Global Enhanced Ambulatory Patient Grouping Software Market

Market Size in USD Billion

USD

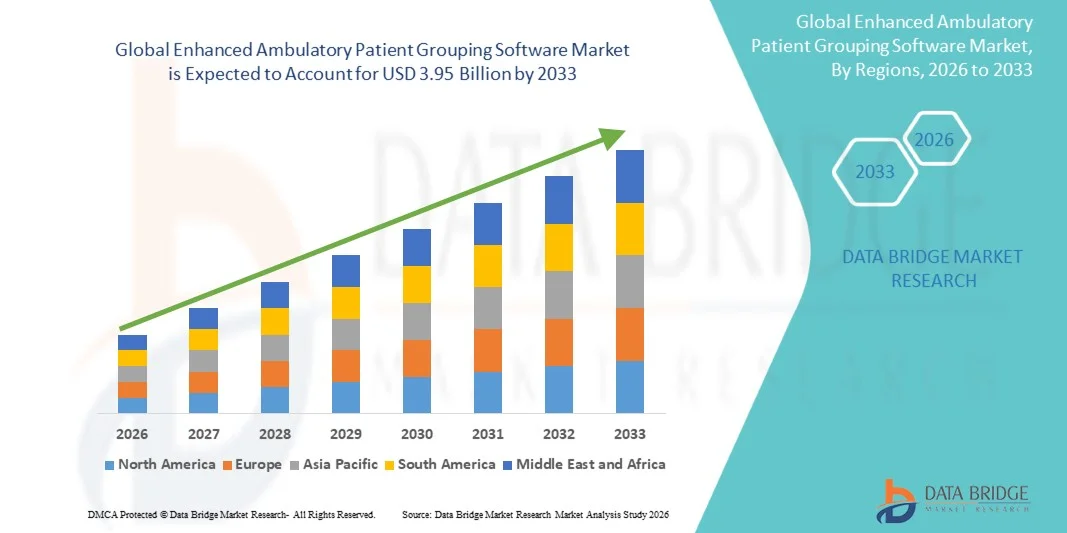

2.09 Billion

USD

3.95 Billion

2025

2033

USD

2.09 Billion

USD

3.95 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.09 Billion | |

| USD 3.95 Billion | |

| % | |

|

Enhanced Ambulatory Patient Grouping Software Market Overview

The Enhanced Ambulatory Patient Grouping Software Market was valued at USD 2.09 billion in 2025 and is projected to reach USD 3.95 billion by 2033, growing at a CAGR of 8.30% from 2026 to 2033. The market is experiencing consistent growth driven by the increasing adoption of digital healthcare technologies, rising demand for accurate healthcare reimbursement systems, and growing implementation of value-based care models across hospitals and ambulatory care centers. Advancements in healthcare IT infrastructure, integration of AI-enabled coding solutions, and expanding demand for efficient outpatient payment classification systems are further supporting market expansion globally.

The growing volume of outpatient visits, increasing complexity of medical billing processes, and rising emphasis on reducing healthcare administrative costs are compelling healthcare providers, payers, and ambulatory surgical centers to adopt advanced Enhanced Ambulatory Patient Grouping (EAPG) software solutions. AI-enabled and cloud-based EAPG platforms are increasingly replacing conventional manual coding and reimbursement methods in many healthcare systems, offering cost-effective, accurate, and streamlined claim processing environments for healthcare revenue cycle management and regulatory compliance.

Key Market Trends & Insights

- North America dominated the Enhanced Ambulatory Patient Grouping Software Market with the largest revenue share of 36.18% in 2025, supported by advanced healthcare IT infrastructure, increasing adoption of automated reimbursement management solutions, and strong implementation of value-based healthcare payment systems across the U.S. and Canada.

- The On-Premises segment dominated the market with a share of 58.42% in 2025 due to its widespread adoption among large hospitals, government healthcare agencies, and integrated healthcare networks that require enhanced data security, regulatory compliance, and greater control over patient billing and reimbursement systems

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by expanding healthcare digitization initiatives, rising healthcare expenditure, increasing outpatient care volumes, and growing adoption of healthcare revenue cycle management solutions in China, India, and Japan.

- The Cloud-Based segment is the fastest-growing delivery mode, projected to register a CAGR of 7.3%, reflecting the increasing demand for scalable, cost-effective, and remotely accessible healthcare reimbursement and patient grouping solutions.

- The Hospitals segment dominates the end user category with a 39.84% revenue share in 2025, led by rising patient admissions, increasing outpatient reimbursement complexities, and growing implementation of automated EAPG software for claims processing and financial management.

- The Predicting and Verifying Expected Payment segment accounted for 34.67% of the market, preferred by healthcare providers and payers requiring accurate reimbursement calculations, payment verification, and optimized revenue cycle management performance.

- The Clinical Insight segment is the fastest-growing application category, with a CAGR of 7.1%, driven by increasing demand for data-driven clinical decision-making, healthcare analytics integration, and improved patient outcome monitoring across modern healthcare systems.

Market Size & Forecast

- Global Market Value (2025): USD 2.09 Billion

- Expected Market Value (2033): USD 3.95 Billion

- Forecast CAGR (2026–2033): 8.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Enhanced Ambulatory Patient Grouping Software Market Segmentation

|

Attributes |

Enhanced Ambulatory Patient Grouping Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• 3M Health Information Systems (U.S.) |

|

Market Opportunities |

· Expansion of Cloud-Based Healthcare Revenue Cycle Management Solutions · Growing Implementation of Value-Based Healthcare and Payment Reform Programs · Increasing Adoption of AI-Enabled Healthcare Analytics and Automation Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Enhanced Ambulatory Patient Grouping Software Market Trends

Trend: Increasing Adoption of AI-Enabled Healthcare Revenue Cycle Management and Outpatient Reimbursement Solutions

Healthcare providers are increasingly adopting advanced Enhanced Ambulatory Patient Grouping (EAPG) software solutions to improve outpatient reimbursement accuracy, optimize revenue cycle management, and streamline healthcare claims processing operations. The growing shift toward value-based care models and outpatient healthcare services is accelerating demand for automated patient grouping systems capable of handling complex billing structures and regulatory compliance requirements. In addition, hospitals, ambulatory surgical centers, and physician clinics are integrating AI-enabled coding and analytics platforms to reduce claim denials, improve payment transparency, and enhance financial performance. For instance, several healthcare systems across North America expanded deployment of cloud-based reimbursement management platforms during 2023–2025 to improve operational efficiency and reduce administrative burdens associated with outpatient payment processing. Furthermore, integration of predictive analytics, electronic health records (EHRs), and automated coding technologies is improving reimbursement accuracy and supporting data-driven healthcare decision-making globally.

Enhanced Ambulatory Patient Grouping Software Market Dynamics

Key Market Driver: Rising Adoption of Value-Based Healthcare and Increasing Outpatient Care Volumes

The increasing transition from fee-for-service reimbursement models to value-based healthcare systems is significantly driving demand for Enhanced Ambulatory Patient Grouping Software globally. Healthcare providers, payers, and government agencies are increasingly utilizing EAPG software to standardize outpatient payment systems, improve reimbursement accuracy, and enhance healthcare cost management. The growing number of outpatient visits, ambulatory surgical procedures, and chronic disease management programs is further accelerating the need for automated patient grouping and healthcare financial analysis platforms.

For instance, rising outpatient service utilization across the U.S., Canada, Germany, and Japan has increased adoption of AI-enabled revenue cycle management and patient grouping software among hospitals and ambulatory care centers. In addition, expanding healthcare digitization initiatives and regulatory requirements for accurate claims processing are encouraging healthcare organizations to invest in advanced reimbursement verification and clinical analytics solutions. The integration of EHR systems, automated coding technologies, and cloud-based healthcare management platforms is also supporting widespread adoption of EAPG software globally.

Key Restraint/Challenge: High Implementation Costs and Complex Regulatory Compliance Requirements

A significant restraint in the Enhanced Ambulatory Patient Grouping Software Market is the high implementation and maintenance cost associated with advanced healthcare IT and reimbursement management systems. Modern EAPG platforms require substantial investment in software integration, cybersecurity infrastructure, cloud deployment, employee training, and ongoing technical support. Smaller hospitals, physician clinics, and independent healthcare providers often face financial challenges in adopting advanced reimbursement management solutions due to limited IT budgets and operational constraints.

In addition, strict healthcare data privacy and reimbursement regulations imposed by authorities such as HIPAA in the U.S. and GDPR in Europe increase compliance and operational complexity for software vendors and healthcare organizations. Companies must ensure secure patient data management, interoperability with existing hospital systems, and continuous coding updates aligned with changing reimbursement guidelines. Furthermore, rising cybersecurity concerns and increasing costs associated with AI-enabled healthcare software deployment during 2023–2025 impacted adoption among certain cost-sensitive healthcare facilities globally.

Key Market Opportunity: Expansion of Cloud-Based Healthcare Analytics and AI-Driven Reimbursement Platforms

The growing adoption of cloud computing, predictive analytics, and AI-enabled healthcare automation technologies presents a major opportunity for the market. Healthcare organizations are increasingly deploying cloud-based EAPG software platforms to improve scalability, automate coding workflows, and enhance real-time reimbursement analysis across multi-location healthcare systems. AI-powered reimbursement management solutions are gaining traction due to their ability to minimize claim denials, improve payment forecasting, and support efficient healthcare financial management.

For instance, several healthcare technology providers across the U.S. and Europe expanded investments in AI-assisted revenue cycle management and automated outpatient payment verification platforms during 2024–2025 to improve healthcare operational efficiency and reduce administrative costs. In addition, rising healthcare digitization initiatives across China, India, Brazil, and Southeast Asia are creating strong growth opportunities for EAPG software vendors to expand cloud-based healthcare analytics solutions and strengthen global distribution networks.

Enhanced Ambulatory Patient Grouping Software Market Scope

The Enhanced Ambulatory Patient Grouping Software market is segmented on the basis of delivery mode, end user, and application.

- By Delivery Mode

On the basis of delivery mode, the Enhanced Ambulatory Patient Grouping Software Market is segmented into on-premises and cloud-based. The On-Premises segment dominated the market with a share of 58.42% in 2025 due to its widespread adoption among large hospitals, government healthcare agencies, and integrated healthcare networks that require enhanced data security, regulatory compliance, and greater control over patient billing and reimbursement systems. Healthcare providers prefer on-premises deployment for managing sensitive patient records, claims processing, and reimbursement analytics while complying with HIPAA and other healthcare data protection regulations. In addition, strong investments in healthcare IT infrastructure, increasing integration with hospital information systems (HIS), and demand for customized reimbursement workflow management solutions continue to support segment dominance. Large healthcare institutions also benefit from reduced latency, improved operational control, and seamless integration with electronic health records (EHRs) and revenue cycle management systems. The presence of established IT support teams and long-term software maintenance contracts further strengthens adoption across developed healthcare markets. Furthermore, increasing use of predictive analytics and AI-powered coding tools within on-premises environments is enhancing operational efficiency and reimbursement accuracy across healthcare facilities globally.

The Cloud-Based segment is expected to witness the fastest CAGR of 8.1% from 2026 to 2033, driven by rising adoption of scalable healthcare IT infrastructure, increasing digital transformation initiatives, and growing demand for remote accessibility across healthcare systems. Cloud-based EAPG software enables healthcare providers to streamline claims processing, improve interoperability, and reduce infrastructure costs while supporting real-time reimbursement analytics and automated updates. Increasing adoption among ambulatory surgical centers, physician clinics, and smaller healthcare facilities is accelerating market growth due to lower upfront investment requirements and flexible deployment capabilities. In addition, advancements in cloud security technologies, AI-enabled healthcare analytics, and integration with telehealth platforms are improving adoption globally. The growing focus on value-based healthcare reimbursement models and centralized healthcare data management is further driving demand for cloud-based EAPG platforms across North America, Europe, and Asia-Pacific healthcare markets.

- By End User

On the basis of end user, the Enhanced Ambulatory Patient Grouping Software Market is segmented into payers, hospitals, ambulatory surgical centers (ASCs), physician clinics, government agencies and researchers, billing services, business partner, and other providers. The Hospitals segment dominated the market with a share of 34.76% in 2025 due to the high volume of outpatient visits, increasing adoption of advanced healthcare reimbursement systems, and growing need for efficient claims management and coding accuracy. Hospitals are increasingly utilizing EAPG software solutions to optimize reimbursement workflows, reduce claim denials, improve revenue cycle management, and comply with evolving healthcare payment regulations. The widespread integration of EHR systems, AI-enabled coding platforms, and automated billing solutions is further supporting segment growth. In addition, rising patient admissions, increasing outpatient procedures, and growing focus on operational efficiency are accelerating software adoption across public and private hospitals globally. Healthcare institutions are also investing in predictive analytics and clinical documentation improvement tools to strengthen financial performance and improve reimbursement transparency. Furthermore, government healthcare reforms and value-based payment initiatives continue to enhance demand for advanced EAPG solutions across large hospital networks.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest CAGR of 8.4% from 2026 to 2033, driven by the rapid expansion of outpatient surgical procedures, rising preference for cost-effective ambulatory care, and increasing adoption of automated reimbursement systems. ASCs are increasingly implementing EAPG software to improve billing efficiency, optimize coding processes, and manage growing patient volumes effectively. The shift toward minimally invasive procedures and same-day surgeries is significantly contributing to segment growth across developed and emerging healthcare markets. In addition, cloud-based reimbursement platforms, automated claims management systems, and real-time financial analytics are improving operational workflows and reimbursement accuracy within ASCs. Rising investments in outpatient healthcare infrastructure and increasing partnerships between healthcare providers and insurance companies are further supporting segment expansion globally.

- By Application

On the basis of application, the Enhanced Ambulatory Patient Grouping Software Market is segmented into setting appropriate incentives, predicting and verifying expected payment, public reporting, quality comparisons, clinical insight, financial analysis, and defining episodes. The Predicting and Verifying Expected Payment segment dominated the market with a share of 31.64% in 2025 due to increasing demand for accurate reimbursement forecasting, claims validation, and healthcare payment transparency across hospitals, payers, and healthcare providers. Healthcare organizations are increasingly deploying EAPG software to automate payment calculations, reduce billing errors, and improve financial planning capabilities. The growing complexity of outpatient reimbursement systems and rising focus on reducing claim denials are significantly driving adoption across healthcare institutions globally. In addition, increasing implementation of value-based payment models and regulatory reporting requirements is accelerating demand for predictive reimbursement analytics solutions. Healthcare providers are also leveraging AI-powered coding verification tools and automated payment validation systems to improve operational efficiency and revenue cycle performance. Furthermore, the expansion of outpatient services and rising healthcare expenditure continue to strengthen demand for accurate payment verification platforms across both developed and emerging healthcare markets.

The Clinical Insight segment is expected to witness the fastest CAGR of 8.0% from 2026 to 2033, driven by growing demand for data-driven clinical decision-making, healthcare analytics, and patient outcome optimization solutions. Healthcare providers are increasingly adopting advanced EAPG platforms integrated with AI, machine learning, and predictive analytics tools to improve treatment planning, patient stratification, and care quality monitoring. The increasing focus on population health management and value-based healthcare delivery is accelerating adoption of clinical insight applications across hospitals, ASCs, and research institutions. In addition, growing integration of EHR systems, clinical documentation tools, and real-time patient analytics is enhancing healthcare workflow efficiency and operational transparency. Rising investments in healthcare digitalization and expanding adoption of advanced healthcare analytics platforms are further expected to support strong segment growth globally over the forecast period.

Enhanced Ambulatory Patient Grouping Software Market Regional Analysis

North America dominated the Enhanced Ambulatory Patient Grouping Software market and accounted for the largest revenue share of 36.18% in 2025, supported by advanced healthcare IT infrastructure, increasing adoption of automated reimbursement management solutions, and strong implementation of value-based healthcare payment systems across the U.S. and Canada. The region also benefits from widespread deployment of electronic health records (EHRs), growing focus on healthcare cost optimization, and increasing demand for accurate outpatient reimbursement and claims management systems. Rising investments in AI-enabled healthcare analytics, cloud-based revenue cycle management platforms, and healthcare interoperability solutions continue to strengthen North America’s leadership position in the global market.

U.S. Enhanced Ambulatory Patient Grouping Software Market Insight

The U.S. Enhanced Ambulatory Patient Grouping Software market is witnessing strong growth due to rising adoption of value-based reimbursement models, increasing outpatient care volumes, and expanding implementation of advanced healthcare revenue cycle management systems. The country’s highly developed healthcare infrastructure, along with widespread integration of electronic health records, AI-powered coding platforms, and automated claims processing technologies, is driving demand across hospitals, ambulatory surgical centers, and payer organizations. In addition, growing emphasis on reducing claim denials, improving reimbursement accuracy, and streamlining healthcare billing workflows is accelerating adoption of Enhanced Ambulatory Patient Grouping Software solutions across the U.S. healthcare system.

Europe Enhanced Ambulatory Patient Grouping Software Market Insight

The Europe Enhanced Ambulatory Patient Grouping Software market remains a major contributor to global revenue, driven by increasing healthcare digitization, strong government support for healthcare IT modernization, and growing demand for efficient outpatient reimbursement management solutions. The widespread adoption of healthcare analytics platforms, automated coding systems, and interoperable hospital information systems is supporting market expansion across the region. Increasing focus on healthcare cost control, patient outcome improvement, and regulatory compliance continues to strengthen adoption of Enhanced Ambulatory Patient Grouping Software throughout Europe.

U.K. Enhanced Ambulatory Patient Grouping Software Market Insight

The U.K. Enhanced Ambulatory Patient Grouping Software market is experiencing steady growth, supported by rising implementation of digital healthcare technologies, increasing outpatient service utilization, and growing focus on improving healthcare reimbursement efficiency. Healthcare providers are increasingly adopting AI-powered billing systems, cloud-based healthcare analytics platforms, and automated coding solutions to optimize revenue cycle management and reduce administrative burdens. Furthermore, ongoing NHS digital transformation initiatives and increasing investments in healthcare data interoperability are positioning the U.K. as a key innovation hub in the Enhanced Ambulatory Patient Grouping Software industry.

Germany Enhanced Ambulatory Patient Grouping Software Market Insight

The Germany Enhanced Ambulatory Patient Grouping Software market is expanding steadily due to the country’s advanced healthcare infrastructure, strong adoption of healthcare IT solutions, and increasing focus on improving operational efficiency within hospitals and outpatient care centers. Healthcare providers are increasingly utilizing automated reimbursement systems, predictive healthcare analytics, and digital claims management platforms to streamline billing workflows and improve payment accuracy. Continuous advancements in healthcare digitization, combined with government initiatives supporting smart healthcare systems and data integration, are further driving market growth in Germany.

Asia-Pacific Enhanced Ambulatory Patient Grouping Software Market Insight

The Asia-Pacific Enhanced Ambulatory Patient Grouping Software market is expected to witness rapid growth, driven by expanding healthcare digitization initiatives, rising healthcare expenditure, increasing outpatient care volumes, and growing adoption of healthcare revenue cycle management solutions across countries such as China, India, and Japan. Growing awareness regarding healthcare operational efficiency, increasing implementation of electronic medical records, and rising investments in healthcare IT infrastructure are supporting regional market expansion. In addition, the rapid expansion of private healthcare facilities, diagnostic centers, and outpatient care networks is accelerating adoption of Enhanced Ambulatory Patient Grouping Software across the region.

Japan Enhanced Ambulatory Patient Grouping Software Market Insight

The Japan Enhanced Ambulatory Patient Grouping Software market is witnessing consistent growth due to rising investments in healthcare automation technologies, increasing demand for accurate reimbursement systems, and growing focus on improving healthcare operational efficiency. Hospitals, outpatient clinics, and healthcare research organizations are increasingly adopting AI-enabled billing platforms, healthcare analytics systems, and automated coding solutions to optimize financial management and patient care delivery. Moreover, increasing integration of cloud-based healthcare systems and the country’s strong focus on digital healthcare innovation are further contributing to market growth.

China Enhanced Ambulatory Patient Grouping Software Market Insight

The China Enhanced Ambulatory Patient Grouping Software market is growing rapidly, driven by expanding healthcare infrastructure, rising government focus on healthcare digitization, and increasing adoption of automated reimbursement and hospital management systems. Growing implementation of AI-powered healthcare analytics platforms, cloud-based billing solutions, and interoperable electronic medical record systems across hospitals and outpatient care centers is significantly boosting market demand. In addition, rising healthcare expenditure, increasing patient volumes, and rapid technological advancements are positioning China as one of the fastest-growing markets for Enhanced Ambulatory Patient Grouping Software globally.

Enhanced Ambulatory Patient Grouping Software Market Share

The Enhanced Ambulatory Patient Grouping Software industry is primarily led by well-established companies, including:

- 3M Health Information Systems (U.S.)

- Cotiviti, Inc. (U.S.)

- Optum, Inc. (U.S.)

- Conduent Incorporated (U.S.)

- McKesson Corporation (U.S.)

- Oracle Cerner (U.S.)

- TruCode LLC (U.S.)

- MedeAnalytics, Inc. (U.S.)

- The SSI Group, LLC (U.S.)

- Change Healthcare (U.S.)

- Allscripts Healthcare Solutions, Inc. (U.S.)

- NextGen Healthcare, Inc. (U.S.)

- Health Catalyst, Inc. (U.S.)

- Experian Health (U.S.)

- Dolbey Systems, Inc. (U.S.)

- Nuance Communications, Inc. (U.S.)

- Epic Systems Corporation (U.S.)

- Craneware plc (U.K.)

- Wolters Kluwer N.V. (Netherlands)

- UnitedHealth Group Incorporated (U.S.)

- GE HealthCare Technologies Inc. (U.S.)

- Inovalon Holdings, Inc. (U.S.)

- MedAssets (U.S.)

- CareCloud, Inc. (U.S.)

- eClinicalWorks LLC (U.S.)

- Medical Information Technology, Inc. (MEDITECH) (U.S.)

- Waystar Holding Corp. (U.S.)

- R1 RCM Inc. (U.S.)

- athenahealth, Inc. (U.S.)

- FinThrive Revenue Systems, LLC (U.S.)

Latest Developments in Enhanced Ambulatory Patient Grouping Software Market

- In September 2025, Moog Inc. has unveiled its latest motion systems all electric E60 Series and the electro pneumatic P60 Series, setting a new benchmark for simulation across aviation, land, and maritime training with support for up to 14,000 kg loads and high fidelity motion for Level D flight simulators and other professional uses. The upgraded platforms deliver enhanced reliability, compact design and sustained operational uptime, reflecting modernized electronics and sustainable operation. These new systems strengthen Moog’s market leadership in simulation motion technology by boosting performance, energy efficiency, and usability

- In January 2025, Exail Technologies has acquired Leukos, a French photonics specialist known for pulsed micro lasers, supercontinuum laser sources, ultrafast lasers, and simulation-enabled optical systems, strengthening its technological and industrial capabilities in advanced laser and simulation technologies. The deal integrates Leukos’s expertise with Exail’s photonics, optical, and simulation platforms, broadening product offerings for applications in biophotonics, microelectronics, and high-fidelity training simulations. This strategic acquisition accelerates Exail’s innovation in high-tech technologies, creating synergies that expand its reach in scientific, industrial, and simulation applications while reinforcing its position as a leading advanced-technology provider

- In November 2025, IPG Automotive launched CarMaker 15.0, the latest version of its driving simulation software used for virtual vehicle development. The new release improves simulation accuracy by integrating virtual electronic control units (vECUs), allowing engineers to test software and vehicle systems at earlier development stages. It also includes enhanced sensor models and improved endurance testing capabilities for ADAS and autonomous vehicles. This development strengthens IPG Automotive’s position in the driving simulator market, as CarMaker enables automotive manufacturers to perform complex vehicle tests in a virtual driving environment instead of physical road testing.

- In November 2024, IPG Automotive released CarMaker 14.0, introducing new simulation capabilities including advanced sensor models and more realistic virtual environments. The update allows developers to simulate complex traffic scenarios involving pedestrians, vehicles, and different weather conditions. These features help automotive companies test ADAS and autonomous driving systems more efficiently in driving simulators, reducing development time and cost. The upgrade also expanded simulation capabilities for heavy-duty vehicles using the TruckMaker platform.

- In June 2023, IPG Automotive participated in the UNICARagil research project, collaborating with universities and industry partners to develop automated vehicle architectures. The company contributed its CarMaker driving simulation platform to support simulation and validation of automated driving systems in Software-in-the-Loop (SIL) and Hardware-in-the-Loop (HIL) environments. This collaboration demonstrates the application of Enhanced Ambulatory Patient Grouping Software in research and development of autonomous mobility solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.