Global Electrically Conductive Adhesives Market

Market Size in USD Billion

USD

3.62 Billion

USD

6.94 Billion

2025

2033

USD

3.62 Billion

USD

6.94 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.62 Billion | |

| USD 6.94 Billion | |

| % | |

|

Electrically Conductive Adhesive Market Overview

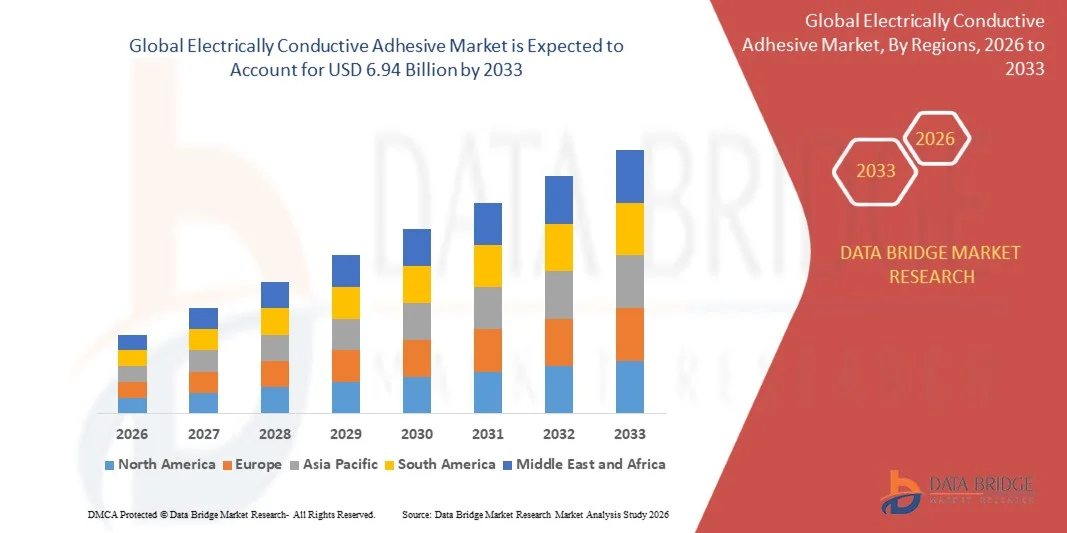

The Electrically Conductive Adhesive Market was valued at USD 3.62 billion in 2025 and is projected to reach USD 6.94 billion by 2033, growing at a CAGR of 8.48% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for miniaturized electronic devices, rising adoption of advanced packaging technologies, and expanding applications across consumer electronics, automotive electronics, renewable energy systems, and telecommunications.

The growing shift toward lightweight and lead-free interconnection solutions, coupled with stringent environmental regulations restricting conventional soldering materials, is encouraging manufacturers to adopt electrically conductive adhesives. These adhesives provide reliable electrical conductivity, improved thermal performance, and compatibility with sensitive electronic components, making them essential for printed circuit boards, semiconductor packaging, display assemblies, sensors, and electric vehicle electronics. Continuous advancements in conductive filler technologies and flexible electronics are further accelerating market expansion across both developed and emerging economies.

Key Market Trends & Insights

- North America dominated the Electrically Conductive Adhesive Market with the largest revenue share of 34.18% in 2025, supported by strong demand from the electronics, aerospace, automotive, and semiconductor industries, along with continuous investments in advanced manufacturing technologies.

- The Isotropic Conductive Adhesives segment led the market with a 63.48% share in 2025, driven by widespread adoption across printed circuit boards, semiconductor packaging, automotive electronics, and industrial electronic assemblies

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by increasing investments in electric vehicles, advanced electronics manufacturing, renewable energy systems, and 5G infrastructure development.

- Anisotropic Conductive Adhesives are the fastest-growing type, projected to register a CAGR of 8.4%, reflecting the surge in demand for high-precision electronic assembly and advanced display technologies.

- The Consumer Electronics segment dominated the application category with a 39.64% revenue share in 2025, led by extensive use of conductive adhesives in smartphones, tablets, wearables, displays, laptops, and other electronic devices.

- Epoxy accounted for 46.72% of the market, preferred by its excellent electrical conductivity, strong adhesion properties, and superior thermal and chemical resistance

- The Silicone segment is the fastest-growing chemistry category, with a CAGR of 8.2%, driven by the increasing demand for flexible and high-temperature-resistant electronic materials.

Market Size & Forecast

- Global Market Value (2025): USD 3.62 Billion

- Expected Market Value (2033): USD 6.94 Billion

- Forecast CAGR (2026–2033): 8.48%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Electrically Conductive Adhesive Market Segmentation

|

Attributes |

Electrically Conductive Adhesive Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Henkel AG & Co. KGaA (Germany) · H.B. Fuller Company (U.S.) · Panacol-Elosol GmbH (Germany) · Master Bond Inc. (U.S.) · Permabond LLC (U.S.) · Dymax Corporation (U.S.) · MG Chemicals (Canada) · Creative Materials Inc. (U.S.) · Aremco Products, Inc. (U.S.) · Epoxy Technology, Inc. (U.S.) · Delo Industrie Klebstoffe GmbH & Co. KGaA (Germany) · ThreeBond Holdings Co., Ltd. (Japan) · Hernon Manufacturing, Inc. (U.S.) · Nagase & Co., Ltd. (Japan) · Mitsubishi Chemical Corporation (Japan) · Panasonic Holdings Corporation (Japan) · Resonac Corporation (Japan) · KYOCERA Corporation (Japan) · Park Aerospace Corp. (U.S.) · Atom Adhesives (U.S.) |

|

Market Opportunities |

· Growing adoption of flexible and wearable electronics · Rising deployment of electric vehicle batteries and power electronics · Increasing investment in advanced semiconductor packaging technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Electrically Conductive Adhesive Market Trends

Trend: Rising Adoption of Flexible and Printed Electronics

Manufacturers are increasingly adopting electrically conductive adhesives in flexible circuits, wearable devices, printed sensors, and foldable displays due to their ability to provide reliable electrical connections without the thermal stress associated with conventional soldering. The growing demand for lightweight, compact, and bendable electronic products is accelerating innovation in adhesive formulations that offer enhanced conductivity, flexibility, and durability. In addition, advancements in printed electronics and smart device technologies are expanding the use of conductive adhesives across next-generation consumer and industrial applications.

For instance, in January 2025, Henkel expanded its conductive adhesive portfolio for flexible hybrid electronics applications, supporting growing demand for wearable devices, smart sensors, and advanced printed electronic assemblies.

Electrically Conductive Adhesive Market Dynamics

Key Market Driver: Increasing Demand from Electric Vehicles and Advanced Electronics

The rapid growth of electric vehicles, battery systems, and advanced electronic components has created substantial demand for electrically conductive adhesives that provide reliable electrical interconnections while reducing overall assembly weight. Automotive manufacturers and electronics producers are increasingly utilizing conductive adhesives in battery packs, sensors, control modules, and power electronics to improve performance, design flexibility, and manufacturing efficiency. The ability of these materials to support miniaturization trends while maintaining conductivity is further strengthening adoption across high-growth end-use industries.

For instance, in March 2024, Parker Hannifin introduced advanced conductive adhesive solutions designed to support electric vehicle battery assemblies and next-generation electronic component integration

Key Restraint/Challenge: High Cost of Silver-Based Conductive Materials

A significant restraint in the Electrically Conductive Adhesive Market is the high cost associated with silver-based conductive fillers used in premium adhesive formulations. These materials provide superior electrical performance and reliability but substantially increase production costs, limiting adoption among price-sensitive manufacturers and applications. Market participants also face challenges related to raw material price volatility, supply chain fluctuations, and maintaining cost competitiveness against conventional soldering technologies, particularly in large-volume consumer electronics production environments.

For instance, fluctuations in global silver prices during 2024 increased manufacturing costs for conductive adhesive producers, creating pricing pressures across electronics and semiconductor supply chains.

Key Market Opportunity: Expansion of Advanced Semiconductor Packaging Technologies

The increasing adoption of advanced semiconductor packaging technologies presents a significant market opportunity. Electrically conductive adhesives are becoming essential for chip packaging, heterogeneous integration, and miniaturized electronic assemblies where conventional joining methods face technical limitations. The ongoing development of high-performance computing devices, artificial intelligence hardware, and next-generation communication systems is further expanding demand for conductive materials that deliver superior electrical and thermal performance while supporting increasingly compact package architectures.

For instance, in 2025, leading semiconductor manufacturers expanded investments in advanced packaging facilities, driving greater utilization of conductive adhesive materials for high-density interconnect and chip integration applications.

Electrically Conductive Adhesive Market Scope

The electrically conductive adhesive market is segmented on the basis of type, application, chemistry, and filler material.

- By Type

On the basis of type, the Electrically Conductive Adhesive Market is segmented into isotropic conductive adhesives and anisotropic conductive adhesives. The Isotropic Conductive Adhesives (ICA) segment dominated the market with a 63.48% share in 2025, owing to its widespread adoption across printed circuit boards, semiconductor packaging, automotive electronics, and industrial electronic assemblies. These adhesives conduct electricity in all directions, making them suitable for a broad range of interconnection applications. Manufacturers prefer ICA products because of their ease of processing, strong bonding performance, and compatibility with automated assembly systems. The segment is benefiting from increasing demand for miniaturized electronic devices and high-density circuit designs. Their ability to replace traditional soldering methods while supporting lead-free manufacturing requirements is further strengthening adoption. Growing investments in consumer electronics and advanced semiconductor manufacturing continue to support the segment’s dominant position globally.

The Anisotropic Conductive Adhesives (ACA) segment is projected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by increasing demand for high-precision electronic assembly and advanced display technologies. These adhesives conduct electricity only in the vertical direction, preventing short circuits between closely spaced conductive tracks. Rising adoption in flexible displays, touch panels, wearable electronics, and semiconductor packaging is accelerating market expansion. Continuous advancements in display manufacturing and flexible electronics are creating new growth opportunities. ACA solutions also support lightweight and compact device architectures required in next-generation consumer electronics. Increasing investments in foldable smartphones, smart sensors, and advanced packaging technologies are expected to further boost demand.

- By Application

On the basis of application, the Electrically Conductive Adhesive Market is segmented into automotive, consumer electronics, aerospace, biosciences, and others. The Consumer Electronics segment dominated the market with a 39.64% share in 2025, driven by extensive use of conductive adhesives in smartphones, tablets, wearables, displays, laptops, and other electronic devices. The trend toward device miniaturization and higher circuit density has significantly increased the demand for reliable conductive bonding solutions. Electrically conductive adhesives offer superior compatibility with heat-sensitive electronic components compared to conventional soldering methods. Growing global demand for smart devices and connected technologies continues to support segment growth. Manufacturers are increasingly utilizing these materials to improve assembly efficiency and product performance. Continuous innovation in consumer electronics and expanding production volumes are sustaining the segment’s market leadership.

The Automotive segment is expected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, fueled by the rapid expansion of electric vehicles, autonomous driving technologies, and advanced driver assistance systems. Modern vehicles require a growing number of sensors, control modules, battery systems, and electronic components that utilize conductive adhesives for reliable electrical connectivity. The shift toward lightweight vehicle designs is encouraging manufacturers to adopt adhesive-based assembly solutions. Electrification trends are creating substantial demand for conductive materials in battery packs and power electronics. Increasing regulatory focus on vehicle efficiency and emissions reduction is further accelerating adoption. Strong investments in automotive electronics innovation are expected to support long-term growth in this segment.

- By Chemistry

On the basis of chemistry, the Electrically Conductive Adhesive Market is segmented into epoxy, silicone, acrylic, polyurethane, and others. The Epoxy segment dominated the market with a 46.72% share in 2025, owing to its excellent electrical conductivity, strong adhesion properties, and superior thermal and chemical resistance. Epoxy-based conductive adhesives are widely used in semiconductor packaging, printed circuit boards, automotive electronics, and industrial electronic assemblies. These materials provide reliable long-term performance under demanding operating conditions. Their compatibility with various conductive fillers, including silver and carbon materials, further enhances their commercial appeal. Growing demand for durable and high-performance electronic interconnections continues to support market expansion. The segment also benefits from extensive use in advanced manufacturing and precision electronic applications.

The Silicone segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by increasing demand for flexible and high-temperature-resistant electronic materials. Silicone-based conductive adhesives provide excellent flexibility, environmental stability, and resistance to thermal cycling, making them suitable for automotive, aerospace, and wearable electronic applications. The growing adoption of flexible electronics and next-generation sensors is supporting demand growth. These materials also perform effectively in harsh environmental conditions where conventional adhesive systems may fail. Rising investments in electric vehicles and advanced electronic systems are creating new opportunities for silicone formulations. Continuous product innovation aimed at improving conductivity and durability is expected to further strengthen segment growth.

- By Filler Material

On the basis of filler material, the Electrically Conductive Adhesive Market is segmented into silver fillers, carbon fillers, copper fillers, and others. The Silver Fillers segment dominated the market with a 54.81% share in 2025, driven by their superior electrical conductivity, reliability, and compatibility with a wide range of adhesive chemistries. Silver-filled conductive adhesives are extensively utilized in semiconductor packaging, consumer electronics, automotive systems, and photovoltaic applications. These fillers enable high-performance electrical connections while supporting miniaturized device architectures. Their ability to deliver stable conductivity over long operational lifecycles makes them highly preferred in critical electronic applications. Increasing demand for advanced electronic components and high-density circuit assemblies continues to support segment dominance. Strong adoption across premium electronics and industrial applications further reinforces their leading market position.

The Copper Fillers segment is expected to witness the fastest growth at a CAGR of 8.9% from 2026 to 2033, fueled by increasing demand for cost-effective alternatives to silver-based conductive materials. Copper fillers offer attractive conductivity characteristics while significantly reducing material costs for manufacturers. Advancements in oxidation-resistant copper technologies are improving performance and expanding commercial adoption. Growing production of consumer electronics, automotive electronics, and industrial devices is creating favorable growth opportunities. Manufacturers are increasingly investing in copper-based formulations to balance performance and cost efficiency. Rising pressure to optimize manufacturing expenses while maintaining electrical performance is expected to accelerate growth within this segment.

Electrically Conductive Adhesive Market Regional Analysis

North America dominated the Electrically Conductive Adhesive Market with the largest revenue share of 34.18% in 2025, supported by strong demand from the electronics, aerospace, automotive, and semiconductor industries, along with continuous investments in advanced manufacturing technologies. The region also benefits from a robust innovation ecosystem, high adoption of electric vehicles, and increasing development of next-generation semiconductor packaging solutions. Growing demand for miniaturized electronic devices, advanced sensors, and high-performance interconnection materials continues to support market expansion. Increasing focus on domestic semiconductor production, electronics supply chain resilience, and technological advancements in conductive materials further strengthens North America’s leadership position in the global market.

U.S. Electrically Conductive Adhesive Market Insight

The U.S. electrically conductive adhesive market is witnessing strong growth due to rising investments in semiconductor manufacturing, electric vehicle production, and advanced electronics development technologies. The country’s mature electronics and automotive ecosystem, along with increasing adoption of high-performance conductive materials for packaging, sensors, and battery systems, is driving demand across industrial, consumer, and aerospace applications. In addition, growing emphasis on domestic semiconductor production and next-generation electronic device innovation is accelerating conductive adhesive adoption across manufacturers and technology companies.

Europe Electrically Conductive Adhesive Market Insight

The Europe electrically conductive adhesive market remains a major contributor to global revenue, driven by strong industrial capabilities, technological innovation, and high demand for advanced electronic assembly solutions. The widespread use of conductive adhesives in automotive electronics, renewable energy systems, and semiconductor packaging applications is supporting market expansion across the region. Increasing investments in sustainable manufacturing technologies, coupled with stringent environmental regulations and strong research capabilities, continue to enhance the adoption of electrically conductive adhesives throughout Europe.

U.K. Electrically Conductive Adhesive Market Insight

The U.K. electrically conductive adhesive market is experiencing steady growth, supported by rising adoption of conductive materials in electronics manufacturing, automotive systems, and aerospace applications. Increasing investments in advanced electronic assembly technologies and growing demand for lightweight, reliable interconnection solutions are contributing to market growth. Furthermore, integration of flexible electronics, smart sensors, and next-generation semiconductor technologies is improving product performance and manufacturing efficiency, positioning the U.K. as a key innovation hub in the electrically conductive adhesive industry.

Germany Electrically Conductive Adhesive Market Insight

The Germany electrically conductive adhesive market is expanding steadily due to the country’s strong automotive manufacturing base, advanced industrial capabilities, and increasing adoption of next-generation electronic materials. Automotive companies, electronics manufacturers, and research institutions are increasingly utilizing conductive adhesives for battery systems, electronic modules, and semiconductor packaging applications. Continuous advancements in electric vehicle technologies, electronics miniaturization, and sustainable manufacturing processes, along with strong government focus on industrial innovation, are further driving market growth in Germany.

Asia-Pacific Electrically Conductive Adhesive Market Insight

The Asia-Pacific electrically conductive adhesive market is expected to witness rapid growth, driven by expanding electronics manufacturing, increasing semiconductor production, and rising investments in electric vehicle infrastructure across countries such as China, India, Japan, and South Korea. Growing demand for consumer electronics, rising adoption of advanced packaging technologies, and increasing need for cost-effective interconnection solutions are supporting regional market expansion. In addition, the growing presence of global electronics supply chains and semiconductor fabrication facilities is accelerating conductive adhesive adoption across commercial and industrial sectors.

Japan Electrically Conductive Adhesive Market Insight

The Japan electrically conductive adhesive market is witnessing consistent growth due to rising investments in semiconductor technologies, electronics innovation, and advanced manufacturing initiatives. Electronics manufacturers, automotive companies, and research organizations are increasingly adopting conductive adhesives for high-density packaging, sensors, and precision electronic assemblies. Moreover, increasing integration of flexible electronics and the country’s focus on advanced mobility and smart technology solutions are further contributing to market growth.

China Electrically Conductive Adhesive Market Insight

The China electrically conductive adhesive market is growing rapidly, driven by expanding electronics production, increasing semiconductor manufacturing capacity, and rising government support for advanced technology industries. Growing adoption of conductive materials across consumer electronics, electric vehicles, renewable energy systems, and telecommunications sectors is significantly boosting market demand. In addition, rising investments in semiconductor packaging, increasing focus on domestic technology development, and rapid industrial modernization are positioning China as one of the fastest-growing markets for electrically conductive adhesives globally.

Electrically Conductive Adhesive Market Share

The electrically conductive adhesive industry is primarily led by well-established companies, including:

- Henkel AG & Co. KGaA (Germany)

- B. Fuller Company (U.S.)

- Panacol-Elosol GmbH (Germany)

- Master Bond Inc. (U.S.)

- Permabond LLC (U.S.)

- Dymax Corporation (U.S.)

- MG Chemicals (Canada)

- Creative Materials Inc. (U.S.)

- Aremco Products, Inc. (U.S.)

- Epoxy Technology, Inc. (U.S.)

- Delo Industrie Klebstoffe GmbH & Co. KGaA (Germany)

- ThreeBond Holdings Co., Ltd. (Japan)

- Hernon Manufacturing, Inc. (U.S.)

- Nagase & Co., Ltd. (Japan)

- Mitsubishi Chemical Corporation (Japan)

- Panasonic Holdings Corporation (Japan)

- Resonac Corporation (Japan)

- KYOCERA Corporation (Japan)

- Park Aerospace Corp. (U.S.)

- Atom Adhesives (U.S.)

Latest Developments in Electrically Conductive Adhesive Market

- In September 2024, Panacol announced the launch of Elecolit® 3648, a newly developed electrically conductive adhesive designed for flexible perovskite and organic photovoltaic (OPV) applications. The one-component conductive adhesive enables reliable electrical connections on temperature-sensitive substrates and supports the growing adoption of flexible solar cells, wearable electronics, and printed electronics. The product was developed to improve manufacturing efficiency while maintaining flexibility and conductivity in advanced electronic applications

- In November 2022, Henkel announced the launch of LOCTITE ABLESTIK ICP 2120, an innovative moisture-curing electrically conductive adhesive developed for compact camera modules in mobile devices. The product provides reliable electrical grounding, room-temperature curing capability, and protection for heat-sensitive substrates, helping electronics manufacturers improve yields and reliability while supporting increasingly miniaturized device designs

- In July 2022, Panacol highlighted expanded commercialization activities for its Elecolit conductive adhesive portfolio, focusing on electrically conductive bonding solutions for PCB assembly, die attach, shielding, and advanced electronics manufacturing. The development reflected increasing industry demand for lead-free conductive interconnection technologies across semiconductor and electronics applications

- In October 2021, DuPont continued expanding the deployment of advanced adhesive materials for electric vehicle battery systems and high-performance electronics manufacturing. The company emphasized the use of innovative adhesive technologies to improve thermal management, assembly performance, and component integration in next-generation mobility and electronics applications

- In June 2021, DuPont introduced BETASEAL™ 900EI, a next-generation adhesive solution for electric vehicle battery pack assembly. The technology was developed to improve battery pack manufacturing efficiency, reduce assembly complexity, and support advanced EV architectures, highlighting the growing role of specialty adhesive technologies in electrified transportation systems

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Electrically Conductive Adhesives Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Electrically Conductive Adhesives Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Electrically Conductive Adhesives Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.