Global Emission Monitoring System Market

Market Size in USD Billion

USD

4.51 Billion

USD

9.53 Billion

2025

2033

USD

4.51 Billion

USD

9.53 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.51 Billion | |

| USD 9.53 Billion | |

| % | |

|

Emission Monitoring System Market Overview

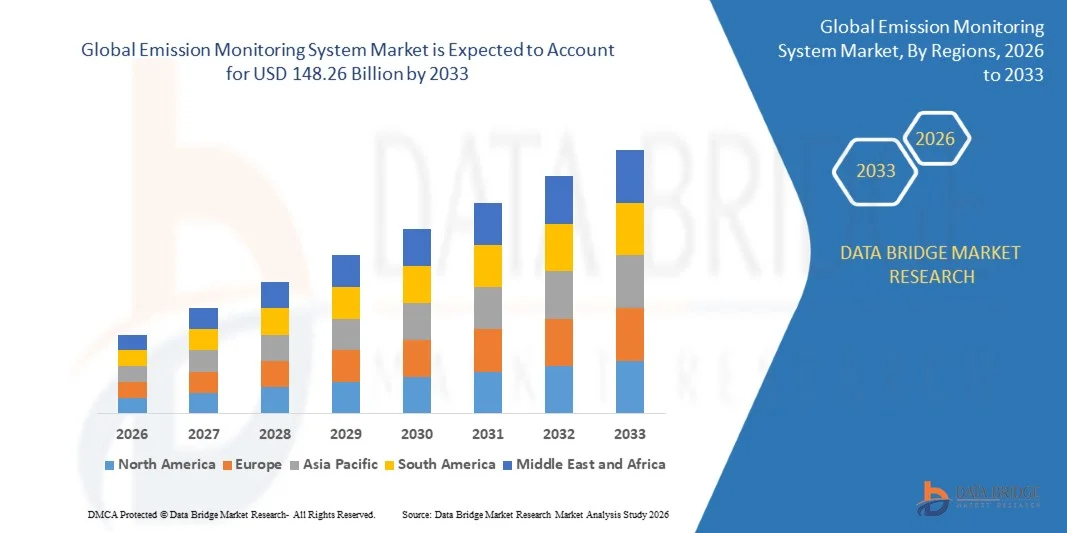

The Emission Monitoring System Market was valued at USD 36.38 billion in 2025 and is projected to reach USD 148.26 billion by 2033, growing at a CAGR of 19.20% from 2026 to 2033. The market is experiencing robust growth driven by increasingly stringent environmental regulations, rising industrial focus on emission control and sustainability, and growing adoption of real-time monitoring technologies across power generation, oil & gas, chemicals, cement, and manufacturing industries.

Governments and environmental agencies worldwide are implementing stricter air quality standards and carbon emission reduction targets, compelling industries to deploy advanced emission monitoring systems for continuous compliance and reporting. Continuous Emission Monitoring Systems (CEMS), predictive analytics platforms, and IoT-enabled monitoring solutions are increasingly replacing traditional periodic testing methods by providing real-time data, automated reporting, and enhanced operational transparency. The rapid expansion of industrial activities, combined with growing investments in smart environmental monitoring infrastructure and decarbonization initiatives, is further accelerating adoption across both developed and emerging economies.

Key Market Trends & Insights

- North America dominated the emission monitoring system market with the largest revenue share of approximately 36.8% in 2025, supported by stringent environmental compliance requirements, widespread deployment of continuous emission monitoring systems across industrial facilities, and strong regulatory oversight from environmental agencies. The region also benefits from advanced industrial infrastructure and high adoption of digital monitoring technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 21.1% from 2026 to 2033. Growth is driven by rapid industrialization, increasing environmental awareness, stricter emission control regulations, expanding power generation capacity, and significant investments in air quality monitoring infrastructure across China, India, Japan, and Southeast Asian countries.

- The Solution Type segment held the largest market revenue share of approximately 68.9% in 2025 driven by widespread deployment of continuous emission monitoring systems (CEMS), gas analyzers, particulate monitoring equipment, and environmental data management platforms across industrial facilities. Organizations prefer integrated monitoring solutions due to their ability to provide real-time emission tracking, automated reporting, and regulatory compliance management.

- The Service Type segment is projected to register the fastest growth at a CAGR of 20.7% from 2026 to 2033, driven by rising demand for system maintenance, calibration, consulting, managed monitoring services, and regulatory compliance support. Increasing complexity of environmental regulations and growing outsourcing of monitoring operations are accelerating segment expansion.

- The Software as A Service segment accounted for the largest market revenue share of approximately 56.4% in 2025 owing to increasing adoption of cloud-based emission monitoring software, environmental reporting platforms, and analytics solutions that enable remote monitoring and regulatory compliance management.

- The Platform as A Service segment is anticipated to witness the fastest growth at a CAGR of 21.4% from 2026 to 2033, supported by growing demand for customizable environmental data platforms, AI-driven analytics tools, and scalable integration capabilities for industrial IoT-based emission monitoring applications.

- The Large Enterprises segment dominated the market with a revenue share of approximately 71.6% in 2025 due to extensive regulatory compliance obligations, larger industrial operations, and substantial investments in environmental sustainability initiatives. Large enterprises are major adopters of advanced monitoring technologies across energy, manufacturing, chemical, and mining industries.

- The Small and Medium Enterprises segment is expected to register the fastest CAGR of 20.2% from 2026 to 2033, driven by increasing regulatory enforcement, growing awareness regarding environmental compliance, and rising availability of cost-effective cloud-based monitoring solutions.

- The Private Cloud segment held the largest market revenue share of approximately 44.8% in 2025 driven by increasing concerns regarding industrial data security, regulatory compliance requirements, and the need for greater control over sensitive environmental and operational information.

- The Hybrid Cloud segment is projected to witness the fastest growth at a CAGR of 22.1% from 2026 to 2033, supported by growing demand for flexible deployment architectures that combine on-premise infrastructure with cloud-based analytics, enabling organizations to optimize performance, scalability, and compliance management across geographically distributed industrial facilities.

Market Size & Forecast

- Global Market Value (2025): USD 36.38 Billion

- Expected Market Value (2033): USD 148.26 Billion

- Forecast CAGR (2026–2033): 19.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Emission Monitoring System Market Segmentation

|

Attributes |

Emission Monitoring System Key Market Insights |

|

Segments Covered |

· By Type: Solution Type and Service Type · By Service Model: Software as A Service, Platform as A Service, and Infrastructure as A Service · By Organisation Size: Small and Medium Enterprises and Large Enterprises · By Deployment Model: Public Cloud, Private Cloud, and Hybrid Cloud |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Oracle Corporation (U.S.) |

|

Market Opportunities |

• Expansion Of Carbon Capture And Storage Monitoring Applications • Growing Adoption Of AI-Powered Emission Analytics And Predictive Compliance Solutions |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Emission Monitoring System Market Trends

Trend: Increasing Adoption Of AI-Enabled Continuous Emission Monitoring And Real-Time Environmental Compliance

Growing regulatory pressure to reduce industrial emissions and improve environmental transparency is accelerating demand for advanced emission monitoring technologies across power generation, oil & gas, chemicals, cement, mining, and manufacturing sectors. Traditional manual sampling and periodic inspections often fail to provide continuous visibility into emission levels, encouraging industries to adopt automated monitoring systems capable of delivering real-time data, predictive alerts, and regulatory reporting with higher accuracy.

Industrial operators are increasingly integrating Continuous Emission Monitoring Systems (CEMS), cloud-based analytics platforms, and IoT-enabled sensors to monitor pollutants such as carbon dioxide (CO₂), sulfur dioxide (SO₂), nitrogen oxides (NOx), particulate matter, and volatile organic compounds. For instance, power utilities are deploying AI-driven monitoring platforms to optimize combustion efficiency while maintaining regulatory compliance. In industrial facilities, real-time monitoring solutions are helping reduce environmental risks, improve operational performance, and streamline reporting requirements for environmental authorities.

The rapid expansion of environmental, social, and governance (ESG) initiatives is further driving adoption of advanced emission monitoring technologies. In addition, governments worldwide are strengthening carbon reporting requirements and air quality regulations, increasing demand for automated compliance solutions. In 2025, several large utility operators across Europe and North America reported reductions of approximately 15–20% in compliance-related operational incidents after implementing AI-enabled continuous emission monitoring platforms integrated with predictive maintenance systems.

Emission Monitoring System Market Dynamics

Key Market Driver: Stringent Environmental Regulations And Rising Industrial Emission Compliance Requirements

Governments and environmental agencies worldwide are implementing increasingly strict regulations to control industrial emissions, improve air quality, and support climate change mitigation initiatives. Industries are facing mounting pressure to continuously monitor emissions, maintain regulatory compliance, and reduce environmental impacts, creating strong demand for advanced monitoring technologies capable of delivering accurate and real-time emission data.

Industries such as power generation, refining, chemicals, metals, and cement manufacturing are increasingly investing in emission monitoring systems to comply with environmental regulations and avoid operational penalties. For instance, operators are deploying CEMS solutions to continuously track emissions from boilers, furnaces, stacks, and industrial processing units. Regulatory frameworks including the U.S. Clean Air Act, the European Industrial Emissions Directive, and China's ultra-low emission policies continue to accelerate technology adoption across industrial facilities.

Similarly, environmental agencies are requiring more frequent and automated reporting of emission levels, increasing the need for digital monitoring infrastructure. Real-world industrial installations across the U.S. and Germany during 2024 demonstrated that facilities equipped with advanced continuous monitoring systems improved reporting accuracy by approximately 25–35% while significantly reducing compliance management costs.

Key Restraint/Challenge: High Implementation Costs And Complex System Integration Requirements

Advanced emission monitoring systems require substantial investments in hardware, software, calibration equipment, communication infrastructure, and ongoing maintenance services. The high upfront capital expenditure associated with system deployment often creates adoption challenges for small and medium-sized industrial facilities operating under constrained budgets.

In addition, integrating emission monitoring platforms with existing industrial control systems, enterprise software, and legacy infrastructure can be technically complex and time-consuming. Facilities must also ensure continuous calibration, sensor accuracy, and compliance with evolving regulatory standards, increasing operational costs and implementation complexity. These challenges are particularly significant in emerging markets where environmental monitoring infrastructure remains underdeveloped.

Commercial deployment assessments indicate that full-scale continuous emission monitoring installations for large industrial facilities can increase project costs by approximately 15–25% compared with conventional periodic testing programs, creating return-on-investment concerns for certain end users despite long-term compliance benefits.

Key Market Opportunity: Expansion Of Carbon Management And Smart Industrial Sustainability Programs

The global transition toward decarbonization, carbon neutrality, and sustainable industrial operations is creating significant opportunities for emission monitoring technologies. Organizations increasingly require accurate emissions data to support carbon accounting, ESG reporting, emissions trading programs, and sustainability performance measurement across complex industrial operations.

Industrial companies are increasingly deploying advanced monitoring systems, For instance for greenhouse gas tracking, carbon footprint measurement, and emissions verification, to support sustainability targets and regulatory disclosures. In energy and manufacturing sectors, growing adoption of digital twins, artificial intelligence, and industrial IoT platforms is enabling more sophisticated emissions management strategies based on real-time operational intelligence.

In addition, advancements in cloud analytics, remote monitoring technologies, and sensor miniaturization are improving monitoring efficiency and expanding applications across industrial, commercial, and municipal sectors. Carbon reduction programs implemented during 2025 across major industrial facilities in Japan and South Korea reported emission tracking accuracy improvements of approximately 20–30% following integration of AI-enabled emission monitoring platforms with enterprise sustainability management systems.

Emission Monitoring System Market Scope

The market is segmented on the basis of type, service model, organisation size, and deployment model.

- By Type

On the basis of type, the emission monitoring system market is segmented into Solution Type and Service Type. The Solution Type segment held the largest market revenue share of approximately 68.9% in 2025 driven by widespread deployment of continuous emission monitoring systems (CEMS), gas analyzers, particulate monitoring equipment, and environmental data management platforms across industrial facilities. Organizations prefer integrated monitoring solutions due to their ability to provide real-time emission tracking, automated reporting, and regulatory compliance management.

The Service Type segment is projected to register the fastest growth at a CAGR of 20.7% from 2026 to 2033, driven by rising demand for system maintenance, calibration, consulting, managed monitoring services, and regulatory compliance support. Increasing complexity of environmental regulations and growing outsourcing of monitoring operations are accelerating segment expansion.

- By Service Model

On the basis of service model, the emission monitoring system market is segmented into Software as A Service (SaaS), Platform as A Service (PaaS), and Infrastructure as A Service (IaaS). The Software as A Service segment accounted for the largest market revenue share of approximately 56.4% in 2025 owing to increasing adoption of cloud-based emission monitoring software, environmental reporting platforms, and analytics solutions that enable remote monitoring and regulatory compliance management.

The Platform as A Service segment is anticipated to witness the fastest growth at a CAGR of 21.4% from 2026 to 2033, supported by growing demand for customizable environmental data platforms, AI-driven analytics tools, and scalable integration capabilities for industrial IoT-based emission monitoring applications.

- By Organisation Size

On the basis of organisation size, the emission monitoring system market is segmented into Small and Medium Enterprises and Large Enterprises. The Large Enterprises segment dominated the market with a revenue share of approximately 71.6% in 2025 due to extensive regulatory compliance obligations, larger industrial operations, and substantial investments in environmental sustainability initiatives. Large enterprises are major adopters of advanced monitoring technologies across energy, manufacturing, chemical, and mining industries.

The Small and Medium Enterprises segment is expected to register the fastest CAGR of 20.2% from 2026 to 2033, driven by increasing regulatory enforcement, growing awareness regarding environmental compliance, and rising availability of cost-effective cloud-based monitoring solutions.

- By Deployment Model

On the basis of deployment model, the emission monitoring system market is segmented into Public Cloud, Private Cloud, and Hybrid Cloud. The Private Cloud segment held the largest market revenue share of approximately 44.8% in 2025 driven by increasing concerns regarding industrial data security, regulatory compliance requirements, and the need for greater control over sensitive environmental and operational information.

The Hybrid Cloud segment is projected to witness the fastest growth at a CAGR of 22.1% from 2026 to 2033, supported by growing demand for flexible deployment architectures that combine on-premise infrastructure with cloud-based analytics, enabling organizations to optimize performance, scalability, and compliance management across geographically distributed industrial facilities.

Emission Monitoring System Market Regional Analysis

North America Emission Monitoring System Market Insight

North America dominated the emission monitoring system market with the largest revenue share of 38.74% in 2025, supported by stringent environmental regulations, widespread deployment of continuous emission monitoring systems (CEMS), and increasing investments in industrial sustainability initiatives. Regulatory agencies across the region mandate real-time emissions tracking across power generation, oil & gas, chemical, and manufacturing facilities. The growing focus on carbon reduction, air quality compliance, and digital environmental reporting continues to strengthen adoption of advanced emission monitoring technologies across industrial sectors.

U.S. Emission Monitoring System Market Insight

The U.S. emission monitoring system market captured the largest revenue share in 2025 within North America, fueled by strict environmental compliance requirements established by federal and state agencies. Industries are increasingly deploying advanced monitoring platforms to track pollutants such as NOx, SO₂, CO₂, and particulate matter emissions. The growing adoption of cloud-based analytics, industrial IoT integration, and predictive environmental management solutions is further accelerating market expansion. In addition, ongoing modernization of power plants and industrial facilities continues to support demand for sophisticated emission monitoring systems.

Europe Emission Monitoring System Market Insight

The Europe emission monitoring system market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by ambitious carbon neutrality targets, tightening industrial emission standards, and increasing investments in environmental monitoring infrastructure. Governments and industries across the region are prioritizing continuous emissions tracking to comply with evolving sustainability regulations. Growing deployment of smart manufacturing technologies and digital environmental reporting platforms is further strengthening market growth across multiple industrial sectors.

U.K. Emission Monitoring System Market Insight

The U.K. emission monitoring system market is expected to witness the fastest growth rate from 2026 to 2033, driven by expanding decarbonization initiatives and stricter industrial emissions regulations. Industries are increasingly investing in real-time emissions monitoring technologies to improve environmental compliance and operational transparency. The growing emphasis on net-zero targets, combined with increasing adoption of digital compliance management systems, is expected to continue supporting market growth throughout the forecast period.

Germany Emission Monitoring System Market Insight

The Germany emission monitoring system market is expected to witness the fastest growth rate from 2026 to 2033, fueled by strong industrial activity, rigorous environmental policies, and growing investments in clean manufacturing technologies. Germany’s focus on industrial sustainability and energy transition programs is accelerating the deployment of advanced emission monitoring solutions across power generation, automotive, chemicals, and heavy manufacturing industries. Integration of automated environmental reporting and industrial automation technologies is further enhancing market development.

Asia-Pacific Emission Monitoring System Market Insight

The Asia-Pacific emission monitoring system market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding power generation capacity, and increasing government initiatives focused on pollution control. Rising environmental awareness and strengthening emission regulations across countries such as China, India, Japan, and South Korea are driving widespread adoption of monitoring technologies. Furthermore, growing investments in smart factories and industrial digitalization are creating significant opportunities for market expansion across the region.

Japan Emission Monitoring System Market Insight

The Japan emission monitoring system market is expected to witness the fastest growth rate from 2026 to 2033 due to increasing focus on industrial efficiency, environmental sustainability, and advanced manufacturing practices. Japanese industries are actively adopting sophisticated monitoring technologies to comply with evolving environmental regulations and improve operational performance. The integration of AI-enabled analytics, IoT-connected sensors, and automated compliance systems is further supporting market growth across energy, manufacturing, and chemical sectors.

China Emission Monitoring System Market Insight

The China emission monitoring system market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid industrial expansion, stringent pollution control policies, and large-scale investments in environmental monitoring infrastructure. China continues to strengthen emissions compliance requirements across power plants, steel facilities, cement manufacturing, and chemical industries. The country's focus on air quality improvement, carbon emission reduction, and smart industrial development is significantly driving the adoption of advanced emission monitoring technologies.

Emission Monitoring System Market Share

The Emission Monitoring System industry is primarily led by well-established companies, including:

• Oracle Corporation (U.S.)

• Cisco Systems, Inc. (U.S.)

• SAP SE (Germany)

• IBM Corporation (U.S.)

• Microsoft Corporation (U.S.)

• Fujitsu Limited (Japan)

• Infor, Inc. (U.S.)

• Epicor Software Corporation (U.S.)

• Atos Syntel Inc. (France)

• RapidScale, Inc. (U.S.)

• Retail Solutions, Inc. (U.S.)

• Softvision LLC (U.S.)

• DXC Technology Company (U.S.)

• Amazon Web Services, Inc. (U.S.)

• Infosys Limited (India)

• Cognizant Technology Solutions Corporation (U.S.)

• Wipro Limited (India)

Latest Developments in Emission Monitoring System Market

- In February 2026, Oracle Corporation, product launch, introduced an AI-powered retail cloud analytics platform integrating predictive demand forecasting and real-time customer behavior insights. The solution is designed to improve inventory optimization, enhance personalized shopping experiences, and support data-driven retail decision-making. This development is expected to accelerate AI adoption across retail cloud environments and strengthen competitive differentiation in advanced retail analytics.

- In October 2025, Amazon Web Services (AWS), service expansion, launched an enhanced suite of retail-focused cloud intelligence and automation solutions. The initiative aims to improve operational visibility, streamline omnichannel retail management, and enable faster processing of large-scale consumer data. The development is expected to boost cloud adoption among retailers and reinforce AWS’s leadership position in retail cloud infrastructure.

- In June 2024, Microsoft Corporation, strategic partnership, expanded collaboration with a leading global retail chain to deploy a cloud-based inventory and supply chain management platform. The solution is intended to improve stock visibility, reduce inventory inefficiencies, and support real-time operational decision-making. This partnership strengthens Microsoft's retail cloud ecosystem while encouraging broader digital transformation across the retail sector.

- In March 2024, Google Cloud, sustainability initiative, launched a cloud-enabled retail sustainability program focused on helping retailers monitor emissions, optimize resource utilization, and improve environmental reporting. The initiative supports retailers in achieving sustainability objectives while improving operational efficiency. The development is expected to increase demand for environmentally focused cloud solutions within the retail industry.

- In October 2023, Flipkart Internet Private Limited, platform launch, introduced Flipkart Commerce Cloud to provide AI-driven retail technology solutions for international retailers, marketplaces, and e-commerce businesses. The platform aims to support business expansion, improve operational efficiency, and address complex retail challenges through intelligent automation. This launch strengthens cloud-based retail innovation and expands access to scalable digital commerce infrastructure.

- In January 2023, Ernst & Young Global Limited, product launch, unveiled the EY Retail Intelligence solution built on Microsoft Cloud and Cloud for Retail technologies. The platform is designed to enhance customer engagement, improve retail analytics capabilities, and deliver seamless shopping experiences through advanced data insights. The launch supports growing adoption of cloud-enabled retail intelligence solutions and strengthens digital transformation initiatives across the retail sector.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.