Global Familial Adenomatous Polyposis Treatment Market

Market Size in USD Billion

USD

2.09 Billion

USD

6.42 Billion

2024

2032

USD

2.09 Billion

USD

6.42 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.09 Billion | |

| USD 6.42 Billion | |

| % | |

|

Familial Adenomatous Polyposis Treatment Market Size

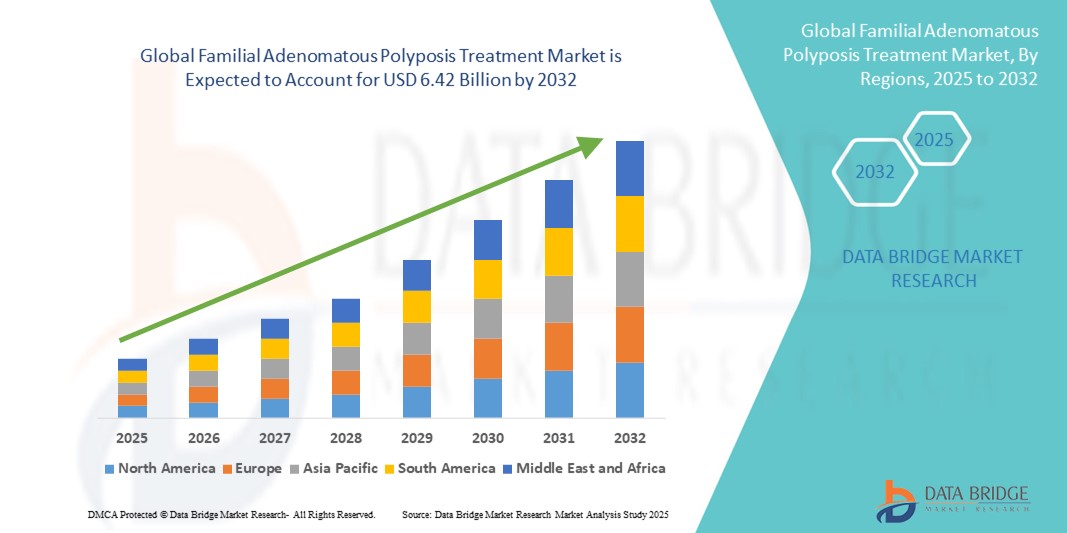

- The global familial adenomatous polyposis treatment market size was valued at USD 2.09 billion in 2024 and is expected to reach USD 6.42 billion by 2032, at a CAGR of 15.00% during the forecast period

- The market growth is largely fueled by increasing awareness of genetic disorders and advancements in targeted therapies, leading to more effective management of familial adenomatous polyposis (FAP) across different patient populations

- Furthermore, rising demand for early detection, personalized treatment strategies, and improved patient outcomes is driving the adoption of Familial Adenomatous Polyposis Treatment solutions, thereby significantly boosting the industry's growth

Familial Adenomatous Polyposis Treatment Market Analysis

- Familial Adenomatous Polyposis (FAP) treatment options, encompassing surgical interventions, targeted therapies, and supportive care, are increasingly vital components of modern gastrointestinal healthcare due to their effectiveness in preventing colorectal cancer, improving patient quality of life, and enabling personalized treatment strategies

- The escalating demand for effective treatment options for familial adenomatous polyposis (FAP) is primarily fueled by increasing awareness about early diagnosis, rising prevalence of the disease, and growing investments in research and development of novel therapies

- North America dominated the familial adenomatous polyposis treatment market with the largest revenue share of 43.0% in 2024, driven by advanced healthcare infrastructure, high adoption of genetic screening programs, and the presence of key pharmaceutical companies investing in innovative therapies. The U.S. remains a major contributor, with rising awareness campaigns and early intervention strategies enhancing market growth

- Asia-Pacific is expected to be the fastest-growing region in the familial adenomatous polyposis treatment market during the forecast period, with a CAGR of 8.6% from 2025 to 2032, due to increasing urbanization, rising disposable incomes, and expansion of healthcare facilities offering specialized gastrointestinal and genetic services

- The Familial Adenomatous Polyposis segment dominated familial adenomatous polyposis treatment market with a market share of 45.2% in 2024, due to its higher prevalence compared to other subtypes and its critical need for early intervention to prevent colorectal cancer

Report Scope and Familial Adenomatous Polyposis Treatment Market Segmentation

|

Attributes |

Familial Adenomatous Polyposis Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Familial Adenomatous Polyposis Treatment Market Trends

Enhanced Patient Outcomes and Personalized Care

- A significant and accelerating trend in the global familial adenomatous polyposis treatment market is the increasing adoption of personalized and targeted therapeutic approaches. This trend is enhancing patient outcomes and improving long-term management of the disease

- For instance, advanced surgical interventions combined with prophylactic measures are helping patients effectively reduce the risk of colorectal cancer, while targeted pharmacological therapies provide alternatives to delay or complement surgery

- Integration of genetic testing and early screening programs enables clinicians to identify high-risk patients promptly, allowing for timely interventions and tailored treatment strategies based on individual patient profiles

- The expansion of specialized treatment centers and gastroenterology clinics facilitates centralized, high-quality care, ensuring that patients have access to comprehensive FAP management services under one roof

- This trend towards more effective, evidence-based, and patient-centric treatment strategies is fundamentally reshaping clinical practices and improving the overall quality of care in the FAP therapeutic landscape

- The demand for advanced treatment options that combine surgical, pharmacological, and supportive care is growing rapidly across both developed and emerging markets, as healthcare providers increasingly focus on optimizing outcomes and quality of life for patients

Familial Adenomatous Polyposis Treatment Market Dynamics

Driver

Growing Need Due to Rising Prevalence and Awareness of FAP

- The increasing prevalence of familial adenomatous polyposis, coupled with growing awareness among patients, caregivers, and healthcare providers, is a major driver for the expanding demand for effective treatment solutions. Early detection and intervention are essential to prevent progression to colorectal cancer, creating a critical need for timely therapeutic and diagnostic interventions

- For instance, in April 2023, Takeda Pharmaceutical Company Limited expanded its clinical trials program for CEQ-508, targeting patients with genetically confirmed FAP. Such strategic initiatives by leading companies are expected to significantly boost the growth of the FAP Treatment market in the forecast period

- As patients and caregivers become increasingly informed about symptoms such as bloody stool, unexplained diarrhea, abdominal cramps, bloating, and weight loss, the adoption of pharmacological therapies such as Icosapent, Eflornithine Hydrochloride, and Aspirin, alongside emerging therapies such as CEQ-508, is gaining momentum

- Furthermore, the growing focus on routine screening, continuous monitoring through diagnostic centers, and home healthcare services is improving treatment adherence and patient outcomes. Healthcare providers are emphasizing personalized treatment plans, integrating pharmacological therapy with dietary management and symptom-based care to manage disease progression effectively

- The availability of both branded and generic formulations, combined with expanding distribution through hospital pharmacies, retail outlets, and online platforms, is improving accessibility and affordability for patients across developed and emerging market

Restraint/Challenge

High Treatment Costs and Limited Awareness in Emerging Markets

- The relatively high cost of advanced therapies, including CEQ-508, Eflornithine Hydrochloride, and other specialized FAP treatments, poses a significant barrier to market growth, especially in price-sensitive regions. Many patients in emerging economies face financial constraints, limiting access to these therapies despite their proven efficacy in preventing disease progression

- Inadequate insurance coverage and limited reimbursement options in certain regions further exacerbate the affordability challenge, making it difficult for patients to initiate or maintain long-term treatment regimens

- In addition, limited awareness among patients, caregivers, and some healthcare providers about the early symptoms of Familial Adenomatous Polyposis—such as bloody stool, unexplained diarrhea, abdominal cramps, bloating, and weight loss—delays diagnosis and treatment initiation. This lack of awareness results in disease progression to more severe conditions, including colorectal cancer, before interventions are administered

- Addressing these challenges requires a multifaceted approach, including patient education campaigns, professional training for healthcare providers, and awareness initiatives led by governments or patient advocacy groups. These measures aim to improve early diagnosis rates, ensure timely initiation of therapy, and enhance patient adherence

- Furthermore, ongoing research and development efforts focused on cost-effective, safe, and more accessible treatment options are essential to overcoming these market barriers. Expansion of home-based care services, telemedicine support, and outreach programs in remote or underserved areas can also mitigate challenges related to accessibility and affordability, fostering broader market adoption over the forecast period

Familial Adenomatous Polyposis Treatment Market Scope

The market is segmented on the basis of product type, symptoms, disease subtype, end-users, and distribution channel.

- By Product Type

On the basis of product type, the familial adenomatous polyposis treatment market is segmented into Icosapent, Eflornithine Hydrochloride, Aspirin, CEQ-508, and Others. The Icosapent segment dominated the largest market revenue share of 44.0% in 2024, driven by its well-documented clinical efficacy in preventing polyp growth and reducing colorectal cancer risk in high-risk patients. Its favorable safety profile and well-established dosing guidelines encourage physician preference and patient adherence. Furthermore, increasing awareness among patients about preventive care contributes to strong market penetration. The segment also benefits from extensive research publications validating its long-term benefits. In addition, growing inclusion in treatment protocols and coverage by insurance plans enhances its widespread adoption. Icosapent’s integration in multidisciplinary treatment approaches ensures its leadership in the market.

The CEQ-508 segment is expected to witness the fastest CAGR of 10.2% from 2025 to 2032, fueled by ongoing clinical trials demonstrating promising efficacy, as well as increasing physician awareness of its targeted therapeutic potential. Its adoption is driven by emerging evidence highlighting symptom-specific benefits and reduced adverse effects. Regulatory approvals in key regions further accelerate market uptake. Growth is also supported by rising patient interest in novel therapies with personalized treatment options. Expanding research collaborations and early adoption in specialty centers enhance visibility and acceptance. CEQ-508’s strong pipeline developments and positive clinical outcomes are central to its rapid growth trajectory.

- By Symptoms

On the basis of symptoms, the familial adenomatous polyposis treatment market is segmented into Bloody Stool, Unexplained Diarrhea, Abdominal Cramps, Bloating, Weight Loss, Lethargy, and Vomiting. The Bloody Stool segment dominated the market with a revenue share of 41.5% in 2024, as it is the most common and alarming early indicator prompting timely diagnosis and intervention. Healthcare providers prioritize treatments for patients presenting with this symptom due to associated higher risk of polyp progression. Increasing screening initiatives targeting symptomatic patients reinforce the segment’s dominance. Awareness campaigns by patient advocacy groups further support early detection. The segment also benefits from strong clinical guideline recommendations emphasizing monitoring and therapeutic intervention. Improved diagnostic tools facilitate rapid identification, supporting high adoption of therapies in this patient group.

The Abdominal Cramps segment is anticipated to witness the fastest CAGR of 9.8% from 2025 to 2032, driven by greater patient reporting and heightened recognition among clinicians of symptom-specific therapy needs. Expansion of educational programs and improved physician awareness contribute to rapid adoption. Growing use of imaging and monitoring techniques for early symptom identification also supports growth. Patients increasingly seek targeted therapy to relieve discomfort, creating additional market demand. Health systems are integrating symptom management into comprehensive care plans. Rising incidence reporting and diagnostic improvements further enhance market uptake for this subsegment.

- By Disease Subtype

On the basis of disease subtype, the familial adenomatous polyposis treatment market is segmented into Attenuated FAP, Familial Adenomatous Polyposis, Gardner Syndrome, and Turcot Syndrome. The Familial Adenomatous Polyposis segment dominated with a market share of 45.2% in 2024, due to its higher prevalence compared to other subtypes and its critical need for early intervention to prevent colorectal cancer. Routine genetic screening and strong clinical awareness drive early diagnosis, supporting market dominance. Integration into established treatment protocols ensures wide therapy adoption. Ongoing research on disease management further strengthens clinical confidence. Patient advocacy and education programs emphasize early intervention benefits. The availability of both conventional and novel therapeutic options under this segment enhances its leadership in the market.

The Gardner Syndrome segment is projected to witness the fastest CAGR of 10.0% from 2025 to 2032, fueled by advancements in genetic testing enabling early detection and a growing emphasis on multidisciplinary management. Clinician awareness of extracolonic manifestations is increasing targeted therapy adoption. Rising patient education and proactive monitoring contribute to faster uptake. Research initiatives are expanding understanding of disease complexity, supporting therapeutic development. The segment benefits from evolving treatment pipelines focusing on precision medicine. Early interventions and specialized care centers drive accelerated growth in this niche patient population.

- By End-Users

On the basis of end-users, the familial adenomatous polyposis treatment market is segmented into Clinics, Hospitals, Diagnostic Centres, Home Healthcare, and Others. The Hospitals segment dominated with a revenue share of 47.1% in 2024, due to centralized facilities, availability of gastroenterology specialists, and the ability to provide integrated monitoring for high-risk patients. Hospitals also facilitate coordinated therapy and follow-up, improving patient outcomes. Institutional purchasing policies and structured care pathways strengthen this segment’s position. High patient footfall ensures consistent therapy demand. Inclusion in hospital formularies supports wide access. Hospitals’ capacity to deliver specialized, evidence-based care maintains market leadership.

The Home Healthcare segment is expected to witness the fastest CAGR of 9.5% from 2025 to 2032, driven by rising preference for patient-centric care, convenience for chronic condition management, and growing awareness of home-based monitoring technologies. Remote therapy management is increasingly adopted for post-operative care and long-term maintenance. Expanded insurance coverage and supportive infrastructure enhance access. Patient preference for reduced hospital visits accelerates growth. Integration with telehealth services ensures continuity of care. The segment benefits from increasing partnerships between home healthcare providers and specialty centers.

- By Distribution Channel

On the basis of distribution channel, the familial adenomatous polyposis treatment market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The Hospital Pharmacy segment dominated with a market share of 46.0% in 2024, owing to direct access to prescription-based therapies, clinical oversight, and professional guidance for patient management. Hospitals ensure proper dosing, monitoring, and adherence, supporting high adoption rates. Integration with care pathways strengthens market dominance. Institutional contracts and bulk procurement policies drive sustained supply. Presence of specialty pharmacists reinforces credibility. Hospitals’ ability to deliver safe and effective treatment maintains leadership in the distribution space.

The Online Pharmacy segment is anticipated to witness the fastest CAGR of 11.0% from 2025 to 2032, driven by rising e-commerce penetration, convenience of doorstep delivery, and increasing adoption in urban and remote locations. Growth is fueled by patient preference for privacy and faster access to therapies. Awareness campaigns and digital marketing enhance segment visibility. Partnerships with logistics and telemedicine platforms improve delivery efficiency. Regulatory clarity and payment flexibility support increased adoption. Expansion of online pharmacy infrastructure accelerates accessibility and patient adherence.

Familial Adenomatous Polyposis Treatment Market Regional Analysis

- North America dominated the familial adenomatous polyposis treatment market with the largest revenue share of 43.0% in 2024, driven by advanced healthcare infrastructure, high adoption of genetic screening programs, and the presence of key pharmaceutical companies investing in innovative therapies

- Rising awareness campaigns and early intervention strategies have significantly enhanced market growth. The U.S. remains the major contributor within the region, supported by robust clinical research, accessibility of novel treatments, and comprehensive patient management programs. Widespread availability of specialty clinics and hospitals offering gastroenterology and genetic services further reinforces the region’s dominance

- Increasing focus on preventive care and routine monitoring of high-risk populations strengthens the adoption of targeted therapies. In addition, collaborations between academic institutes and healthcare providers facilitate faster adoption of cutting-edge treatment options

U.S. Familial Adenomatous Polyposis Treatment Market Insight

The U.S. familial adenomatous polyposis treatment market captured the largest revenue share of 82% in 2024 within North America, driven by the widespread uptake of genetic testing and advanced therapeutic interventions. Patients benefit from comprehensive treatment plans combining enzyme therapy, nutritional management, and prophylactic interventions. The country has a strong presence of pharmaceutical and biotechnology firms developing both branded and generic therapies, accelerating market growth. Early diagnosis initiatives and national awareness programs encourage timely intervention, enhancing patient outcomes. Hospitals, specialty clinics, and research centers provide integrated treatment options, boosting therapy adoption. Moreover, expanding reimbursement coverage and insurance support enable broader patient access to FAP treatments.

Europe Familial Adenomatous Polyposis Treatment Market Insight

The Europe familial adenomatous polyposis treatment market is projected to expand at a steady CAGR during the forecast period, supported by increasing investment in healthcare infrastructure and genetic research initiatives. Stringent regulatory standards and preventive care programs drive early diagnosis and therapy adoption. Rising awareness of hereditary gastrointestinal disorders, coupled with increased access to hospitals and specialty clinics, strengthens market growth. Countries like Germany, France, and Italy are witnessing higher adoption of enzyme replacement therapy and nutritional management plans. The integration of advanced diagnostics in routine care facilitates timely intervention. In addition, the presence of established pharmaceutical companies in the region ensures availability of both generic and branded therapies.

U.K. Familial Adenomatous Polyposis Treatment Market Insight

The U.K. familial adenomatous polyposis treatment market is expected to grow at a notable CAGR, driven by increased awareness of genetic testing and proactive preventive care programs. The country emphasizes early diagnosis and patient monitoring, particularly in high-risk populations. Hospitals and specialized gastroenterology clinics offer comprehensive FAP management, including enzyme therapy and nutritional interventions. Expansion of national healthcare initiatives promotes widespread adoption of evidence-based therapies. The robust healthcare infrastructure and insurance coverage further support accessibility. Collaborative research efforts among academic institutions contribute to innovation and therapy optimization.

Germany Familial Adenomatous Polyposis Treatment Market Insight

The Germany familial adenomatous polyposis treatment market is expected to expand at a considerable CAGR due to strong investment in healthcare research, genetic screening, and preventive care programs. The country has well-developed hospitals and specialized clinics offering both diagnostic and therapeutic services for FAP patients. Patients benefit from early intervention strategies, including enzyme replacement therapy and prophylactic surgical options. Growing awareness of hereditary colorectal disorders drives therapy adoption. The presence of multinational pharmaceutical companies enhances availability of branded and generic therapies. Integration of advanced diagnostics in routine clinical care supports timely treatment and improved patient outcomes.

Asia-Pacific Familial Adenomatous Polyposis Treatment Market Insight

The Asia-Pacific familial adenomatous polyposis treatment market is expected to be the fastest-growing region with a CAGR of 8.6% from 2025 to 2032, driven by increasing urbanization, rising disposable incomes, and expansion of healthcare facilities offering specialized gastrointestinal and genetic services. Countries such as China, India, and Japan are investing in advanced diagnostic tools and genetic screening programs. Awareness campaigns on hereditary gastrointestinal disorders are boosting early intervention and treatment adoption. Expansion of hospitals, specialty clinics, and homecare support services is increasing therapy accessibility. The region is witnessing growing investments in both generic and branded therapeutic options. Improved healthcare infrastructure and patient education further accelerate market growth.

Japan Familial Adenomatous Polyposis Treatment Market Insight

The Japan familial adenomatous polyposis treatment market is gaining momentum due to high public awareness of hereditary colorectal diseases, widespread genetic testing programs, and well-developed healthcare infrastructure. Hospitals and specialty clinics provide comprehensive FAP management, integrating nutritional support and enzyme replacement therapy. Preventive care initiatives and national health guidelines emphasize early diagnosis and long-term monitoring. Collaboration between research institutions and pharmaceutical companies fosters innovation in treatment options. Patient-focused programs ensure increased therapy adherence and improved outcomes. Government initiatives supporting specialized gastrointestinal care further stimulate market expansion.

China Familial Adenomatous Polyposis Treatment Market Insight

The China familial adenomatous polyposis treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by rapid urbanization, growing awareness of hereditary gastrointestinal disorders, and increasing accessibility to healthcare services. Expanding hospitals, diagnostic centers, and specialty clinics are improving patient reach. National genetic screening programs are promoting early detection and therapy initiation. The market benefits from the availability of both affordable generic therapies and branded treatment options. Rising disposable incomes and healthcare spending contribute to increasing adoption rates. Collaboration between domestic pharmaceutical firms and research institutes fosters continuous improvement in treatment efficacy.

Familial Adenomatous Polyposis Treatment Market Share

The familial adenomatous polyposis treatment industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Viatris Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- Merck & Co., Inc. (U.S.)

- AstraZeneca (U.K.)

- Bristol Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Lilly USA, LLC (U.S.)

- Johnson & Johnson and its affiliates (U.S.)

- Sanofi (France)

- GSK plc (U.K.)

- Amgen Inc. (U.S.)

- Celgene Corporation (U.S.)

- Biogen Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

- Eisai Co., Ltd. (Japan)

Latest Developments in Global Familial Adenomatous Polyposis Treatment Market

- In May 2025, Recursion Pharmaceuticals announced preliminary Phase 1b/2 data for REC-4881, a MEK1/2 inhibitor, in the treatment of FAP. The open-label study demonstrated a median 43% reduction in polyp burden at the Week 13 assessment among six patients. This is notable as FAP, a rare genetic disorder causing numerous gastrointestinal polyps and a high risk of colorectal cancer, currently lacks FDA-approved treatments

- In February 2025, Biodexa Pharmaceuticals received Fast Track designation from the U.S. FDA for eRapa, an encapsulated form of rapamycin, for the treatment of FAP. This designation aims to expedite the development and review of drugs that treat serious conditions and fill an unmet medical need

- In April 2025, researchers at the University of Bonn discovered a mechanism in the local immune system that can drive the development of duodenal cancer in FAP patients. This finding offers a promising new approach to preventing duodenal carcinoma in individuals with FAP

- In June 2025, a comprehensive review published in Familial Cancer explored non-surgical management strategies for large bowel disease in FAP patients. The review emphasized the role of endoscopic interventions and chemoprevention as viable alternatives to traditional surgical approaches, offering patients less invasive options for managing the disease

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.