Global Epinephrine Auto Injector Market

Market Size in USD Billion

USD

2.58 Billion

USD

4.88 Billion

2025

2033

USD

2.58 Billion

USD

4.88 Billion

2025

2033

Forecast Period |

2026 - 2033 |

Market Size (Base Year) |

USD 2.58 Billion |

Market Size (Forecast Year) |

USD 4.88 Billion |

CAGR |

% |

Major Markets Players |

|

Epinephrine Auto-Injector Market Overview

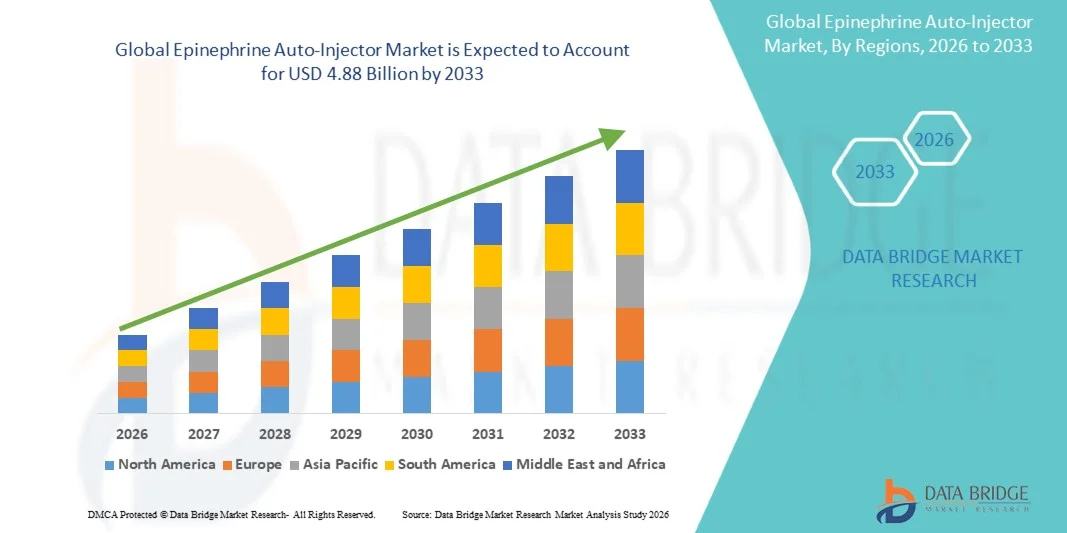

The Epinephrine Auto-Injector Market was valued at USD 2.58 billion in 2025 and is projected to reach USD 4.88 billion by 2033, growing at a CAGR of 8.30% from 2026 to 2033. The market is experiencing consistent growth supported by growing demand for easy-to-use, portable, and reliable drug delivery devices, along with expanding adoption across hospitals, retail pharmacies, and homecare settings.

The increasing incidence of food allergies, medication-induced hypersensitivity, and insect sting reactions is significantly boosting the need for epinephrine auto-injectors globally. In addition, supportive regulatory frameworks mandating the availability of emergency anaphylaxis treatment in schools, workplaces, and public institutions are strengthening market penetration. Continuous advancements in device design such as improved safety features, intuitive activation mechanisms, and enhanced shelf-life stability alongside rising patient education and emergency preparedness initiatives, are further accelerating market growth.

Key Market Trends & Insights

- North America dominated the Epinephrine Auto-Injector Market with the largest revenue share of 38.92% in 2025, supported by high awareness of anaphylaxis management, strong healthcare infrastructure, and widespread availability of branded and generic auto-injectors.

- The Single-dose auto-injectors segment led the market with a 46.15% share in 2025, driven by their simplicity, rapid administration capability, and strong preference among patients and caregivers during emergency anaphylaxis situations.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by rising allergy prevalence, improving healthcare access, increasing diagnostic rates, and growing awareness programs in countries such as China, India, and Japan.

- Twin-pack auto-injectors are the fastest-growing product type, projected to register a CAGR of 8.8%, reflecting the surge in clinical recommendations for carrying a backup dose in case of severe or biphasic allergic reactions.

- The 0.30 mg segment dominated the vehicle type category with a 58.72% revenue share in 2025, led by its wide used as the standard adult dose for managing moderate to severe anaphylaxis cases.

- over 12 years accounted for 49.35% of the market, preferred by the higher exposure to allergens in adolescents and adults and greater self-administration capability.

- The 6 to 12 years segment is the fastest-growing application category, with a CAGR of 8.9%, driven by rising food allergy detection in early childhood and growing school-based emergency preparedness initiatives.

Market Size & Forecast

- Global Market Value (2025): USD 2.58 Billion

- Expected Market Value (2033): USD 4.88 Billion

- Forecast CAGR (2026–2033): 8.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Epinephrine Auto-Injector Market Segmentation

|

Attributes |

Epinephrine Auto-Injector Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Viatris Inc. (U.S.) · Pfizer Inc. (U.S.) · Teva Pharmaceutical Industries Ltd. (Israel) · Amphastar Pharmaceuticals, Inc. (U.S.) · Sandoz Group AG (Switzerland) · Hikma Pharmaceuticals PLC (U.K.) · Sun Pharmaceutical Industries Ltd. (India) · kaléo Inc. (U.S.) · ALK-Abelló A/S (Denmark) · Aurobindo Pharma Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Cipla Limited (India) · Perrigo Company plc (Ireland) · Apotex Inc. (Canada) · Lupin Limited (India) · Fresenius Kabi AG (Germany) · B. Braun SE (Germany) · ARS Pharmaceuticals, Inc. (U.S.) · Novartis AG (Switzerland) · Meda AB (Sweden) |

|

Market Opportunities |

· Integration of smart auto-injectors with digital health platforms · Rising adoption of generic and biosimilar epinephrine products · Expanding school and workplace emergency preparedness mandates |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Epinephrine Auto-Injector Market Trends

Trend: Rising Adoption of Patient-Friendly Emergency Self-Administration Devices

Patients and caregivers are increasingly preferring easy-to-use epinephrine auto-injectors that enable rapid self-administration during anaphylactic emergencies without clinical assistance. Manufacturers are focusing on ergonomic designs, hidden needle mechanisms, and simplified activation systems to reduce usage errors and improve compliance. Growing awareness campaigns and allergy education programs are further driving widespread adoption across pediatric and adult populations, while digital instructions and training devices are improving real-world preparedness. For instance, the launch of user-centric devices such as Auvi-Q and EpiPen redesign updates highlights this shift toward improved usability and patient safety.

Epinephrine Auto-Injector Market Dynamics

Key Market Driver: Rising Prevalence of Severe Allergic Reactions and Anaphylaxis Cases

The increasing global incidence of food allergies, drug hypersensitivity, and insect sting-induced anaphylaxis is significantly driving demand for epinephrine auto-injectors across all age groups. Healthcare providers and regulatory bodies are emphasizing rapid-access emergency treatment, leading to higher prescription rates and mandatory availability in schools and public institutions. Expanding awareness among patients regarding early intervention is further supporting market growth, alongside improved diagnostic rates in developed and emerging healthcare systems. For instance, rising peanut allergy cases in children across North America and Europe has led to widespread school-based epinephrine stocking policies.

Key Restraint/Challenge: High Cost and Limited Affordability of Branded Devices in Emerging Markets

Despite strong demand, the market faces challenges due to the high cost of branded epinephrine auto-injectors, which limits accessibility in low- and middle-income regions. Repeated prescription requirements and short product shelf-life further increase the overall treatment burden for patients and healthcare systems. Limited reimbursement coverage in certain countries also restricts adoption, particularly where emergency allergy preparedness infrastructure is still developing. For instance, the high pricing of branded EpiPen devices has led to delayed adoption in several Asia-Pacific and Latin American markets.

Key Market Opportunity: Expansion of Digital Health Integration and Smart Allergy Management Solutions

The integration of digital health technologies with epinephrine auto-injectors presents a significant opportunity for market expansion through improved patient monitoring and emergency response systems. Smart devices with connectivity features, dose tracking, and mobile alerts can enhance adherence and ensure timely replacement before expiry. Growing investment in connected healthcare ecosystems and remote patient management platforms is further enabling innovation in allergy care. For instance, development of connected medical devices with mobile app-based allergy action plans and reminder systems is expanding personalized anaphylaxis management solutions globally.

Epinephrine Auto-Injector Market Scope

The epinephrine auto-injector market is segmented on the basis of product type, dosage strength, application, and end-user.

- By Product Type

On the basis of product type, the Epinephrine Auto-Injector Market is segmented into single-dose auto-injectors, twin-pack auto-injectors, and prefilled syringe devices. The Single-dose auto-injectors segment dominated the market with a 46.15% share in 2025, owing to their simplicity, rapid administration capability, and strong preference among patients and caregivers during emergency anaphylaxis situations. These devices are widely prescribed due to their portability, ease of use, and reduced risk of dosage error. Increasing awareness programs and school-based allergy management policies further strengthen their adoption. They are also supported by strong availability across retail pharmacies and hospital systems. Continuous design improvements such as voice guidance and hidden needle systems enhance patient confidence. The segment remains the standard first-line emergency treatment option globally.

The Twin-pack auto-injectors segment is expected to witness the fastest growth at a CAGR of 8.8% from 2026 to 2033, driven by increasing clinical recommendations for carrying a backup dose in case of severe or biphasic allergic reactions. Physicians are increasingly prescribing dual-pack devices to ensure safety during repeated anaphylaxis episodes. Insurance coverage expansion in developed markets is also improving accessibility. Rising awareness among high-risk patients is further boosting demand. The segment benefits from regulatory guidance recommending availability of two doses in emergency kits. Growing adoption in school and travel settings is further accelerating growth.

- By Dosage Strength

On the basis of dosage strength, the market is segmented into 0.30 mg and 0.15 mg formulations. The 0.30 mg dosage segment dominated the market with a 58.72% share in 2025, as it is widely used as the standard adult dose for managing moderate to severe anaphylaxis cases. This dosage is most commonly prescribed across hospitals, clinics, and retail pharmacies due to its effectiveness in adult emergency treatment. High prevalence of food and drug allergies among adults further supports demand. Strong physician preference and inclusion in treatment guidelines reinforce its dominance. It is also widely available across branded and generic formulations. Continuous prescription renewal cycles maintain consistent market demand.

The 0.15 mg dosage segment is expected to witness the fastest growth at a CAGR of 8.6% from 2026 to 2033, driven by rising incidence of food allergies in children and increasing pediatric allergy awareness. Schools and childcare institutions are increasingly stocking pediatric doses as part of emergency preparedness programs. Early diagnosis of allergies in infants and young children is further expanding usage. Regulatory emphasis on child-specific emergency care protocols is supporting adoption. Expanding pediatric healthcare access in emerging economies is also contributing to growth. Improved caregiver training initiatives are enhancing correct usage rates.

- By Application

On the basis of application, the market is segmented into under 6 years, 6 to 12 years, and over 12 years age groups. The over 12 years segment dominated the market with a 49.35% share in 2025, driven by higher exposure to allergens in adolescents and adults and greater self-administration capability. This group represents the largest share of diagnosed allergy patients requiring emergency epinephrine access. Strong prescription rates in schools, workplaces, and travel medicine settings support segment dominance. Increasing urbanization and dietary changes are contributing to rising allergy prevalence. Improved awareness among teenagers regarding self-management of anaphylaxis further strengthens demand. Widespread availability in pharmacies ensures easy access for this group.

The 6 to 12 years segment is expected to witness the fastest growth at a CAGR of 8.9% from 2026 to 2033, driven by rising food allergy detection in early childhood and growing school-based emergency preparedness initiatives. Schools are increasingly mandated to stock epinephrine auto-injectors for student safety. Parental awareness regarding early intervention is also improving adoption rates. Pediatric allergist recommendations for early prescription further support growth. Expansion of pediatric healthcare infrastructure in developing regions is contributing to increased diagnosis. Awareness campaigns targeting childhood allergies are further accelerating market penetration.

- By End-User

On the basis of end-user, the market is segmented into hospitals, clinics, and individuals. The individuals segment dominated the market with a 52.84% share in 2025, driven by increasing preference for at-home emergency preparedness and self-management of anaphylaxis risk. Patients with known severe allergies are increasingly prescribed personal auto-injectors for immediate response. Rising awareness campaigns and patient education programs are strengthening adoption. Easy availability through retail and online pharmacies supports direct consumer access. Strong repeat prescription cycles also contribute to sustained demand. The segment benefits from growing emphasis on personalized emergency care solutions.

The clinics segment is expected to witness the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by increasing outpatient allergy diagnosis and preventive care consultations. Clinics are playing a key role in early identification and prescription of epinephrine auto-injectors. Rising demand for allergy testing services is further supporting growth. Expansion of primary healthcare networks in emerging economies is improving access. Physicians in clinic settings are increasingly recommending emergency epinephrine kits for at-risk patients. Growing integration of allergy education programs in outpatient care is further accelerating adoption.

Epinephrine Auto-Injector Market Regional Analysis

North America dominated the Epinephrine Auto-Injector Market with the largest revenue share of 38.92% in 2025, supported by high awareness of anaphylaxis management, strong healthcare infrastructure, and widespread availability of branded and generic auto-injectors. The region also benefits from widespread availability of branded and generic auto-injectors, favorable reimbursement policies, and strong presence of leading pharmaceutical companies. Increasing adoption of emergency preparedness programs in schools, workplaces, and public spaces further strengthens market growth. Rising diagnosis rates of food and drug allergies along with high patient education levels continue to reinforce North America’s leadership position in the global market.

U.S. Epinephrine Auto-Injector Market Insight

The U.S. epinephrine auto-injector market is witnessing strong growth due to high prevalence of severe allergic reactions, strong awareness of anaphylaxis management, and well-established healthcare infrastructure. The country’s mature pharmaceutical ecosystem, along with widespread availability of branded and generic auto-injectors, is driving demand across hospitals, retail pharmacies, and homecare settings. In addition, strong insurance coverage, school-based allergy action plans, and emergency preparedness programs are accelerating adoption. Continuous product innovations and rising patient education initiatives further reinforce the U.S. as the largest contributor to the global market.

Europe Epinephrine Auto-Injector Market Insight

The Europe epinephrine auto-injector market remains a major contributor to global revenue, driven by strong regulatory frameworks, increasing allergy awareness, and expanding public access to emergency epinephrine. The widespread use of auto-injectors in schools, workplaces, and healthcare institutions is supporting market expansion across the region. Increasing investments in allergy diagnostics, coupled with standardized treatment guidelines and strong healthcare systems, continue to enhance adoption. Growing emphasis on patient safety and preventive care further strengthens Europe’s position in the global market.

U.K. Epinephrine Auto-Injector Market Insight

The U.K. epinephrine auto-injector market is experiencing steady growth, supported by rising allergy prevalence, strong NHS-backed awareness programs, and increasing prescriptions for emergency epinephrine devices. Growing demand for cost-effective, easy-to-use auto-injectors in both pediatric and adult populations is contributing to market growth. Furthermore, integration of digital healthcare systems and patient training initiatives is improving correct usage and adherence. Expanding availability across community pharmacies continues to position the U.K. as a key European market.

Germany Epinephrine Auto-Injector Market Insight

The Germany epinephrine auto-injector market is expanding steadily due to high healthcare standards, increasing allergy diagnosis rates, and strong focus on patient safety and emergency preparedness. Hospitals, clinics, and pharmacies are increasingly adopting auto-injectors as part of standard anaphylaxis management protocols. Continuous awareness campaigns and physician-driven prescriptions are further supporting demand. In addition, Germany’s strong pharmaceutical manufacturing base and structured healthcare reimbursement system enhance market accessibility.

Asia-Pacific Epinephrine Auto-Injector Market Insight

The Asia-Pacific epinephrine auto-injector market is expected to witness rapid growth, driven by rising allergy prevalence, improving healthcare access, and increasing awareness of anaphylaxis management across countries such as China, India, and Japan. Expanding healthcare infrastructure and growing adoption of emergency care standards are supporting regional market expansion. In addition, increasing availability of generic products and rising investments in public health awareness are accelerating adoption. The region is emerging as one of the fastest-growing markets globally due to improving diagnosis rates and affordability initiatives.

Japan Epinephrine Auto-Injector Market Insight

The Japan epinephrine auto-injector market is witnessing consistent growth due to strong healthcare infrastructure, increasing food allergy cases, and rising awareness of emergency self-administration. Pharmaceutical companies and healthcare providers are increasingly promoting early diagnosis and preventive treatment approaches. Integration of advanced healthcare technologies and strong regulatory support for patient safety are further driving adoption. In addition, growing emphasis on pediatric allergy management is supporting steady market expansion.

China Epinephrine Auto-Injector Market Insight

The China epinephrine auto-injector market is growing rapidly, driven by increasing urbanization, rising allergy awareness, and expanding access to modern healthcare services. Growing diagnosis of food and environmental allergies is significantly boosting demand for emergency epinephrine devices. Government efforts to improve healthcare infrastructure and emergency response systems are further supporting market growth. In addition, increasing availability of affordable generic auto-injectors and expanding pharmacy networks are positioning China as one of the fastest-growing markets globally.

Epinephrine Auto-Injector Market Share

The epinephrine auto-injector industry is primarily led by well-established companies, including:

- Viatris Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Amphastar Pharmaceuticals, Inc. (U.S.)

- Sandoz Group AG (Switzerland)

- Hikma Pharmaceuticals PLC (U.K.)

- Sun Pharmaceutical Industries Ltd. (India)

- kaléo Inc. (U.S.)

- ALK-Abelló A/S (Denmark)

- Aurobindo Pharma Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Perrigo Company plc (Ireland)

- Apotex Inc. (Canada)

- Lupin Limited (India)

- Fresenius Kabi AG (Germany)

- Braun SE (Germany)

- ARS Pharmaceuticals, Inc. (U.S.)

- Novartis AG (Switzerland)

- Meda AB (Sweden)

Latest Developments in Epinephrine Auto-Injector Market

- In September 2024, Amneal Pharmaceuticals challenged Colorado’s mandatory low-cost epinephrine auto-injector distribution program. The lawsuit filed by Amneal Pharmaceuticals against Colorado highlights growing regulatory pressure on manufacturers to supply epinephrine auto-injectors at reduced or no cost under public health initiatives. The case reflects ongoing debates between affordability mandates and pharmaceutical pricing sustainability in the allergy treatment market.

- In August 2024, U.S. FDA approved neffy (intranasal epinephrine), the first needle-free treatment option for anaphylaxis. The approval of neffy marked a major advancement in the epinephrine market by introducing the first non-injectable alternative to traditional auto-injectors for emergency allergic reactions. Clinical studies demonstrated that intranasal epinephrine provides comparable effectiveness to injectable formats, offering a critical option for patients who have needle anxiety or difficulty using standard devices

- In October 2023, FDA expansion of authorized generic EpiPen improved affordability and access in the United States. The introduction and wider availability of authorized generic versions of EpiPen increased competition in the epinephrine auto-injector market and helped reduce treatment costs for patients. This development enabled greater pharmacy-level substitution and improved access for uninsured and underinsured populations

- In March 2023, Viatris expanded production and distribution of EpiPen and its authorized generics to strengthen global supply. Viatris increased manufacturing capacity and expanded distribution networks to ensure stable availability of epinephrine auto-injectors across key healthcare markets. This initiative helped address supply constraints and ensured continuous access for patients requiring emergency anaphylaxis treatment

- In February 2021, kaléo expanded Auvi-Q access programs to improve affordability and patient reach. kaléo implemented enhanced affordability initiatives and direct-to-patient delivery models to reduce barriers to accessing epinephrine auto-injectors. The Auvi-Q device, featuring a voice-guided system, improved ease of use during emergency situations, especially for children and caregivers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.