Global Electric Vehicles Polymer Market

Market Size in USD Billion

USD

5.29 Billion

USD

9.10 Billion

2025

2033

USD

5.29 Billion

USD

9.10 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.29 Billion | |

| USD 9.10 Billion | |

| % | |

|

Electric Vehicles Polymer Market Size

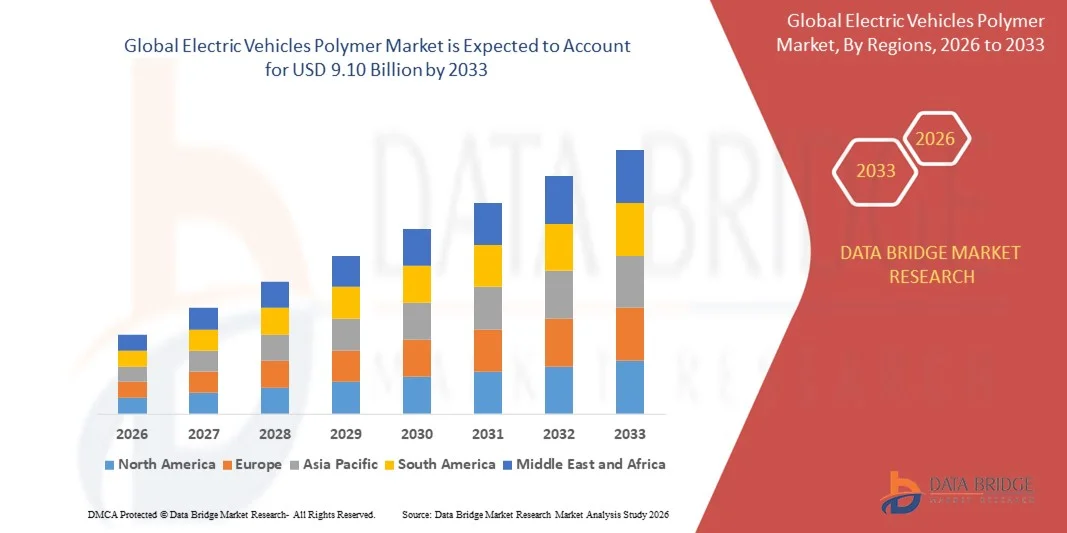

- The global electric vehicles polymer market size was valued at USD 5.29 billion in 2025 and is expected to reach USD 9.10 billion by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fuelled by the increasing adoption of electric vehicles worldwide, driven by government incentives, stricter emission regulations, and growing consumer demand for sustainable transportation

- Rising use of lightweight polymers in EV components such as batteries, interiors, and exteriors is contributing to improved vehicle efficiency and performance, further boosting market demand

Electric Vehicles Polymer Market Analysis

- The market is witnessing significant growth due to the shift toward lightweight materials in EV manufacturing to enhance driving range and reduce overall vehicle weight

- Increasing investments by automotive manufacturers in research and development of advanced polymer composites are driving innovation and supporting market expansion

- North America dominated the electric vehicles polymer market with the largest revenue share in 2025, driven by increasing EV adoption, government incentives for green mobility, and advanced automotive manufacturing infrastructure

- Asia-Pacific region is expected to witness the highest growth rate in the global electric vehicles polymer market, driven by rising urbanization, increasing EV production, technological advancements in polymer materials, and strong government policies supporting electrification and sustainable transportation

- The Engineering Plastics segment held the largest market revenue share in 2025, driven by their high strength-to-weight ratio, thermal stability, and suitability for structural and battery components in EVs. These polymers enable manufacturers to reduce overall vehicle weight while maintaining durability, performance, and safety standards

Report Scope and Electric Vehicles Polymer Market Segmentation

|

Attributes |

Electric Vehicles Polymer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• BASF SE (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Electric Vehicles Polymer Market Trends

Rising Adoption of Lightweight Polymers in Electric Vehicles

- The growing shift toward lightweight and high-performance polymers is transforming the electric vehicles (EV) industry by enabling improved battery efficiency, extended driving range, and enhanced vehicle safety. The use of advanced polymers in interiors, exteriors, and battery components reduces overall vehicle weight, contributing to better energy efficiency and lower emissions. In addition, the integration of polymers supports innovative EV designs, enhances crashworthiness, and facilitates compliance with evolving environmental regulations

- Increasing demand for electric vehicles across developed and emerging markets is accelerating the adoption of polymer-based components. Polymers are particularly valuable where metal alternatives are heavier or less durable, helping manufacturers achieve performance targets and regulatory compliance. The trend is further reinforced by government incentives for lightweight materials and ongoing investments in EV infrastructure, boosting global adoption

- The affordability, versatility, and ease of processing of modern polymers are making them attractive for large-scale EV production, enabling cost-effective and scalable manufacturing of lightweight parts without compromising structural integrity. Polymers also allow for rapid prototyping, design flexibility, and integration of multifunctional components, supporting innovation in EV assembly lines

- For instance, in 2023, several EV manufacturers in Europe and the U.S. reported a reduction in battery and chassis weight after integrating high-performance polymer composites, leading to improved vehicle range and lower energy consumption. These changes also contributed to improved driving performance, reduced carbon footprint, and lower operational costs for consumers

- While polymer adoption in EVs is accelerating efficiency and sustainability, its impact depends on continued material innovation, regulatory approvals, and cost optimization. Manufacturers must focus on developing tailored polymer solutions for different EV applications to fully capitalize on this growing demand, while maintaining safety standards and lifecycle durability

Electric Vehicles Polymer Market Dynamics

Driver

Increasing Demand for Lightweight and High-Performance Materials in Electric Vehicles

- The global push toward sustainable and energy-efficient transportation is driving automakers to prioritize polymers in EV manufacturing. Lightweight polymers help reduce vehicle mass, improving battery efficiency and driving range, while supporting overall environmental goals. This focus also encourages manufacturers to invest in renewable energy-powered production processes, reinforcing the sustainability aspect of EVs

- OEMs are increasingly incorporating high-performance polymers in structural, interior, and battery components to meet design and safety standards. This shift is supported by evolving consumer preferences for energy-efficient, eco-friendly vehicles. Enhanced material properties, including impact resistance and thermal stability, allow EVs to meet rigorous safety certifications, further increasing consumer trust

- Research and development efforts by material suppliers are producing innovative polymers with heat resistance, durability, and lightweight characteristics, enabling their wider adoption in the EV industry. These advancements also include flame-retardant additives, recyclability features, and compatibility with advanced coatings, expanding the application scope for EV manufacturers

- For instance, in 2022, leading EV manufacturers in North America implemented polymer-based battery housings and interior panels, significantly reducing vehicle weight while maintaining safety and performance standards. The adoption of these materials also resulted in decreased maintenance costs, longer component life, and improved thermal management of battery systems

- While the growing emphasis on lightweight materials is driving market demand, the industry must ensure material performance, cost-effectiveness, and regulatory compliance to sustain long-term adoption. Collaborations between OEMs and polymer suppliers, along with government-backed initiatives, are helping accelerate R&D and large-scale deployment

Restraint/Challenge

High Cost of Advanced Polymers and Limited Manufacturing Infrastructure

- Advanced high-performance polymers such as PEEK, PPS, and PA66 blends remain costly compared with traditional materials, limiting widespread adoption, particularly among mid-tier EV manufacturers. The high costs also impact overall vehicle pricing, potentially reducing consumer adoption rates and slowing market expansion in price-sensitive regions

- Many regions lack sufficient manufacturing infrastructure and expertise to process complex polymer composites for large-scale EV production, creating supply bottlenecks and increasing lead times. Limited access to specialized equipment, automated processing lines, and trained workforce further hinders timely production and consistent quality across global EV markets

- The need for specialized equipment and technical know-how for polymer processing poses barriers in integrating polymers into existing automotive production lines, slowing market penetration. These challenges also affect scaling new polymer formulations, performing quality assurance testing, and maintaining compliance with evolving safety and environmental regulations

- For instance, in 2023, several EV startups in Asia-Pacific reported delays in production due to limited access to advanced polymer processing facilities and skilled personnel, affecting market growth. The shortage of raw materials and reliance on imports for certain polymer grades further exacerbated production constraints and impacted supply chain efficiency

- While polymer technology continues to advance, addressing cost, infrastructure, and processing challenges is critical. Stakeholders must focus on localized manufacturing, scalable production solutions, and cost optimization to unlock long-term market potential. Strategic partnerships, government support, and technology transfer initiatives are key to overcoming these barriers and sustaining industry growth

Electric Vehicles Polymer Market Scope

The market is segmented on the basis of type, component, and vehicle type.

- By Type

On the basis of type, the electric vehicles polymer market is segmented into Engineering Plastics, Elastomers, and Others. The Engineering Plastics segment held the largest market revenue share in 2025, driven by their high strength-to-weight ratio, thermal stability, and suitability for structural and battery components in EVs. These polymers enable manufacturers to reduce overall vehicle weight while maintaining durability, performance, and safety standards.

The Elastomers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by their flexibility, impact resistance, and vibration damping properties, making them ideal for seals, gaskets, and interior components. Elastomer-based polymers are particularly popular for improving ride comfort, noise reduction, and overall vehicle performance in modern electric vehicles.

- By Component

On the basis of component, the market is segmented into Powertrain, Exterior, Interior, and Others. The Powertrain segment accounted for the largest revenue share in 2025, owing to the increasing use of polymers in battery housings, electric motors, and thermal management systems. Polymer integration in powertrain components contributes to weight reduction, energy efficiency, and improved thermal and electrical insulation.

The Interior segment is expected to witness the fastest growth from 2026 to 2033, driven by the demand for lightweight, durable, and aesthetically appealing materials in dashboards, panels, and seats. Polymers in interiors provide design flexibility, enhance user comfort, and support multifunctional applications such as embedded electronics and sensors.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Battery Electric Vehicles (BEVs), Hybrid Electric Vehicles (HEVs), and Plug-in Hybrid Electric Vehicles (PHEVs). The BEVs segment held the largest market share in 2025, fueled by the rising adoption of fully electric vehicles across developed and emerging markets. Polymers are widely used in BEVs for weight optimization, battery efficiency, and regulatory compliance.

The HEVs segment is expected to witness the fastest growth from 2026 to 2033, driven by increasing consumer preference for fuel-efficient vehicles and stricter emission norms. Polymer-based components in HEVs help improve fuel economy, reduce carbon footprint, and enhance vehicle performance without compromising safety or design flexibility.

Electric Vehicles Polymer Market Regional Analysis

- North America dominated the electric vehicles polymer market with the largest revenue share in 2025, driven by increasing EV adoption, government incentives for green mobility, and advanced automotive manufacturing infrastructure

- Consumers and OEMs in the region highly value lightweight and high-performance polymer components for improving energy efficiency, driving range, and vehicle safety

- The widespread adoption is further supported by strong R&D capabilities, high disposable incomes, and a technologically inclined workforce, establishing polymers as a preferred material for battery, interior, and exterior components

U.S. Electric Vehicles Polymer Market Insight

The U.S. electric vehicles polymer market captured the largest revenue share in North America in 2025, fueled by rapid EV adoption and growing consumer demand for energy-efficient vehicles. Automakers are increasingly integrating engineering plastics and elastomers in battery housings, interior panels, and exterior parts to reduce vehicle weight and enhance performance. Government policies promoting clean transportation and investment in polymer R&D further drive market growth. Moreover, partnerships between polymer suppliers and EV manufacturers are supporting the development of cost-effective, high-performance polymer solutions.

Europe Electric Vehicles Polymer Market Insight

The Europe electric vehicles polymer market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict environmental regulations, rising EV adoption, and the push for sustainable automotive materials. The region’s focus on reducing vehicle emissions and promoting lightweight components fosters polymer integration in powertrain, interiors, and exteriors. European OEMs are also leveraging high-performance polymers for EV battery components to enhance safety and durability.

Germany Electric Vehicles Polymer Market Insight

The Germany electric vehicles polymer market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong automotive industry, emphasis on innovation, and focus on sustainability. Increasing demand for lightweight, high-strength polymers in EVs supports the shift from metal to polymer-based components. The integration of advanced polymers in battery enclosures, chassis, and interiors is becoming widespread, meeting consumer expectations for efficiency, safety, and eco-friendliness.

U.K. Electric Vehicles Polymer Market Insight

The U.K. electric vehicles polymer market is expected to witness the fastest growth rate from 2026 to 2033, driven by government initiatives promoting low-emission vehicles, growing EV adoption, and increasing investments in lightweight materials. Automakers in the U.K. are incorporating high-performance polymers in battery housings, interior panels, and exterior components to reduce vehicle weight and enhance energy efficiency. The focus on sustainable transportation, combined with R&D in advanced polymer solutions, is supporting market expansion across both passenger and commercial electric vehicles.

Asia-Pacific Electric Vehicles Polymer Market Insight

The Asia-Pacific electric vehicles polymer market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, rising disposable incomes, and government support for EV adoption in countries such as China, Japan, and India. The region is emerging as a hub for EV production and polymer component manufacturing, enabling affordable, high-quality polymer solutions for large-scale EV deployment. Growing awareness of energy-efficient and sustainable vehicles is further boosting demand for lightweight polymers in APAC.

Japan Electric Vehicles Polymer Market Insight

The Japan electric vehicles polymer market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced automotive technology, high EV adoption, and emphasis on vehicle safety and efficiency. Japanese OEMs are increasingly integrating engineering plastics and elastomers in interiors, exteriors, and battery components to reduce weight and enhance driving range. The government’s promotion of sustainable mobility and focus on research in polymer innovations further supports market expansion.

China Electric Vehicles Polymer Market Insight

The China electric vehicles polymer market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly growing EV market, supportive government policies, and large-scale production capabilities. China is a major hub for polymer component manufacturing, providing affordable, high-performance materials for battery, interior, and exterior parts. Rising consumer demand for energy-efficient vehicles, combined with investments in advanced polymer technologies, is propelling the market in China.

Electric Vehicles Polymer Market Share

The Electric Vehicles Polymer industry is primarily led by well-established companies, including:

• BASF SE (Germany)

• DuPont (U.S.)

• Dow (U.S.)

• Covestro AG (Germany)

• Celanese Corporation (U.S.)

• SABIC (Saudi Arabia)

• Solvay (Belgium)

• LANXESS (Germany)

• LG Chem (South Korea)

• Asahi Kasei Corporation (Japan)

• Evonik Industries AG (Germany)

• DAIKIN INDUSTRIES, Ltd. (Japan)

• Arkema (France)

• Mitsubishi Engineering-Plastics Corporation (Japan)

• JSR Corporation (Japan)

• AGC Chemicals Americas (U.S.)

• Sumitomo Chemical Co., Ltd. (Japan)

• LyondellBasell Industries Holdings B.V. (Netherlands)

• Elkem ASA (Norway)

• DSM (Netherlands)

Latest Developments in Global Electric Vehicles Polymer Market

- In April 2024, BASF SE inaugurated a new polymer compounding plant in Shanghai, China, to produce advanced engineering plastics for electric vehicles. The facility expands supply to major EV manufacturers in Asia, supporting lightweight components, improving energy efficiency, and strengthening BASF’s presence in the EV polymer market

- In May 2024, DuPont announced a strategic partnership with BYD to co-develop high-performance polymers for lightweight and fire-resistant EV battery enclosures. The collaboration enhances battery safety, vehicle efficiency, and supports BYD’s next-generation electric vehicle models

- In June 2024, Solvay launched a recyclable polymer for EV interior components, targeting automakers focused on sustainability. The new material helps meet stricter environmental regulations, reduces carbon footprint, and boosts demand for eco-friendly automotive polymers

- In July 2024, LG Chem signed a multi-year supply contract with Tesla to provide advanced polymers for battery packs and structural components. This reduces vehicle weight, enhances performance, and supports Tesla’s commitment to energy-efficient, high-performance EVs

- In August 2024, SABIC opened a dedicated polymer innovation center in the Netherlands, focused on developing lightweight chassis materials and EV battery housings. The center accelerates R&D, fosters technological innovation, and strengthens SABIC’s market position in EV polymers

- In September 2024, Covestro acquired Polymatech, a startup specializing in high-performance polymers for EV powertrain and thermal management systems, for USD 120 million. The acquisition expands Covestro’s product portfolio, enhances R&D capabilities, and strengthens its EV market footprint

- In January 2025, Toray Industries launched a carbon fiber-reinforced polymer for EV body panels. The new material reduces vehicle weight, improves crash safety, and offers high structural durability, supporting automakers in meeting performance and efficiency targets

- In February 2025, Celanese Corporation secured a contract to supply advanced polymer solutions for Rivian’s next-generation electric SUVs. The polymers support lightweight and durable interior and exterior components, improving vehicle efficiency and sustainability

- In March 2025, Arkema announced a USD 200 million investment in a new EV polymer production facility in Texas. The plant will produce specialty polymers for batteries and charging infrastructure, increasing manufacturing capacity and supporting market expansion

- In April 2025, DSM Engineering Materials partnered with Hyundai Motor Company to develop bio-based polymers for EV platforms. The collaboration promotes sustainable, high-performance materials for electric vehicles and strengthens both companies’ positions in the EV polymer market

- In May 2025, Mitsubishi Chemical Holdings appointed a new CEO to drive growth and innovation in its EV polymer segment. The leadership change aims to accelerate global expansion, R&D initiatives, and strengthen the company’s competitive edge

- In June 2025, Eastman Chemical launched a thermoplastic polymer for EV battery thermal management. The material improves safety, energy efficiency, and overall performance, supporting OEMs in producing reliable, high-performance electric vehicles

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Electric Vehicles Polymer Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Electric Vehicles Polymer Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Electric Vehicles Polymer Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.