Global Epistaxis Treatment Market

Market Size in USD Million

USD

253.60 Million

USD

383.33 Million

2024

2032

USD

253.60 Million

USD

383.33 Million

2024

2032

| 2025 - 2032 | |

| USD 253.60 Million | |

| USD 383.33 Million | |

| % | |

|

Epistaxis Treatment Market Size

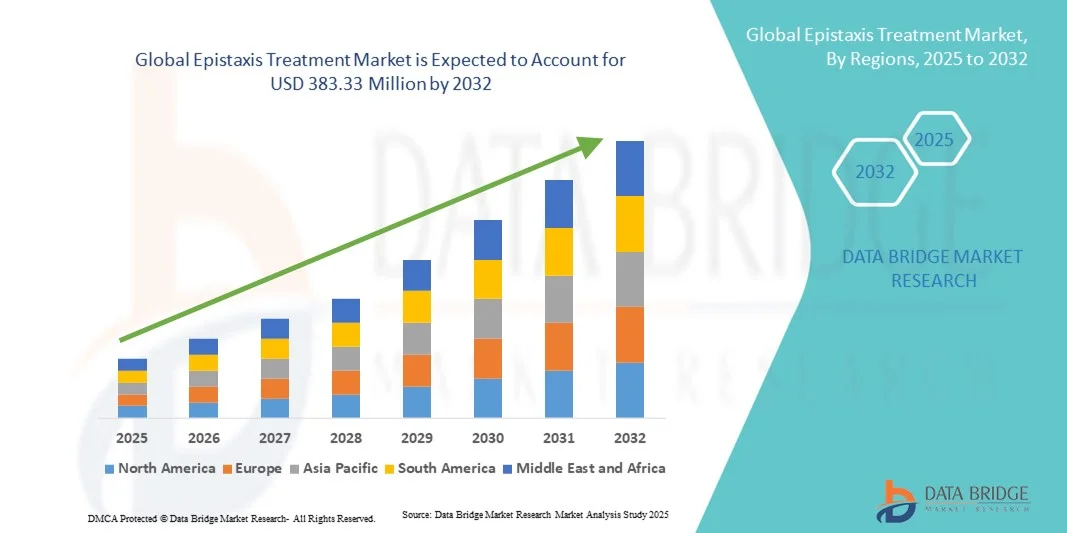

- The global epistaxis treatment market size was valued at USD 253.6 million in 2024 and is expected to reach USD 383.33 million by 2032, at a CAGR of 5.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of epistaxis (nosebleeds) due to factors such as rising respiratory disorders, hypertension, and trauma, along with growing awareness of effective treatment options among patients and healthcare providers

- Furthermore, advancements in minimally invasive procedures, hemostatic agents, and nasal care devices, coupled with rising adoption of specialized ENT clinics, are accelerating the uptake of epistaxis treatment solutions, thereby significantly boosting the industry's growth

Epistaxis Treatment Market Analysis

- Epistaxis, commonly known as nosebleeds, represents a significant ENT concern requiring effective management strategies, ranging from medication to minimally invasive procedures. The market for Epistaxis Treatment is expanding due to rising prevalence, increased awareness, and growing healthcare access across regions

- The increasing incidence of underlying conditions such as hypertension, blood disorders, and seasonal allergies, combined with greater patient awareness, is fueling the demand for advanced treatment options. Additionally, the adoption of minimally invasive procedures and advanced hemostatic agents is improving clinical outcomes

- North America dominated the epistaxis treatment market with the largest revenue share of 42.5% in 2024, driven by well-established healthcare infrastructure, high patient awareness, and the presence of leading pharmaceutical and medical device companies. The U.S. accounted for a major portion of this growth, fueled by increased hospitalizations for ENT procedures, widespread adoption of advanced hemostatic agents, and robust insurance coverage supporting treatment access

- Asia-Pacific is expected to be the fastest growing region in the epistaxis treatment market during the forecast period, attributed to improving healthcare infrastructure, rising disposable incomes, and expanding awareness about ENT disorders in countries such as China, India, and Japan. Rapid urbanization and government initiatives promoting ENT healthcare further support market expansion

- The Anterior segment dominated the epistaxis treatment market with the largest market revenue share of 62% in 2024, driven by its higher prevalence in clinical cases and the ease of treatment using topical and minimally invasive procedures

Report Scope and Epistaxis Treatment Market Segmentation

|

Attributes |

Epistaxis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Epistaxis Treatment Market Trends

Increasing Focus on Minimally Invasive and Patient-Friendly Treatments

- A significant and accelerating trend in the global epistaxis treatment market is the shift toward minimally invasive procedures, improved hemostatic agents, and patient-friendly interventions. This trend is driven by growing awareness of effective treatment options that reduce discomfort and recovery time

- For instance, the development of advanced nasal packing materials, topical hemostatic agents, and endoscopic cauterization tools allows clinicians to manage epistaxis more effectively and with less patient discomfort

- The adoption of innovative surgical techniques, such as endoscopic laser cauterization, is gaining traction in specialized ENT clinics and hospitals, offering precise treatment while minimizing bleeding and complications

- Research initiatives and clinical studies supporting the safety and efficacy of new treatments are shaping treatment protocols and driving adoption among healthcare providers

- Pharmaceutical and medical device companies are increasingly focusing on improving delivery mechanisms for hemostatic drugs and interventions, enhancing patient compliance and outcomes

- The trend toward patient-centered and evidence-based epistaxis treatment is expected to continue reshaping the market, with hospitals, specialty clinics, and ambulatory care centers seeking advanced solutions for improved care quality

Epistaxis Treatment Market Dynamics

Driver

Rising Prevalence of Epistaxis and Increasing Awareness of Treatment Options

- The increasing incidence of epistaxis among pediatric, adult, and geriatric populations, combined with rising awareness of effective management options, is a major driver for the market

- For instance, in March 2024, leading ENT clinics reported a notable increase in outpatient visits for nosebleed management, emphasizing the need for advanced hemostatic interventions

- Healthcare providers are adopting a combination of pharmacological and procedural interventions to manage recurrent or severe cases, driving demand for innovative treatment modalities

- The growing emphasis on early diagnosis, preventive care, and patient education contributes to higher adoption of epistaxis treatments in hospitals, clinics, and ambulatory centers

- Availability of comprehensive treatment protocols and training programs for healthcare professionals further supports the market expansion

- Technological advancements in hemostatic agents, minimally invasive devices, and nasal cauterization tools are enabling better clinical outcomes, thus fueling market growth

- Patient preference for effective, fast-acting, and low-risk interventions continues to drive the demand for newer epistaxis treatment solutions

Restraint/Challenge

Limited Access to Specialized Care and High Cost of Advanced Treatments

- Limited access to specialized ENT care in rural and underserved regions poses a challenge to broader market penetration. Patients may face difficulties in reaching hospitals or clinics equipped with advanced treatment modalities

- High costs associated with advanced hemostatic agents, endoscopic equipment, and procedural interventions can restrict adoption, particularly in developing regions or among cost-sensitive patients

- For instance, in some countries, the price of surgical intervention or premium nasal packing devices remains a barrier for wide usage, leading to reliance on traditional, less effective methods

- Inadequate insurance coverage or reimbursement policies for advanced epistaxis treatments can further slow adoption

- Continuous need for clinician training and proficiency in minimally invasive procedures adds to operational costs for healthcare providers

- Overcoming these challenges through government healthcare initiatives, improved insurance coverage, training programs, and development of cost-effective treatment solutions will be crucial for sustained market growth

Epistaxis Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the epistaxis treatment market is segmented into anterior and posterior. The Anterior segment dominated the largest market revenue share of 62% in 2024, driven by its higher prevalence in clinical cases and the ease of treatment using topical and minimally invasive procedures. Anterior bleeds are more common, accounting for a significant portion of patient visits, and healthcare providers often prioritize them for immediate intervention. Clinics and hospitals are well-equipped to handle these cases using established protocols, and the availability of cost-effective treatments contributes to higher adoption rates. Furthermore, the segment benefits from a strong awareness among general practitioners and ENT specialists, increasing early diagnosis and management. Preventive care initiatives, training programs, and patient education regarding nasal hygiene further support the segment’s dominance. The convenience of outpatient management for anterior bleeds enhances treatment accessibility, particularly in urban centers. The segment also sees robust adoption of topical vasoconstrictors, chemical cautery, and nasal packing, complementing the standard care practices. Patient preference for minimally invasive interventions and rapid recovery strengthens its market position. Overall, anterior epistaxis treatment represents the largest and most consistent revenue contributor across regions.

The Posterior segment is expected to witness the fastest CAGR of 8.5% from 2025 to 2032, driven by the increasing recognition of more severe cases requiring specialized intervention. Posterior bleeds, although less common, often require advanced techniques such as arterial ligation or balloon catheterization. Growing investment in hospital infrastructure, particularly in tertiary care centers, supports the adoption of posterior epistaxis management. Rising prevalence among older populations with comorbidities like hypertension and anticoagulant use contributes to segment growth. Advanced procedural training, awareness campaigns, and the development of innovative hemostatic devices are also fueling market expansion. Additionally, the segment benefits from increasing use of interventional radiology procedures and image-guided treatments. Growth is further supported by rising hospital admissions and referrals for complex epistaxis cases. High unmet medical need and technological advancements in treatment modalities make this segment highly attractive for healthcare providers and device manufacturers. Increasing insurance coverage and reimbursement for advanced procedures further contribute to the accelerating adoption rate. The combination of clinical necessity, procedural advancements, and supportive healthcare policies drives the segment’s superior CAGR.

- By Treatment

On the basis of treatment, the epistaxis treatment market is segmented into topical vasoconstrictors, chemical cautery, electrocautery, nasal tampon, foley catheter, and arterial ligation. The Topical Vasoconstrictors segment dominated with a market share of 55% in 2024, owing to its wide availability, ease of use, and cost-effectiveness for managing mild to moderate anterior bleeds. Healthcare practitioners often prefer topical solutions for their rapid onset, minimal discomfort, and ability to be administered in outpatient settings. This segment is further supported by strong awareness among general practitioners and ENT specialists, who regularly recommend topical vasoconstrictors as first-line therapy. Increasing OTC availability and patient self-care awareness also enhance its adoption. The segment benefits from consistent demand across hospitals, clinics, and homecare settings. Regulatory approvals and standardized guidelines for topical agents contribute to treatment consistency. Additionally, its compatibility with other treatment options, including nasal packing and cautery, reinforces its prevalence in practice. Rising patient preference for non-invasive approaches and growing clinical experience enhance segment dominance. Medical training programs emphasize topical vasoconstrictors as foundational treatment, further supporting its widespread use.

The Arterial Ligation segment is expected to register the fastest CAGR of 9.2% from 2025 to 2032, driven by increasing cases of severe posterior epistaxis requiring surgical intervention. Technological advancements in endoscopic and image-guided ligation procedures enhance procedural success and patient outcomes. Growing investments in hospital infrastructure and specialized ENT units facilitate adoption. Rising awareness among clinicians about early surgical intervention to prevent complications supports market growth. The segment is further bolstered by expanding training programs and increased procedural reimbursement. The need for effective management of recurrent or life-threatening bleeds fuels clinical adoption. Patient demand for minimally invasive and long-lasting solutions contributes to segment acceleration. Additionally, the segment benefits from collaboration between device manufacturers and healthcare providers to optimize procedural efficacy. Increasing prevalence of comorbid conditions such as hypertension and anticoagulant therapy drives clinical necessity. Overall, arterial ligation demonstrates robust growth due to high unmet needs, technological innovation, and favorable healthcare dynamics.On the basis of route of administration, the epistaxis treatment market is segmented into oral, parenteral, topical, and others. The Topical segment dominated the market with a sh

- By Route of Administration

are of 58% in 2024, attributed to its extensive use in managing anterior epistaxis. Topical administration provides direct and immediate action on the affected site, making it the preferred choice for mild to moderate bleeds. Clinicians appreciate the convenience, low risk, and minimal training required for administration. The segment also benefits from the development of user-friendly delivery devices and nasal sprays. Widespread OTC availability and patient preference for non-invasive treatments support consistent market dominance. Healthcare professionals often combine topical therapies with other interventions such as nasal packing or cautery for enhanced effectiveness. Rising patient awareness of self-care techniques, particularly for recurrent minor bleeds, further drives adoption. Regulatory approvals and clinical guidelines standardizing topical therapies reinforce market stability. The combination of accessibility, effectiveness, and patient compliance maintains its leading position.

The Parenteral segment is expected to witness the fastest CAGR of 8.8% from 2025 to 2032, driven by the increasing use of injectable hemostatic agents in severe or posterior epistaxis cases. Hospitals and specialty clinics are increasingly adopting parenteral therapies for controlled, targeted treatment. Rising hospital admissions for high-risk patients and complex cases support growth. Development of new injectable agents and delivery systems enhances treatment efficacy. Clinician preference for rapid and reliable results contributes to adoption. The segment also benefits from increasing reimbursement coverage for parenteral therapies. Technological advances in minimally invasive injection techniques improve patient outcomes and reduce complications. Awareness campaigns and clinical guidelines recommending parenteral interventions for severe bleeds further accelerate adoption. Overall, parenteral therapies are experiencing robust growth due to clinical necessity, innovation, and increased healthcare investments.

- By End-Users

On the basis of end-users, the epistaxis treatment market is segmented into clinics, hospitals, homecare, and others. The Hospitals segment dominated with a market share of 60% in 2024, owing to the high volume of epistaxis cases managed in inpatient and outpatient settings. Hospitals provide access to comprehensive treatment options, including surgical interventions, advanced hemostatic devices, and multidisciplinary care. The segment benefits from infrastructure availability, trained specialists, and advanced diagnostic tools. Increasing hospital admissions for severe bleeds and high patient trust in hospital care support dominance. Hospitals also benefit from insurance reimbursements and standardized protocols for epistaxis management. Collaborative research and training programs further strengthen the hospital segment. High patient volume, superior treatment capabilities, and emergency readiness make hospitals the preferred choice for severe and recurrent epistaxis.

The Homecare segment is expected to register the fastest CAGR of 9% from 2025 to 2032, driven by growing adoption of self-administered topical therapies and non-invasive treatments. Increased patient awareness and convenience of home-based management support growth. Development of user-friendly nasal sprays and monitoring devices enables effective homecare treatment. Rising elderly population and chronic patients preferring homecare solutions enhance adoption. Integration with telemedicine services and digital health apps improves treatment compliance and outcomes. The segment benefits from expansion of homecare delivery services and online pharmacy availability. Growth is also supported by patient education campaigns promoting self-management for minor epistaxis. Overall, homecare demonstrates significant CAGR due to convenience, accessibility, and patient preference.

- By Distribution Channel

On the basis of distribution channel, the epistaxis treatment market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment dominated with a market share of 57% in 2024, driven by the direct availability of treatments to inpatients and emergency cases. Hospitals ensure immediate access to medications and devices required for epistaxis management. The segment benefits from institutional procurement policies, bulk purchasing, and established distribution networks. Strong ties between hospital pharmacies and treatment protocols support consistent demand. Availability of advanced therapies, procedural devices, and clinician-preferred brands ensures market dominance. Regulatory compliance and inventory management systems further strengthen hospital pharmacy operations.

The Online Pharmacy segment is expected to witness the fastest CAGR of 10% from 2025 to 2032, fueled by the rise in e-commerce, home delivery services, and patient preference for convenient access to medications. Increased awareness about minor epistaxis management and OTC availability of topical agents drives online sales. The segment benefits from growing digital health adoption, smartphone usage, and expanding internet penetration. Online platforms offer competitive pricing, discounts, and subscription services, enhancing patient engagement. Easy access for rural and urban populations supports market growth. Overall, online pharmacies demonstrate strong CAGR due to convenience, accessibility, and changing consumer behavior.

Epistaxis Treatment Market Regional Analysis

- North America dominated the epistaxis treatment market with the largest revenue share of 42.5% in 2024, driven by well-established healthcare infrastructure, high patient awareness, and the presence of leading pharmaceutical and medical device companies

- The market accounted for a major portion of this growth, fueled by increased hospitalizations for ENT procedures, widespread adoption of advanced hemostatic agents, and robust insurance coverage supporting treatment access

- Growing awareness of preventive care, rising outpatient ENT visits, and ongoing research initiatives in specialized clinics and hospitals further propel market expansion in the region

U.S. Epistaxis Treatment Market Insight

The U.S. epistaxis treatment market captured the largest revenue share in North America in 2024, driven by the rapid expansion of hospitals and specialized ENT clinics, increasing patient awareness, and adoption of advanced therapeutic modalities. Strong healthcare infrastructure, well-trained specialists, and favorable reimbursement policies contribute to the accelerated uptake of epistaxis treatment procedures and medications. The growing prevalence of chronic and recurrent epistaxis cases is further stimulating the adoption of innovative treatment options.

Europe Epistaxis Treatment Market Insight

The Europe epistaxis treatment market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent healthcare regulations, rising patient awareness, and increasing hospitalizations for ENT disorders. The growth is further supported by improved diagnostic and treatment facilities, rising prevalence of comorbidities such as hypertension and coagulation disorders, and increasing adoption of advanced hemostatic therapies. Residential and outpatient ENT clinics are investing in minimally invasive and patient-friendly treatment options, enhancing market penetration across the region.

U.K. Epistaxis Treatment Market Insight

The U.K. epistaxis treatment market is expected to grow at a noteworthy CAGR during the forecast period, fueled by rising awareness about ENT health and preventive care. The increasing number of ENT outpatient visits, coupled with adoption of advanced hemostatic agents and nasal interventions, is driving treatment demand. Rising healthcare expenditure, robust hospital infrastructure, and government-led initiatives promoting access to specialized ENT care support market growth.

Germany Epistaxis Treatment Market Insight

The Germany epistaxis treatment market is projected to expand at a considerable CAGR during the forecast period, attributed to growing awareness of ENT disorders and availability of advanced treatment modalities. Germany’s strong hospital network, presence of specialized ENT clinics, and focus on patient-centric care contribute to increasing adoption of innovative treatment methods. Continued investment in healthcare infrastructure and advancements in minimally invasive techniques further drive market growth.

Asia-Pacific Epistaxis Treatment Market Insight

The Asia-Pacific epistaxis treatment market is poised to grow at the fastest CAGR during the forecast period from 2025 to 2032, driven by improving healthcare infrastructure, rising disposable incomes, and expanding awareness about ENT disorders in countries such as China, India, and Japan. Rapid urbanization, government initiatives promoting ENT healthcare, and growing hospital and clinic networks are key factors supporting market expansion. Increasing accessibility to advanced hemostatic agents, growing outpatient and specialized ENT facilities, and a rising middle-class population contribute to the region’s accelerating market growth.

Japan Epistaxis Treatment Market Insight

The Japan epistaxis treatment market is gaining momentum due to rapid urbanization, high patient awareness, and a strong healthcare system. Advanced ENT clinics, growing adoption of minimally invasive procedures, and focus on patient convenience are driving treatment uptake. An aging population and increasing incidence of chronic epistaxis cases further support market expansion in both hospitals and outpatient care centers.

China Epistaxis Treatment Market Insight

The China epistaxis treatment market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the country’s expanding healthcare infrastructure, growing number of hospitals and specialized ENT clinics, rising patient awareness, and government initiatives promoting ENT health programs. Improved access to diagnostic and treatment facilities, adoption of advanced hemostatic therapies, and increasing healthcare investments are key factors propelling market growth. Rising disposable incomes, urbanization, and emphasis on preventive care further enhance market penetration across both urban and semi-urban regions.

Epistaxis Treatment Market Share

The Epistaxis Treatment industry is primarily led by well-established companies, including:

- Fresenius Kabi AG (Germany)

- Baxter (U.S.)

- Taiho Pharmaceutical Co., Ltd. (Japan)

- Medtronic (Ireland)

- Glenmark Pharmaceuticals (India)

- Aralez Bio (Canada)

- PharmaTech Solutions (U.S.)

- Sinclair Pharma (U.K.)

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

Latest Developments in Global Epistaxis Treatment Market

- In December 2023, Akums Drugs & Pharmaceuticals introduced Doxylamine + Pyridoxine extended-release tablets, a therapy approved by both the Central Drugs Standard Control Organisation (CDSCO) in India and the U.S. Food and Drug Administration (FDA). This combination aims to offer an effective tool to manage symptoms of nausea and vomiting during pregnancy, ensuring better outcomes for both mothers and infants

- In June 2025, the University of California, Los Angeles (UCLA) initiated an efficacy study to evaluate whether Pazopanib, taken daily for 24 weeks, would reduce the severity of nosebleeds in patients with hereditary hemorrhagic telangiectasia (HHT). The study aims to assess the impact on nosebleed duration, blood loss, and overall safety

- In August 2025, Anthem Blue Cross and Blue Shield updated its medical policy to include minimally invasive techniques for inactivating the posterior nasal nerve (PNN) to decrease symptoms of chronic rhinitis or nasal congestion. This includes devices like ClariFix (cryotherapy), RhinAer Stylus, and Neuromark system (radiofrequency), offering new treatment options for patients with chronic nasal symptoms

- In May 2025, Akums Drugs & Pharmaceuticals was granted a patent for its extended-release formulation of Doxylamine and Pyridoxine, designed specifically to address nausea and vomiting in pregnancy (NVP). This innovation aims to provide a more effective and convenient treatment option for managing NVP symptoms

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.