Global Emulsion Adhesives Market

Market Size in USD Billion

USD

18.16 Billion

USD

30.50 Billion

2024

2032

USD

18.16 Billion

USD

30.50 Billion

2024

2032

| 2025 - 2032 | |

| USD 18.16 Billion | |

| USD 30.50 Billion | |

| % | |

|

Emulsion Adhesives Market Size

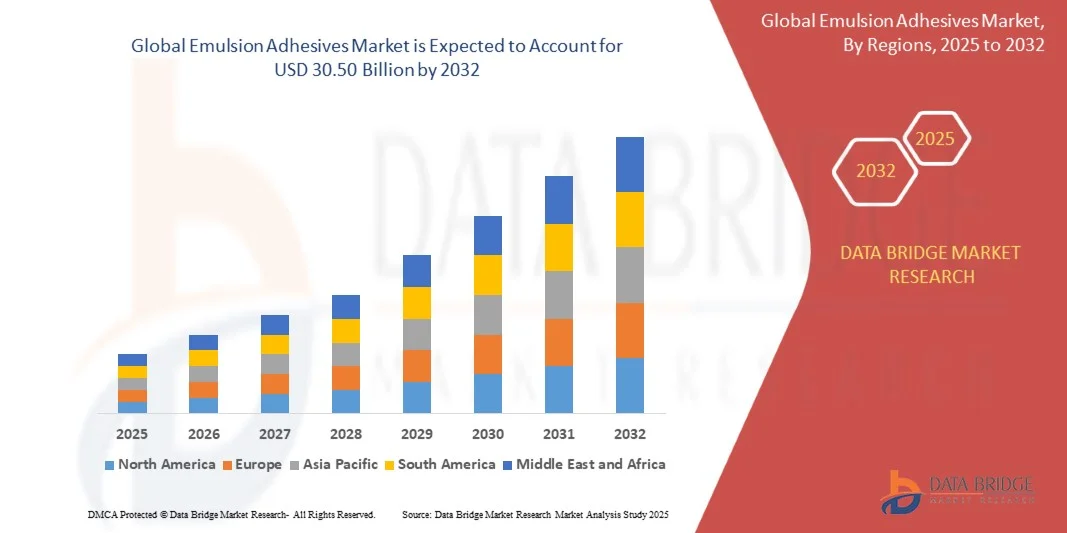

- The global emulsion adhesives market size was valued at USD 18.16 billion in 2024 and is expected to reach USD 30.50 billion by 2032, at a CAGR of 6.70% during the forecast period

- The market growth is largely fueled by the rising demand for strong, durable, and eco-friendly adhesives across diverse industries such as construction, packaging, automotive, and woodworking. Increasing industrialization and urbanization, particularly in emerging economies, are driving higher consumption of emulsion adhesives for both commercial and residential applications

- Furthermore, growing emphasis on sustainable and water-based adhesive solutions, along with innovations in high-performance formulations, is encouraging manufacturers and end-users to adopt emulsion adhesives over traditional solvent-based alternatives. These factors are collectively accelerating market expansion, boosting adoption across various end-use sectors

Emulsion Adhesives Market Analysis

- Emulsion adhesives are water-based bonding solutions that offer strong adhesion, flexibility, and resistance to environmental factors such as moisture and temperature variations. They are widely used in applications including tapes and labels, paper and packaging, construction, automotive, and woodworking, providing reliable performance and ease of processing

- The escalating demand for emulsion adhesives is primarily driven by increased construction and packaging activities, rising automotive production, and the shift toward sustainable, non-toxic adhesive solutions. In addition, technological advancements and product innovations in specialty adhesives are enhancing performance and expanding their applicability, further supporting market growth

- Asia-Pacific dominated the emulsion adhesives market with a share of 42.5% in 2024, due to expanding construction and automotive industries, growing packaging and labeling demand, and a strong presence of adhesive manufacturing hubs

- North America is expected to be the fastest growing region in the emulsion adhesives market during the forecast period due to robust demand for emulsion adhesives in construction, automotive, packaging, and woodworking sectors

- Permanent segment dominated the market with a market share of 62.6% in 2024, due to its strong bonding properties and reliability across critical applications such as construction, automotive, and industrial manufacturing. Permanent emulsions are preferred where long-term durability, resistance to mechanical stress, and adherence to diverse substrates are essential. Their consistent performance in both indoor and outdoor conditions and compatibility with advanced coating and finishing technologies further strengthen their market leadership

Report Scope and Emulsion Adhesives Market Segmentation

|

Attributes |

Emulsion Adhesives Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Emulsion Adhesives Market Trends

Growing Demand for Eco-Friendly Adhesives

- The emulsion adhesives market is experiencing robust growth driven by rising demand for environmentally friendly bonding solutions across industries such as packaging, automotive, construction, and woodworking. These water-based adhesives are favored for their low volatile organic compound (VOC) emissions, non-toxic profiles, and alignment with global sustainability initiatives

- For instance, Henkel AG & Co. KGaA has been actively expanding its portfolio of low-VOC, bio-based emulsion adhesives tailored for flexible packaging and building materials. BASF SE similarly invests in developing waterborne adhesive technologies designed to meet stringent environmental regulations while delivering strong adhesion and durability

- Technological advancements in polymer chemistry are enhancing emulsion adhesive performance, offering improved tack, shear strength, and temperature resistance. This innovation enables broader application across textiles, electronics, and automotive interiors, supporting the shift toward greener manufacturing processes

- Sustainability regulations and increasing consumer awareness regarding ecological impact are compelling manufacturers to prioritize bio-based, recyclable, and biodegradable adhesive solutions. The growing e-commerce sector is also propelling demand for sustainable adhesives in corrugated packaging, labels, and paper products

- Collaborative efforts between industry players and regulatory bodies are accelerating the adoption of circular economy principles within adhesive production and application. The focus on innovation and eco-compliant adhesive formulations is expected to significantly shape the market trajectory throughout the next decade

- The sustained push toward eco-friendly adhesives, combined with expanding end-use markets and regulatory support, is transforming emulsion adhesives into a critical component of sustainable product design and industrial processes

Emulsion Adhesives Market Dynamics

Driver

Rising Use in Packaging Industry

- The packaging industry’s rapid growth, particularly driven by e-commerce, food, and consumer goods sectors, is a primary driver of emulsion adhesive demand. The adhesives’ compatibility with various substrates such as paper, cardboard, and flexible films makes them ideal for strong, fast-bonding, and cost-effective packaging applications

- For instance, Avery Dennison has expanded its emulsion adhesive offerings tailored for pressure-sensitive labels and flexible packaging in response to increased demand for durable yet recyclable materials. Amcor’s use of water-based adhesives in sustainable packaging solutions exemplifies the industry's orientation toward eco-conscious bonding technologies

- Increasing consumer preference for sustainable packaging with lower environmental footprints is encouraging converters and brand owners to adopt emulsion adhesives. These adhesives contribute to reducing packaging waste and VOC emissions, aligning with corporate ESG goals and regulatory mandates

- Technological advancements that improve adhesive lifecycle, moisture resistance, and ease of recycling further boost emulsion adhesive adoption in packaging. The demand for innovative packaging formats, such as intelligent and smart packs, is also driving customized adhesive formulations

- The packaging industry's growth and sustainability imperatives underscore emulsion adhesives as a key enabler for next-generation, eco-friendly packaging solutions. This trend is firmly established as a market growth engine with expanding geographic and sectoral reach

Restraint/Challenge

Fluctuating Raw Material Prices

- The emulsion adhesives market faces challenges from volatility in raw material prices, particularly for key input chemicals such as acrylic polymers and bio-based feedstocks. These fluctuations impact production costs and complicate pricing strategies for manufacturers and end-users

- For instance, global supply chain disruptions and increased demand for bio-based oils have led to periods of raw material scarcity and price spikes, affecting adhesive producers worldwide. This volatility adds financial risk to product formulations and continuity of supply, especially impacting smaller manufacturers with limited hedging capabilities

- Uncertainty in feedstock availability is compounded by geopolitical tensions, environmental events, and regulatory changes that influence the cost and accessibility of petrochemical and renewable raw materials. These market dynamics can constrain long-term investment and R&D initiatives

- Price fluctuations also impact customer procurement behavior, sometimes leading to delayed orders, contract renegotiations, or exploration of alternative adhesive technologies. Maintaining a resilient and diversified supply chain is crucial for managing risks associated with raw material cost volatility

- In conclusion, while demand for emulsion adhesives remains strong, raw material price volatility is a significant restraint. Market players must focus on strategic sourcing, cost optimization, and innovation in sustainable raw materials to safeguard growth and ensure supply chain stability in a dynamic environment

Emulsion Adhesives Market Scope

The market is segmented on the basis of chemical composition, product, type, and application.

• By Chemical Composition

On the basis of chemical composition, the emulsion adhesives market is segmented into rubber-based and acrylic-based. The acrylic-based segment dominated the largest market revenue share in 2024, owing to its superior adhesion properties, durability, and resistance to environmental factors such as heat, moisture, and UV exposure. Acrylic-based emulsions are highly versatile, suitable for a wide range of substrates, and compatible with various industrial and consumer applications, which has made them the preferred choice across construction, packaging, and woodworking industries. Their ease of formulation and ability to provide strong bonding without compromising flexibility further drive their dominance.

The rubber-based segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by growing demand in pressure-sensitive applications such as tapes, labels, and self-adhesive films. Rubber-based emulsions offer excellent tackiness, immediate bonding strength, and cost-effectiveness, making them attractive for industries requiring high initial adhesion and quick set times. Increasing adoption in the packaging and automotive sectors for lightweight bonding applications is further supporting growth.

• By Product

On the basis of product, the emulsion adhesives market is categorized into permanent and removable. The permanent segment dominated the market with a share of 62.6% in 2024, driven by its strong bonding properties and reliability across critical applications such as construction, automotive, and industrial manufacturing. Permanent emulsions are preferred where long-term durability, resistance to mechanical stress, and adherence to diverse substrates are essential. Their consistent performance in both indoor and outdoor conditions and compatibility with advanced coating and finishing technologies further strengthen their market leadership.

The removable segment is anticipated to witness the fastest growth rate from 2025 to 2032, owing to increasing consumer and industrial demand for repositionable and temporary bonding solutions. Removable emulsions are widely used in office supplies, labels, packaging, and temporary protective films. Their ability to provide strong initial adhesion while allowing clean removal without residue makes them highly suitable for evolving packaging and labeling trends emphasizing recyclability and reusability.

• By Type

On the basis of type, the emulsion adhesives market is segmented into acrylic polymer emulsion, lattices, vinyl acetate ethylene (VAE) emulsion, polyurethane dispersion (PUD), polyvinyl acetate (PVA) emulsion, and others. The acrylic polymer emulsion segment dominated the market in 2024, attributed to its versatile performance, strong adhesion to a variety of substrates, and resistance to aging and environmental stress. Its widespread use across construction, woodworking, and packaging applications is further bolstered by ease of formulation and compatibility with modern processing equipment.

The polyurethane dispersion (PUD) segment is projected to witness the fastest growth from 2025 to 2032, driven by increasing adoption in automotive, footwear, and specialty construction applications. PUD emulsions offer high flexibility, chemical resistance, and environmental friendliness, aligning with sustainability trends and regulatory standards. Their ability to provide strong bonding for challenging substrates and suitability for waterborne formulations is fueling rapid uptake across diverse industries.

• By Application

On the basis of application, the emulsion adhesives market is segmented into tapes and labels, paper and packaging, construction, automotive and transportation, woodworking, and others. The construction segment dominated the largest market share in 2024, owing to the increasing use of emulsion adhesives in flooring, wall panels, insulation, and structural bonding. Construction applications demand adhesives with high bonding strength, durability, and resistance to moisture and temperature variations, which has reinforced the use of emulsions in this sector. The segment’s growth is also supported by rising infrastructure development and urbanization across emerging markets.

The tapes and labels segment is expected to witness the fastest CAGR from 2025 to 2032, fueled by rapid expansion in packaging, logistics, and consumer goods industries. Adhesives in tapes and labels require strong initial tack, peel strength, and compatibility with various surfaces, which emulsion adhesives effectively provide. Rising e-commerce, modern retail, and increased demand for lightweight, recyclable packaging are further propelling growth in this segment.

Emulsion Adhesives Market Regional Analysis

- Asia-Pacific dominated the emulsion adhesives market with the largest revenue share of 42.5% in 2024, driven by expanding construction and automotive industries, growing packaging and labeling demand, and a strong presence of adhesive manufacturing hubs

- The region’s cost-effective manufacturing landscape, rising investments in specialty adhesive production, and growing exports of adhesive products are accelerating market expansion

- The availability of skilled labor, favorable government policies, and rapid industrialization across developing economies are contributing to increased consumption of emulsion adhesives in both industrial and consumer applications

China Emulsion Adhesives Market Insight

China held the largest share in the Asia-Pacific emulsion adhesives market in 2024, owing to its status as a global leader in adhesive manufacturing and construction material production. The country's strong industrial base, favorable government policies supporting chemical and material sector expansion, and extensive export capabilities are major growth drivers. Demand is further bolstered by increasing investments in automotive, packaging, and woodworking sectors, as well as rapid urbanization across major cities.

India Emulsion Adhesives Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by a rapidly expanding construction sector, increasing packaging and labeling demand, and rising investments in specialty adhesive infrastructure. Government initiatives promoting domestic manufacturing and self-reliance in chemical production are strengthening demand. In addition, growing automotive assembly and woodworking industries, along with rising exports of adhesive products, are contributing to robust market expansion.

Europe Emulsion Adhesives Market Insight

The Europe emulsion adhesives market is expanding steadily, supported by stringent regulatory standards, high demand for eco-friendly and sustainable adhesives, and growing investments in specialty and high-performance products. The region places strong emphasis on product quality, environmental compliance, and innovative adhesive formulations, particularly in construction, automotive, and packaging applications. The increasing adoption of advanced adhesive technologies is further enhancing market growth.

Germany Emulsion Adhesives Market Insight

Germany’s emulsion adhesives market is driven by its leadership in high-precision industrial manufacturing, strong chemical industry heritage, and export-oriented production model. The country has well-established R&D networks and partnerships between academic institutions and adhesive manufacturers, fostering continuous innovation in specialty and high-performance emulsions. Demand is particularly strong in construction, automotive, and industrial packaging applications.

U.K. Emulsion Adhesives Market Insight

The U.K. market is supported by a mature construction and packaging sector, growing focus on sustainability, and increasing demand for eco-friendly adhesive solutions. Rising emphasis on research and development, industry-academia collaborations, and production of specialty adhesive formulations continue to strengthen the U.K.’s position in high-value adhesive markets.

North America Emulsion Adhesives Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by robust demand for emulsion adhesives in construction, automotive, packaging, and woodworking sectors. A strong focus on sustainable and high-performance adhesives, advancements in material science, and growing adoption of eco-friendly formulations are boosting market demand. Rising reshoring of manufacturing and increasing collaboration between industrial and chemical players are supporting market expansion.

U.S. Emulsion Adhesives Market Insight

The U.S. accounted for the largest share in the North America market in 2024, underpinned by its expansive industrial and construction sectors, strong R&D infrastructure, and significant investment in specialty adhesive production. The country’s focus on sustainability, regulatory compliance, and innovative adhesive technologies is encouraging the use of high-performance emulsion adhesives. Presence of key players, advanced manufacturing facilities, and a mature distribution network further solidify the U.S.’s leading position in the region.

Emulsion Adhesives Market Share

The emulsion adhesives industry is primarily led by well-established companies, including:

- Wacker Chemie AG (Germany)

- Ashland (U.S.)

- Henkel Adhesives Technologies India Private Limited (India)

- H.B. Fuller Company (U.S.)

- 3M (U.S.)

- Pidilite Industries Ltd (India)

- Arkema (France)

- Dow (U.S.)

- CEMEDINE Co., Ltd. (Japan)

- Paramelt RMC B.V. (Netherlands)

- STI Polymer (U.S.)

- Tailored Chemical (U.S.)

- Halltech Inc. (U.S.)

- StanChem Inc. (U.S.)

- Falcon Chemicals LLC (U.A.E.)

- Valco Cincinnati, Inc. (U.S.)

- Star Bond (Thailand) Company Limited (Thailand)

- Sika AG (Switzerland)

- Franklin International (U.S.)

- Parker Hannifin Corp (U.S.)

- Mapei S.p.A (Italy)

Latest Developments in Emulsion Adhesives Market

- In October 2023, Asahi Kasei announced investments in new coating machines for its Hipore™ lithium-ion battery separators at its existing facilities in the U.S., Japan, and South Korea. This expansion is expected to strengthen the company’s market position in the high-performance battery materials sector by increasing production capacity, improving operational efficiency, and supporting the growing global demand for lithium-ion batteries. The project is slated to be operational by the beginning of Q1 FY2026, positioning Asahi Kasei to meet both domestic and international battery industry requirements

- In July 2023, Sika completed the acquisition of a leading tile setting materials manufacturer operating under the Chema brand in Peru. This strategic move enhances Sika’s foothold in the rapidly expanding mortar and construction adhesives market by broadening its distribution network and creating significant cross-selling opportunities. The acquisition is expected to accelerate market penetration, strengthen brand presence in Latin America, and generate synergies through optimized production and expanded product offerings

- In May 2023, H.B. Fuller announced the acquisition of Beardow Adams, a British family-owned multipurpose industrial adhesives developer. This acquisition is projected to drive profitable growth and strengthen H.B. Fuller’s position in the global adhesives market. By integrating Beardow Adams’ production capabilities, expanding distribution channels, and leveraging differentiated innovation, H.B. Fuller is positioned to enhance its market share in industrial adhesives and deliver comprehensive solutions across various end-use industries

- In February 2023, 3M launched a new medical adhesive capable of adhering to the skin for up to 28 days, doubling the previous standard of 14 days for extended medical adhesives. This innovation targets the healthcare and medical wearable market by enabling longer-term use of health monitors, sensors, and wearable devices, improving patient care and reducing the need for frequent adhesive replacements. The development strengthens 3M’s competitive edge in the medical adhesives segment by combining extended performance with reliability for critical healthcare applications

- In June 2023, Avient Corporation, in collaboration with BASF, introduced color grades of Ultrason®, a high-performance polymer, to the global market. This joint initiative provides end-users in consumer, food service, and electrical electronics (EE) healthcare sectors with technical support throughout the production process, from base polymer to final colored product. The launch is expected to enhance market adoption of Ultrason® by enabling customized solutions, improving product differentiation, and expanding applications across high-performance polymer markets worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Emulsion Adhesives Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Emulsion Adhesives Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Emulsion Adhesives Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.