Global Essential Thrombocytosis Treatment Market

Market Size in USD Million

USD

968.50 Million

USD

1,509.03 Million

2025

2033

USD

968.50 Million

USD

1,509.03 Million

2025

2033

| 2026 - 2033 | |

| USD 968.50 Million | |

| USD 1,509.03 Million | |

| % | |

|

Essential Thrombocytosis Treatment Market Size

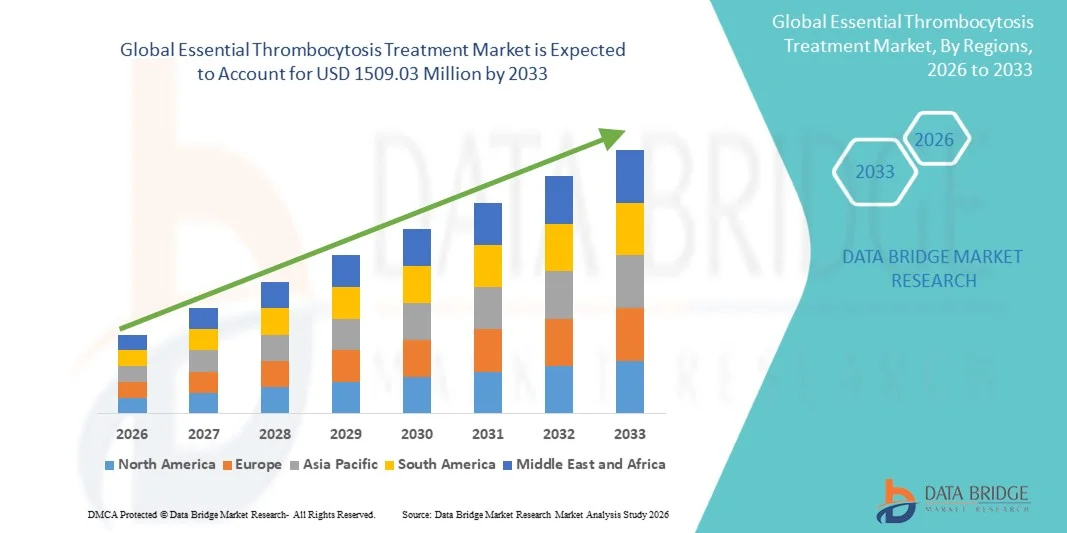

- The global essential thrombocytosis treatment market size was valued at USD 968.50 Million in 2025 and is expected to reach USD 1509.03 Million by 2033, at a CAGR of 5.70% during the forecast period

- The market growth is largely fueled by increasing awareness of blood disorders, rising prevalence of Essential Thrombocytosis (ET), and growing adoption of advanced diagnostic and therapeutic interventions in hematology

- Furthermore, the expanding availability of targeted therapies, such as JAK2 inhibitors, cytoreductive agents, and platelet-lowering medications, coupled with improved access to specialized hematology care, is accelerating the uptake of Essential Thrombocytosis Treatment solutions, thereby significantly boosting the industry's growth

Essential Thrombocytosis Treatment Market Analysis

- Essential Thrombocytosis Treatment, encompassing therapies and interventions for elevated platelet disorders, is increasingly vital in modern healthcare due to its role in preventing complications, improving patient outcomes, and integrating with specialized hematology care

- The escalating demand for essential thrombocytosis treatment is primarily fueled by rising disease awareness, advancements in targeted therapies, growing access to specialized healthcare facilities, and the increasing prevalence of hematologic disorders

- North America dominated the essential thrombocytosis treatment market with the largest revenue share of approximately 39.5% in 2025, characterized by advanced healthcare infrastructure, high treatment awareness, and strong availability of specialized therapies, with the U.S. experiencing substantial growth due to early diagnosis and adoption of modern hematology treatment protocols

- Asia-Pacific is expected to be the fastest-growing region in the essential thrombocytosis treatment market during the forecast period due to rising healthcare expenditure, increasing prevalence of hematologic disorders, expanding access to specialized care, and growing awareness of disease management

- The oral segment dominated the largest market revenue share of 56.7% in 2025, due to convenience, efficacy, and widespread acceptance

Report Scope and Essential Thrombocytosis Treatment Market Segmentation

|

Attributes |

Essential Thrombocytosis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Essential Thrombocytosis Treatment Market Trends

“Rising Adoption of Targeted Therapies and Personalized Medicine”

- A significant and accelerating trend in the global essential thrombocytosis treatment market is the growing adoption of targeted therapies, including JAK2 inhibitors and novel cytoreductive agents. These therapies are increasingly preferred over traditional treatments due to their ability to specifically modulate platelet production and reduce thrombotic risks

- For instance, ruxolitinib and hydroxyurea-based regimens are being widely incorporated into treatment protocols for patients with high-risk profiles, improving disease management outcomes. Similarly, emerging combination therapies aim to enhance efficacy while minimizing side effects

- The focus on personalized medicine enables physicians to tailor treatments based on patient genetic profiles, risk factors, and disease progression, resulting in more effective care. Clinical studies and real-world evidence support improved survival and quality of life for patients receiving targeted therapies

- Healthcare providers are increasingly integrating genetic testing and risk stratification into standard protocols, facilitating precise therapy selection. Pharmaceutical companies are investing in research and development to expand the pipeline of targeted agents, addressing unmet clinical needs

- Patient advocacy groups are also driving awareness of individualized treatment options, influencing therapy adoption. The use of biomarker-guided therapy helps in monitoring response and adjusting dosing regimens efficiently

Essential Thrombocytosis Treatment Market Dynamics

Driver

“Increasing Prevalence and Early Diagnosis of Essential Thrombocytosis”

- The rising prevalence of essential thrombocytosis, particularly among aging populations, is a significant driver for market growth. Early diagnosis and timely intervention are critical to prevent thrombotic complications and improve patient outcomes

- For instance, routine blood screening and platelet count monitoring have increased early detection rates, enabling proactive treatment

- Physicians are now more aware of the importance of differentiating Essential Thrombocytosis from secondary thrombocytosis, ensuring appropriate therapy

- Advances in diagnostic tools, including genetic testing for JAK2, CALR, and MPL mutations, facilitate accurate identification of patients

- Early intervention reduces complications such as stroke or deep vein thrombosis, improving patient quality of life

- Growing awareness among healthcare providers about risk stratification and treatment guidelines supports increased therapy adoption

- Hospitals and specialty clinics are integrating structured care pathways to manage high-risk patients effectively

- Increased patient awareness campaigns highlight the importance of early diagnosis and ongoing monitoring

- Pharmaceutical companies are collaborating with healthcare institutions to support screening initiatives

- The aging global population, combined with better healthcare access, continues to expand the pool of diagnosed patients

- Improved diagnostic accuracy ensures that patients receive the right treatment at the right time

- These factors collectively drive the demand for Essential Thrombocytosis therapies across regions

Restraint/Challenge

“Side Effects of Long-Term Therapies and High Treatment Costs”

- Concerns related to adverse effects from long-term therapy, including cytoreductive agents and anticoagulants, pose a significant challenge to market growth. Patients may experience complications such as myelosuppression, anemia, or bleeding events, affecting adherence

- For instance, hydroxyurea treatment, while effective, requires close monitoring to avoid toxicity. Some patients discontinue therapy due to side effects, reducing market uptake

- In addition, high costs associated with targeted therapies and genetic testing can limit access, particularly in developing regions

- Insurance coverage varies significantly, influencing patient affordability and adoption rates. While generic formulations are gradually becoming available, branded therapies with advanced efficacy still carry a premium price

- Limited patient awareness about alternative or supportive therapies can reduce overall market penetration. Healthcare providers must balance efficacy with safety when prescribing treatments, which can slow widespread adoption

- Regulatory compliance and monitoring requirements for novel agents can add to operational and financial burdens for clinics and hospitals. Availability of trained specialists to manage high-risk patients also impacts treatment adoption

- Patient hesitancy due to potential side effects may result in delayed initiation of therapy. Efforts to develop cost-effective and safer therapies are ongoing but require time and investment. Addressing these challenges through improved patient education, financial assistance programs, and safer formulations is critical for sustained market growth

Essential Thrombocytosis Treatment Market Scope

The market is segmented on the basis of treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel

• By Treatment

On the basis of treatment, the Essential Thrombocytosis Treatment market is segmented into medication, plateletpheresis, and others. The medication segment dominated the largest market revenue share of 57.4% in 2025, driven by its broad clinical adoption for managing elevated platelet counts and reducing thrombotic risk. Oral medications, including hydroxyurea and interferon-based therapies, are widely prescribed due to proven efficacy and safety profiles. Physicians prioritize medications as first-line therapy for high-risk patients. Hospitals and clinics maintain extensive inventories of medications for immediate treatment. Medications enable both acute management and long-term maintenance, improving patient quality of life. Insurance coverage and reimbursement support widespread access. Advancements in formulation and dosing flexibility enhance adherence. Patients value medications for convenience and consistent symptom control. Clinical guidelines recommend medication as a standard treatment protocol. Pharmaceutical companies continue investing in improved compounds. Overall, medications remain the cornerstone of Essential Thrombocytosis management in 2025.

The plateletpheresis segment is expected to witness the fastest CAGR of 10.8% from 2026 to 2033, driven by growing adoption for patients with extreme thrombocytosis or those intolerant to medication. Plateletpheresis rapidly reduces circulating platelet counts and mitigates thrombotic risk. Hospitals and specialty centers increasingly offer apheresis services. Technological improvements enhance procedure efficiency and patient safety. Outpatient and inpatient settings are integrating plateletpheresis into treatment protocols. Rising awareness of procedural efficacy among hematologists supports adoption. Patients requiring rapid intervention increasingly benefit from this approach. Insurance coverage is gradually improving, expanding access. Clinical studies reinforce procedural effectiveness and safety. Training and guidelines help standardize protocols. Adoption is rising in regions with advanced hematology care.

• By Diagnosis

On the basis of diagnosis, the Essential Thrombocytosis Treatment market is segmented into blood tests, bone marrow biopsy, gene mutation analysis, and others. The blood tests segment held the largest market revenue share of 45.6% in 2025, driven by the routine use of complete blood counts to detect elevated platelet levels. Blood tests are minimally invasive, cost-effective, and widely available across hospitals and clinics. They facilitate early detection and ongoing monitoring of patients. Physicians rely on blood counts to guide treatment initiation and adjust therapy. Hospitals integrate automated analyzers for accuracy and efficiency. Screening protocols for high-risk populations enhance diagnostic uptake. Blood tests support monitoring of response to medications. Reimbursement and insurance coverage improve access. Laboratories and clinics maintain established testing workflows. Patient convenience and familiarity further reinforce adoption. Combined clinical utility and operational ease make blood tests the preferred diagnostic method.

The gene mutation analysis segment is expected to witness the fastest CAGR of 11.2% from 2026 to 2033, fueled by the growing importance of JAK2, CALR, and MPL mutation testing for personalized treatment. Genetic testing enables risk stratification and therapy selection. Hospitals and specialty laboratories increasingly adopt molecular diagnostics. Early identification of high-risk mutations improves prognosis and guides therapeutic decisions. Integration of molecular testing into routine protocols enhances precision care. Awareness among hematologists regarding mutation-guided management is rising. Insurance and reimbursement support gradually expand patient access. Advances in testing platforms reduce turnaround time and cost. Education campaigns for clinicians and patients improve adoption rates. Adoption is particularly high in developed regions with advanced healthcare infrastructure. Genetic testing drives personalized therapy and enhances clinical outcomes. These factors collectively support rapid growth for gene mutation analysis through 2033.

• By Symptoms

On the basis of symptoms, the Essential Thrombocytosis Treatment market is segmented into dizziness, bleeding, headache, chest pain, numbness, sweating, temporary vision changes, redness and burning pain in the hands and feet, itchiness, fainting, and others. The bleeding segment accounted for the largest market revenue share of 36.5% in 2025, as hemorrhagic events represent a critical clinical manifestation of Essential Thrombocytosis. Patients frequently present with easy bruising, nosebleeds, or prolonged bleeding. Management of bleeding complications is a key therapeutic priority. Hospitals and clinics focus on early detection and prevention. Medications, plateletpheresis, and supportive care are utilized to control bleeding risk. Clinical guidelines emphasize monitoring for hemorrhagic events. Patients value timely intervention to reduce complications. Awareness campaigns inform patients and caregivers about early warning signs. Physician vigilance ensures rapid response and appropriate therapy. Effective management improves patient quality of life. Access to diagnostic and treatment resources enhances outcomes. Combined clinical importance and patient concern make bleeding the dominant symptom segment.

The redness and burning pain in the hands and feet segment is expected to witness the fastest CAGR of 9.9% from 2026 to 2033, driven by increasing recognition of microvascular complications. Patients with erythromelalgia and localized pain are seeking earlier intervention. Hospitals and specialty clinics incorporate symptom management into routine care. Therapies targeting vascular inflammation and platelet control improve patient comfort. Awareness among hematologists of symptom-specific treatment strategies is growing. OTC and prescription medications aid symptom relief. Patient-reported outcomes guide therapy adjustments. Telemedicine enables better monitoring of symptom progression. Clinical studies support effective management of burning pain and redness. Education programs for patients encourage early reporting and adherence. Combined advances in care delivery and awareness support rapid growth for this segment.

• By Dosage

On the basis of dosage, the Essential Thrombocytosis Treatment market is segmented into tablet, capsule, injection, and others. The tablet segment dominated the largest market revenue share of 52.1% in 2025, driven by widespread preference for oral administration and ease of use. Tablets are convenient, support consistent dosing, and are easily prescribed in both outpatient and hospital settings. Physicians rely on tablets for long-term management of platelet counts. Patients value adherence and flexibility in administration. Retail pharmacies and hospital pharmacies widely stock tablet formulations. Tablets allow combination therapy with other supportive medications. Insurance coverage enhances access for patients. Clinical studies demonstrate efficacy and safety of oral tablets. Tablets reduce the need for invasive interventions. Education campaigns support patient understanding and proper usage. Overall, tablets remain the dominant dosage form.

The injection segment is expected to witness the fastest CAGR of 10.5% from 2026 to 2033, fueled by increasing use of injectable medications and biologics for high-risk patients. Injectable therapies allow rapid control of platelet counts and acute symptom management. Hospitals and specialty centers provide image-guided or monitored injections. Patient demand for fast-acting treatment supports growth. Clinical protocols incorporate injections for refractory cases. Insurance and reimbursement gradually improve accessibility. Pharmaceutical innovations expand injectable options. Education of healthcare providers supports proper administration. Hospital adoption is increasing due to procedural efficacy. Clinical evidence confirms safety and effectiveness. Patient convenience and improved outcomes drive adoption.

• By Route of Administration

On the basis of route of administration, the Essential Thrombocytosis Treatment market is segmented into oral, intralesional, intravenous, intramuscular, subcutaneous, and others. The oral segment dominated the largest market revenue share of 56.7% in 2025, due to convenience, efficacy, and widespread acceptance. Patients prefer oral administration for long-term therapy and adherence. Physicians prioritize oral routes for first-line treatment. Hospitals and clinics stock oral medications extensively. Oral administration allows easy combination with other therapies. Insurance coverage improves access. Patient familiarity enhances compliance. Clinical guidelines recommend oral routes for most high-risk patients. Pharmaceutical companies continue developing oral formulations with improved pharmacokinetics. Convenience and patient preference drive continued dominance.

The subcutaneous segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by increasing adoption of biologics and supportive therapies administered via subcutaneous injection. Subcutaneous administration improves patient comfort and allows self-administration at home. Hospitals and clinics support training for patients and caregivers. Clinical studies confirm efficacy and safety. Rising awareness among hematologists drives adoption. Insurance coverage and patient assistance programs facilitate access. Telemedicine and remote monitoring support adherence. Patient convenience and improved outcomes promote growth. Technological advances in needle-free or auto-injector devices further enhance uptake. Education and clinical guidance reinforce adoption. These factors collectively support rapid growth through 2033.

• By End-Users

On the basis of end-users, the Essential Thrombocytosis Treatment market is segmented into clinic, hospital, and others. The hospital segment accounted for the largest market revenue share of 49.8% in 2025, driven by the availability of advanced diagnostic and treatment facilities for high-risk patients. Hospitals provide multidisciplinary care, including hematology, cardiology, and vascular services. Patient volume and case complexity contribute to hospital dominance. Hospitals integrate monitoring tools for platelet counts and thrombotic risk. Physicians rely on hospital infrastructure for safe administration of therapies. Hospitals maintain inventories of medication, plateletpheresis equipment, and supportive care products. Clinical protocols and guidelines reinforce hospital adoption. Insurance coverage favors hospital-based interventions. Hospitals provide patient education and follow-up care. Marketing and training programs strengthen hospital role. Overall, hospitals remain the primary end-user.

The clinic segment is expected to witness the fastest CAGR of 9.7% from 2026 to 2033, fueled by growing outpatient care and demand for routine monitoring of low- to medium-risk patients. Clinics provide accessible care, early detection, and follow-up services. Telemedicine integration supports remote monitoring. Physicians manage therapy adjustments efficiently in outpatient settings. Clinics increase patient convenience and adherence. Expansion of specialty hematology clinics supports growth. Cost-effective care and shorter waiting times encourage utilization. Education and awareness campaigns improve patient engagement. Standardized protocols in clinics facilitate treatment consistency. Combined, these factors drive rapid growth for clinics.

• By Distribution Channel

On the basis of distribution channel, the Essential Thrombocytosis Treatment market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The retail pharmacy segment dominated the largest market revenue share of 46.2% in 2025, due to easy access, widespread availability, and convenience for patients. Retail pharmacies stock oral medications, supportive therapies, and supplements. Patients value accessibility and immediate product availability. Pharmacists guide patients on dosage and adherence. Retail chains and independent stores provide broad geographic coverage. Marketing campaigns and brand recognition reinforce retail dominance. Insurance coverage supports access through retail channels. Repeat purchases and patient familiarity strengthen adoption. Retail pharmacies integrate with local clinics to enhance availability. Convenience and accessibility make retail the primary distribution channel.

The online pharmacy segment is expected to witness the fastest CAGR of 12.5% from 2026 to 2033, driven by digitalization and e-commerce expansion. Patients increasingly prefer home delivery for medications and monitoring devices. Telemedicine integration facilitates prescription fulfillment. Online pharmacies provide a wider product range than local stores. Price competition, subscription models, and promotions attract users. Regulatory frameworks gradually improve, enabling safe online distribution. Digital marketing and awareness campaigns support adoption. Convenience, accessibility, and privacy drive growth. Technological innovations streamline order processing and patient adherence.

Essential Thrombocytosis Treatment Market Regional Analysis

- North America dominated the essential thrombocytosis treatment market with the largest revenue share of approximately 39.5% in 2025, characterized by advanced healthcare infrastructure, high treatment awareness, and strong availability of specialized therapies, with the U.S. experiencing substantial growth due to early diagnosis and adoption of modern hematology treatment protocols

- Consumers in the region highly value the accessibility of specialized hematology centers, advanced diagnostic services, and availability of medications including platelet-lowering agents and targeted therapies

- This widespread adoption is further supported by high healthcare spending, well-trained medical personnel, and the growing preference for personalized treatment approaches, establishing North America as the leading region for essential thrombocytosis management

U.S. Essential Thrombocytosis Treatment Market Insight

The U.S. essential thrombocytosis treatment market captured the largest revenue share in 2025 within North America, fueled by the increasing prevalence of myeloproliferative disorders and widespread adoption of advanced hematology treatment protocols. Patients are increasingly seeking specialized care involving plateletpheresis, targeted medication, and comprehensive monitoring. The growing integration of diagnostic innovations, gene mutation analysis, and personalized treatment plans further propels the Essential Thrombocytosis Treatment industry. Moreover, strong insurance coverage and established hematology centers significantly contribute to the market's expansion.

Europe Essential Thrombocytosis Treatment Market Insight

The Europe essential thrombocytosis treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of hematologic disorders, government initiatives promoting early diagnosis, and widespread availability of advanced therapies. The increase in urbanization, coupled with the demand for specialized treatment centers, is fostering the adoption of platelet-lowering therapies and supportive care. European patients are also drawn to the comprehensive monitoring and multidisciplinary approach offered by leading healthcare providers.

U.K. Essential Thrombocytosis Treatment Market Insight

The U.K. essential thrombocytosis treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of hematologic disorders, rising awareness of early diagnosis, and growing preference for specialized hematology care. Additionally, government healthcare programs and robust clinical infrastructure are encouraging both patients and physicians to adopt modern treatment regimens, including targeted medications and plateletpheresis. The U.K.’s emphasis on preventive care and chronic disease management is expected to continue stimulating market growth.

Germany Essential Thrombocytosis Treatment Market Insight

The Germany essential thrombocytosis treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of essential thrombocytosis, well-developed healthcare infrastructure, and the demand for technologically advanced and patient-centric solutions. Germany’s focus on early diagnosis, advanced hematology labs, and clinical research promotes the adoption of innovative therapies, particularly in specialized hospital settings. Integration of gene mutation testing and tailored treatment protocols is becoming increasingly prevalent, aligning with local patient expectations.

Asia-Pacific Essential Thrombocytosis Treatment Market Insight

The Asia-Pacific essential thrombocytosis treatment market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing healthcare expenditure, rising prevalence of hematologic disorders, and expanding access to specialized care in countries such as China, Japan, and India. The region's growing awareness of early diagnosis and disease management, supported by government initiatives and investments in healthcare infrastructure, is driving adoption of essential thrombocytosis therapies. Furthermore, as APAC strengthens its hematology healthcare facilities and enhances accessibility to modern treatment options, the market is expanding to a wider patient population.

Japan Essential Thrombocytosis Treatment Market Insight

The Japan essential thrombocytosis treatment market is gaining momentum due to the country’s high healthcare standards, aging population, and rising prevalence of myeloproliferative disorders. Japanese patients are increasingly prioritizing specialized care in advanced hematology centers. Integration of advanced diagnostics, personalized treatment protocols, and plateletpheresis procedures is fueling market growth. Additionally, Japan’s emphasis on preventive healthcare and chronic disease management is likely to spur demand for comprehensive thrombocytosis treatment solutions in both hospital and clinical settings.

China Essential Thrombocytosis Treatment Market Insight

The China essential thrombocytosis treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's expanding middle class, rapid urbanization, and growing healthcare awareness. China has seen increasing investments in specialized hematology centers, modern diagnostic laboratories, and availability of advanced treatment options. Rising prevalence of hematologic disorders, combined with government initiatives promoting early detection and disease management, are key factors propelling the market in China. The increasing accessibility and affordability of essential thrombocytosis therapies are further expanding the patient base across both urban and semi-urban regions.

Essential Thrombocytosis Treatment Market Share

The Essential Thrombocytosis Treatment industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- GlaxoSmithKline plc (U.K.)

- Bristol-Myers Squibb (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Sanofi S.A. (France)

- AstraZeneca plc (U.K.)

- Incyte Corporation (U.S.)

- Bayer AG (Germany)

- Celgene Corporation (U.S.)

- Roche Holding AG (Switzerland)

- Novimmune SA (Switzerland)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

Latest Developments in Global Essential Thrombocytosis Treatment Market

- In January 2025, the Phase 3 Ropeginterferon alfa-2b (P1101 / BESREMi) — previously approved for polycythemia vera — was reported to have succeeded in the SURASS-ET trial for ET, achieving a significantly higher durable clinical response rate than Anagrelide (42.9% vs. 6.0%), along with a greater reduction in JAK2 V617F allele burden over 12 months

- In August 2024, the European Commission (EC) granted marketing authorization for a “Type II variation” of Peginterferon alfa-2a (PEGASYS) allowing its use as a monotherapy for adults with ET — representing a notable regulatory milestone since ET has had very few drugs specifically approved for it in Europe

- In March 2025, multiple market‑analysis sources projected a strong upswing in the ET treatment market, driven by the recent approvals and the advancing pipeline of novel therapeutics (including interferons and other investigational agents), indicating growing commercial and clinical interest in ET

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.