Global Electron Beam Machining Market

Market Size in USD Billion

USD

222.50 Billion

USD

292.98 Billion

2025

2033

USD

222.50 Billion

USD

292.98 Billion

2025

2033

| 2026 - 2033 | |

| USD 222.50 Billion | |

| USD 292.98 Billion | |

| % | |

|

Electron Beam Machining Market Size

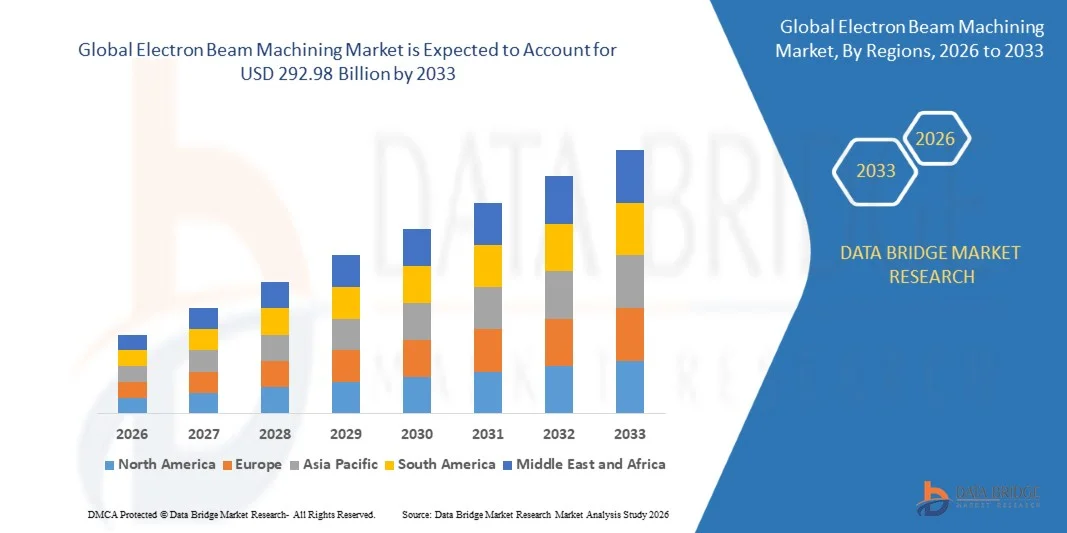

- The global electron beam machining market size was valued at USD 222.50 billion in 2025and is expected to reach USD 292.98 billion by 2033, at a CAGR of 3.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for high-precision manufacturing techniques in aerospace, automotive, and electronics industries, where complex and micro-scale components require superior accuracy and surface quality

- Rising adoption of advanced machining processes in medical device manufacturing and semiconductor production is further supporting market expansion due to the need for contamination-free and highly controlled processing environments

Electron Beam Machining Market Analysis

- The market is witnessing steady growth due to the rising shift toward non-contact and high-energy beam-based machining technologies that offer improved efficiency and reduced material distortion

- Increasing investments in advanced manufacturing and Industry 4.0 technologies are enhancing the integration of electron beam machining in automated production systems

- North America dominated the electron beam machining market with the largest revenue share in 2025, driven by increasing demand for high-precision manufacturing technologies across aerospace, automotive, electronics, and defense industries

- Asia-Pacific region is expected to witness the highest growth rate in the global electron beam machining market, driven by expanding manufacturing activities, rising semiconductor production, increasing aerospace investments, and growing adoption of advanced machining technologies across emerging economies

- The stainless steel segment held the largest market revenue share in 2025 driven by its extensive use in automotive, aerospace, medical, and industrial applications requiring high precision machining and superior corrosion resistance. Stainless steel materials are widely preferred due to their durability, machinability, and compatibility with advanced electron beam processing technologies

Report Scope and Electron Beam Machining Market Segmentation

|

Attributes |

Electron Beam Machining Key Market Insights |

|

Segments Covered |

· By Material: Stainless Steel, Titanium, Nickel, and Others · By Equipment: Cathode, Annular Bias Grid, and Others · By Application: Welding, Drilling, and Surface Treatment · By Industry: Automotive, Aerospace and Defense, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Global Beam Technologies AG (Germany) |

|

Market Opportunities |

• Aerospace And Defense Applications Expansion |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Electron Beam Machining Market Trends

“Advancement In High-Precision And Non-Contact Machining Technologies”

- The increasing shift toward high-precision manufacturing is significantly driving the adoption of electron beam machining systems, as industries demand superior accuracy, minimal thermal distortion, and enhanced surface quality for complex components. This technology is gaining traction in aerospace, automotive, and electronics sectors due to its ability to machine hard and heat-resistant materials with exceptional precision. The trend is further supported by growing demand for miniaturized and complex geometries in advanced engineering applications

- Rising integration of automation, digital control systems, and Industry 4.0 technologies is enhancing the efficiency and scalability of electron beam machining processes. Manufacturers are increasingly adopting AI-based monitoring and real-time process optimization to improve productivity and reduce operational errors. This is strengthening the role of electron beam machining in smart manufacturing environments and high-value production lines

- Expanding applications in semiconductor fabrication, medical devices, and defense manufacturing are accelerating market demand, as these industries require contamination-free and highly controlled machining environments. The ability of electron beam machining to deliver ultra-fine precision without physical contact is making it suitable for critical and sensitive component production

- For instance, in 2024, leading aerospace manufacturers in Germany and the U.S. increased the use of electron beam machining for turbine blades and engine components, driven by demand for lightweight, high-performance materials. These applications improved production accuracy, reduced material waste, and enhanced overall component durability in extreme operating conditions

- While adoption is increasing, market growth depends on continued technological advancements, improved energy efficiency, and cost optimization of electron beam systems. Manufacturers are also focusing on enhancing system reliability and scalability to support wider industrial adoption across emerging precision engineering applications

Electron Beam Machining Market Dynamics

Driver

“Rising Demand For Precision Engineering And Advanced Manufacturing Processes”

- Growing need for high-accuracy machining in aerospace, automotive, and electronics industries is a major driver of the electron beam machining market, as manufacturers seek advanced solutions for processing complex and high-strength materials. The technology enables precise cutting, welding, and drilling with minimal thermal impact, making it highly suitable for critical engineering applications

- Increasing use of high-performance materials such as titanium alloys, superalloys, and composites is further boosting demand for electron beam machining systems. These materials are widely used in aerospace and defense applications, where conventional machining methods often face limitations in achieving required precision and structural integrity

- Expansion of semiconductor and microelectronics manufacturing is also supporting market growth, as electron beam machining is widely used for micro-scale fabrication and component structuring. The demand for smaller, more powerful electronic devices is encouraging manufacturers to adopt advanced beam-based machining solutions for improved accuracy and efficiency

- For instance, in 2023, major electronics manufacturers in Japan and South Korea adopted electron beam machining systems for micro-component fabrication used in semiconductor devices and precision sensors. This adoption improved production consistency, reduced defect rates, and enhanced miniaturization capabilities in high-tech electronic products

- Despite strong demand, market expansion depends on technological advancements, skilled workforce availability, and cost reduction of equipment and maintenance. Continuous innovation in beam control systems and energy efficiency will be critical for sustaining long-term growth and industrial adoption

Restraint/Challenge

“High Capital Investment And Operational Complexity”

- The high cost of electron beam machining equipment remains a significant challenge, limiting adoption among small and medium-scale manufacturers. The requirement for vacuum systems, specialized infrastructure, and advanced control units increases initial investment and operational expenses, making it less accessible for cost-sensitive industries

- Technical complexity and the need for highly skilled operators also restrict widespread adoption, as system setup, maintenance, and process optimization require specialized expertise. This creates barriers for industries lacking trained personnel or advanced manufacturing capabilities

- Limited flexibility compared to conventional machining methods further challenges market growth, as electron beam machining is primarily suitable for specific high-precision applications. This restricts its use in mass production environments where cost efficiency and versatility are critical

- For instance, in 2024, several mid-sized manufacturing firms in Southeast Asia reported delayed adoption of electron beam machining systems due to high installation costs and lack of trained technical staff. In addition, maintenance requirements and vacuum chamber constraints increased operational downtime and reduced overall cost efficiency

- Addressing these challenges will require technological simplification, cost-effective system development, and expanded training programs for operators. Improvements in automation, modular system design, and service support infrastructure will be essential to enhance adoption and unlock broader market potential globally

Electron Beam Machining Market Scope

The market is segmented on the basis of material, equipment, application, and industry.

- By Material

On the basis of material, the electron beam machining market is segmented into Stainless Steel, Titanium, Nickel, and Others. The stainless steel segment held the largest market revenue share in 2025 driven by its extensive use in automotive, aerospace, medical, and industrial applications requiring high precision machining and superior corrosion resistance. Stainless steel materials are widely preferred due to their durability, machinability, and compatibility with advanced electron beam processing technologies.

The titanium segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand from aerospace and defense industries where lightweight, high-strength, and heat-resistant materials are essential. Titanium components are increasingly processed using electron beam machining due to the technology’s ability to achieve high precision with minimal thermal distortion.

- By Equipment

On the basis of equipment, the electron beam machining market is segmented into Cathode, Annular Bias Grid, and Others. The cathode segment held the largest market revenue share in 2025 driven by its critical role in generating and controlling electron beams during machining processes. Cathodes are extensively utilized in industrial electron beam systems due to their operational stability, efficiency, and ability to support high-precision manufacturing applications.

The annular bias grid segment is expected to witness the fastest growth rate from 2026 to 2033, driven by advancements in beam control technologies and increasing demand for enhanced machining accuracy. Annular bias grids help improve beam focusing and process stability, making them increasingly important in high-performance and micro-machining applications.

- By Application

On the basis of application, the electron beam machining market is segmented into Welding, Drilling, and Surface Treatment. The welding segment held the largest market revenue share in 2025 driven by increasing demand for high-strength and precision joining processes in aerospace, automotive, and heavy industrial sectors. Electron beam welding offers deep penetration, minimal material distortion, and superior weld quality, making it highly suitable for complex engineering applications.

The drilling segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising demand for micro-drilling and high-precision hole manufacturing in electronics, aerospace, and medical device industries. Electron beam drilling enables accurate machining of extremely small and complex holes with high speed and efficiency.

- By Industry

On the basis of industry, the electron beam machining market is segmented into Automotive, Aerospace and Defense, and Others. The aerospace and defense segment held the largest market revenue share in 2025 driven by the increasing use of high-performance alloys and precision-engineered components in aircraft and defense systems. Electron beam machining is widely adopted in this industry due to its capability to process complex geometries and heat-resistant materials with exceptional accuracy.

The automotive segment is expected to witness the fastest growth rate from 2026 to 2033, driven by growing demand for lightweight vehicle components, electric vehicle production, and advanced manufacturing technologies. Automotive manufacturers are increasingly utilizing electron beam machining to improve production efficiency, component durability, and precision in critical applications.

Electron Beam Machining Market Regional Analysis

- North America dominated the electron beam machining market with the largest revenue share in 2025, driven by increasing demand for high-precision manufacturing technologies across aerospace, automotive, electronics, and defense industries

- Industries in the region highly value the superior machining accuracy, minimal thermal distortion, and advanced material processing capabilities offered by electron beam machining systems for critical and complex engineering applications

- This widespread adoption is further supported by strong technological infrastructure, rising investments in advanced manufacturing, and the growing integration of automation and Industry 4.0 technologies, establishing electron beam machining as an essential solution for high-performance industrial production

U.S. Electron Beam Machining Market Insight

The U.S. electron beam machining market captured the largest revenue share in 2025 within North America, fueled by increasing investments in aerospace, defense, and semiconductor manufacturing industries. Manufacturers are increasingly prioritizing high-precision machining technologies to improve production efficiency and component quality. The growing adoption of automation, advanced robotics, and smart manufacturing systems further supports market expansion. Moreover, strong research and development activities and the presence of leading manufacturing companies are significantly contributing to the growth of the electron beam machining industry in the U.S.

Europe Electron Beam Machining Market Insight

The Europe electron beam machining market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by rising demand for advanced manufacturing technologies and precision engineering solutions. The increasing use of lightweight and high-strength materials in aerospace and automotive industries is encouraging adoption of electron beam machining systems. European manufacturers are also focusing on sustainable and energy-efficient production technologies, further supporting market growth. The region is witnessing increasing deployment of advanced machining technologies across industrial and defense applications.

U.K. Electron Beam Machining Market Insight

The U.K. electron beam machining market is expected to witness the fastest growth rate from 2026 to 2033, driven by growing investments in aerospace engineering, automotive innovation, and advanced industrial manufacturing. The increasing focus on precision manufacturing and high-performance component production is encouraging adoption of electron beam machining technologies. In addition, the country’s emphasis on automation and digital manufacturing systems is supporting technological advancements in machining processes. The presence of established aerospace and defense manufacturers is also contributing to market expansion.

Germany Electron Beam Machining Market Insight

The Germany electron beam machining market is expected to witness the fastest growth rate from 2026 to 2033, fueled by the country’s strong industrial manufacturing base and increasing focus on engineering excellence. Germany’s advanced automotive and aerospace sectors are driving demand for high-precision machining technologies capable of processing complex and heat-resistant materials. The integration of Industry 4.0 technologies and smart production systems is further supporting market adoption. In addition, rising investments in research and industrial automation are strengthening the country’s position in advanced manufacturing technologies.

Asia-Pacific Electron Beam Machining Market Insight

The Asia-Pacific electron beam machining market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, increasing manufacturing activities, and expanding electronics and automotive industries in countries such as China, Japan, and India. The region’s growing focus on advanced manufacturing and precision engineering is accelerating adoption of electron beam machining systems. Furthermore, increasing investments in semiconductor manufacturing and aerospace development are supporting market growth. Rising affordability of advanced manufacturing technologies is also expanding market opportunities across emerging economies.

Japan Electron Beam Machining Market Insight

The Japan electron beam machining market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced electronics industry, strong robotics sector, and emphasis on precision engineering. Japanese manufacturers are increasingly utilizing electron beam machining technologies for semiconductor fabrication, automotive components, and high-performance industrial applications. The integration of automation and AI-driven manufacturing systems is further driving market growth. Moreover, increasing demand for miniaturized and high-precision electronic components is strengthening adoption across multiple industries.

China Electron Beam Machining Market Insight

The China electron beam machining market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrial expansion, strong manufacturing capabilities, and increasing investments in aerospace, electronics, and automotive industries. China is emerging as a major hub for advanced manufacturing technologies, with growing adoption of precision machining systems across industrial sectors. The expansion of semiconductor production and smart manufacturing initiatives is further driving market demand. In addition, government support for industrial modernization and technological innovation is significantly contributing to the growth of the electron beam machining market in China.

Electron Beam Machining Market Share

The Electron Beam Machining industry is primarily led by well-established companies, including:

- Global Beam Technologies AG (Germany)

- Mitsubishi Electric Corporation (Japan)

- pro-beam (Germany)

- C. Instruments (Canada)

- Cambridge Vacuum Engineering (U.K.)

- Sciaky Inc., (U.S.)

- Bodycote (U.K.)

- EB Industries (U.S.)

- Beijing Zhong Ke Electric Co.Ltd. (China)

- Sodick (Japan)

- FOCUS GmbH (Germany)

- Evobeam GmbH (Germany)

- Josch Strahlschweißtechnik GmbH (Germany)

- Acceleron Inc (U.S.)

- AVIC (China)

Latest Developments in Global Electron Beam Machining Market

- In March 2025, SLAC National Accelerator Laboratory announced a breakthrough in electron beam technology by achieving a peak beam current of 100 kA for femtosecond durations. This development is expected to enhance high-speed and ultra-precision materials processing capabilities across advanced manufacturing industries. The innovation enables improved efficiency and accuracy in processing complex materials while expanding research opportunities in next-generation machining technologies. It is anticipated to strengthen technological advancements and accelerate adoption of electron beam systems in aerospace, semiconductor, and high-performance industrial applications

- In January 2025, JEOL launched the JAM-5200EBM 6 kW additive manufacturing unit featuring extended cathode life and improved operational efficiency. The new system is designed to enhance production reliability and reduce maintenance frequency in industrial electron beam manufacturing processes. This development supports cost optimization and improved productivity for manufacturers utilizing advanced additive manufacturing technologies. The launch is expected to strengthen JEOL’s market presence while supporting broader adoption of electron beam-based manufacturing systems across aerospace and precision engineering industries

- In August 2024, Hitachi High-Tech introduced advanced X-ray analytics solutions focused on improving quality control for electric vehicle battery manufacturing. The technology is designed to enhance inspection accuracy, detect material defects, and improve overall production reliability in battery systems. This innovation supports growing demand for high-performance EV batteries while improving manufacturing precision and operational efficiency. The development is expected to accelerate adoption of advanced beam and inspection technologies in the automotive and electronics industries

- In June 2024, TWI Global highlighted the advantages of electron beam welding technology by demonstrating up to 95% strength retention compared to base metal structures. The development emphasizes the effectiveness of electron beam welding in producing strong, durable, and high-quality joints for aerospace, automotive, and industrial applications. This advancement is expected to increase confidence in beam-based welding technologies for critical engineering components. It also strengthens market demand for advanced electron beam solutions by showcasing superior performance and structural reliability in precision manufacturing processes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.