Global Endoscopic Hemostasis Market

Market Size in USD Billion

USD

2.46 Billion

USD

4.24 Billion

2025

2033

USD

2.46 Billion

USD

4.24 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.46 Billion | |

| USD 4.24 Billion | |

| % | |

|

Endoscopic Hemostasis Market Size

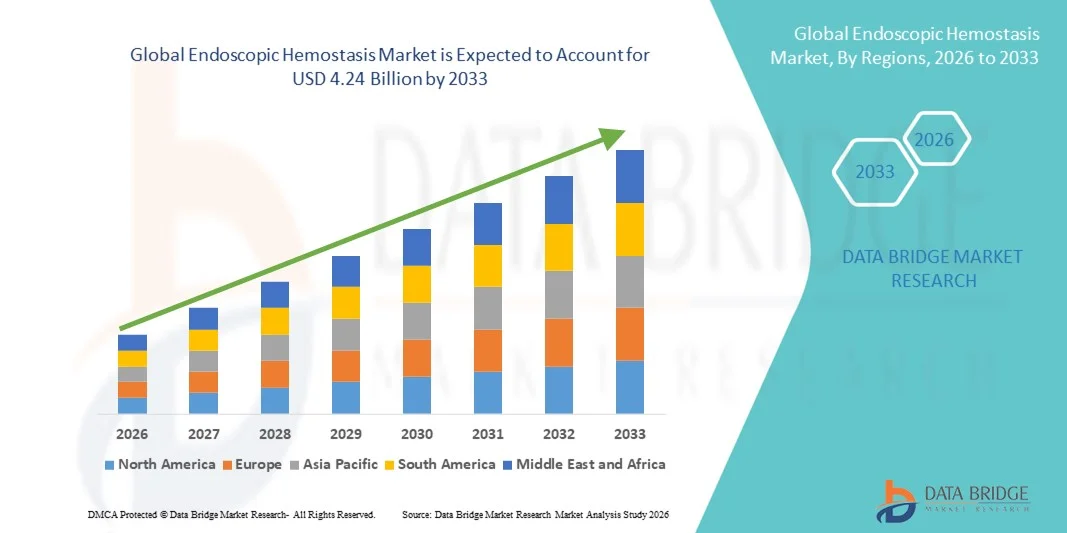

- The global endoscopic hemostasis market is expected to reach USD 4.24 billion by 2033 from USD 2.46 billion in 2025, growing with a CAGR of 8.1% in the forecast period of 2026 to 2033.

- The global endoscopic hemostasis market is witnessing steady and robust growth, driven by the rising prevalence of gastrointestinal disorders, increasing incidence of colorectal cancer, peptic ulcers, and gastrointestinal bleeding, and the growing adoption of minimally invasive endoscopic procedures across the region..

- Market growth is further supported by stringent clinical guidelines, a strong focus on patient safety and procedural efficacy, and rising demand for advanced hemostatic technologies that improve procedural outcomes and reduce complication rates. Continuous advancements in endoscopic device design, including improved clips, coagulation systems, sprays, and combination therapies, are enhancing precision, ease of use, and clinical effectiveness. Moreover, increasing investments in medical device R&D, technological innovation, and the integration of next-generation materials and energy-based systems are driving product innovation and supporting the long-term growth of the Asia-Pacific endoscopic hemostasis market.

Endoscopic Hemostasis Market Analysis

- Expanding healthcare infrastructure, rising volumes of endoscopic procedures, and increasing adoption of minimally invasive treatment approaches are fueling strong demand for endoscopic hemostasis devices in global. Healthcare providers are increasingly incorporating advanced hemostatic technologies to improve procedural efficiency, reduce complication rates, shorten hospital stays, and enhance overall patient outcomes, thereby supporting sustained market growth.

- The North America is projected to dominate the global endoscopic hemostasis Market, capturing 37.24% market share in 2026, driven by established healthcare infrastructure, high volume of endoscopic procedures, strong adoption of advanced medical technologies, and presence of leading medical device manufacturers. Favorable reimbursement frameworks, a skilled clinical workforce, and continuous investments in healthcare innovation

- Asia-Pacific is the fastest-growing country in the global endoscopic hemostasis market, supported by early adoption of digital health and advanced endoscopy platforms, strong integration of AI-assisted diagnostics and image-guided endoscopic procedures, and a high level of clinical research participation in gastrointestinal and interventional endoscopy. The country’s well-structured referral pathways, emphasis on day-care and outpatient endoscopic treatments, and rapid commercial uptake of next-generation hemostatic devices by clinicians further accelerate procedural volumes. In addition, collaborations between hospitals, academic institutions, and medical device manufacturers, along with streamlined regulatory approval timelines for innovative technologies, continue to position Denmark as a leading early-adopter market, driving faster growth compared to other Asia Pacific countries.

- The Mechanical Hemostasis Devices segment is dominating the global endoscopic hemostasis Market, accounting for 44.32% market share in 2025. This dominance is driven by the widespread clinical adoption of endoscopic clips and band ligation devices due to their proven efficacy, ease of deployment, cost-effectiveness, and suitability for a broad range of gastrointestinal bleeding indications. Their strong safety profile and compatibility with standard endoscopic procedures continue to support sustained demand across healthcare settings.

Report Scope and Endoscopic Hemostasis Market Segmentation

|

Attributes |

Endoscopic Hemostasis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

Asia-Pacific

Europe

North America

South America

Middle East and Africa

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. . |

Endoscopic Hemostasis Market Trends

Increasing Adoption of Advanced Minimally Invasive Endoscopic Hemostasis Technologies

- The steady expansion of endoscopic and minimally invasive procedures across Global is a major factor driving the increased adoption of endoscopic hemostasis devices. As the incidence of gastrointestinal bleeding, colorectal disorders, and related conditions continues to rise, healthcare providers increasingly rely on advanced hemostasis solutions to ensure effective bleeding control, procedural safety, and improved patient outcomes across high-volume clinical environments.

- Endoscopic hemostasis devices play a critical role in ensuring clinical efficacy, patient safety, and procedural reliability throughout diagnostic and therapeutic endoscopy. By enabling rapid bleeding control, reducing complication risks, and supporting minimally invasive treatment approaches, these devices help optimize procedural workflows while improving recovery times and overall quality of care across healthcare facilities.

- The growing adoption of advanced endoscopic technologies, including high-definition imaging, therapeutic endoscopy, and combination hemostasis techniques, has increased demand for high-performance hemostatic solutions. Innovations in mechanical clips, thermal coagulation systems, injection therapies, and topical hemostatic agents are enhancing procedural precision, treatment success rates, and clinician confidence while supporting evolving clinical practices.

- Healthcare providers across the care continuum are increasingly adopting endoscopic hemostasis devices to meet rising regulatory, safety, and clinical performance standards. Stringent clinical guidelines, growing emphasis on patient safety and outcome-based care, and increasing demand for minimally invasive interventions are encouraging hospitals and clinics to integrate advanced hemostasis technologies that ensure consistency, compliance, and high-quality care delivery.

- Overall, the expanding scale of endoscopic procedures, clinical innovation, and healthcare infrastructure development positions endoscopic hemostasis devices as an essential component of modern gastrointestinal care. These solutions support procedural efficiency, patient safety, regulatory compliance, and sustainable growth across Global’s evolving endoscopy landscape, making this insight readily reusable across regions by adapting healthcare system dynamics and adoption patterns.

Endoscopic Hemostasis Market Dynamics

Driver

Rise in Gastrointestinal Bleeding Cases

- The rising incidence of gastrointestinal bleeding has been established as a foundational force propelling growth in the global endoscopic hemostasis market. As the prevalence of upper and lower gastrointestinal bleeding conditions increases worldwide, demand for minimally invasive, endoscopy-based therapeutic interventions has been intensified. Endoscopic hemostasis offers critical clinical advantages, including rapid bleeding control, reduced need for surgical intervention, lower transfusion requirements, and shorter hospital stays, thereby positioning it as a first-line treatment modality in acute and chronic gastrointestinal bleeding management. Consequently, the escalation in gastrointestinal bleeding cases—driven by aging populations, higher prevalence of liver disease, anticoagulant use, and delayed care access during systemic healthcare disruptions—has translated into higher procedural volumes and broader adoption of advanced endoscopic hemostasis devices across hospitals and endoscopy centers globally.

- For instances,

- In September 2021, Medscape reported that upper gastrointestinal bleeding occurred at an incidence of approximately 100 cases per 100,000 population annually and remained one of the most common causes of emergency hospital admissions, underscoring a persistently high disease burden requiring endoscopic intervention.

- In June2023, Gastroenterology Research journal reported that mortality related to upper gastrointestinal bleeding in the U.S. increased between 2012 and 2021, with steeper increases observed toward the later years, indicating worsening clinical outcomes and intensified treatment requirements.

- In June 2023, StatPearls Publishing stated that gastrointestinal bleeding continues to represent a frequent global medical emergency, with urgent endoscopic diagnosis and hemostatic treatment remaining critical to reducing mortality and morbidity.

- In January 2025, the Journal of Clinical Medicine reported that patients with advanced liver disease exhibited significantly higher incidence of massive gastrointestinal bleeding episodes, reinforcing the link between chronic disease prevalence and increased need for endoscopic hemostasis.

- In September 2025, PubMed Central highlighted that upper gastrointestinal bleeding remained a life-threatening complication among chronic liver disease populations, sustaining elevated demand for endoscopic therapeutic procedures.

- The global escalation in gastrointestinal bleeding incidence is being firmly established as a permanent structural growth engine for the endoscopic hemostasis market. The continuous rise in acute bleeding events, combined with expanding populations affected by chronic liver disease, antithrombotic medication use, and age-related gastrointestinal pathology, is creating a sustained and non-cyclical requirement for endoscopic bleeding control. As clinical guidelines increasingly prioritize endoscopic therapy as first-line management, reliance on hemostasis technologies for emergency intervention, recurrence prevention, and complication management is being structurally reinforced. Furthermore, improving survival rates are extending patient monitoring and repeat intervention cycles, thereby multiplying lifetime procedural demand. This dynamic is anchoring endoscopic hemostasis adoption closely to global epidemiological trends, positioning this driver as a long-term foundational pillar for market expansion across developed and emerging healthcare systems.

Restraint/Challenge

High Cost and Technical Complexity of Endoscopic Hemostasis Devices

- Despite growing clinical adoption, the Global endoscopic hemostasis market continues to face structural restraint due to the high cost and technical complexity of advanced endoscopic hemostasis devices. These technologies often require significant upfront capital investment for equipment procurement, continuous expenditure on consumables, and specialized maintenance. In addition, effective use of hemostatic endoscopic devices demands advanced physician training, skilled support staff, and sophisticated hospital infrastructure, limiting adoption in cost-sensitive healthcare systems. Public hospitals in low- and middle-income countries, and even budget-constrained facilities in developed regions, frequently encounter barriers related to affordability, reimbursement gaps, and workforce readiness. As a result, uneven access and slower penetration of advanced endoscopic hemostasis technologies persist, constraining broader market expansion.

- For Instance,

- In November 2022, according to the high cost of gastrointestinal endoscopy procedures and equipment is a major restraint. For example, TNE costs Euro 125.90 per procedure, while oral endoscopy costs Euro 184.10 and MACE costs Euro 407.10. Additionally, equipment maintenance and reprocessing add to the cost, with flexible endoscopes costing around Euro 79,330, making procedures expensive overall.

- In June 2024, Science direct highlighted that the high cost of gastrointestinal endoscopy is exacerbated in low-income and middle-income countries (LICs and LMICs) due to the lack of local maintenance and repair facilities. Scopes requiring repairs must be shipped abroad, incurring significant costs and delays. Additionally, cheaper second-hand and Chinese-manufactured endoscopes often lack adequate service and maintenance support.

- In October 2025, BMJ Open Gastroenterology published a micro-costing study showing that in a UK National Health Service hospital, the total per-procedure cost of reusable gastrointestinal endoscopes was an estimated GBP107.34, with capital and maintenance costs as major cost drivers, highlighting economic barriers to wide adoption of endoscopic equipment in public health settings.

- In August 2024, a ScienceDirect narrative review reported that purchase, maintenance, and associated logistics costs of endoscopy equipment remain a major barrier to developing and sustaining endoscopy services in low- and middle-income countries, due to high device cost and lack of infrastructure.

- In February 2025, as per science direct the high cost of gastrointestinal endoscopy is evident in various studies, especially for screening and surveillance. For instance, while general population screenings may not be cost-effective in Western regions, targeted surveillance for high-risk groups, such as those with gastric intestinal metaplAsia, can still be cost-effective, with ICERs ranging from USD 20,739.1 to 98,402.2 per QALY.

- The compiled evidence clearly indicates that the high cost and technical complexity associated with gastrointestinal endoscopy and endoscopic hemostasis devices represent a persistent restraint on market growth. Substantial capital investment for equipment procurement, elevated per-procedure costs, and ongoing expenses related to maintenance, reprocessing, and repair significantly increase the overall cost burden on healthcare systems. These challenges are further intensified in low- and middle-income regions where limited technical infrastructure and lack of local servicing capabilities delay adoption and restrict procedural capacity. Even in developed healthcare systems, cost-effectiveness considerations influence screening strategies and limit widespread implementation. Collectively, these economic and operational constraints slow penetration of advanced endoscopic hemostasis technologies, reinforcing affordability and technical complexity as structural barriers to broader market expansion

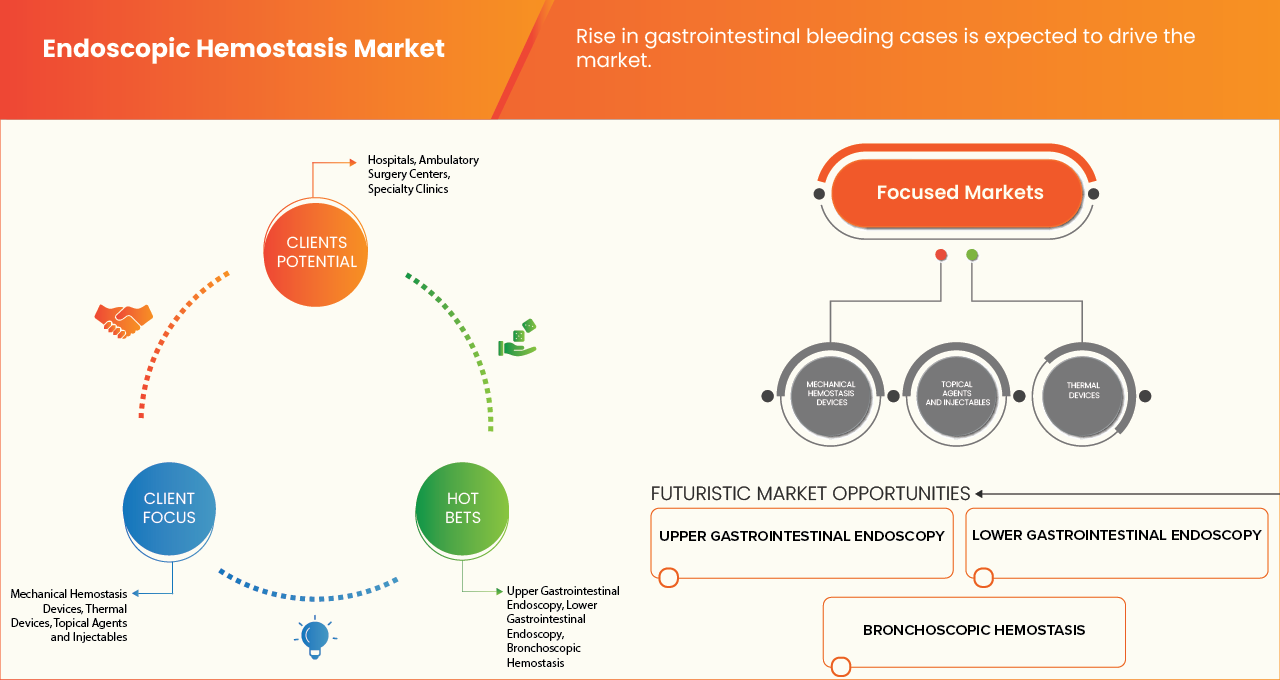

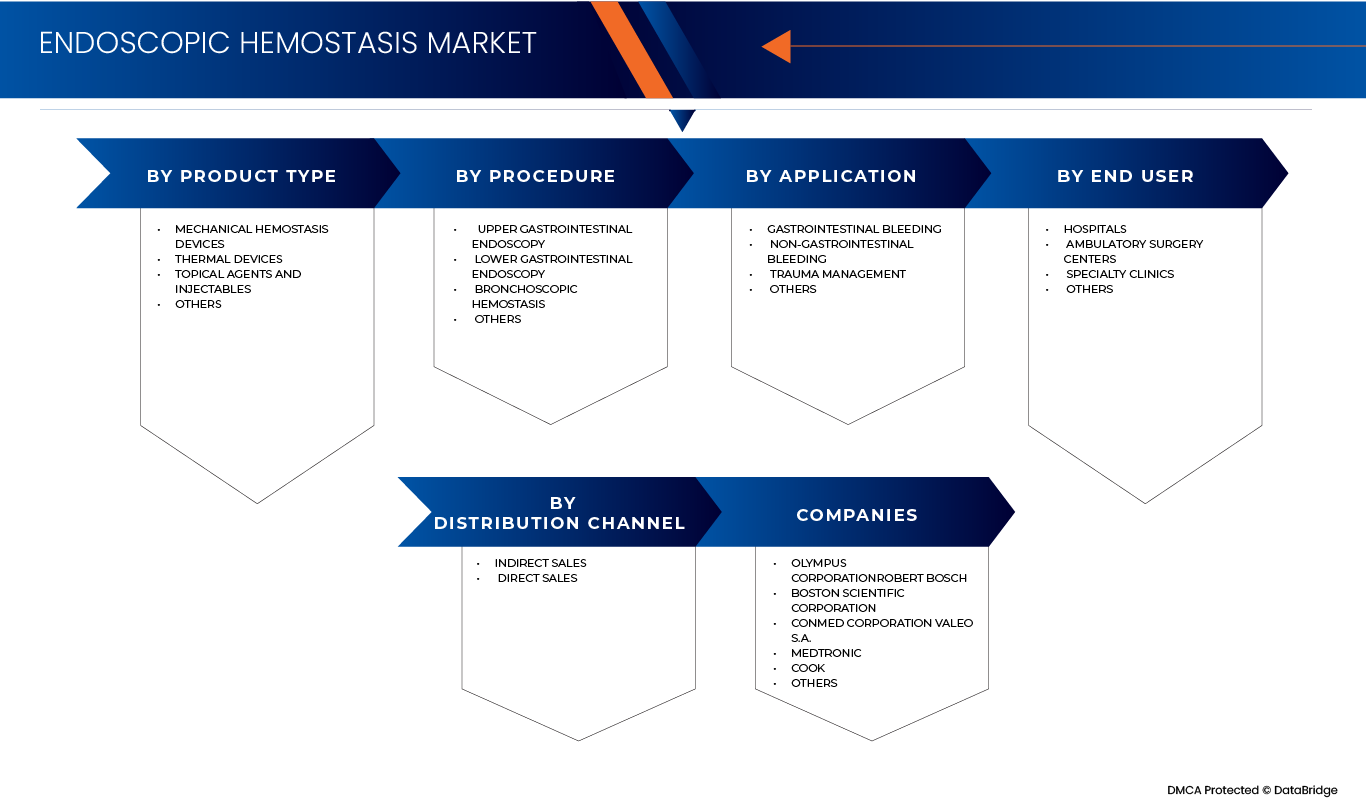

Endoscopic Hemostasis Market Scope

The global endoscopic hemostasis market is categorized into five key segments: product type, procedure, application, end user, and distribution channel.

- By product type

On the basis of product type, the Global endoscopic hemostasis market is segmented into mechanical hemostasis devices, thermal devices, topical agents and injectables, and others. In 2026, the mechanical hemostasis devices segment is projected to dominate the Global endoscopic hemostasis Market with the largest market share of 44.35%, owing to its widespread clinical preference for achieving immediate, controlled, and durable bleeding cessation during endoscopic interventions. Mechanical solutions such as clips and banding devices are routinely favored for their ability to provide precise vessel closure without inducing thermal tissue damage, thereby lowering rebleeding rates and post-procedure complications. Their applicability across a broad spectrum of bleeding scenarios, including peptic ulcers, variceal hemorrhage, and post-polypectomy bleeding, has resulted in consistently high utilization in both emergency and elective endoscopic settings. The strong reliance on mechanical hemostasis as a first-line therapeutic approach underscores its substantial contribution to overall market revenues and reinforces its dominant position within the product type landscape throughout the forecast period.

The topical agents and injectables segment is the fastest-growing segment in the endoscopic hemostasis market, with a CAGR of 8.5%. Growth is driven by the increasing incidence of gastrointestinal bleeding, widespread adoption of minimally invasive endoscopic procedures, and strong clinical demand for rapid-acting, easy-to-administer hemostatic solutions. Continuous advancements in formulation effectiveness, safety, and procedural efficiency are expected to sustain segment growth during the forecast period.

- By procedure

On the basis of procedure, the market is segmented into upper gastrointestinal endoscopy, lower gastrointestinal endoscopy, bronchoscopic hemostasis, and others. In 2026, the upper gastrointestinal endoscopy segment is projected to dominate the Global endoscopic hemostasis Market with a market share of 44,09%, due to its extensive clinical adoption as the frontline procedural approach for managing acute and recurrent gastrointestinal bleeding. Upper GI endoscopy is widely relied upon for the diagnosis and immediate therapeutic control of bleeding ulcers, variceal hemorrhage, and Dieulafoy lesions, where rapid hemostatic intervention is clinically critical. The high procedural frequency in emergency departments and tertiary-care hospitals, combined with strong guideline support for early endoscopic intervention, is expected to sustain its leading market position. Its continued dominance is reflected in its substantial market share and steady growth trajectory through 2033, indicating persistent demand across both developed and emerging healthcare systems.

The lower gastrointestinal endoscopy segment is the fastest-growing application segment in the endoscopic hemostasis market, registering a CAGR of 8.5%. This growth is supported by rising prevalence of lower gastrointestinal bleeding conditions, increasing volumes of diagnostic and therapeutic colonoscopy procedures, and improved detection of colorectal disorders. Ongoing technological advancements in endoscopic hemostasis devices and growing emphasis on early diagnosis are expected to further drive adoption during the forecast period.

- By application

On the basis of application, the market is segmented into gastrointestinal bleeding, non-gastrointestinal bleeding, trauma management, and others. In 2026, the gastrointestinal bleeding segment is projected to dominate the Global endoscopic hemostasis Market with a market share of 71.80%, owing to the high global prevalence of peptic ulcers, esophageal varices, and colorectal malignancies requiring endoscopic bleeding control. Gastrointestinal bleeding remains the most common indication for endoscopic hemostasis procedures, driving consistent utilization of mechanical, thermal, and topical hemostatic solutions across hospital and ambulatory care settings. The critical need for rapid bleeding control to reduce morbidity, hospital length of stay, and mortality is expected to reinforce sustained demand within this application segment. Its large share of total market value highlights the central role of gastrointestinal indications in shaping overall market dynamics during the forecast period.

The trauma management segment is the fastest-growing segment in the endoscopic hemostasis market, with a CAGR of 8.7%. Growth is driven by the increasing occurrence of acute bleeding associated with traumatic injuries and a growing preference for minimally invasive techniques that enable rapid bleeding control. Improved clinical outcomes, reduced surgical intervention rates, and advancements in emergency endoscopic hemostasis technologies are expected to support continued expansion of this segment over the forecast period.

- By end user

On the basis of end user, the market is segmented into hospitals, ambulatory surgery centers, specialty clinics, and others. In 2026, the hospitals segment is projected to dominate the Global endoscopic hemostasis Market with the largest market share of 53.12%, due to the concentration of advanced endoscopy infrastructure, skilled gastroenterologists, and emergency care capabilities within hospital settings. Complex bleeding cases, including severe upper and lower gastrointestinal hemorrhage, are predominantly managed in public and private hospitals where comprehensive diagnostic and interventional resources are available. Higher patient inflow, greater procedural volumes, and established procurement frameworks further strengthen hospital demand for endoscopic hemostasis devices and consumables. This structural dependence on hospital-based care is expected to maintain the segment’s leading position through 2033 despite gradual growth in outpatient settings.

The ambulatory surgery centers segment is the fastest-growing end-user segment in the endoscopic hemostasis market, recording a CAGR of 8.5%. Growth is driven by the increasing shift toward outpatient endoscopic procedures, demand for cost-effective healthcare delivery, and shorter patient recovery times. Advancements in compact, efficient hemostasis devices suitable for outpatient settings are expected to further accelerate adoption during the forecast period.

- By distribution channel

On the basis of distribution channel, the market is segmented into direct sales and indirect sales, with indirect sales further segmented into online and offline channels. In 2026, the indirect sales segment is projected to dominate the Global endoscopic hemostasis Market with the largest market share of 58.86% as procurement is largely conducted through distributors, group purchasing organizations, and regional medical supply networks. Indirect channels are widely preferred due to their ability to offer bundled products, inventory management support, and broader geographic reach, particularly in emerging markets and decentralized healthcare systems. Hospitals and ambulatory centers frequently rely on distributor-led sourcing to ensure consistent availability of critical hemostasis devices while optimizing procurement costs. This distribution structure is expected to continue driving higher adoption of indirect sales channels throughout the forecast period.

The indirect sales segment is the fastest-growing distribution channel in the endoscopic hemostasis market, with a CAGR of 8.2%. This growth is supported by the expanding role of distribution partners and group purchasing networks in enhancing product accessibility and supply efficiency. Increasing reliance on centralized procurement models, bundled purchasing agreements, and regional distributor expertise is expected to continue driving growth of the indirect sales channel throughout the forecast period.

Endoscopic Hemostasis Market Regional Analysis

- North America represents one of the most important markets for endoscopic hemostasis devices, supported by its advanced healthcare infrastructure, strong medical device manufacturing base, and high adoption of minimally invasive endoscopic procedures. Continuous clinical innovation in gastroenterology, a high volume of diagnostic and therapeutic endoscopies, and strict clinical and regulatory standards are driving steady adoption of advanced mechanical, thermal, and topical hemostasis solutions across hospitals and specialty care centers.

- The Middle East & Africa is witnessing growing demand for endoscopic hemostasis technologies as increasing prevalence of gastrointestinal disorders, an aging population, and rising emphasis on minimally invasive treatment approaches reshape clinical practice. Healthcare providers are increasingly focused on improving patient safety, reducing procedure-related complications, and enhancing clinical efficiency, which is accelerating the adoption of reliable and cost-effective hemostasis devices across public and private healthcare settings.

- Asia-Pacific continues to emerge as a key growth hub for the endoscopic hemostasis market, driven by strong clinical expertise in gastroenterology, expanding access to advanced endoscopic services, and increasing focus on patient-centered and outcome-driven care. The country’s emphasis on clinical quality, safety, and technological innovation is encouraging healthcare institutions to adopt advanced hemostasis solutions that improve procedural outcomes, support minimally invasive interventions, and comply with evolving regulatory and healthcare standards.

North America Endoscopic Hemostasis Market Insight

The North America Endoscopic Hemostasis Market is gaining strong traction due to the country’s high volume of gastrointestinal endoscopic procedures and early adoption of advanced therapeutic endoscopy techniques. North America hospitals and specialty clinics place strong emphasis on clinical precision, procedural reliability, and evidence-based device selection, driving consistent demand for high-performance mechanical and energy-based hemostasis solutions. In addition, the presence of leading medical device manufacturers, well-established clinical training programs, and strict regulatory and quality standards is fostering rapid uptake of technologically advanced hemostasis devices. North America focus on procedural standardization, patient safety, and outcome optimization reinforces its position as a technology-led and innovation-driven market within global.

Asia-Pacific Endoscopic Hemostasis Market Insight

The Asia-Pacific Endoscopic Hemostasis Market continues to expand as healthcare providers prioritize minimally invasive treatment pathways, efficiency in endoscopy units, and reduction of procedure-related complications. Rising incidence of gastrointestinal bleeding conditions, combined with increasing demand on NHS endoscopy services, is accelerating adoption of cost-effective, easy-to-use hemostasis devices that support high procedural throughput. Strong emphasis on clinical guidelines, value-based care, and standardized treatment protocols is shaping purchasing decisions, while growing use of ambulatory and day-care endoscopy settings is further supporting demand. These factors collectively position the Japan market as one driven by access, efficiency, and scalable clinical adoption rather than device manufacturing concentration.

Endoscopic Hemostasis Market Share

The Endoscopic Hemostasis industry is primarily led by well-established companies, including:

- Micro-Tech Endoscopy (China)

- Taewoong Medical Co., Ltd. (South Korea)

- Ovesco Endoscopy AG (China)

- Apollo Endosurgery, Inc. (U.S.)

- Argon Medical Devices, Inc. (U.S.)

- Olympus Corporation (Japan)

- Boston Scientific Corporation (U.S.)

- CONMED Corporation (U.S.)

- Medtronic (Ireland)

- Cook (U.S.)

- ERBE Elektromedizin GmbH (China)

- Karl Storz SE & Co. KG (China)

- Pentax Medical (Japan)

- Endoskopie Technik Gerhard (China)

- Merit Medical Systems, Inc. (U.S.)

- Diversatek, Inc. (U.S.)

- STERIS plc (Japan)

- B. Braun SE (China)

- Duomed Group (Belgium)

Latest Developments in the Global Endoscopic Hemostasis Market

- In December 2025, Olympus tripled its corporate venture capital fund commitment by launching Olympus Innovation Ventures Fund II with an additional $150 million to invest in MedTech startups focused on endoscopy, diagnostics, digital health, and related innovation fields to reinforce long-term growth and technological leadership

- In October 2025, Boston Scientific announced an agreement to acquire Nalu Medical, Inc., a privately held medical device company focused on implantable neurostimulation technologies for chronic pain. The acquisition was positioned to strengthen Boston Scientific’s neuromodulation portfolio, accelerate innovation in pain management, and expand treatment options for patients with chronic pain conditions

- In October 2025, CONMED Corporation announced a strategic exit from its gastroenterology business, divesting its GI product lines and related assets as part of a portfolio realignment to concentrate on core surgical and orthopaedic solutions. The move was positioned to streamline the company’s product focus, sharpen investment in high-growth procedural areas, and improve long-term revenue and margin profiles by reallocating resources toward CONMED’s flagship device platforms and emerging technologies

- In August 2025, the U.S. Food and Drug Administration (FDA) approved the first-of-its-kind IDE clinical study of Cook Medical’s ADVANCE EVERO 18 everolimus-coated PTA balloon catheter, enabling evaluation of its safety and effectiveness in treating symptomatic peripheral arterial disease. The decision marked a milestone for drug-coated balloon technology, supporting Cook’s advancement of next-generation endovascular therapies aimed at reducing restenosis and improving long-term vessel patency in patients with lower-extremity arterial disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL ENDOSCOPIC HEMOSTASIS MARKET

1.4 LIMITATIONS

1.5 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 MARKETS COVERED

2.2 GEOGRAPHICAL SCOPE

2.3 YEARS CONSIDERED FOR THE STUDY

2.4 CURRENCY AND PRICING

2.5 DBMR TRIPOD DATA VALIDATION MODEL

2.6 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.7 MULTIVARIATE MODELLING

2.8 DBMR MARKET POSITION GRID

2.9 VENDOR SHARE ANALYSIS

2.1 MARKET END-USER COVERAGE GRID

2.11 SECONDARY SOURCES

2.12 ASSUMPTIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 PORTERS FIVE FORCES ANALYSIS

4.2 BRAND OUTLOOK

4.2.1 BRAND COMPARATIVE ANALYSIS OF KEY GLOBAL PLAYERS

4.2.1.1 BRAND COMPARATIVE NARRATIVE (ANALYTICAL OVERVIEW)

4.2.2 PRODUCT VS BRAND OVERVIEW — GLOBAL ENDOSCOPIC HEMOSTASIS MARKET

4.2.2.1 PRODUCT OVERVIEW — ENDOSCOPIC HEMOSTASIS DEVICES

4.2.2.2 BRAND OVERVIEW — INFLUENCE ON GLOBAL CLINICAL ADOPTION

4.3 CONSUMER BUYING BEHAVIOUR

4.3.1 CLINICAL EFFECTIVENESS AND PATIENT OUTCOMES

4.3.2 COST AND VALUE CONSIDERATIONS

4.3.3 COMPATIBILITY AND INTEGRATION

4.3.4 TRAINING REQUIREMENTS AND EASE OF USE

4.3.5 REIMBURSEMENT AND HEALTHCARE POLICY ALIGNMENT

4.3.6 PROCUREMENT PROCESSES AND BULK AGREEMENTS

4.3.7 INFLUENCE OF CLINICAL STAKEHOLDERS

4.3.8 TRENDS IN BUYER BEHAVIOUR

4.3.9 CONCLUSION

4.4 PATENT ANALYSIS

4.4.1 PATENT QUALITY AND STRENGTH – GLOBAL ENDOSCOPIC HEMOSTASIS MARKET

4.4.2 COUNTRY PATENT LANDSCAPE

4.4.3 IP STRATEGY AND MANAGEMENT

4.4.4 LICENSING AND COLLABORATION

4.5 RAW MATERIAL COVERAGE

4.5.1 METALLIC COMPONENTS AND ALLOY SYSTEMS

4.5.2 POLYMERIC AND SYNTHETIC MATERIALS

4.5.3 NATURAL AND BIOCOMPATIBLE MATERIALS

4.5.4 ELECTRICAL AND THERMAL MATERIAL SYSTEMS

4.5.5 EXPENDABLE ACCESSORIES AND SINGLE-USE MATERIALS

4.6 TECHNOLOGICAL ADVANCEMENTS IN GLOBAL ENDOSCOPIC HEMOSTASIS MARKET

4.6.1 ENHANCED MECHANICAL HEMOSTASIS TOOLS

4.6.2 ADVANCED THERMAL COAGULATION AND ENERGY-BASED SYSTEMS

4.6.3 NOVEL TOPICAL HEMOSTATIC AGENTS

4.6.4 INTEGRATION WITH ADJUNCTIVE DIAGNOSTIC TECHNOLOGIES

4.6.5 DEVELOPMENT OF MULTIFUNCTIONAL AND COMBINATION DEVICES

4.6.6 IMPROVED USER ERGONOMICS AND DEVICE DEPLOYMENT SYSTEMS

4.6.7 CONCLUSION

4.7 VALUE CHAIN ANALYSIS

4.7.1 OVERVIEW

4.7.2 RAW MATERIALS & COMPONENTS

4.7.3 DEVICE DESIGN, R&D & MANUFACTURING

4.7.4 PROCESSING, FINISHING & STERILIZATION

4.7.5 PACKAGING & LABELING

4.7.6 LOGISTICS, DISTRIBUTION & COMMERCIALIZATION

4.7.7 CONCLUSION

4.8 VENDOR SELECTION CRITERIA

4.8.1 CLINICAL PERFORMANCE

4.8.2 REGULATORY COMPLIANCE AND APPROVALS

4.8.3 COST AND TOTAL VALUE PROPOSITION

4.8.4 SUPPLY CHAIN ROBUSTNESS AND LOGISTICS

4.8.5 SUPPORT, TRAINING AND CLINICAL EDUCATION

4.8.6 QUALITY SYSTEMS AND REPROCESSING GUIDANCE

4.8.7 REPUTATION, PEER ACCEPTANCE AND POST-MARKET PERFORMANCE

4.8.8 INNOVATION AND FUTURE-READINESS

4.9 COMPANY EVALUATION QUADRANT

4.1 PROFIT MARGIN SCENARIO

4.10.1 MARGIN IMPROVEMENT DRIVERS

4.10.2 COST PRESSURE

4.10.3 REGIONAL VARIATIONS

4.10.4 FUTURE SCENARIOS

4.11 CLIMATE CHANGE SCENARIO

4.11.1 ENVIRONMENTAL CONCERNS

4.11.2 INDUSTRY RESPONSE

4.11.3 GOVERNMENT’S ROLE

4.11.4 ANALYST RECOMMENDATIONS

4.12 INNOVATION TRACKER AND STRATEGIC ANALYSIS

4.12.1 MAJOR DEALS AND STRATEGIC ALLIANCES ANALYSIS

4.12.1.1 JOINT VENTURES

4.12.1.2 MERGERS AND ACQUISITIONS

4.12.1.3 LICENSING AND PARTNERSHIP

4.12.1.4 TECHNOLOGY COLLABORATIONS

4.12.2 STRATEGIC DIVESTMENTS

4.12.3 STAGE OF DEVELOPMENT

4.12.4 TIMELINES AND MILESTONES

4.12.5 INNOVATION STRATEGIES AND METHODOLOGIES

4.12.6 RISK ASSESSMENT AND MITIGATION

4.12.7 FUTURE OUTLOOK

4.13 PRICING ANALYSIS

4.13.1 HEMOSTATIC CLIPS AND FORCEPS PRICING

4.13.2 BANDING AND COAGULATION DEVICES

4.13.3 REGULATORY AND REIMBURSEMENT IMPACT

4.14 SUPPLY CHAIN ANALYSIS

4.14.1 OVERVIEW

4.14.2 LOGISTIC COST SCENARIO

4.14.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

4.14.4 CONCLUSION

5 TARIFFS & IMPACT ON THE MARKET

5.1 OVERVIEW

5.2 CURRENT TARIFF RATE (S) IN TOP-5 COUNTRY MARKETS

5.3 OUTLOOK: LOCAL PRODUCTION V/S IMPORT RELIANCE

5.4 VENDOR SELECTION CRITERIA

5.5 IMPACT ON SUPPLY CHAIN

5.5.1 RAW MATERIAL PROCUREMENT

5.5.2 MANUFACTURING AND PRODUCTION

5.5.3 LOGISTICS AND DISTRIBUTION

5.5.4 PRICE PITCHING AND POSITION OF MARKET

5.6 INDUSTRY PARTICIPANTS: PROACTIVE MOVES

5.6.1 SUPPLY CHAIN OPTIMIZATION

5.6.2 JOINT VENTURE ESTABLISHMENTS

5.7 IMPACT ON PRICES

5.8 REGULATORY INCLINATION

5.8.1 GEOPOLITICAL SITUATION

5.8.2 TRADE PARTNERSHIPS BETWEEN THE COUNTRIES

5.8.2.1 FREE TRADE AGREEMENTS

5.8.2.2 ALLIANCES ESTABLISHMENTS

5.8.3 STATUS ACCREDITATION (INCLUDING MFTN)

5.8.4 DOMESTIC COURSE OF CORRECTION

5.8.4.1 INCENTIVE SCHEMES TO BOOST PRODUCTION OUTPUTS

5.8.4.2 ESTABLISHMENT OF SEZS/INDUSTRIAL PARKS

6 REGULATION COVERAGE

6.1 PRODUCT CODES

6.2 CERTIFIED STANDARDS

6.3 SAFETY STANDARDS

6.3.1 MATERIAL HANDLING & STORAGE

6.3.2 TRANSPORT & PRECAUTIONS

6.3.3 HAZARD IDENTIFICATION

7 MARKET OVERVIEW

7.1 DRIVERS

7.1.1 RISE IN GASTROINTESTINAL BLEEDING CASES

7.1.2 AGING POPULATION DRIVING INCREASED DEMAND FOR GI DISORDERS

7.1.3 ADOPTION OF MINIMALLY INVASIVE ENDOSCOPIC PROCEDURES

7.1.4 RISING AWARENESS AND EXPANDED SCREENING PROGRAMS FOR GASTROINTESTINAL ENDOSCOPY

7.2 RESTRAINTS

7.2.1 HIGH COST AND TECHNICAL COMPLEXITY OF ENDOSCOPIC HEMOSTASIS DEVICES

7.2.2 LIMITED AWARENESS IN LOW-INCOME COUNTRIES

7.3 OPPORTUNITIES

7.3.1 TECHNOLOGICAL ADVANCEMENTS IN HEMOSTASIS DEVICES

7.3.2 EXPANSION IN EMERGING MARKETS (ASIA-PACIFIC, LATIN AMERICA)

7.3.3 GROWING ADOPTION OF HOME-BASED AND CAPSULE ENDOSCOPY SOLUTIONS

7.4 CHALLENGES

7.4.1 REIMBURSEMENT ISSUES FOR ENDOSCOPIC PROCEDURES

7.4.2 COMPLEXITIES IN ENDOSCOPE REPROCESSING AND STERILIZATION PROCESSES

8 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE

8.1 OVERVIEW

8.2 MECHANICAL HEMOSTASIS DEVICES

8.2.1 MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

8.2.1.1 HEMOSTATIC CLIPS

8.2.1.1.1 HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE

8.2.1.1.1.1 THROUGH-THE-SCOPE (TTS) CLIPS

8.2.1.1.1.2 OVER-THE-SCOPE (OTS) CLIPS

8.2.1.1.2 HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL

8.2.1.1.2.1 STAINLESS STEEL

8.2.1.1.2.2 TITANIUM

8.2.1.2 BANDING DEVICES

8.2.1.2.1 BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE

8.2.1.2.1.1 VARICEAL BANDING KITS

8.2.1.2.1.2 OESOPHAGEAL BANDING DEVICES

8.2.1.3 HEMOSTATIC FORCEPS

8.2.1.4 OTHERS

8.2.2 MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

8.2.2.1 NORTH AMERICA

8.2.2.2 EUROPE

8.2.2.3 ASIA-PACIFIC

8.2.2.4 SOUTH AMERICA

8.2.2.5 MIDDLE EAST & AFRICA

8.3 THERMAL DEVICES

8.3.1 THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

8.3.1.1 ARGON PLASMA COAGULATORS

8.3.1.2 HEATER PROBES

8.3.1.3 BIPOLAR COAGULATION DEVICES

8.3.1.3.1 BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE

8.3.1.3.1.1 MONOPOLAR

8.3.1.3.1.2 BIPOLAR

8.3.1.3.2 BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION

8.3.1.3.2.1 UPPER GI BLEEDING

8.3.1.3.2.2 LOWER GI BLEEDING

8.3.1.4 OTHERS

8.3.2 THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

8.3.2.1 NORTH AMERICA

8.3.2.2 EUROPE

8.3.2.3 ASIA-PACIFIC

8.3.2.4 SOUTH AMERICA

8.3.2.5 MIDDLE EAST & AFRICA

8.4 TOPICAL AGENTS AND INJECTABLES

8.4.1 TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

8.4.1.1 EPINEPHRINE INJECTION

8.4.1.2 HEMOSTATIC SPRAY (POWDER)

8.4.1.3 HEMOSTATIC GELS

8.4.1.4 FIBRIN SEALANTS

8.4.1.5 SCLEROSING AGENTS

8.4.2 TOPICAL AGENTS AND INJECTABLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

8.4.2.1 NORTH AMERICA

8.4.2.2 EUROPE

8.4.2.3 ASIA-PACIFIC

8.4.2.4 SOUTH AMERICA

8.4.2.5 MIDDLE EAST & AFRICA

8.5 OTHERS

8.5.1 OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

8.5.1.1 NORTH AMERICA

8.5.1.2 EUROPE

8.5.1.3 ASIA-PACIFIC

8.5.1.4 SOUTH AMERICA

8.5.1.5 MIDDLE EAST & AFRICA

9 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE TYPE

9.1 OVERVIEW

9.2 UPPER GASTROINTESTINAL ENDOSCOPY

9.2.1 UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

9.2.1.1 BLEEDING ULCER MANAGEMENT

9.2.1.2 VARICEAL BLEEDING

9.2.1.3 DIEULAFOY LESION

9.2.2 UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

9.2.2.1 NORTH AMERICA

9.2.2.2 EUROPE

9.2.2.3 ASIA-PACIFIC

9.2.2.4 SOUTH AMERICA

9.2.2.5 MIDDLE EAST & AFRICA

9.3 LOWER GASTROINTESTINAL ENDOSCOPY

9.3.1 LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

9.3.1.1 COLONIC BLEEDING

9.3.1.2 DIVERTICULAR BLEEDING

9.3.2 LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

9.3.2.1 NORTH AMERICA

9.3.2.2 EUROPE

9.3.2.3 ASIA-PACIFIC

9.3.2.4 SOUTH AMERICA

9.3.2.5 MIDDLE EAST & AFRICA

9.4 BRONCHOSCOPIC HEMOSTASIS

9.4.1 BRONCHOSCOPIC HEMOSTASIS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

9.4.1.1 NORTH AMERICA

9.4.1.2 EUROPE

9.4.1.3 ASIA-PACIFIC

9.4.1.4 SOUTH AMERICA

9.4.1.5 MIDDLE EAST & AFRICA

9.5 OTHERS

9.5.1 OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

9.5.1.1 NORTH AMERICA

9.5.1.2 EUROPE

9.5.1.3 ASIA-PACIFIC

9.5.1.4 SOUTH AMERICA

9.5.1.5 MIDDLE EAST & AFRICA

10 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION

10.1 OVERVIEW

10.2 GASTROINTESTINAL BLEEDING

10.2.1 GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

10.2.1.1 PEPTIC ULCER BLEEDING

10.2.1.2 ESOPHAGEAL VARICES

10.2.1.3 COLORECTAL CANCERS

10.2.2 GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE

10.2.2.1 MECHANICAL HEMOSTASIS DEVICES

10.2.2.2 THERMAL DEVICES

10.2.2.3 TOPICAL AGENTS AND INJECTABLES

10.2.2.4 OTHERS

10.2.3 GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

10.2.3.1 NORTH AMERICA

10.2.3.2 EUROPE

10.2.3.3 ASIA-PACIFIC

10.2.3.4 SOUTH AMERICA

10.2.3.5 MIDDLE EAST & AFRICA

10.3 NON-GASTROINTESTINAL BLEEDING

10.3.1 NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

10.3.1.1 NASAL BLEEDING (EPISTAXIS)

10.3.1.2 POST-SURGICAL BLEEDING

10.3.2 NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE

10.3.2.1 MECHANICAL HEMOSTASIS DEVICES

10.3.2.2 THERMAL DEVICES

10.3.2.3 TOPICAL AGENTS & INJECTABLES

10.3.2.4 OTHERS

10.3.3 NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

10.3.3.1 NORTH AMERICA

10.3.3.2 EUROPE

10.3.3.3 ASIA-PACIFIC

10.3.3.4 SOUTH AMERICA

10.3.3.5 MIDDLE EAST & AFRICA

10.4 TRAUMA MANAGEMENT

10.4.1 TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE

10.4.1.1 MECHANICAL HEMOSTASIS DEVICES

10.4.1.2 THERMAL DEVICES

10.4.1.3 TOPICAL AGENTS & INJECTABLES

10.4.1.4 OTHERS

10.4.2 TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

10.4.2.1 NORTH AMERICA

10.4.2.2 EUROPE

10.4.2.3 ASIA-PACIFIC

10.4.2.4 SOUTH AMERICA

10.4.2.5 MIDDLE EAST & AFRICA

10.5 OTHERS

10.5.1 OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

10.5.1.1 NORTH AMERICA

10.5.1.2 EUROPE

10.5.1.3 ASIA-PACIFIC

10.5.1.4 SOUTH AMERICA

10.5.1.5 MIDDLE EAST & AFRICA

11 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY END USER

11.1 OVERVIEW

11.2 HOSPITALS

11.2.1 HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE

11.2.1.1 PUBLIC

11.2.1.2 PRIVATE

11.2.2 HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

11.2.2.1 NORTH AMERICA

11.2.2.2 EUROPE

11.2.2.3 ASIA-PACIFIC

11.2.2.4 SOUTH AMERICA

11.2.2.5 MIDDLE EAST & AFRICA

11.3 AMBULATORY SURGERY CENTERS

11.3.1 AMBULATORY SURGERY CENTERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

11.3.1.1 NORTH AMERICA

11.3.1.2 EUROPE

11.3.1.3 ASIA-PACIFIC

11.3.1.4 SOUTH AMERICA

11.3.1.5 MIDDLE EAST & AFRICA

11.4 SPECIALTY CLINICS

11.4.1 SPECIALTY CLINICS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

11.4.1.1 NORTH AMERICA

11.4.1.2 EUROPE

11.4.1.3 ASIA-PACIFIC

11.4.1.4 SOUTH AMERICA

11.4.1.5 MIDDLE EAST & AFRICA

11.5 OTHERS

11.5.1 OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

11.5.1.1 NORTH AMERICA

11.5.1.2 EUROPE

11.5.1.3 ASIA-PACIFIC

11.5.1.4 SOUTH AMERICA

11.5.1.5 MIDDLE EAST & AFRICA

12 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL

12.1 OVERVIEW

12.2 INDIRECT SALES

12.2.1 INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE

12.2.1.1 OFFLINE

12.2.1.2 ONLINE

12.2.2 INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

12.2.2.1 NORTH AMERICA

12.2.2.2 EUROPE

12.2.2.3 ASIA-PACIFIC

12.2.2.4 SOUTH AMERICA

12.2.2.5 MIDDLE EAST & AFRICA

12.3 DIRECT SALES

12.3.1 DIRECT SALES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

12.3.1.1 NORTH AMERICA

12.3.1.2 EUROPE

12.3.1.3 ASIA-PACIFIC

12.3.1.4 SOUTH AMERICA

12.3.1.5 MIDDLE EAST & AFRICA

13 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY REGION

13.1 OVERVIEW

13.2 NORTH AMERICA

13.2.1 U.S.

13.2.2 CANADA

13.2.3 MEXICO

13.3 EUROPE

13.3.1 GERMANY

13.3.2 U.K.

13.3.3 FRANCE

13.3.4 ITALY

13.3.5 SPAIN

13.3.6 NETHERLANDS

13.3.7 BELGIUM

13.3.8 SWITZERLAND

13.3.9 SWEDEN

13.3.10 DENMARK

13.3.11 NORWAY

13.3.12 FINLAND

13.3.13 RUSSIA

13.3.14 TURKEY

13.3.15 REST OF EUROPE

13.4 ASIA PACIFIC

13.4.1 CHINA

13.4.2 JAPAN

13.4.3 INDIA

13.4.4 SOUTH KOREA

13.4.5 AUSTRALIA

13.4.6 INDONESIA

13.4.7 THAILAND

13.4.8 MALAYSIA

13.4.9 SINGAPORE

13.4.10 PHILIPPINES

13.4.11 NEW ZEALAND

13.4.12 HONG KONG

13.4.13 TAIWAN

13.4.14 REST OF ASIA-PACIFIC

13.5 MIDDLE EAST AND AFRICA

13.5.1 SAUDI ARABIA

13.5.2 UNITED ARAB EMIRATES

13.5.3 EGYPT

13.5.4 ISRAEL

13.5.5 QATAR

13.5.6 KUWAIT

13.5.7 OMAN

13.5.8 BAHRAIN

13.5.9 REST OF MIDDLE EAST AND AFRICA

13.6 SOUTH AMERICA

13.6.1 BRAZIL

13.6.2 ARGENTINA

13.6.3 COLOMBIA

13.6.4 CHILE

13.6.5 PERU

13.6.6 ECUADOR

13.6.7 VENEZUELA

13.6.8 URUGUAY

13.6.9 PARAGUAY

13.6.10 BOLIVIA

13.6.11 REST OF SOUTH AMERICA

14 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET: COMPANY LANDSCAPE

14.1 COMPANY SHARE ANALYSIS: GLOBAL

14.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

14.3 COMPANY SHARE ANALYSIS: EUROPE

14.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

15 SWOT ANALYSIS

16 COMPANY PROFILES MANUFACTURERS

16.1 OLYMPUS CORPORATION

16.1.1 COMPANY SNAPSHOT

16.1.2 REVENUE ANALYSIS

16.1.3 COMPANY SHARE ANALYSIS

16.1.4 PRODUCT PORTFOLIO

16.1.5 RECENT DEVELOPMENT

16.2 BOSTON SCIENTIFIC CORPORATION

16.2.1 COMPANY SNAPSHOT

16.2.2 REVENUE ANALYSIS

16.2.3 COMPANY SHARE ANALYSIS

16.2.4 PRODUCT PORTFOLIO

16.2.5 RECENT DEVELOPMENT

16.3 CONMED CORPORATION

16.3.1 COMPANY SNAPSHOT

16.3.2 REVENUE ANALYSIS

16.3.3 COMPANY SHARE ANALYSIS

16.3.4 PRODUCT PORTFOLIO

16.3.5 RECENT DEVELOPMENT

16.4 MEDTRONIC

16.4.1 COMPANY SNAPSHOT

16.4.2 REVENUE ANALYSIS

16.4.3 COMPANY SHARE ANALYSIS

16.4.4 PRODUCT PORTFOLIO

16.4.5 RECENT DEVELOPMENT

16.5 COOK

16.5.1 COMPANY SNAPSHOT

16.5.2 COMPANY SHARE ANALYSIS

16.5.3 PRODUCT PORTFOLIO

16.5.4 RECENT DEVELOPMENT

16.6 ANKAFERD

16.6.1 COMPANY SNAPSHOT

16.6.2 PRODUCT PORTFOLIO

16.6.3 RECENT DEVEOPMENT

16.7 B. BRAUN SE

16.7.1 COMPANY SNAPSHOT

16.7.2 PRODUCT PORTFOLIO

16.7.3 RECENT DEVEOPMENT

16.8 CREO MEDICAL GMBH

16.8.1 COMPANY SNAPSHOT

16.8.2 PRODUCT PORTFOLIO

16.8.3 RECENT DEVELOPMENT

16.9 DIVERSATEK, INC.

16.9.1 COMPANY SNAPSHOT

16.9.2 PRODUCT PORTFOLIO

16.9.3 RECENT DEVEOPMENT

16.1 DUOMED GROUP

16.10.1 COMPANY SNAPSHOT

16.10.2 PRODUCT PORTFOLIO

16.10.3 RECENT DEVEOPMENT

16.11 ENDOCLOT PLUS, INC.

16.11.1 COMPANY SNAPSHOT

16.11.2 PRODUCT PORTFOLIO

16.11.3 RECENT DEVEOPMENT

16.12 ERBE ELEKTROMEDIZIN GMBH

16.12.1 COMPANY SNAPSHOT

16.12.2 PRODUCT PORTFOLIO

16.12.3 RECENT DEVELOPMENT

16.13 FUJIFILM HOLDINGS CORPORATION

16.13.1 COMPANY SNAPSHOT

16.13.2 REVENUE ANALYSIS

16.13.3 PRODUCT PORTFOLIO

16.13.4 RECENT DEVELOPMENT

16.14 JOHNSON & JOHNSON (ETHICON)

16.14.1 COMPANY SNAPSHOT

16.14.2 REVENUE ANALYSIS

16.14.3 PRODUCT PORTFOLIO

16.14.4 RECENT DEVEOPMENT

16.15 KARL STORZ SE & CO. KG, TUTTLINGEN

16.15.1 COMPANY SNAPSHOT

16.15.2 PRODUCT PORTFOLIO

16.15.3 RECENT DEVEOPMENT

16.16 MEDITALIA S.R.L.

16.16.1 COMPANY SNAPSHOT

16.16.2 PRODUCT PORTFOLIO

16.16.3 RECENT DEVELOPMENT

16.17 MICRO-TECH ENDOSCOPY

16.17.1 COMPANY SNAPSHOT

16.17.2 PRODUCT PORTFOLIO

16.17.3 RECENT DEVELOPMENT

16.18 MTW ENDOSKOPIE MANUFAKTU

16.18.1 COMPANY SNAPSHOT

16.18.2 PRODUCT PORTFOLIO

16.18.3 RECENT DEVEOPMENT

16.19 OVESCO ENDOSCOPY AG

16.19.1 COMPANY SNAPSHOT

16.19.2 PRODUCT PORTFOLIO

16.19.3 RECENT DEVEOPMENT

16.2 PENTAX MEDICAL

16.20.1 COMPANY SNAPSHOT

16.20.2 SOLUTION PORTFOLIO

16.20.3 RECENT DEVELOPMENT

16.21 STERIS

16.21.1 COMPANY SNAPSHOT

16.21.2 REVENUE ANALYSIS

16.21.3 PRODUCT PORTFOLIO

16.21.4 RECENT DEVELOPMENT

17 COMPANY PROFILES DISTRIBUTOR

17.1 BOSTON IVY HEALTHCARE SOLUTIONS PRIVATE LIMITED

17.1.1 COMPANY SNAPSHOT

17.1.2 PRODUCT PORTFOLIO

17.1.3 RECENT DEVELOPMENT

17.2 CARDINAL HEALTH

17.2.1 COMPANY SNAPSHOT

17.2.2 REVENUE ANALYSIS

17.2.3 PRODUCT PORTFOLIO

17.2.4 RECENT DEVEOPMENT

17.3 HENRY SCHEIN, INC.

17.3.1 COMPANY SNAPSHOT

17.3.2 REVENUE ANALYSIS

17.3.3 PRODUCT PORTFOLIO

17.3.4 RECENT DEVEOPMENT

17.4 MCKESSON MEDICAL-SURGICAL INC.

17.4.1 COMPANY SNAPSHOT

17.4.2 PRODUCT PORTFOLIO

17.4.3 RECENT DEVEOPMENT

17.5 MFI MEDICAL

17.5.1 COMPANY SNAPSHOT

17.5.2 PRODUCT PORTFOLIO

17.5.3 RECENT DEVEOPMENT

18 QUESTIONNAIRE

19 RELATED REPORTS

List of Table

TABLE 1 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 2 GLOBAL MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 3 GLOBAL HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 4 GLOBAL HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 5 GLOBAL BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 6 GLOBAL MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 7 GLOBAL THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 8 GLOBAL BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 9 GLOBAL BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 10 GLOBAL THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 11 GLOBAL TOPICAL AGENTS & INJECTABLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 12 GLOBAL TOPICAL AGENTS AND INJECTABLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 13 GLOBAL OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 14 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 15 GLOBAL UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 16 GLOBAL UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 17 GLOBAL LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 18 GLOBAL LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 19 GLOBAL BRONCHOSCOPIC HEMOSTASIS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 20 GLOBAL OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 21 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 22 GLOBAL GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 23 GLOBAL GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 24 GLOBAL GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 25 GLOBAL NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 26 GLOBAL NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 27 GLOBAL NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 28 GLOBAL TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 29 GLOBAL TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 30 GLOBAL OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 31 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 32 GLOBAL HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 33 GLOBAL HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 34 GLOBAL AMBULATORY SURGERY CENTERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 35 GLOBAL SPECIALTY CLINICS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 36 GLOBAL OTHERS IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 37 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 38 GLOBAL INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 39 GLOBAL INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 40 GLOBAL DIRECT SALES IN ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 41 GLOBAL ENDOSCOPIC HEMOSTASIS MARKET, BY REGION, 2018-2033, (USD THOUSAND)

TABLE 42 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 43 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 44 NORTH AMERICA MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 45 NORTH AMERICA HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 46 NORTH AMERICA HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 47 NORTH AMERICA BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 48 NORTH AMERICA THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 49 NORTH AMERICA BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 50 NORTH AMERICA BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 51 NORTH AMERICA TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 52 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 53 NORTH AMERICA UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 54 NORTH AMERICA LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 55 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 56 NORTH AMERICA GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 57 NORTH AMERICA GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 58 NORTH AMERICA NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 59 NORTH AMERICA NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 60 NORTH AMERICA TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 61 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 62 NORTH AMERICA HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 63 NORTH AMERICA ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 64 NORTH AMERICA INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 65 U.S. ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 66 U.S. MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 67 U.S. HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 68 U.S. HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 69 U.S. BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 70 U.S. THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 71 U.S. BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 72 U.S. BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 73 U.S. TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 74 U.S. ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 75 U.S. UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 76 U.S. LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 77 U.S. ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 78 U.S. GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 79 U.S. GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 80 U.S. NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 81 U.S. NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 82 U.S. TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 83 U.S. ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 84 U.S. HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 85 U.S. ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 86 U.S. INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 87 CANADA ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 88 CANADA MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 89 CANADA HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 90 CANADA HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 91 CANADA BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 92 CANADA THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 93 CANADA BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 94 CANADA BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 95 CANADA TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 96 CANADA ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 97 CANADA UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 98 CANADA LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 99 CANADA ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 100 CANADA GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 101 CANADA GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 102 CANADA NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 103 CANADA NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 104 CANADA TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 105 CANADA ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 106 CANADA HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 107 CANADA ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 108 CANADA INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 109 MEXICO ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 110 MEXICO MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 111 MEXICO HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 112 MEXICO HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 113 MEXICO BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 114 MEXICO THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 115 MEXICO BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 116 MEXICO BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 117 MEXICO TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 118 MEXICO ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 119 MEXICO UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 120 MEXICO LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 121 MEXICO ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 122 MEXICO GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 123 MEXICO GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 124 MEXICO NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 125 MEXICO NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 126 MEXICO TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 127 MEXICO ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 128 MEXICO HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 129 MEXICO ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 130 MEXICO INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 131 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY COUNTRY, 2018-2033 (USD THOUSAND)

TABLE 132 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 133 EUROPE MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 134 EUROPE HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 135 EUROPE HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 136 EUROPE BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 137 EUROPE THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 138 EUROPE BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 139 EUROPE BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 140 EUROPE TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 141 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 142 EUROPE UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 143 EUROPE LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 144 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 145 EUROPE GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 146 EUROPE GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 147 EUROPE NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 148 EUROPE NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 149 EUROPE TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 150 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 151 EUROPE HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 152 EUROPE ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 153 EUROPE INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 154 GERMANY ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 155 GERMANY MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 156 GERMANY HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 157 GERMANY HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 158 GERMANY BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 159 GERMANY THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 160 GERMANY BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 161 GERMANY BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 162 GERMANY TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 163 GERMANY ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 164 GERMANY UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 165 GERMANY LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 166 GERMANY ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 167 GERMANY GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 168 GERMANY GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 169 GERMANY NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 170 GERMANY NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 171 GERMANY TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 172 GERMANY ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 173 GERMANY HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 174 GERMANY ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 175 GERMANY INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 176 U.K. ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 177 U.K. MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 178 U.K. HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 179 U.K. HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 180 U.K. BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 181 U.K. THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 182 U.K. BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 183 U.K. BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 184 U.K. TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 185 U.K. ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 186 U.K. UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 187 U.K. LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 188 U.K. ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 189 U.K. GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 190 U.K. GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 191 U.K. NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 192 U.K. NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 193 U.K. TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 194 U.K. ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 195 U.K. HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 196 U.K. ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 197 U.K. INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 198 FRANCE ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 199 FRANCE MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 200 FRANCE HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 201 FRANCE HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 202 FRANCE BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 203 FRANCE THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 204 FRANCE BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 205 FRANCE BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 206 FRANCE TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 207 FRANCE ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 208 FRANCE UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 209 FRANCE LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 210 FRANCE ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 211 FRANCE GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 212 FRANCE GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 213 FRANCE NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 214 FRANCE NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 215 FRANCE TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 216 FRANCE ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 217 FRANCE HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 218 FRANCE ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 219 FRANCE INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 220 ITALY ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 221 ITALY MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 222 ITALY HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 223 ITALY HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 224 ITALY BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 225 ITALY THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 226 ITALY BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 227 ITALY BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 228 ITALY TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 229 ITALY ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 230 ITALY UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 231 ITALY LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 232 ITALY ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 233 ITALY GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 234 ITALY GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 235 ITALY NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 236 ITALY NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 237 ITALY TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 238 ITALY ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 239 ITALY HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 240 ITALY ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 241 ITALY INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 242 SPAIN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 243 SPAIN MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 244 SPAIN HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 245 SPAIN HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 246 SPAIN BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 247 SPAIN THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 248 SPAIN BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 249 SPAIN BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 250 SPAIN TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 251 SPAIN ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)

TABLE 252 SPAIN UPPER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 253 SPAIN LOWER GASTROINTESTINAL ENDOSCOPY IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 254 SPAIN ENDOSCOPIC HEMOSTASIS MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 255 SPAIN GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 256 SPAIN GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 257 SPAIN NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 258 SPAIN NON-GASTROINTESTINAL BLEEDING IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 259 SPAIN TRAUMA MANAGEMENT IN ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 260 SPAIN ENDOSCOPIC HEMOSTASIS MARKET, BY END USER, 2018-2033 (USD THOUSAND)

TABLE 261 SPAIN HOSPITALS IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 262 SPAIN ENDOSCOPIC HEMOSTASIS MARKET, BY DISTRIBUTION CHANNEL, 2018-2033 (USD THOUSAND)

TABLE 263 SPAIN INDIRECT SALES IN ENDOSCOPIC HEMOSTASIS, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 264 NETHERLANDS ENDOSCOPIC HEMOSTASIS MARKET, BY PRODUCT TYPE, 2018-2033 (USD THOUSAND)

TABLE 265 NETHERLANDS MECHANICAL HEMOSTASIS DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 266 NETHERLANDS HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 267 NETHERLANDS HEMOSTATIC CLIPS IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY MATERIAL, 2018-2033 (USD THOUSAND)

TABLE 268 NETHERLANDS BANDING DEVICES IN MECHANICAL HEMOSTASIS DEVICES MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 269 NETHERLANDS THERMAL DEVICES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 270 NETHERLANDS BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY ENERGY TYPE, 2018-2033 (USD THOUSAND)

TABLE 271 NETHERLANDS BIPOLAR COAGULATION IN THERMAL DEVICES MARKET, BY APPLICATION, 2018-2033 (USD THOUSAND)

TABLE 272 NETHERLANDS TOPICAL AGENTS & INJECTIBLES IN ENDOSCOPIC HEMOSTASIS MARKET, BY TYPE, 2018-2033 (USD THOUSAND)

TABLE 273 NETHERLANDS ENDOSCOPIC HEMOSTASIS MARKET, BY PROCEDURE, 2018-2033 (USD THOUSAND)