billion

2025

2033

USD

1.02 Billion

USD

10.01 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.02 Billion | |

| USD 10.01 Billion | |

| % | |

|

Electric Vehicle Charging Cables Market Overview

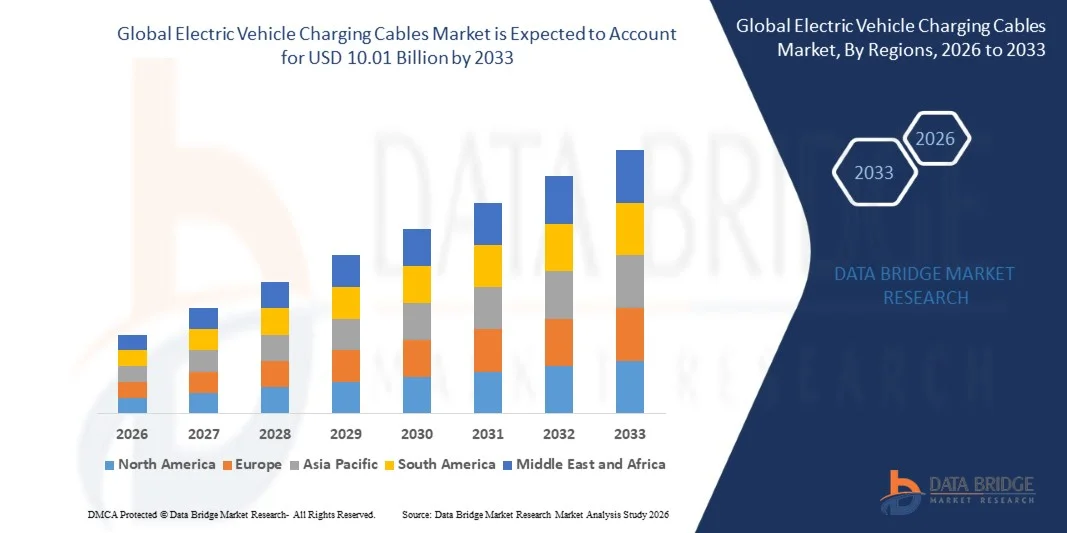

The Electric Vehicle Charging Cables Market was valued at USD 1.02 billion in 2025 and is projected to reach USD 10.01 billion by 2033, growing at a CAGR of 33.00% from 2026 to 2033. The market is experiencing rapid growth driven by accelerating electric vehicle adoption, expanding public and private charging infrastructure, and increasing government investments in clean transportation initiatives. Rising demand for fast, reliable, and high-power charging solutions, combined with technological advancements in charging systems and connector standards, is further supporting market expansion across residential, commercial, and public charging applications.

The global transition toward low-emission mobility, combined with stringent vehicle emission regulations and ambitious electrification targets, is compelling governments, utilities, automotive manufacturers, and charging network operators to invest heavily in EV charging infrastructure. High-performance charging cables are becoming critical components of both AC and DC charging systems, enabling efficient power transfer while ensuring safety, durability, and compatibility across multiple vehicle platforms. Advancements in liquid-cooled cable technology, lightweight materials, and ultra-fast charging systems are helping address challenges related to power delivery and charging efficiency. In addition, the rapid expansion of battery electric vehicles, growing deployment of highway fast-charging corridors, and increasing integration of smart charging technologies are creating substantial opportunities for charging cable manufacturers. As charging networks continue to scale globally, demand for advanced EV charging cables capable of supporting higher voltage architectures and faster charging speeds is expected to accelerate significantly throughout the forecast period.

Key Market Trends & Insights

- North America dominated the electric vehicle charging cables market with the largest revenue share of 36.8% in 2025, supported by strong EV adoption rates, extensive charging network expansion, favorable government funding programs, and the presence of leading charging infrastructure providers and automotive manufacturers.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 35.7% from 2026 to 2033. Growth is driven by rising EV production and sales, large-scale charging infrastructure investments across China, Japan, South Korea, and India, supportive government policies, and expanding domestic manufacturing capabilities.

- The Private Charging segment held the largest market revenue share of approximately 61.8% in 2025 driven by widespread installation of residential charging systems, increasing home EV ownership, and the convenience of overnight charging. Home charging solutions remain highly preferred among EV users due to lower charging costs and greater accessibility. The growing availability of smart home charging equipment and government incentives supporting residential charger installation are further strengthening segment demand. In addition, rising adoption of battery electric vehicles among individual consumers continues to accelerate deployment of private charging infrastructure across developed and emerging economies.

- The Public Charging segment is projected to register the fastest growth at a CAGR of 35.4% from 2026 to 2033, driven by rapid deployment of public charging infrastructure, government investments in charging corridors, and increasing adoption of electric mobility across urban and commercial environments. Growing demand for fast-charging stations in shopping centers, highways, commercial complexes, and fleet depots is supporting segment expansion. Major charging network operators are continuously expanding station coverage to reduce range anxiety and improve accessibility. Increasing investments in ultra-fast charging technologies are also contributing significantly to market growth.

- The Alternate Charging segment held the largest market revenue share of approximately 58.7% in 2025 driven by its extensive use in residential and workplace charging applications. AC charging systems offer cost-effective installation and remain widely utilized for daily vehicle charging requirements. The segment benefits from widespread compatibility with existing electrical infrastructure and lower equipment costs compared to DC systems. Growing installation of workplace charging facilities and apartment-based charging solutions is further supporting segment dominance.

- The Direct Charging segment is projected to register the fastest growth at a CAGR of 37.2% from 2026 to 2033, driven by increasing demand for ultra-fast charging capabilities, expansion of public DC charging stations, and growing adoption of long-range electric vehicles. DC charging significantly reduces charging time, making it highly attractive for commercial and highway charging applications. Rising deployment of 350 kW and higher charging systems is accelerating demand for advanced high-capacity charging cables. The increasing adoption of high-voltage EV platforms is further boosting segment growth.

- The Up to 5 Meters segment held the largest market revenue share of approximately 47.5% in 2025 driven by its widespread suitability for residential charging installations and standard parking configurations. These cables offer ease of handling, lower material costs, and efficient charging performance. Their compact design reduces storage requirements while maintaining operational convenience for everyday users. Growing adoption of home charging solutions continues to support strong demand for shorter cable configurations.

- The 5 Meters to 10 Meters segment is projected to register the fastest growth at a CAGR of 34.8% from 2026 to 2033, driven by increasing deployment across commercial facilities, public charging stations, and fleet charging environments requiring greater installation flexibility. Longer cables provide easier vehicle access across different parking layouts and charging station designs. Expansion of public charging infrastructure in urban locations is contributing to rising demand. Fleet operators are also increasingly utilizing longer cable systems to support diverse vehicle configurations.

- The Straight Cable segment held the largest market revenue share of approximately 68.2% in 2025 driven by its lower manufacturing cost, wider compatibility, and extensive adoption across residential and public charging systems. Straight cables are preferred for high-power charging applications due to improved current carrying capabilities. Their simple design enhances durability and supports efficient power transfer across various charging levels. Increasing deployment of fast-charging stations continues to reinforce demand for straight cable solutions.

- The Coiled Cable segment is projected to register the fastest growth at a CAGR of 33.6% from 2026 to 2033, driven by increasing demand for compact storage solutions, improved cable management, and enhanced user convenience in urban charging environments. Coiled cables reduce ground contact and help minimize wear and tear during daily operation. Their ability to retract automatically makes them particularly attractive for residential and commercial charging applications. Growing emphasis on user-friendly charging infrastructure is supporting segment expansion.

- The Level 2 segment held the largest market revenue share of approximately 52.9% in 2025 driven by its balance between charging speed, installation cost, and widespread deployment across residential, commercial, and workplace charging applications. Level 2 charging continues to represent the most commonly installed charging solution globally. The segment benefits from growing EV ownership and increasing installation of destination charging stations. Its ability to provide significantly faster charging than Level 1 systems makes it highly attractive for everyday use.

- The Level 3 segment is projected to register the fastest growth at a CAGR of 39.1% from 2026 to 2033, driven by accelerating investments in fast-charging infrastructure, increasing highway charging deployments, and growing demand for reduced vehicle charging times. Level 3 systems are becoming essential for long-distance travel and commercial fleet operations. Automotive manufacturers and charging network providers are increasingly focusing on ultra-fast charging capabilities. The expansion of high-power charging corridors is expected to significantly support segment growth.

- The Thermoplastic Elastomer (TPE) Jacket segment held the largest market revenue share of approximately 44.6% in 2025 driven by its superior flexibility, weather resistance, durability, and suitability for both indoor and outdoor charging applications. TPE jackets are increasingly preferred for next-generation charging cable designs. They provide excellent performance across varying temperature conditions while maintaining cable flexibility. Growing demand for durable and lightweight charging solutions continues to support segment growth.

- The All Rubber Jacket segment is projected to register the fastest growth at a CAGR of 34.2% from 2026 to 2033, driven by increasing demand for high-performance cables capable of operating under harsh environmental and industrial conditions. Rubber jackets offer superior mechanical protection and enhanced resistance to abrasion, moisture, and chemicals. These characteristics make them particularly suitable for heavy-duty charging infrastructure applications. Expanding deployment of outdoor fast-charging systems is contributing to rising demand.

- The 16-32 Amp segment held the largest market revenue share of approximately 63.4% in 2025 driven by widespread utilization in residential and standard commercial charging installations. The segment remains highly popular due to lower infrastructure requirements and compatibility with most passenger electric vehicles. Cost-effective deployment and broad availability further strengthen adoption across key markets. Growing residential charger installations continue to support segment dominance.

- The 33-72 Amp segment is projected to register the fastest growth at a CAGR of 38.5% from 2026 to 2033, driven by increasing deployment of high-power charging stations, growing adoption of fast-charging technologies, and rising demand for rapid charging solutions across commercial and fleet applications. Higher current capacity enables faster charging performance and improved operational efficiency. The segment is benefiting from the increasing introduction of long-range EVs and high-voltage battery systems. Continued expansion of ultra-fast charging infrastructure is expected to drive strong growth throughout the forecast period.

Market Size & Forecast

- Global Market Value (2025): USD 1.02 Billion

- Expected Market Value (2033): USD 10.01 Billion

- Forecast CAGR (2026–2033): 33.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Electric Vehicle Charging Cables Market Segmentation

|

Attributes |

Electric Vehicle Charging Cables Key Market Insights |

|

Segments Covered |

· By Application: Private Charging and Public Charging), Power Supply · By Type: Alternate Charging and Direct Charging · By Cable Length: Meters to 5 Meters, Meters to 10 Meters, and Above 10 Meters · By Shape: Straight Cable and Coiled Cable · By Charging Level: Level 1, Level 2, and Level 3 · By Jacket Material: All Rubber Jacket, Thermoplastic Elastomer (TPE) Jacket, and Polyvinyl Chloride (PVC) Jacket), Current (16-32 Amp and 33-72 Amp |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• LEONI AG (Germany) |

|

Market Opportunities |

• Expansion Of Ultra-Fast EV Charging Infrastructure Networks |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Electric Vehicle Charging Cables Market Trends

Trend: Expansion Of Ultra-Fast Charging Infrastructure And High-Power EV Charging Technologies

Increasing adoption of electric vehicles worldwide is creating strong demand for faster, safer, and more efficient charging solutions across public, commercial, and residential charging networks. Conventional charging systems often require longer charging durations, creating range anxiety and limiting user convenience, encouraging governments and charging network operators to invest in high-power charging infrastructure supported by advanced charging cable technologies.

Automotive manufacturers and charging providers are increasingly deploying ultra-fast DC charging systems, For instance 350 kW and above charging stations, to reduce charging times and improve EV usability. Advanced liquid-cooled charging cables are gaining traction because they can safely handle higher current loads while maintaining flexibility and reducing cable weight. These technologies are becoming essential for supporting next-generation electric vehicles equipped with high-voltage battery architectures and extended driving ranges.

The rapid expansion of public charging networks across major EV markets is further accelerating demand for advanced charging cables. In addition, leading charging infrastructure providers are investing in smart charging technologies that improve energy management and charging efficiency. Industry developments during 2025 demonstrated that several ultra-fast charging systems can deliver up to 300 kilometers of driving range in less than 15 minutes, highlighting the growing importance of high-performance charging cable solutions within the EV ecosystem.

Electric Vehicle Charging Cables Market Dynamics

Key Market Driver: Rapid Expansion Of Electric Vehicle Charging Infrastructure

Governments, utilities, and private charging operators worldwide are making substantial investments in EV charging infrastructure to support accelerating electric vehicle adoption and decarbonization objectives. The increasing deployment of public fast-charging stations, workplace chargers, fleet charging facilities, and residential charging systems is creating strong demand for reliable and durable charging cables capable of supporting diverse charging requirements.

Countries across North America, Europe, and Asia-Pacific are implementing large-scale charging infrastructure programs, For instance highway fast-charging corridors and urban charging networks, to improve EV accessibility and reduce range anxiety. Automotive manufacturers are also expanding partnerships with charging network providers to ensure seamless charging experiences for vehicle owners. These developments are increasing the need for high-quality charging cables that offer enhanced safety, durability, and compatibility with evolving charging standards.

Real-world deployment data highlights the scale of market growth. According to international energy industry estimates, the global number of public EV charging points exceeded 5 million units in 2024, with fast chargers representing one of the fastest-growing infrastructure categories. The continuous expansion of charging networks is expected to generate sustained demand for charging cables throughout the forecast period.

Key Restraint/Challenge: High Infrastructure Costs And Standardization Complexities

Despite strong market growth, the EV charging cable industry faces challenges associated with high infrastructure deployment costs and evolving charging standards across different regions. Advanced charging cables designed for high-power applications often require specialized materials, enhanced insulation systems, and sophisticated thermal management technologies, increasing overall manufacturing costs.

In addition, variations in connector types, charging protocols, and regulatory requirements across global markets create compatibility and standardization challenges for manufacturers and charging operators. The deployment of ultra-fast charging infrastructure also requires significant investments in electrical grid upgrades and supporting equipment, creating financial barriers in certain regions. These factors can slow infrastructure rollout and impact adoption rates in developing markets.

Industry assessments indicate that installation costs for high-power DC fast-charging systems can be several times higher than conventional AC charging infrastructure due to equipment, grid connection, and operational requirements. Managing these costs while maintaining charging performance remains a key challenge for industry participants.

Key Market Opportunity: Adoption Of High-Voltage Platforms And Next-Generation Charging Technologies

The emergence of advanced electric vehicle architectures and ultra-fast charging technologies is creating substantial opportunities for charging cable manufacturers. Modern electric vehicles increasingly utilize 800-volt and higher battery systems that require charging cables capable of safely handling elevated power levels while maintaining efficiency and user convenience.

Automotive manufacturers are increasingly introducing high-voltage EV platforms, For instance in premium passenger vehicles, commercial fleets, and high-performance electric models, to enable faster charging and improved vehicle performance. Charging infrastructure providers are simultaneously deploying liquid-cooled charging cable systems that support power outputs exceeding 350 kW while reducing cable thickness and improving user handling. These innovations are opening new opportunities across public charging, fleet electrification, and commercial transportation applications.

In addition, advancements in cable materials, thermal management systems, and smart monitoring technologies are improving product reliability and operational efficiency. EV charging pilot programs conducted across Europe, China, and the U.S. during 2025 demonstrated charging times reduced by nearly 30–40% when utilizing next-generation high-power charging systems, reinforcing the significant market potential for advanced EV charging cable solutions.

Electric Vehicle Charging Cables Market Scope

The market is segmented on the basis of application, type, cable length, shape, charging level, jacket material, and current.

- By Application

On the basis of application, the electric vehicle charging cables market is segmented into Private Charging and Public Charging. The Private Charging segment held the largest market revenue share of approximately 61.8% in 2025 driven by widespread installation of residential charging systems, increasing home EV ownership, and the convenience of overnight charging. Home charging solutions remain highly preferred among EV users due to lower charging costs and greater accessibility. The growing availability of smart home charging equipment and government incentives supporting residential charger installation are further strengthening segment demand. In addition, rising adoption of battery electric vehicles among individual consumers continues to accelerate deployment of private charging infrastructure across developed and emerging economies.

The Public Charging segment is projected to register the fastest growth at a CAGR of 35.4% from 2026 to 2033, driven by rapid deployment of public charging infrastructure, government investments in charging corridors, and increasing adoption of electric mobility across urban and commercial environments. Growing demand for fast-charging stations in shopping centers, highways, commercial complexes, and fleet depots is supporting segment expansion. Major charging network operators are continuously expanding station coverage to reduce range anxiety and improve accessibility. Increasing investments in ultra-fast charging technologies are also contributing significantly to market growth.

- By Type

On the basis of type, the electric vehicle charging cables market is segmented into Alternate Charging and Direct Charging. The Alternate Charging segment held the largest market revenue share of approximately 58.7% in 2025 driven by its extensive use in residential and workplace charging applications. AC charging systems offer cost-effective installation and remain widely utilized for daily vehicle charging requirements. The segment benefits from widespread compatibility with existing electrical infrastructure and lower equipment costs compared to DC systems. Growing installation of workplace charging facilities and apartment-based charging solutions is further supporting segment dominance.

The Direct Charging segment is projected to register the fastest growth at a CAGR of 37.2% from 2026 to 2033, driven by increasing demand for ultra-fast charging capabilities, expansion of public DC charging stations, and growing adoption of long-range electric vehicles. DC charging significantly reduces charging time, making it highly attractive for commercial and highway charging applications. Rising deployment of 350 kW and higher charging systems is accelerating demand for advanced high-capacity charging cables. The increasing adoption of high-voltage EV platforms is further boosting segment growth.

- By Cable Length

On the basis of cable length, the electric vehicle charging cables market is segmented into Up to 5 Meters, 5 Meters to 10 Meters, and Above 10 Meters. The Up to 5 Meters segment held the largest market revenue share of approximately 47.5% in 2025 driven by its widespread suitability for residential charging installations and standard parking configurations. These cables offer ease of handling, lower material costs, and efficient charging performance. Their compact design reduces storage requirements while maintaining operational convenience for everyday users. Growing adoption of home charging solutions continues to support strong demand for shorter cable configurations.

The 5 Meters to 10 Meters segment is projected to register the fastest growth at a CAGR of 34.8% from 2026 to 2033, driven by increasing deployment across commercial facilities, public charging stations, and fleet charging environments requiring greater installation flexibility. Longer cables provide easier vehicle access across different parking layouts and charging station designs. Expansion of public charging infrastructure in urban locations is contributing to rising demand. Fleet operators are also increasingly utilizing longer cable systems to support diverse vehicle configurations.

- By Shape

On the basis of shape, the electric vehicle charging cables market is segmented into Straight Cable and Coiled Cable. The Straight Cable segment held the largest market revenue share of approximately 68.2% in 2025 driven by its lower manufacturing cost, wider compatibility, and extensive adoption across residential and public charging systems. Straight cables are preferred for high-power charging applications due to improved current carrying capabilities. Their simple design enhances durability and supports efficient power transfer across various charging levels. Increasing deployment of fast-charging stations continues to reinforce demand for straight cable solutions.

The Coiled Cable segment is projected to register the fastest growth at a CAGR of 33.6% from 2026 to 2033, driven by increasing demand for compact storage solutions, improved cable management, and enhanced user convenience in urban charging environments. Coiled cables reduce ground contact and help minimize wear and tear during daily operation. Their ability to retract automatically makes them particularly attractive for residential and commercial charging applications. Growing emphasis on user-friendly charging infrastructure is supporting segment expansion.

- By Charging Level

On the basis of charging level, the electric vehicle charging cables market is segmented into Level 1, Level 2, and Level 3. The Level 2 segment held the largest market revenue share of approximately 52.9% in 2025 driven by its balance between charging speed, installation cost, and widespread deployment across residential, commercial, and workplace charging applications. Level 2 charging continues to represent the most commonly installed charging solution globally. The segment benefits from growing EV ownership and increasing installation of destination charging stations. Its ability to provide significantly faster charging than Level 1 systems makes it highly attractive for everyday use.

The Level 3 segment is projected to register the fastest growth at a CAGR of 39.1% from 2026 to 2033, driven by accelerating investments in fast-charging infrastructure, increasing highway charging deployments, and growing demand for reduced vehicle charging times. Level 3 systems are becoming essential for long-distance travel and commercial fleet operations. Automotive manufacturers and charging network providers are increasingly focusing on ultra-fast charging capabilities. The expansion of high-power charging corridors is expected to significantly support segment growth.

- By Jacket Material

On the basis of jacket material, the electric vehicle charging cables market is segmented into All Rubber Jacket, Thermoplastic Elastomer (TPE) Jacket, and Polyvinyl Chloride (PVC) Jacket. The Thermoplastic Elastomer (TPE) Jacket segment held the largest market revenue share of approximately 44.6% in 2025 driven by its superior flexibility, weather resistance, durability, and suitability for both indoor and outdoor charging applications. TPE jackets are increasingly preferred for next-generation charging cable designs. They provide excellent performance across varying temperature conditions while maintaining cable flexibility. Growing demand for durable and lightweight charging solutions continues to support segment growth.

The All Rubber Jacket segment is projected to register the fastest growth at a CAGR of 34.2% from 2026 to 2033, driven by increasing demand for high-performance cables capable of operating under harsh environmental and industrial conditions. Rubber jackets offer superior mechanical protection and enhanced resistance to abrasion, moisture, and chemicals. These characteristics make them particularly suitable for heavy-duty charging infrastructure applications. Expanding deployment of outdoor fast-charging systems is contributing to rising demand.

- By Current

On the basis of current, the electric vehicle charging cables market is segmented into 16-32 Amp and 33-72 Amp. The 16-32 Amp segment held the largest market revenue share of approximately 63.4% in 2025 driven by widespread utilization in residential and standard commercial charging installations. The segment remains highly popular due to lower infrastructure requirements and compatibility with most passenger electric vehicles. Cost-effective deployment and broad availability further strengthen adoption across key markets. Growing residential charger installations continue to support segment dominance.

The 33-72 Amp segment is projected to register the fastest growth at a CAGR of 38.5% from 2026 to 2033, driven by increasing deployment of high-power charging stations, growing adoption of fast-charging technologies, and rising demand for rapid charging solutions across commercial and fleet applications. Higher current capacity enables faster charging performance and improved operational efficiency. The segment is benefiting from the increasing introduction of long-range EVs and high-voltage battery systems. Continued expansion of ultra-fast charging infrastructure is expected to drive strong growth throughout the forecast period.

Electric Vehicle Charging Cables Market Regional Analysis

North America Electric Vehicle Charging Cables Market Insight

North America dominated the electric vehicle charging cables market with the largest revenue share of 36.8% in 2025, supported by strong electric vehicle adoption, expanding public charging infrastructure, and substantial government investments in clean transportation initiatives. The region benefits from a mature EV ecosystem, increasing deployment of DC fast-charging stations, and growing consumer preference for battery electric vehicles. Rising investments from automotive manufacturers, utilities, and charging network operators are further accelerating demand for advanced charging cable solutions. The increasing focus on reducing transportation emissions continues to support long-term market expansion.

U.S. Electric Vehicle Charging Cables Market Insight

The U.S. electric vehicle charging cables market captured the largest revenue share in 2025 within North America, fueled by rapid EV adoption and extensive investments in charging infrastructure development. Consumers and commercial fleet operators are increasingly adopting electric vehicles, creating strong demand for reliable and high-performance charging systems. The expansion of highway charging corridors, workplace charging installations, and residential charging networks continues to drive cable demand. Moreover, federal funding programs supporting charging infrastructure deployment are significantly contributing to market growth across the country.

Europe Electric Vehicle Charging Cables Market Insight

The Europe electric vehicle charging cables market is expected to witness substantial growth from 2026 to 2033, primarily driven by stringent vehicle emission regulations, aggressive electrification targets, and widespread EV adoption. Governments across the region continue to support charging infrastructure deployment through subsidies and policy incentives. Increasing demand for public fast-charging stations and growing investments in sustainable transportation solutions are encouraging market expansion. The region is also witnessing strong adoption of high-power charging technologies and advanced cable systems capable of supporting ultra-fast charging applications.

U.K. Electric Vehicle Charging Cables Market Insight

The U.K. electric vehicle charging cables market is expected to witness significant growth from 2026 to 2033, driven by increasing EV registrations, expanding public charging networks, and government initiatives promoting zero-emission transportation. Consumers are increasingly transitioning toward electric mobility due to rising environmental awareness and favorable policy support. The growing installation of residential chargers and workplace charging facilities is contributing to market development. In addition, investments in rapid and ultra-rapid charging infrastructure are expected to create strong demand for advanced charging cable solutions.

Germany Electric Vehicle Charging Cables Market Insight

The Germany electric vehicle charging cables market is expected to witness strong growth from 2026 to 2033, fueled by the country's leadership in automotive manufacturing and increasing investments in electric mobility infrastructure. Germany continues to prioritize transportation electrification through supportive government policies and industry partnerships. Rising deployment of public charging stations, increasing EV production, and growing consumer acceptance of electric vehicles are supporting market growth. The adoption of high-voltage vehicle architectures and fast-charging technologies is also contributing to increased demand for advanced charging cables.

Asia-Pacific Electric Vehicle Charging Cables Market Insight

The Asia-Pacific electric vehicle charging cables market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid EV adoption, expanding charging infrastructure, and strong government support for electrification programs. Countries such as China, Japan, South Korea, and India are investing heavily in charging networks to support growing electric vehicle fleets. Rising urbanization, increasing environmental concerns, and improving charging accessibility are accelerating market development. The region's strong manufacturing base for EV components and charging equipment further supports industry expansion.

Japan Electric Vehicle Charging Cables Market Insight

The Japan electric vehicle charging cables market is expected to witness notable growth from 2026 to 2033 due to increasing adoption of electric and plug-in hybrid vehicles, advancements in charging technologies, and government initiatives promoting carbon neutrality. The Japanese market places significant emphasis on technological innovation, safety, and charging efficiency. Growing deployment of fast-charging infrastructure and increasing integration of smart charging solutions are supporting market expansion. Furthermore, the country's automotive manufacturers continue to invest in next-generation EV technologies, creating additional opportunities for charging cable suppliers.

China Electric Vehicle Charging Cables Market Insight

The China electric vehicle charging cables market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's dominant position in global EV production and sales. China operates one of the world's largest charging infrastructure networks, generating substantial demand for charging cables across residential, commercial, and public charging applications. Strong government support, large-scale investments in charging stations, and increasing adoption of battery electric vehicles continue to drive market growth. The rapid expansion of ultra-fast charging infrastructure and domestic manufacturing capabilities further strengthens China's leadership position in the electric vehicle charging cables market.

Electric Vehicle Charging Cables Market Share

The Electric Vehicle Charging Cables industry is primarily led by well-established companies, including:

• LEONI AG (Germany)

• Brugg Kabel AG (Switzerland)

• Yangzhou Teison New Energy Co., Ltd. (China)

• Prysmian S.p.A. (Italy)

• Aptiv (Ireland)

• BESEN Group (China)

• DYDEN CORPORATION. (Japan)

• TE Connectivity (Ireland)

• SINBON Electronics Co., Ltd. (Taiwan)

• Coroplast Fritz Müller GmbH & Co. KG (Germany)

• PHOENIX CONTACT (Germany)

• Systems Wire Cable (U.S.)

• Eland Cables (U.K.)

• Manlon Polymers (India)

• Chengdu Khons Technology Co., Ltd. (China)

• Allwyn Cables (India)

• IONITY GmbH (Germany)

• Elkem ASA (Norway)

• HWATEK Wires & Cable Co., Ltd. (China)

Latest Developments in Electric Vehicle Charging Cables Market

- In January 2026, Rolec announced a product launch with the introduction of its upgraded UltraCharge DC Charging Range developed in partnership with EVbee. The new UltraCharge 180 system enables simultaneous charging of two electric vehicles using dual CCS2 charging cables, improving charging efficiency in high-traffic locations such as motorways and retail destinations. The development strengthens public fast-charging infrastructure, reduces charging wait times, and supports the growing adoption of long-range electric vehicles. This launch is expected to accelerate deployment of high-capacity charging networks across key transportation corridors.

- In December 2025, Polycab India announced a product portfolio expansion by introducing AC/DC chargers, EV charging guns, and automotive cables at Auto EV Bharat 2025. The newly launched solutions are designed to comply with international standards while supporting residential, commercial, and fast-charging applications. The development enhances the company's presence in the electric mobility ecosystem and improves the availability of locally manufactured charging components. It is expected to support India's expanding EV infrastructure and strengthen domestic supply chain capabilities.

- In November 2025, Cord introduced EVIRA, a portable EV charging solution specifically designed for workshops, vehicle dealerships, and pre-delivery inspection facilities. The charger provides significantly faster charging performance compared to conventional charging systems while offering compatibility with standard industrial power connections. The innovation improves operational flexibility for automotive service providers and reduces vehicle preparation time. Its introduction is expected to increase adoption of portable charging technologies across commercial EV service environments.

- In October 2025, InstaVolt announced a strategic technology partnership with Trackit247 to launch a GPS-enabled tracking solution for EV charging cables. The system provides real-time monitoring and recovery capabilities aimed at addressing the growing issue of cable theft at charging stations. This development improves infrastructure security, reduces maintenance costs, and enhances operational reliability for charging network operators. The initiative is expected to encourage wider deployment of public charging infrastructure by minimizing asset protection concerns.

- In July 2022, TE Connectivity completed the acquisition of ERNI as part of its strategic expansion initiative in advanced connectivity solutions. The acquisition strengthened TE Connectivity’s portfolio of high-speed and fine-pitch connectors serving factory automation, automotive, medical, and industrial sectors. The development enhances product innovation capabilities and broadens the company’s customer reach across high-growth industries. The transaction is expected to support advancements in next-generation EV charging and connectivity technologies.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.