Global Endoluminal Suturing Devices Market

Market Size in USD Million

USD

81.60 Million

USD

200.17 Million

2025

2033

USD

81.60 Million

USD

200.17 Million

2025

2033

| 2026 - 2033 | |

| USD 81.60 Million | |

| USD 200.17 Million | |

| % | |

|

Endoluminal Suturing Devices Market Overview

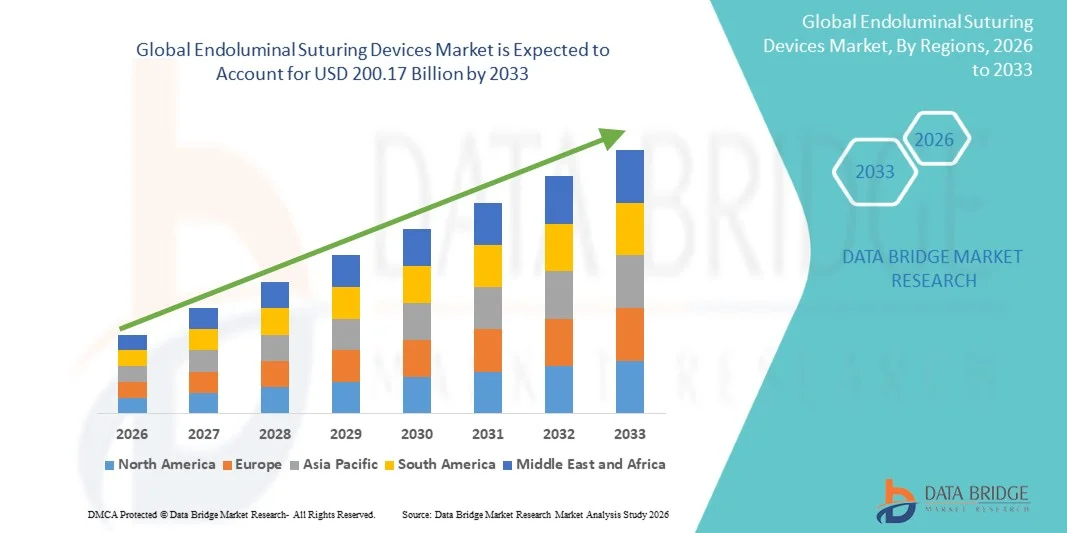

The Endoluminal Suturing Devices Market was valued at USD 81.60 billion in 2025 and is projected to reach USD 200.17 billion by 2033, growing at a CAGR of 11.87% from 2026 to 2033. The Endoluminal Suturing Devices Market is experiencing steady growth driven by the increasing adoption of minimally invasive surgical procedures, rising prevalence of gastrointestinal disorders, advancements in endoscopic technologies, and growing demand for effective alternatives to traditional surgical interventions.

The increasing incidence of conditions such as obesity, gastrointestinal leaks, fistulas, and bariatric surgery complications, combined with the growing preference for less invasive treatment options, is encouraging healthcare providers to adopt advanced endoluminal suturing solutions. These devices enable secure tissue approximation, defect closure, and post-surgical repair through endoscopic approaches, reducing recovery time, hospital stays, and procedural risks compared with conventional open surgeries. Furthermore, continuous innovations in flexible endoscopy, robotic-assisted platforms, and advanced suturing systems are expanding applications across bariatric procedures, gastrointestinal surgery, and therapeutic endoscopy, supporting market growth across developed and emerging healthcare markets.

Key Market Trends & Insights

- North America dominated the Endoluminal Suturing Devices Market with the largest revenue share of 34.00% in 2025, supported by the high adoption of advanced minimally invasive surgical technologies, strong presence of leading medical device manufacturers, increasing bariatric and gastrointestinal procedures, and well-established healthcare infrastructure.

- The bariatric surgery segment dominated the market with a 41.55% share in 2025, owing to the increasing prevalence of obesity worldwide and rising adoption of minimally invasive weight-loss procedures.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.2% from 2026 to 2033, fueled by improving healthcare infrastructure, rising obesity and gastrointestinal disease burden, increasing surgical procedure volumes, and growing adoption of advanced endoscopic technologies across China, India, and Japan.

- Gastroesophageal reflux disease (GERD) surgery is the fastest-growing application segment, projected to register a CAGR of 7.0%, supported by increasing GERD prevalence, growing preference for less invasive treatment options, and advancements in endoluminal repair procedures.

- Hospitals dominated the end-use segment with a 59.68% revenue share in 2025, owing to higher procedure volumes, availability of advanced endoscopy facilities, skilled surgeons, and increasing adoption of endoluminal suturing systems for complex gastrointestinal and bariatric interventions.

Market Size & Forecast

- Global Market Value (2025): USD 81.60 Billion

- Expected Market Value (2033): USD 200.17 Billion

- Forecast CAGR (2026–2033): 11.87%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Endoluminal Suturing Devices Market Segmentation

|

Attributes |

Endoluminal Suturing Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Apollo Endosurgery, Inc. (U.S.) |

|

Market Opportunities |

· Growing Adoption of Minimally Invasive and Bariatric Procedures · Technological Advancements in Endoscopic Suturing Systems · Expansion Across Emerging Healthcare Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Endoluminal Suturing Devices Market Trends

Trend: Rising Adoption of Minimally Invasive Endoscopic Procedures

Healthcare providers are increasingly adopting advanced endoluminal suturing devices to support minimally invasive procedures across bariatric surgery, gastrointestinal surgery, and gastroesophageal reflux disease (GERD) treatment. These devices enable precise tissue approximation, reduced surgical trauma, shorter recovery times, and improved patient outcomes compared with traditional surgical approaches. The growing preference for incision-free or reduced-incision procedures is accelerating the use of endoscopic suturing technologies in hospitals and ambulatory surgical centers. The rising global burden of obesity and gastrointestinal disorders is further supporting demand, with bariatric endoscopic procedures gaining traction as an alternative treatment option for weight management.

Endoluminal Suturing Devices Market Dynamics

Key Market Driver: Increasing Demand for Bariatric and Gastrointestinal Minimally Invasive Treatments

The increasing prevalence of obesity, gastroesophageal reflux disease (GERD), and gastrointestinal disorders is driving the adoption of endoluminal suturing devices worldwide. These systems are increasingly used in procedures such as endoscopic sleeve gastroplasty (ESG), fistula closure, leak repair, and gastrointestinal defect management. According to global health estimates, obesity continues to rise significantly, creating greater demand for less invasive weight-loss interventions. Healthcare systems are increasingly shifting toward procedures that reduce hospital stays, minimize complications, and improve recovery outcomes, encouraging hospitals and ambulatory surgical clinics to invest in advanced endoscopic technologies. The growing adoption of procedures such as ESG highlights the expanding role of endoluminal suturing devices, as these techniques provide a minimally invasive approach for gastric volume reduction without traditional surgical incisions.

Key Restraint/Challenge: High Cost of Advanced Endoscopic Suturing Systems and Limited Skilled Expertise

A major challenge for the Endoluminal Suturing Devices Market is the high acquisition cost associated with advanced endoscopic suturing platforms, accessories, and required training programs. These systems often require specialized endoscopy infrastructure, compatible imaging technologies, and skilled physicians trained in complex suturing techniques. The overall cost of device procurement, maintenance, and surgeon training can limit adoption, particularly among smaller hospitals and healthcare facilities in developing regions. In addition, the learning curve associated with advanced endoscopic suturing procedures remains a barrier, as successful outcomes depend on operator expertise and procedural experience. Limited availability of trained gastroenterologists and endoscopic surgeons in emerging markets can slow market penetration.

Key Market Opportunity: Integration of Advanced Technologies and Expansion of Outpatient Endoscopic Procedures

The integration of advanced technologies, including robotic-assisted endoscopy, improved visualization systems, and AI-enabled procedural guidance, presents significant growth opportunities for endoluminal suturing devices. AI-based image analysis and navigation technologies have the potential to improve procedural accuracy, support physician decision-making, and enhance training capabilities for complex endoscopic interventions. The increasing shift toward ambulatory surgical care is also creating new opportunities, as healthcare providers seek cost-effective treatment models with shorter patient recovery periods. Growing investments in healthcare infrastructure across Asia-Pacific, particularly in countries such as China and India, are expected to expand access to advanced minimally invasive procedures and support future market growth.

Endoluminal Suturing Devices Market Scope

The endoluminal suturing devices market is segmented on the basis of application and end user.

By Application

On the basis of application, the Endoluminal Suturing Devices Market is segmented into bariatric surgery, gastrointestinal surgery, gastroesophageal reflux disease surgery, and others. The bariatric surgery segment dominated the market with a 41.55% share in 2025, owing to the increasing prevalence of obesity worldwide and rising adoption of minimally invasive weight-loss procedures. Endoluminal suturing devices are widely used in procedures such as endoscopic sleeve gastroplasty (ESG), enabling gastric volume reduction without traditional surgical incisions. The growing preference for less invasive approaches, shorter hospital stays, reduced postoperative complications, and improved patient recovery outcomes is driving segment expansion. In addition, increasing investments by hospitals and bariatric centers in advanced endoscopic technologies are reinforcing the leading position of this segment globally.

The gastroesophageal reflux disease (GERD) surgery segment is expected to witness the fastest growth at a CAGR of 7.0% from 2026 to 2033, driven by the rising global burden of GERD and increasing demand for alternative treatment options beyond conventional medication therapy. The adoption of endoluminal suturing technologies for procedures such as transoral incisionless fundoplication (TIF) and endoscopic repair techniques is increasing due to reduced invasiveness and improved patient outcomes. Furthermore, advancements in endoscopic visualization, procedural accuracy, and surgeon training are supporting wider adoption of these devices in GERD management.

By End-Use

On the basis of end-use, the Endoluminal Suturing Devices Market is segmented into hospitals, ambulatory surgical clinics, and Others. The hospitals segment dominated the market with a 59.68% share in 2025, supported by the availability of advanced endoscopy infrastructure, skilled gastroenterologists, and higher procedure volumes. Hospitals remain the primary adoption centers for endoluminal suturing devices due to their capability to perform complex bariatric, gastrointestinal, and GERD-related procedures requiring specialized equipment and multidisciplinary expertise. Increasing investments in minimally invasive surgery departments, expansion of advanced gastrointestinal care units, and rising adoption of innovative surgical technologies are further strengthening hospital-based utilization.

The ambulatory surgical clinics segment is projected to register the fastest growth at a CAGR of 6.6% from 2026 to 2033, driven by the increasing shift toward outpatient minimally invasive procedures and cost-effective healthcare delivery models. Ambulatory centers are increasingly adopting endoluminal suturing technologies due to shorter procedure times, reduced recovery periods, and lower healthcare costs compared with traditional inpatient surgeries. The growing demand for same-day surgical procedures, improving reimbursement support, and expansion of specialized outpatient endoscopy facilities are expected to accelerate segment growth during the forecast period.

Endoluminal Suturing Devices Market Regional Analysis

North America dominated the endoluminal suturing devices market and accounted for the largest revenue share of 34.00% in 2025, supported by the high adoption of advanced minimally invasive surgical technologies, strong presence of leading medical device manufacturers, and well-established healthcare infrastructure. The region benefits from increasing demand for bariatric and gastrointestinal procedures, rising preference for endoscopic treatment approaches, and growing adoption of advanced suturing systems in hospitals and ambulatory surgical centers. In addition, continuous technological advancements, favorable reimbursement frameworks, and increasing investments in innovative endoscopic solutions are further strengthening North America’s leading position in the global market.

U.S. Endoluminal Suturing Devices Market Insight

The U.S. endoluminal suturing devices market is witnessing significant growth due to increasing adoption of minimally invasive gastrointestinal procedures, rising prevalence of obesity-related conditions, and growing demand for advanced bariatric surgery solutions. The presence of major medical device companies, strong healthcare spending, and rapid integration of advanced endoscopic technologies are driving market expansion. Furthermore, increasing preference for procedures that reduce recovery time, minimize surgical risks, and improve patient outcomes is accelerating the adoption of endoluminal suturing devices across hospitals and specialized surgical centers.

Europe Endoluminal Suturing Devices Market Insight

The Europe endoluminal suturing devices market remains a significant contributor to global revenue, driven by advanced healthcare systems, growing adoption of minimally invasive procedures, and increasing demand for innovative gastrointestinal treatment solutions. The region benefits from strong clinical expertise, rising investments in endoscopic technologies, and increasing focus on reducing healthcare costs through less invasive interventions. Growing awareness among healthcare providers regarding the benefits of endoluminal suturing systems is supporting market growth across European countries.

U.K. Endoluminal Suturing Devices Market Insight

The U.K. endoluminal suturing devices market is expanding steadily due to increasing adoption of advanced endoscopic procedures, rising demand for minimally invasive gastrointestinal treatments, and growing investments in healthcare technology. Hospitals and surgical centers are increasingly implementing advanced suturing solutions to improve procedural outcomes and enhance patient recovery. In addition, increasing focus on reducing hospital stays and improving treatment efficiency is contributing to the adoption of endoluminal suturing devices in the country.

Germany Endoluminal Suturing Devices Market Insight

The Germany endoluminal suturing devices market is growing due to the country’s advanced healthcare infrastructure, strong medical technology sector, and increasing adoption of innovative surgical solutions. Rising gastrointestinal disease prevalence, expanding bariatric surgery procedures, and growing demand for precision-based minimally invasive interventions are supporting market expansion. Furthermore, Germany’s focus on healthcare innovation and adoption of advanced endoscopy platforms is strengthening the use of endoluminal suturing technologies across clinical settings.

Asia-Pacific Endoluminal Suturing Devices Market Insight

The Asia-Pacific endoluminal suturing devices market is expected to witness the fastest growth, expanding at a CAGR of 7.2% from 2026 to 2033, driven by improving healthcare infrastructure, rising obesity and gastrointestinal disease burden, increasing surgical procedure volumes, and growing adoption of advanced endoscopic technologies. Countries such as China, India, and Japan are experiencing increased demand for minimally invasive procedures due to improving access to healthcare services, rising healthcare investments, and growing awareness of advanced treatment options. In addition, expanding medical device markets and increasing adoption of innovative surgical technologies are accelerating regional growth.

Japan Endoluminal Suturing Devices Market Insight

The Japan endoluminal suturing devices market is witnessing steady growth due to the country’s advanced healthcare system, strong focus on medical innovation, and increasing adoption of minimally invasive surgical procedures. Growing demand for gastrointestinal disease management, aging population-related healthcare needs, and adoption of advanced endoscopic solutions are supporting market expansion. Furthermore, Japan’s strong medical technology ecosystem and emphasis on precision healthcare are contributing to increased utilization of endoluminal suturing devices.

China Endoluminal Suturing Devices Market Insight

The China endoluminal suturing devices market is growing rapidly due to improving healthcare infrastructure, increasing surgical procedure volumes, rising prevalence of gastrointestinal disorders, and growing adoption of advanced minimally invasive techniques. Government initiatives to enhance healthcare access, increasing investments in medical technology, and expanding hospital capabilities are driving demand for endoscopic suturing systems. Moreover, increasing awareness of advanced treatment options and rising adoption of next-generation endoscopy technologies are positioning China as a key growth market for endoluminal suturing devices globally.

Endoluminal Suturing Devices Market Share

The Endoluminal Suturing Devices industry is primarily led by well-established companies, including:

- Apollo Endosurgery, Inc. (U.S.)

- Boston Scientific Corporation (U.S.)

- Medtronic plc (Ireland)

- Johnson & Johnson MedTech (U.S.)

- Olympus Corporation (Japan)

- CONMED Corporation (U.S.)

- STERIS plc (Ireland)

- Cook Medical (U.S.)

- EndoGastric Solutions, Inc. (U.S.)

- Micro-Tech Endoscopy (China)

- ERBE Elektromedizin GmbH (Germany)

- Fujifilm Holdings Corporation (Japan)

- HOYA Corporation (Japan)

- Teleflex Incorporated (U.S.)

- Smith+Nephew plc (United Kingdom)

- Ethicon, Inc. (U.S.)

- Richard Wolf GmbH (Germany)

- KARL STORZ SE & Co. KG (Germany)

- Zimmer Biomet Holdings, Inc. (U.S.)

- Stryker Corporation (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- Applied Medical Resources Corporation (U.S.)

- EndoQuest Robotics, Inc. (U.S.)

- Taewoong Medical Co., Ltd. (South Korea)

- Medi-Globe GmbH (Germany)

- Gastro Medical Solutions (U.S.)

- Limax Biosciences (U.S.)

Latest Developments in Endoluminal Suturing Devices Market

- In May 2021, Apollo Endosurgery highlighted the clinical applications of its OverStitch Endoscopic Suturing System during Digestive Disease Week (DDW) 2021, where more than 30 presentations featured the technology across multiple endoscopic procedures. The presentations included data from the MERIT trial and studies evaluating Endoscopic Sleeve Gastroplasty (ESG), reinforcing the role of endoluminal suturing devices in bariatric and gastrointestinal interventions. This development demonstrated increasing clinical acceptance of advanced endoscopic suturing technologies for minimally invasive procedures

- In January 2022, Apollo Endosurgery announced strong growth in its Endoscopic Suturing System (ESS) portfolio, reporting approximately 55% year-over-year growth in ESS revenue during 2021. The company attributed this growth to increasing adoption of OverStitch and X-Tack® technologies across gastrointestinal and bariatric procedures, reflecting rising demand for minimally invasive therapeutic endoscopy solutions globally

- In August 2022, Endo Tools Therapeutics announced the first U.S. commercial cases using its endomina endoscopic suturing system. The device was designed to enable minimally invasive gastrointestinal tissue approximation and expand treatment options for patients undergoing endoscopic procedures. The milestone marked the company’s expansion into the U.S. market and highlighted growing competition in the endoluminal suturing device space beyond traditional platforms

- In October 2024, clinical research evaluating advanced endoscopic suturing approaches reported continued development in the use of over-the-scope suturing technologies for gastrointestinal defect closure. A systematic review and meta-analysis published in 2024 assessed the efficacy and safety of over-the-scope endoscopic suturing devices for closure of defects after endoscopic submucosal dissection, supporting ongoing innovation and clinical adoption of endoluminal closure technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.