Global Epigenetic Reader Protein Inhibitor Market

Market Size in USD Billion

USD

936.00 Billion

USD

3,971.27 Billion

2025

2033

USD

936.00 Billion

USD

3,971.27 Billion

2025

2033

| 2026 - 2033 | |

| USD 936.00 Billion | |

| USD 3,971.27 Billion | |

| % | |

|

Epigenetic Reader Protein Inhibitor Market Size

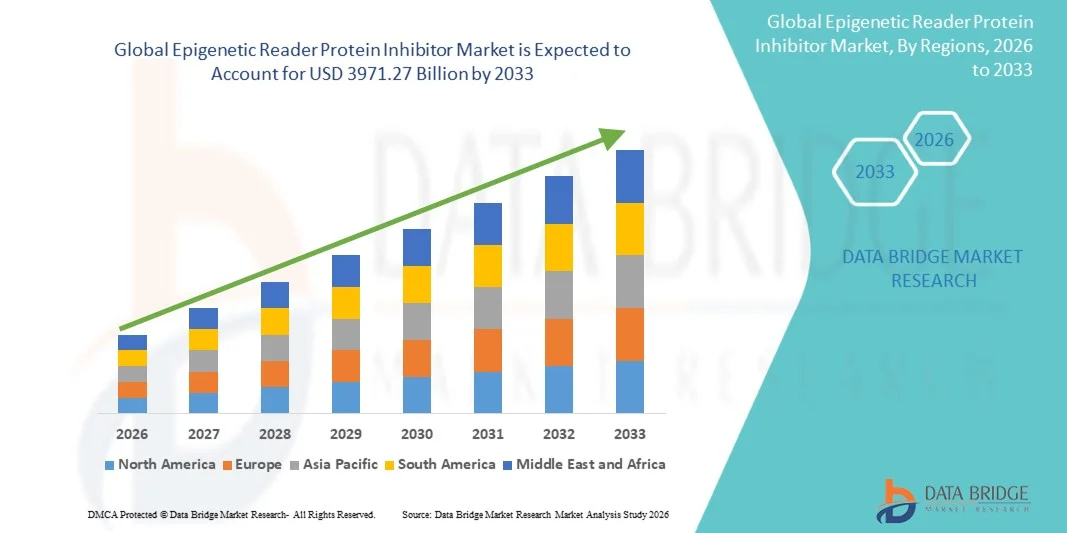

- The global epigenetic reader protein inhibitor market size was valued at USD 936.00 billion in 2025 and is expected to reach USD 3971.27 billion by 2033, at a CAGR of 19.80% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress within epigenome-targeted drug discovery platforms and precision oncology strategies, leading to increased utilization of epigenetic reader protein inhibitors in both clinical trial and approved therapeutic settings

- Furthermore, rising demand for mechanistically innovative, chromatin-targeted, and transcriptionally selective oncology and immunology treatment solutions is establishing epigenetic reader protein inhibitors as the modern targeted epigenetic therapy of choice. These converging factors are accelerating the uptake of epigenetic reader protein inhibitor solutions, thereby significantly boosting the industry's growth

Epigenetic Reader Protein Inhibitor Market Analysis

- Epigenetic reader protein inhibitors, offering targeted disruption of chromatin reader domain interactions with modified histone residues to selectively suppress oncogenic transcriptional programs driven by aberrant epigenetic signaling, are increasingly vital components of modern oncology and immunology drug development in both clinical and translational research settings due to their enhanced transcriptional selectivity, mechanistic differentiation from conventional cytotoxic chemotherapy, and seamless integration with combination immunotherapy and targeted therapy treatment regimens

- The escalating demand for epigenetic reader protein inhibitors is primarily fueled by the widespread prevalence of hematological malignancies and solid tumors driven by aberrant epigenetic reader protein activity, growing recognition of chromatin dysregulation as a major driver of oncogenesis and treatment resistance, and a rising preference for precision epigenomics strategies that selectively suppress disease-driving transcriptional programs

- North America dominated the epigenetic reader protein inhibitor market with the largest revenue share of 39% in 2025, characterized by early clinical adoption of epigenome-targeted therapies, high R&D investment, and a strong presence of key pharmaceutical and biotechnology companies, with the U.S. experiencing substantial growth in epigenetic reader protein inhibitor clinical trial activity, particularly in hematological malignancy and solid tumor combination regimens, driven by innovations from both established oncology pharmaceutical companies and startups focusing on next-generation bromodomain and chromodomain inhibitor design

- Asia-Pacific is expected to be the fastest growing region in the epigenetic reader protein inhibitor market during the forecast period due to increasing cancer incidence rates and rising investment in oncology drug development and epigenomics research infrastructure

- The oral segment held the largest market revenue share of 64.7% in 2025, driven by the predominant formulation of leading clinical-stage BET bromodomain inhibitor candidates including pelabresib and INCB057643 as oral small molecule tablets enabling convenient outpatient administration compatible with the chronic dosing schedules required for epigenetic reader protein inhibitor therapy

Report Scope and Epigenetic Reader Protein Inhibitor Market Segmentation

|

Attributes |

Epigenetic Reader Protein Inhibitor Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Epigenetic Reader Protein Inhibitor Market Trends

“Enhanced Therapeutic Selectivity Through Next-Generation Reader Domain Inhibitor Design and Biomarker-Driven Patient Stratification”

- A significant and accelerating trend in the global epigenetic reader protein inhibitor market is the deepening integration of next-generation reader domain inhibitor design platforms with epigenomic biomarker-based patient stratification strategies. This fusion of precision chromatin chemistry and companion diagnostics is significantly enhancing the therapeutic selectivity and clinical efficacy of epigenetic reader protein inhibitor therapies

- For instance, Constellation Pharmaceuticals has actively pursued the development of pelabresib (CPI-0610), a next-generation BET bromodomain inhibitor designed to selectively suppress BRD4-dependent transcriptional oncogenic programs in myelofibrosis and hematological malignancies. Similarly, Incyte Corporation has advanced its INCB057643 BET bromodomain inhibitor candidate with a combination clinical development strategy incorporating ruxolitinib to achieve synergistic transcriptional reprogramming in myeloproliferative neoplasm patient populations

- Advances in epigenomic biomarker identification and chromatin accessibility profiling technologies enable features such as patient pre-selection based on BET-dependent transcriptional program dependency, enabling more accurate identification of patient populations most likely to respond to BET bromodomain inhibitor therapy. For instance, ChIP-seq and ATAC-seq based chromatin profiling assays are being integrated into clinical trial designs to identify patients with the highest degree of BRD4 occupancy at oncogenic enhancer loci expected to derive the greatest therapeutic benefit from BET inhibitor treatment. In addition, the development of companion diagnostic assays capable of quantifying reader domain protein expression levels and chromatin accessibility from tissue biopsies or liquid biopsy platforms is creating new opportunities to guide epigenetic reader protein inhibitor patient selection in routine clinical practice

- The seamless integration of epigenetic reader protein inhibitors with immune checkpoint inhibitor combination regimens, targeted kinase inhibitor protocols, and standard-of-care chemotherapy platforms facilitates broader clinical adoption across multiple hematological malignancy and solid tumor indications. Through rationally designed combination strategies, oncologists can leverage the transcriptional reprogramming and MYC suppression induced by BET bromodomain inhibitors alongside the immune activation provided by PD-1/PD-L1 checkpoint blockade agents, creating synergistic anti-tumor immune responses

- This trend towards more mechanistically precise, biomarker-guided, and combination-optimized epigenetic reader protein inhibitor therapies is fundamentally reshaping oncologist expectations for epigenome-targeted cancer treatment. Consequently, companies such as Zenith Epigenetics are developing next-generation BET bromodomain inhibitor candidates with enhanced selectivity profiles and improved tolerability for advanced hematological malignancy and solid tumor indications

- The demand for epigenetic reader protein inhibitors that offer seamless integration with biomarker-driven patient selection and combination immunotherapy platforms is growing rapidly across both academic and commercial oncology sectors, as pharmaceutical developers increasingly prioritize mechanistic precision and comprehensive transcriptional anti-tumor activity

Epigenetic Reader Protein Inhibitor Market Dynamics

Driver

“Growing Need Due to Rising Cancer and Autoimmune Disease Incidence and Expanding Precision Epigenomics Adoption”

- The increasing global burden of hematological malignancies, solid tumors, and autoimmune disorders driven by aberrant epigenetic reader protein activity, and the accelerating adoption of epigenome-targeted precision medicine strategies, are significant drivers for the heightened demand for epigenetic reader protein inhibitors

- For instance, in April 2025, Constellation Pharmaceuticals announced positive Phase 3 clinical trial results for pelabresib in combination with ruxolitinib in myelofibrosis patients, demonstrating statistically significant improvements in spleen volume reduction and symptom score outcomes compared to ruxolitinib monotherapy. Such strategies by key companies are expected to drive the epigenetic reader protein inhibitor industry growth in the forecast period

- As oncologists and clinical researchers increasingly recognize aberrant BET bromodomain and chromatin reader protein activity as a critical driver of MYC-dependent oncogenic transcriptional programs and immune evasion in hematological malignancies and solid tumors, epigenetic reader protein inhibitors offer a compelling mechanistic strategy to disrupt disease-driving super-enhancer-mediated transcriptional programs, providing a significant clinical advantage over conventional chemotherapy agents with non-selective cytotoxic mechanisms

- Furthermore, the growing deployment of combination epigenetic therapy regimens incorporating BET bromodomain inhibitors alongside JAK inhibitors, BCL-2 inhibitors, and immune checkpoint inhibitor agents and the desire for novel epigenome-targeting strategies that reprogram tumor immunosuppressive microenvironments are making epigenetic reader protein inhibitors an integral component of next-generation hematological and solid tumor treatment protocols

- The clinical utility of epigenetic reader protein inhibitors in addressing transcriptionally addicted hematological malignancies, their ability to selectively suppress BRD4-dependent MYC and BCL-2 oncogenic transcriptional programs, and their potential to synergize with immune checkpoint blockade through epigenetic derepression of antigen presentation and interferon response pathways are key factors propelling their adoption in both academic medical centers and commercial oncology treatment settings. The trend towards precision epigenomics and the increasing availability of chromatin accessibility and histone modification diagnostic tools further contribute to market growth

Restraint/Challenge

“Concerns Regarding Dose-Limiting Toxicities and High Clinical Development Complexity”

- Concerns surrounding the dose-limiting thrombocytopenia, gastrointestinal toxicity, and reversible elevations in serum creatinine and lipid levels associated with BET bromodomain inhibitor clinical development, as well as the challenges of demonstrating durable single-agent anti-tumor efficacy in molecularly heterogeneous patient populations, pose a significant challenge to broader market penetration

- For instance, early-generation BET bromodomain inhibitor clinical programs including JQ1-derived candidates experienced significant dose-limiting toxicity challenges driven by on-target suppression of normal hematopoiesis, leading to clinical development delays and requiring extensive dose optimization and scheduling modification work to identify tolerable combination regimen strategies

- Addressing these clinical development and tolerability challenges through improved bromodomain selectivity engineering in next-generation BRD4-selective inhibitor design, refined combination regimen strategies leveraging mechanistic synergies between BET inhibitors and BCL-2 or JAK inhibitors at reduced individual agent doses, and more rigorous biomarker-enriched patient stratification are crucial for building clinical confidence

- Companies such as Constellation Pharmaceuticals and Incyte Corporation emphasize their advanced biomarker-guided clinical development strategies and improved next-generation BET inhibitor selectivity profiles in their R&D programs to demonstrate enhanced tolerability and proof of concept in precisely selected patient populations. In addition, the significant cost and timeline requirements associated with epigenetic reader inhibitor clinical development, including the need for chromatin profiling companion diagnostic co-development and complex epigenomic biomarker endpoint validation, can be a barrier to development for smaller biotechnology companies with limited capital resources. While innovative financing models such as academic-industry partnerships and orphan drug designations for rare hematological malignancy indications have enabled some smaller developers to advance their programs, the capital intensity of late-stage oncology clinical development remains a significant market access barrier

- While clinical development strategies and next-generation reader domain inhibitor designs are gradually maturing, the perceived tolerability risks and development complexity of epigenetic reader protein inhibitor programs can still hinder broader investment and commercial commitment, especially for those who do not see immediate near-term regulatory approval catalysts to de-risk the program

- Overcoming these challenges through enhanced selectivity engineering, optimized combination clinical development strategies, and the development of more efficient biomarker-driven epigenetic reader protein inhibitor clinical frameworks will be vital for sustained market growth

Epigenetic Reader Protein Inhibitor Market Scope

The market is segmented on the basis of drug type, indication, treatment type, route of administration, and end-users.

• By Drug Type

On the basis of drug type, the epigenetic reader protein inhibitor market is segmented into BET bromodomain inhibitors, PHD finger inhibitors, chromodomain inhibitors, PWWP domain inhibitors, and others. The BET bromodomain inhibitors segment dominated the largest market revenue share of 43.2% in 2025, driven by the most advanced clinical development track record of any epigenetic reader protein inhibitor class and the well-validated BRD2/BRD3/BRD4 transcriptional co-activator dependency across multiple high-priority hematological malignancy and solid tumor indications. Pharmaceutical developers rely on BET bromodomain inhibitor platforms for their extensive preclinical and clinical pharmacology database, strong mechanistic rationale for MYC oncogene transcriptional suppression, and demonstrated anti-tumor activity in NMC, AML, myelofibrosis, and triple-negative breast cancer preclinical and early clinical settings. The market also sees sustained demand for BET bromodomain inhibitor candidates due to their well-characterized structure-activity relationships, broad therapeutic applicability across multiple oncology and inflammatory indications, and established clinical development infrastructure at leading academic cancer centers globally. Growing investment in next-generation BRD4-selective BET inhibitor design incorporating improved tolerability profiles and enhanced potency is reinforcing the dominant clinical development position of this epigenetic reader inhibitor class. Rising numbers of clinical trials evaluating BET inhibitors in combination with standard-of-care oncology agents are further supporting the strong demand for this segment.

The PWWP domain inhibitors segment is anticipated to witness the fastest growth rate of 23.6% from 2026 to 2033, fueled by growing interest in PWWP reader domain biology as a novel epigenetic vulnerability in hematological malignancies and NSD methyltransferase-dependent cancers, and the emerging clinical validation of PWWP domain inhibition as a strategy to disrupt oncogenic NSD1/NSD2 histone methyltransferase complex recruitment and downstream H3K36 methylation-dependent transcriptional programs. PWWP domain inhibitors offer a mechanistically distinct epigenetic reader protein targeting strategy complementary to the well-established BET bromodomain inhibitor class, providing an attractive pipeline diversification opportunity for pharmaceutical developers seeking to expand their precision epigenomics oncology portfolio. The growing body of preclinical evidence demonstrating potent anti-tumor activity of PWWP domain inhibitors in NSD2-translocated multiple myeloma and NSD1-amplified solid tumor models is driving rapidly expanding pharmaceutical developer interest in PWWP domain inhibitor discovery and early clinical development. Rising funding from both public research sources including NCI SBIR/STTR programs and private venture capital investment in epigenomics-focused biotechnology companies is accelerating PWWP domain inhibitor candidate discovery and IND-enabling development. Regulatory incentives including breakthrough therapy designation and orphan drug status for rare hematological malignancy indications are supporting accelerated PWWP domain inhibitor clinical development timelines.

• By Indication

On the basis of indication, the epigenetic reader protein inhibitor market is segmented into hematological malignancies, solid tumors, autoimmune disorders, inflammatory diseases, and others. The hematological malignancies segment held the largest market revenue share of 41.8% in 2025, driven by the high prevalence of BET bromodomain and other chromatin reader protein dependencies across AML, myelofibrosis, multiple myeloma, diffuse large B-cell lymphoma, and NMC patient populations, and the strong mechanistic rationale for epigenetic reader protein inhibitor therapy in transcriptionally addicted hematological cancer subtypes. The broad clinical applicability of BET and other epigenetic reader protein inhibitors across multiple hematological malignancy histologies, combined with the compelling biological rationale for epigenetic combination therapy strategies leveraging MYC and BCL-2 transcriptional co-suppression, provides a large addressable hematological malignancy patient population and strong commercial rationale for clinical development. Rising global incidence of hematological malignancies including AML and myelofibrosis, combined with significant unmet clinical need in patient populations who fail or are ineligible for current standard-of-care therapies, is reinforcing sustained demand for epigenetic reader protein inhibitor development in the hematological malignancy indication space. Expanding clinical trial infrastructure at leading academic cancer centers and cooperative oncology groups dedicated to hematological malignancy epigenetic therapeutic strategies is further supporting strong segment clinical development activity.

The autoimmune disorders segment is expected to witness the fastest CAGR of 22.4% from 2026 to 2033, driven by the growing body of preclinical and translational evidence demonstrating the critical role of BET bromodomain proteins in driving inflammatory cytokine transcriptional programs underlying autoimmune disease pathogenesis, and the compelling clinical rationale for BET bromodomain inhibitor therapy in NF-kB and AP-1 transcription factor-dependent autoimmune and inflammatory disease indications including rheumatoid arthritis, systemic lupus erythematosus, and inflammatory bowel disease. Rising global prevalence of autoimmune disorders combined with significant unmet clinical need in patient populations with refractory disease unresponsive to currently approved biologic therapies is creating strong demand for mechanistically differentiated epigenetic reader protein inhibitor treatment options. The growing body of preclinical evidence supporting potent anti-inflammatory activity of BET bromodomain inhibitors through selective suppression of NF-kB-dependent pro-inflammatory cytokine transcriptional programs including IL-6, TNF-alpha, and IL-17 is driving rapidly expanding clinical interest in autoimmune disorder-focused BET inhibitor development programs. Strategic industry-academic partnerships and increased NIH and pharmaceutical company R&D investment in epigenetic mechanisms of autoimmune disease are further accelerating the clinical advancement of epigenetic reader protein inhibitor programs in autoimmune indications.

• By Treatment Type

On the basis of treatment type, the epigenetic reader protein inhibitor market is segmented into monotherapy, combination therapy, and others. The combination therapy segment accounted for the largest market revenue share of 58.9% in 2025, driven by the strong clinical rationale for combining epigenetic reader protein inhibitors with JAK inhibitors, BCL-2 inhibitors, immune checkpoint inhibitors, and standard-of-care chemotherapy agents to achieve synergistic anti-tumor activity through mechanistically complementary transcriptional reprogramming and cytotoxic mechanisms. The well-established role of combination therapy as the dominant treatment paradigm in both hematological malignancy and solid tumor oncology, combined with the compelling biological rationale for BET bromodomain inhibitor combinations leveraging MYC and BCL-2 co-suppression to overcome anti-apoptotic resistance mechanisms and potentiate immune checkpoint inhibitor activity, is reinforcing the dominant market position of combination therapy regimens. Growing numbers of Phase 1b/2 and Phase 2/3 combination clinical trials evaluating BET inhibitors alongside ruxolitinib in myelofibrosis and azacitidine in AML are further supporting strong combination therapy segment growth. Rising clinical recognition of epigenetic resistance mechanisms as a primary driver of targeted therapy resistance in hematological malignancies is accelerating the development of BET inhibitor combination strategies designed to normalize aberrant chromatin states and restore treatment sensitivity.

The monotherapy segment is expected to witness the fastest CAGR of 21.8% from 2026 to 2033, driven by growing interest in next-generation highly selective BRD4 inhibitors and PWWP/chromodomain inhibitors with improved single-agent anti-tumor activity profiles and tolerability characteristics enabling clinically meaningful monotherapy responses in molecularly selected patient populations with high epigenetic reader protein dependency. Increasing investment in next-generation epigenetic reader inhibitor design incorporating enhanced selectivity for disease-driving reader domain subtypes and improved pharmacokinetic profiles is enhancing the monotherapy anti-tumor activity potential of novel reader protein inhibitor candidates. The strong clinical unmet need in rare epigenetically driven malignancies such as NMC harboring BRD4-NUT fusion oncoproteins, NSD2-translocated multiple myeloma, and other biomarker-defined hematological malignancies with high epigenetic reader protein dependency, combined with regulatory incentives including breakthrough therapy and orphan drug designations, is supporting accelerated monotherapy clinical development pathways for next-generation epigenetic reader protein inhibitor candidates. Rising academic and biotech investment in highly potent and selective reader domain inhibitors with single-agent anti-tumor activity in biomarker-enriched patient populations is further supporting the long-term growth trajectory of the monotherapy segment.

• By Route of Administration

On the basis of route of administration, the epigenetic reader protein inhibitor market is segmented into oral, intravenous, and others. The oral segment held the largest market revenue share of 64.7% in 2025, driven by the predominant formulation of leading clinical-stage BET bromodomain inhibitor candidates including pelabresib and INCB057643 as oral small molecule tablets enabling convenient outpatient administration compatible with the chronic dosing schedules required for epigenetic reader protein inhibitor therapy. The strong commercial precedent established by the success of oral targeted oncology therapies including ibrutinib, venetoclax, and ruxolitinib in hematological malignancy treatment has reinforced the strategic preference of pharmaceutical developers for oral formulation strategies in epigenetic reader protein inhibitor drug development programs. The established patient preference for oral oncology therapies enabling home-based treatment and reducing the burden of hospital-based infusion visits is further supporting the dominant market position of oral formulations in the epigenetic reader protein inhibitor segment. Growing clinical experience with oral BET inhibitor dosing schedules including intermittent dosing strategies designed to balance anti-tumor efficacy with tolerability management is reinforcing the clinical feasibility of oral epigenetic reader protein inhibitor therapy.

The intravenous segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, driven by growing development of intravenous epigenetic reader protein inhibitor formulations designed to achieve higher peak plasma drug concentrations and more complete target occupancy profiles in aggressive hematological malignancies and rapidly progressing solid tumor indications requiring intensive induction therapy. The development of intravenous BET inhibitor and next-generation chromodomain inhibitor formulations incorporating advanced drug delivery technologies including nanoparticle and liposomal encapsulation is enabling improved tumor tissue drug exposure and reduced systemic toxicity profiles through more targeted drug delivery. Rising clinical interest in combining intravenous epigenetic reader protein inhibitor infusions with standard intravenous chemotherapy induction regimens in AML and aggressive lymphoma treatment protocols is creating new clinical development opportunities for intravenous epigenetic reader protein inhibitor formulations. The strong clinical precedent for intravenous drug delivery in intensive hematological malignancy induction and consolidation treatment settings is further supporting the development of intravenous epigenetic reader protein inhibitor formulation strategies for high-priority hematological oncology indications.

• By End-Users

On the basis of end-users, the epigenetic reader protein inhibitor market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment accounted for the largest market revenue share of 61.4% in 2025, driven by the predominance of hematological malignancy treatment in hospital-based oncology departments and the concentration of epigenetic reader protein inhibitor clinical trial activity at major academic medical centers and National Cancer Institute-designated comprehensive cancer centers globally. The well-established infrastructure of hospital hematology and oncology departments for managing complex multi-agent combination chemotherapy and targeted therapy regimens, patient monitoring during treatment initiation, and management of hematological toxicities associated with BET inhibitor therapy is reinforcing the dominant market position of the hospital end-user segment. Growing concentration of hematological malignancy and solid tumor clinical trial enrollment at comprehensive cancer centers is further supporting hospital segment leadership in epigenetic reader protein inhibitor utilization and clinical development.

The specialty clinics segment is expected to witness the fastest CAGR of 22.8% from 2026 to 2033, driven by the expanding role of dedicated outpatient hematology and oncology specialty clinics as primary sites of care for patients receiving chronic oral epigenetic reader protein inhibitor therapy and maintenance treatment with combination BET inhibitor regimens. The growing trend towards outpatient oncology treatment delivery models, supported by the predominantly oral formulation strategy of leading BET bromodomain inhibitor clinical programs and improved ambulatory patient monitoring capabilities, is accelerating the transition of epigenetic reader protein inhibitor treatment delivery toward the specialty clinic setting. Rising patient preference for the more convenient and personalized care experience offered by dedicated specialty hematology and oncology clinics compared to large hospital-based oncology departments is further supporting specialty clinic segment growth. Expanding specialty clinic infrastructure at private oncology practice networks and regional cancer center outpatient facilities globally is creating additional treatment capacity for oral epigenetic reader protein inhibitor therapy delivery.

Epigenetic Reader Protein Inhibitor Market Regional Analysis

- North America dominated the epigenetic reader protein inhibitor market with the largest revenue share of 39% in 2025, driven by a growing demand for precision epigenomics therapies targeting aberrant chromatin reader protein activity in hematological malignancies and solid tumors, as well as increased investment in epigenetic reader protein inhibitor clinical research and drug discovery activity

- Pharmaceutical and biotechnology companies in the region highly value the mechanistic innovation, transcriptional selectivity potential, and combination therapy synergy offered by epigenetic reader protein inhibitors across multiple high-unmet-need oncology and autoimmune disease indications including AML, myelofibrosis, multiple myeloma, and rheumatoid arthritis

- This widespread clinical and commercial adoption is further supported by high oncology and precision medicine R&D investment, a technologically advanced clinical trial and epigenomics research infrastructure, and the growing preference for biomarker-guided precision epigenomics treatment strategies, establishing epigenetic reader protein inhibitors as a compelling next-generation targeted therapy platform for both academic and commercial oncology and immunology drug development

U.S. Epigenetic Reader Protein Inhibitor Market Insight

The U.S. epigenetic reader protein inhibitor market captured the largest revenue share in 2025 within North America, fueled by the swift expansion of the precision epigenomics drug development ecosystem and the growing clinical investment in chromatin reader protein-targeted therapeutic strategies at leading U.S. comprehensive cancer centers and academic medical institutions. Oncologists and clinical researchers are increasingly prioritizing the development of epigenetic reader protein inhibitor combination regimens designed to overcome resistance mechanisms in hematological malignancies and transcriptionally addicted solid tumors. The growing preference for biomarker-driven oncology clinical trial designs, combined with robust funding from both NCI-sponsored academic research programs and private biotechnology investment in epigenomics-focused drug discovery, further propels the epigenetic reader protein inhibitor industry. Moreover, the increasing integration of epigenetic reader protein inhibitors into innovative combination epigenetic therapy and immunotherapy clinical protocols is significantly contributing to the market's expansion.

Europe Epigenetic Reader Protein Inhibitor Market Insight

The Europe epigenetic reader protein inhibitor market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent oncology drug regulatory pathways supporting expedited clinical development of innovative epigenome-targeted cancer therapies and the escalating demand for chromatin reader protein-targeted treatments across European academic cancer centers and pharmaceutical companies. The growing investment in translational epigenomics research, coupled with the expanding clinical trial network supported by European cooperative oncology groups and EHA-affiliated hematology research consortia, is fostering the clinical advancement of epigenetic reader protein inhibitor development programs. European oncology and hematology researchers are also drawn to the mechanistic innovation and transcriptional selectivity advantages these therapies offer. The region is experiencing significant growth in clinical trial enrollment for BET bromodomain and emerging chromodomain inhibitor candidates across hematological malignancy and autoimmune disease indications.

U.K. Epigenetic Reader Protein Inhibitor Market Insight

The U.K. epigenetic reader protein inhibitor market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the escalating investment in precision epigenomics research programs at leading U.K. academic cancer centers including The Institute of Cancer Research, The Wellcome Sanger Institute, and Cancer Research UK-affiliated institutions. In addition, the growing clinical recognition of aberrant BET bromodomain and chromatin reader protein activity as a critical driver of hematological malignancy oncogenesis and treatment resistance is encouraging both academic oncology researchers and commercial pharmaceutical developers to accelerate clinical investigation of epigenetic reader protein inhibitor candidates. The U.K.'s strong translational epigenomics research infrastructure, alongside its well-developed regulatory framework for early-phase oncology clinical trials through the MHRA, is expected to continue to stimulate market growth.

Germany Epigenetic Reader Protein Inhibitor Market Insight

The Germany epigenetic reader protein inhibitor market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing investment in innovative oncology drug development, strong academic-industry collaboration in epigenomics and chromatin biology research, and growing demand for mechanistically differentiated epigenome-targeted cancer therapies for treatment-resistant hematological malignancy and solid tumor indications. Germany's well-developed pharmaceutical manufacturing and clinical research infrastructure, combined with its emphasis on precision medicine and molecular oncology innovation, promotes the development and clinical evaluation of epigenetic reader protein inhibitor candidates. The integration of epigenetic reader protein inhibitors with immune checkpoint inhibitor and targeted kinase inhibitor combination strategies is also becoming increasingly prevalent in German academic oncology clinical trial programs.

Asia-Pacific Epigenetic Reader Protein Inhibitor Market Insight

The Asia-Pacific epigenetic reader protein inhibitor market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapidly increasing hematological malignancy and solid tumor incidence rates, rising investment in oncology and epigenomics clinical trial infrastructure, and technological advancements in precision epigenomics drug development in countries such as China, Japan, and South Korea. The region's growing orientation towards innovative epigenome-targeted cancer therapies, supported by government initiatives promoting domestic oncology pharmaceutical development and epigenomics research capacity, is driving the adoption of epigenetic reader protein inhibitor research and clinical programs. In addition, as Asia-Pacific emerges as a major hub for oncology clinical trial enrollment, the accessibility of large hematological malignancy and solid tumor patient populations for epigenetic reader protein inhibitor clinical studies is expanding the clinical development capacity for these therapies across the region.

Japan Epigenetic Reader Protein Inhibitor Market Insight

The Japan epigenetic reader protein inhibitor market is gaining momentum due to the country's advanced oncology pharmaceutical development culture, rapid expansion of precision medicine and epigenomics clinical research infrastructure, and strong demand for innovative cancer therapies addressing treatment-resistant hematological malignancy and solid tumor indications. The Japanese market places a significant emphasis on therapeutic innovation and clinical rigor, and the adoption of epigenetic reader protein inhibitor development programs is driven by the increasing sophistication of domestic oncology biotechnology and pharmaceutical R&D capabilities. The integration of epigenetic reader protein inhibitors with other epigenome-targeted approaches including HDAC inhibitors and EZH2 inhibitors is fueling growth in Japanese epigenetic combination therapy clinical trial activity. In addition, Japan's aging population with rising cancer incidence is likely to spur demand for innovative hematological malignancy and solid tumor treatment options including epigenetic reader protein inhibitor-based therapies.

China Epigenetic Reader Protein Inhibitor Market Insight

The China epigenetic reader protein inhibitor market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's rapidly expanding oncology pharmaceutical development ecosystem, high cancer and hematological malignancy incidence burden, and high rates of investment in precision epigenomics clinical research and innovative targeted cancer therapy development. China stands as one of the largest markets for oncology drug development, and epigenetic reader protein inhibitors are attracting increasing research and development interest from both domestic Chinese biotechnology companies and global pharmaceutical companies establishing China-based clinical development programs. The push towards precision epigenomics and the availability of large hematological malignancy patient populations for clinical trial enrollment, alongside strong government support for domestic pharmaceutical innovation, are key factors propelling the market in China.

Epigenetic Reader Protein Inhibitor Market Share

The Epigenetic Reader Protein Inhibitor industry is primarily led by well-established companies, including:

- Roche Holding AG (Switzerland)

- AstraZeneca plc (U.K.)

- GlaxoSmithKline plc (U.K.)

- Pfizer Inc. (U.S.)

- Constellation Pharmaceuticals, Inc. (U.S.)

- Incyte Corporation (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Syros Pharmaceuticals, Inc. (U.S.)

- Zenith Epigenetics Ltd. (Canada)

- Forma Therapeutics Holdings, Inc. (U.S.)

- Kymera Therapeutics, Inc. (U.S.)

- Relay Therapeutics, Inc. (U.S.)

- C4 Therapeutics, Inc. (U.S.)

- Accent Therapeutics, Inc. (U.S.)

- Prelude Therapeutics, Inc. (U.S.)

- EpiStem Ltd. (U.K.)

Latest Developments in Global Epigenetic Reader Protein Inhibitor Market

- In April 2023, Constellation Pharmaceuticals, Inc., a clinical-stage biopharmaceutical company focused on epigenetic therapies, announced positive Phase 3 MANIFEST-2 clinical trial results demonstrating statistically significant superiority of pelabresib in combination with ruxolitinib over ruxolitinib plus placebo in JAK inhibitor-naive myelofibrosis patients, underscoring the company's dedication to advancing next-generation BET bromodomain inhibitor combination therapies for the treatment of myeloproliferative neoplasms with high unmet clinical need. By leveraging its proprietary BET bromodomain inhibitor chemistry and combination clinical development strategy, Constellation Pharmaceuticals is reinforcing its position as a leader in the rapidly growing global epigenetic reader protein inhibitor market

- In March 2023, Incyte Corporation presented updated Phase 1b clinical data from its INCB057643 BET bromodomain inhibitor program in combination with ruxolitinib in myelofibrosis and in combination with azacitidine in acute myeloid leukemia, demonstrating encouraging preliminary anti-tumor activity and manageable tolerability profiles that support continued clinical development. The updated data highlighted Incyte's ongoing commitment to biomarker-guided patient selection strategies and optimized combination dosing regimen development for its BET bromodomain inhibitor platform

- In March 2023, Zenith Epigenetics Ltd. completed a strategic clinical development milestone for its ZEN-3694 BET bromodomain inhibitor candidate in combination with enzalutamide in metastatic castration-resistant prostate cancer, demonstrating preliminary evidence of anti-tumor activity in patients with BET-dependent epigenetic resistance to AR pathway inhibition, underscoring the company's commitment to advancing epigenetic reader protein inhibitors in solid tumor oncology indications beyond hematological malignancies

- In February 2023, Kymera Therapeutics announced a strategic research collaboration with a leading academic epigenomics research institution to co-develop targeted protein degrader strategies incorporating PROTAC technology for selective degradation of BRD4 and other disease-driving BET bromodomain proteins, specifically designed to address tumor cell resistance mechanisms arising from BET inhibitor-mediated target protein upregulation in hematological malignancy and solid tumor indications

- In January 2023, Prelude Therapeutics, Inc. unveiled an expanded epigenetic reader protein inhibitor discovery program targeting novel PWWP domain inhibitors for NSD2-dependent multiple myeloma and NSD1-amplified solid tumor indications, leveraging advanced structure-based drug design and cryo-EM structural characterization to develop first-in-class PWWP domain reader inhibitor candidates with compelling selectivity profiles for disease-driving NSD methyltransferase complex recruitment inhibition

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.