Global Faucets Market

Market Size in USD Billion

USD

7.69 Billion

USD

15.20 Billion

2025

2033

USD

7.69 Billion

USD

15.20 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.69 Billion | |

| USD 15.20 Billion | |

| % | |

|

Global Faucets Market Overview

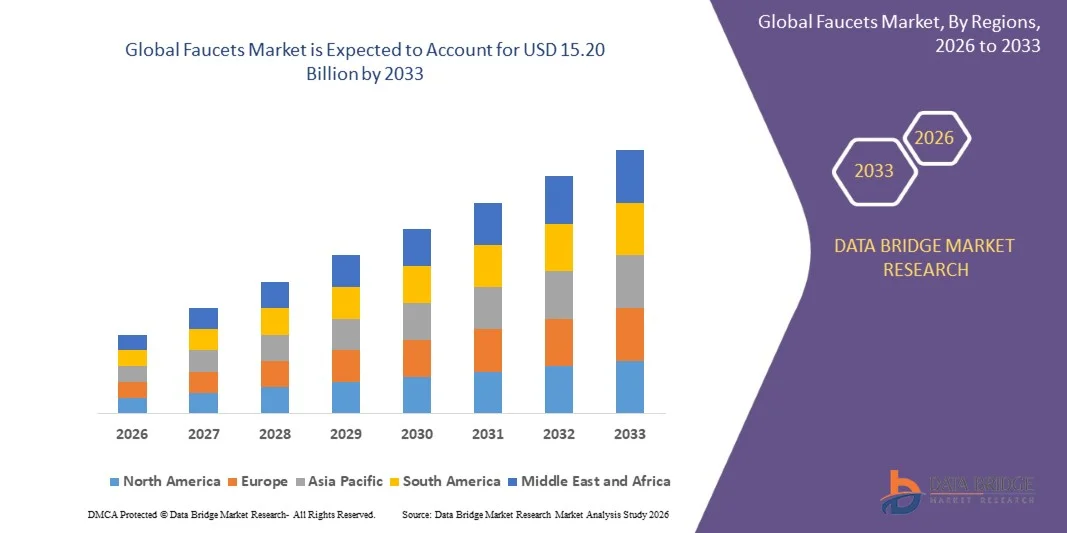

The global faucets market was valued at USD 7.69 billion in 2025 and is projected to reach USD 15.20 billion by 2033, growing at a CAGR of 8.90% from 2026 to 2033. The market is witnessing robust and sustained growth driven by rising global construction and renovation activity, growing consumer demand for premium and technologically advanced faucet solutions, and increasing adoption of water-efficient and touchless faucet technologies across residential and commercial end-use segments. Rapid urbanization, expanding real estate development, and rising consumer spending on home improvement and interior aesthetics are significantly accelerating demand for innovative and design-forward faucet products globally.

The accelerating adoption of smart home technologies and IoT-enabled plumbing fixtures is driving significant innovation in electronic faucet designs, with sensor-activated, voice-controlled, and app-integrated faucet systems gaining strong consumer traction across premium residential and commercial hospitality segments. Growing regulatory emphasis on water conservation through mandatory low-flow fixture standards in key markets including the United States, European Union, and Australia is further incentivizing the transition toward advanced water-saving faucet technologies. In addition, the rising popularity of kitchen and bathroom renovation projects, growing hospitality and commercial construction activity, and increasing preference for customized and aesthetically differentiated faucet designs are collectively broadening the addressable market for premium and specialty faucet product solutions.

Key Market Trends & Insights

- Asia-Pacific dominated the faucets market with the largest revenue share of approximately 38.7% in 2025, supported by rapid urbanization, massive residential and commercial construction activity across China, India, and Southeast Asia, rising consumer disposable incomes enabling premium fixture adoption, and strong manufacturing presence of leading faucet producers in the region. Expanding government investment in urban housing development and sanitation infrastructure modernization programs further consolidates Asia-Pacific's regional market leadership.

- North America is expected to be the fastest-growing region, recording a CAGR of approximately 9.8% from 2026 to 2033. Growth is driven by accelerating adoption of smart and touchless electronic faucet technologies in residential renovation and commercial construction projects, strong consumer spending on premium bathroom and kitchen fixtures, and tightening water efficiency regulations driving upgrade cycles toward water-saving certified faucet products across the region.

- The Electronic product type segment is projected to register the fastest growth at a CAGR of around 11.4% from 2026 to 2033, driven by rising consumer adoption of sensor-activated and touchless faucet technologies in both residential and commercial applications, growing smart home integration trends, and increasing demand from healthcare, hospitality, and commercial building operators for hygienic, contactless water dispensing solutions.

- The Manual product type segment held the largest market revenue share of approximately 73.6% in 2025, reflecting the dominant installed base of conventional manual faucet products across residential and commercial segments globally and the continued preference for reliable, cost-effective manual faucet solutions in price-sensitive residential and developing market applications.

- The One-Hand Mixer type segment held the largest market revenue share of approximately 52.3% in 2025, driven by widespread consumer preference for single-lever faucets offering convenient water temperature and flow control in both kitchen and bathroom applications, combined with strong penetration in mid-to-premium residential renovation and new construction projects globally.

- The Two-Hand Mixer type segment is expected to maintain steady demand, particularly in traditional residential markets and commercial applications requiring precise independent hot and cold water control, supported by strong preference for classic dual-handle faucet aesthetics in heritage and luxury interior design applications.

- The Metal materials segment held the largest market revenue share of approximately 78.4% in 2025, driven by the widespread use of brass, stainless steel, zinc alloy, and copper as primary faucet body materials offering superior corrosion resistance, durability, aesthetic versatility, and compatibility with high-pressure plumbing systems across residential and commercial applications globally.

- The Plastics (PTMT) materials segment is expected to register the fastest growth at a CAGR of around 10.6% from 2026 to 2033, driven by increasing adoption of Poly Tetra Methylene Terephthalate (PTMT) faucets in price-sensitive residential markets, growing preference for corrosion-free and lightweight fixture alternatives, and expanding distribution of PTMT faucet products through organized retail and e-commerce channels in emerging economies.

- The Ceramic Disc technology segment held the largest market revenue share of approximately 38.2% in 2025, driven by the superior durability, leak resistance, precise flow control, and low maintenance requirements of ceramic disc valve technology, making it the preferred cartridge solution for premium residential and commercial faucet applications globally.

- The Cartridge technology segment is expected to register the fastest growth at a CAGR of around 9.4% from 2026 to 2033, supported by widespread adoption in mid-range residential faucet products, ease of cartridge replacement enabling extended product lifecycle, and growing preference among plumbing professionals for cartridge-based faucet systems due to simplified maintenance and repair characteristics.

- The Bathroom application segment held the largest market revenue share of approximately 54.8% in 2025, driven by the higher volume of faucet installations per household in bathroom settings, strong consumer investment in bathroom renovation and premium fixture upgrades, and expanding demand for designer and spa-inspired bathroom faucet collections across residential and hospitality commercial segments.

- The Kitchen application segment is expected to register the fastest growth at a CAGR of around 9.7% from 2026 to 2033, driven by rising consumer demand for multifunctional kitchen faucets with pull-down sprayers, touchless activation, and integrated filtration features, combined with strong kitchen renovation activity and growing popularity of open-plan kitchen design trends across premium residential markets.

- The Offline distribution channel held the largest market revenue share of approximately 67.3% in 2025, driven by the dominant role of plumbing supply stores, home improvement retailers, and sanitary ware showrooms in faucet product discovery, specification, and purchase across residential renovation and commercial construction project procurement processes.

- The Online distribution channel is expected to register the fastest growth at a CAGR of around 12.1% from 2026 to 2033, driven by the rapid expansion of e-commerce home improvement retail, growing consumer comfort with online plumbing fixture purchasing, increasing availability of detailed product specifications and customer reviews facilitating informed online purchase decisions, and competitive pricing advantages offered by digital retail channels.

- The Residential end-user segment held the largest market revenue share of approximately 61.4% in 2025, reflecting strong baseline demand from new residential construction, home renovation activity, and replacement purchases across global housing markets, with growing consumer interest in premium and designer faucet products further supporting segment value growth.

- The Commercial end-user segment is expected to register the fastest growth at a CAGR of around 10.2% from 2026 to 2033, driven by expanding commercial construction activity across hospitality, healthcare, office, and retail sectors, growing adoption of touchless and water-efficient commercial faucet technologies, and increasing specification of premium designer faucet products in luxury hotel, restaurant, and commercial office fitout projects globally.

Market Size & Forecast

- Global Market Value (2025): USD 7.69 Billion

- Expected Market Value (2033): USD 15.20 Billion

- Forecast CAGR (2026–2033): 8.90%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Faucets Market Segmentation

|

Attributes |

Faucets Key Market Insights |

|

Segments Covered |

• By Product Type: Electronic and Manual • By Type: One-Hand Mixer, Two-Hand Mixer, and Others • By Materials: Metal and Plastics (PTMT) • By Technology: Cartridge, Compression, Ceramic Disc, and Ball • By Application: Bathroom, Kitchen, and Others • By Distribution Channel: Online and Offline • By End-User: Residential and Commercial |

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Masco Corporation (U.S.) |

|

Market Opportunities |

• Accelerating Adoption of Smart and Touchless Electronic Faucet Technologies in Residential and Commercial Construction and Renovation Projects • Expanding E-Commerce Distribution Enabling Premium Faucet Brand Penetration in Underserved Residential and Emerging Market Geographies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Faucets Market Trends

Trend: Rising Smart Home Integration and Growing Consumer Demand for Touchless and Water-Efficient Faucet Technologies

The accelerating global adoption of smart home systems and connected home technologies is fundamentally transforming consumer expectations for bathroom and kitchen fixtures, driving a structural shift toward electronically controlled, sensor-activated, and IoT-integrated faucet solutions across premium residential and commercial end-use segments. Smart faucet technologies offering voice-activated water dispensing, precise temperature and flow digital control, water usage monitoring, and smartphone application integration are gaining significant consumer traction as part of broader connected home ecosystem investments.

Leading faucet manufacturers including Moen, Kohler, and Delta Faucet have significantly expanded their smart faucet product portfolios, incorporating Amazon Alexa and Google Assistant voice control compatibility, precision digital temperature setting, and automatic shut-off features designed to address both convenience preferences and water conservation objectives. For instance, Moen's Smart Faucet series and Kohler's Sensate touchless kitchen faucet line have demonstrated strong commercial performance in premium residential renovation markets, with consumer satisfaction ratings reflecting high adoption rates of touchless activation features driven by hygiene awareness trends accelerated by the global pandemic period.

Water conservation regulation is also playing an increasingly significant role in driving technology adoption across the faucets market. Mandatory WaterSense certification requirements in the United States, WELS water efficiency standards in Australia, and Waterwise labeling programs in the United Kingdom are compelling faucet manufacturers to develop products meeting progressively stricter flow rate limitations while maintaining acceptable consumer performance experience. Industry data from 2024 indicates that WaterSense-certified faucets account for over 45% of total U.S. residential faucet sales, reflecting the substantial market penetration of water efficiency standards and the growing consumer acceptance of low-flow faucet technologies.

Global Faucets Market Dynamics

Key Market Driver: Rising Global Construction Activity and Home Renovation Spending Driving Faucet Demand

The sustained global expansion of residential and commercial construction activity, combined with accelerating home improvement and renovation spending across major developed and developing markets, is generating strong and diversified demand for faucet products across all product type, application, and end-user segments. Growing urban populations, rising homeownership rates in emerging economies, and government-backed affordable housing development programs are collectively driving new construction faucet demand across Asia-Pacific, the Middle East, and Latin America.

Home renovation and remodeling activity has emerged as an increasingly significant driver of faucet market growth across North America and Europe, with kitchen and bathroom renovation projects consistently ranking among the highest-value home improvement categories by consumer expenditure. The growing availability of premium and designer faucet products through home improvement retail chains and specialized sanitary ware showrooms, combined with the expansion of e-commerce distribution enabling broader consumer access to premium brand products, is further stimulating upgrade purchases and trading-up behavior among residential consumers seeking to enhance bathroom and kitchen aesthetics.

Construction industry data from 2024 indicates that global residential construction spending exceeded USD 6.5 trillion annually, with sanitary fittings and plumbing fixture specification representing a consistent and recurring component of both new build and renovation project budgets. The increasing prevalence of open-plan kitchen and bathroom design trends favoring statement fixture investments, combined with growing interior design media influence through social platforms promoting aspirational premium faucet aesthetics, is further supporting above-average market growth rates in premium faucet product categories globally.

Key Restraint/Challenge: Intense Price Competition and Raw Material Cost Volatility

The faucets market faces significant competitive intensity challenges driven by the presence of a large number of domestic and international manufacturers across diverse price tiers, creating substantial pricing pressure particularly in mid-range and value residential faucet product segments. The fragmented competitive landscape in key emerging markets including China, India, and Southeast Asia, characterized by numerous local manufacturers competing primarily on price, is creating margin pressure for branded international faucet players and limiting premium pricing power in volume market segments.

In addition, price volatility in key raw materials including brass, copper, zinc alloy, and stainless steel significantly impacts faucet manufacturing costs and margin management for producers across market tiers. Commodity price fluctuations driven by global metal market dynamics, energy cost increases affecting smelting and manufacturing operations, and supply chain disruptions can create meaningful input cost pressures that are difficult to pass through fully to price-sensitive consumer and construction industry buyers, particularly in competitive tender-based commercial procurement processes.

Industry assessments indicate that raw material costs, primarily metals, typically represent 35–55% of total faucet manufacturing cost depending on product type and quality tier, making commodity price management a critical operational priority for faucet manufacturers. Growing environmental regulations governing metal processing and surface finishing operations, including restrictions on lead content in potable water contact surfaces and hexavalent chromium plating processes, are also increasing compliance costs and product reformulation investment requirements for faucet manufacturers serving international regulatory markets.

Key Market Opportunity: Expanding Smart Faucet and Water Conservation Technology Adoption in Commercial and Hospitality Segments

The rapid expansion of smart building technology adoption across commercial real estate, healthcare facilities, luxury hospitality, and corporate office sectors is creating significant premium market opportunities for electronic and sensor-activated faucet system suppliers. Commercial building operators and facility managers are increasingly prioritizing touchless faucet installations for hygiene assurance, water consumption reduction, and building management system integration, creating strong and recurring demand for advanced electronic faucet products in commercial construction and renovation projects.

The global luxury hospitality sector represents a particularly high-value growth opportunity for premium electronic and designer faucet manufacturers, with major hotel brands investing substantially in bathroom and kitchen fixture quality as a key brand differentiation and guest experience investment. In 2025, several major international hotel chains including Marriott and Hilton announced bathroom renovation programs prioritizing smart faucet and water efficiency fixture upgrades across portfolio properties, creating significant commercial procurement opportunities for premium faucet suppliers with established hospitality sector distribution and specification relationships. Industry projections indicate that the commercial smart faucet segment could represent a USD 2.8 billion market opportunity by 2033, driven by expanding building automation integration and growing institutional emphasis on water conservation performance metrics.

Global Faucets Market Scope

The global faucets market is segmented on the basis of product type, type, materials, technology, application, distribution channel, and end-user.

• By Product Type

On the basis of product type, the faucets market is segmented into Electronic and Manual. The Manual segment held the largest market revenue share of approximately 73.6% in 2025, reflecting the dominant installed base and continued preference for conventional manual faucet products across residential and commercial segments globally. Cost-effectiveness, reliability, and compatibility with existing plumbing infrastructure continue to support broad market penetration of manual faucet products across all geographic markets and end-user segments.

The Electronic segment is projected to register the fastest growth at a CAGR of around 11.4% from 2026 to 2033, driven by rising consumer adoption of sensor-activated and touchless faucet technologies in residential and commercial applications, growing smart home integration trends, increasing demand from healthcare and hospitality operators for hygienic touchless water dispensing solutions, and expanding IoT-enabled faucet product availability across premium retail and e-commerce distribution channels.

• By Type

On the basis of type, the market is segmented into One-Hand Mixer, Two-Hand Mixer, and Others. The One-Hand Mixer segment held the largest market revenue share of approximately 52.3% in 2025, driven by widespread consumer preference for single-lever faucet convenience, strong penetration in mid-to-premium residential renovation and new construction projects, and the versatile design compatibility of single-handle faucet styles with both contemporary and transitional interior design trends.

The Two-Hand Mixer segment maintains steady demand across traditional residential markets and commercial applications, supported by strong preference for classic dual-handle aesthetics in heritage, traditional, and luxury residential interior design applications, and practical demand for precise independent hot and cold water control in specific commercial plumbing applications requiring temperature segregation.

• By Materials

On the basis of materials, the market is segmented into Metal and Plastics (PTMT). The Metal segment held the largest market revenue share of approximately 78.4% in 2025, driven by the widespread use of brass, stainless steel, zinc alloy, and copper as primary faucet body and component materials offering superior corrosion resistance, mechanical durability, premium aesthetic finish options, and regulatory compliance for potable water contact applications across residential and commercial markets globally.

The Plastics (PTMT) segment is expected to register the fastest growth at a CAGR of around 10.6% from 2026 to 2033, driven by increasing adoption of corrosion-free, lightweight, and cost-effective PTMT faucets in price-sensitive residential markets across Asia-Pacific and emerging economies, growing preference for lead-free plumbing alternatives, and expanding organized retail and e-commerce distribution of PTMT faucet products offering attractive price-performance propositions for budget-conscious residential consumers.

• By Technology

On the basis of technology, the market is segmented into Cartridge, Compression, Ceramic Disc, and Ball. The Ceramic Disc segment held the largest market revenue share of approximately 38.2% in 2025, driven by the superior durability, precision flow control, excellent leak resistance, and low long-term maintenance cost of ceramic disc valve technology, making it the preferred valve solution across premium residential and commercial faucet applications globally. The longevity advantage of ceramic disc cartridges supporting extended product service life further reinforces segment leadership in premium market tiers.

The Cartridge segment is expected to register the fastest growth at a CAGR of around 9.4% from 2026 to 2033, supported by widespread adoption in mid-range residential faucet product categories, ease of field replacement enabling extended faucet product lifecycle and reduced replacement costs for consumers and building managers, and growing preference among plumbing contractors and specifiers for cartridge-based faucet systems offering simplified maintenance and broad replacement part availability.

• By Application

On the basis of application, the market is segmented into Bathroom, Kitchen, and Others. The Bathroom segment held the largest market revenue share of approximately 54.8% in 2025, driven by the higher volume of faucet fixture points per household in bathroom applications including basin mixers, bath fillers, and shower valves, combined with strong consumer investment in bathroom renovation as a priority home improvement category and growing demand for designer and spa-inspired bathroom faucet collections across premium residential and hospitality commercial segments.

The Kitchen segment is expected to register the fastest growth at a CAGR of around 9.7% from 2026 to 2033, driven by rising consumer demand for multifunctional kitchen faucets incorporating pull-down sprayer systems, touchless activation, integrated water filtration, and digital temperature control features. Growing popularity of open-plan kitchen design trends prioritizing statement fixture investments and increasing kitchen renovation activity across premium North American and European residential markets are further accelerating premium kitchen faucet category growth.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Online and Offline. The Offline distribution channel held the largest market revenue share of approximately 67.3% in 2025, driven by the dominant role of plumbing supply distributors, home improvement retail chains including Home Depot and Lowe's, and specialized sanitary ware showrooms in faucet product specification, selection, and purchase across residential renovation and commercial construction procurement processes. Professional contractor and plumber purchasing through trade accounts at plumbing supply distributors represents a significant and consistently high-volume component of offline faucet channel sales.

The Online distribution channel is expected to register the fastest growth at a CAGR of around 12.1% from 2026 to 2033, driven by rapid expansion of home improvement e-commerce retail platforms, growing consumer comfort with online plumbing fixture purchasing supported by detailed product specifications, augmented reality visualization tools, and customer review content, and competitive pricing advantages and broader product assortment availability offered by online retail channels versus traditional brick-and-mortar stores.

• By End-User

On the basis of end-user, the market is segmented into Residential and Commercial. The Residential segment held the largest market revenue share of approximately 61.4% in 2025, reflecting strong baseline demand from new residential construction, home renovation activity, and faucet replacement purchases across global housing markets. Growing consumer interest in premium designer faucet products and increasing adoption of smart home compatible electronic faucet systems are supporting above-average value growth in residential segment sales across North American and European markets.

The Commercial segment is expected to register the fastest growth at a CAGR of around 10.2% from 2026 to 2033, driven by expanding commercial construction activity across hospitality, healthcare, office, and retail sectors, growing institutional adoption of touchless and water-efficient commercial faucet technologies driven by hygiene standards and water conservation mandates, and increasing specification of premium designer faucet products in luxury hotel, restaurant, and corporate office fitout projects across globally expanding commercial construction markets.

Global Faucets Market Regional Analysis

Asia-Pacific Faucets Market Insight

Asia-Pacific dominated the faucets market with the largest revenue share of 38.7% in 2025, supported by rapid urbanization, massive residential and commercial construction activity across China, India, and Southeast Asia, rising consumer disposable incomes enabling premium fixture adoption, and a strong regional manufacturing base for both domestic and export-oriented faucet production. The region benefits from government investment in urban housing development, infrastructure modernization, and sanitation improvement programs that are generating substantial new construction faucet demand across residential, commercial, and public sector categories. Growing middle-class consumer aspiration for premium bathroom and kitchen fixtures, combined with expanding organized retail and e-commerce distribution of branded faucet products, is further driving market premiumization.

China Faucets Market Insight

The China faucets market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's massive residential and commercial construction sector, the world's largest real estate development activity, and a rapidly evolving consumer preference for premium and branded bathroom and kitchen faucet products. China's established position as the world's largest faucet manufacturing and export hub provides strong domestic supply chain depth supporting both domestic market supply and international market competitiveness. Growing consumer adoption of smart home technologies, increasing bathroom and kitchen renovation spending among urban middle-class consumers, and the rapid expansion of e-commerce home improvement retail platforms are significantly driving market value growth and product premiumization across Chinese faucet market segments.

Japan Faucets Market Insight

The Japan faucets market is expected to witness strong growth from 2026 to 2033, driven by increasing demand for technologically advanced and water-efficient bathroom and kitchen fixtures, rising renovation activities in urban residential buildings, and strong consumer preference for premium-quality sanitary products. The country’s emphasis on smart home integration and hygiene-focused living standards is accelerating adoption of sensor-based, touchless, and temperature-controlled faucet systems across residential, commercial, and hospitality sectors. In addition, Japan’s aging population is increasing demand for user-friendly and ergonomic faucet designs, while the expansion of high-end housing projects and sustainable building infrastructure continues to support market growth across major metropolitan areas.

North America Faucets Market Insight

North America is expected to be the fastest-growing region in the global faucets market, recording a CAGR of approximately 9.8% from 2026 to 2033, driven by accelerating adoption of smart and touchless electronic faucet technologies in residential renovation and commercial construction projects, strong consumer spending on premium kitchen and bathroom fixture upgrades, and tightening WaterSense and state-level water efficiency regulations driving replacement purchase cycles toward certified water-saving faucet products. The region benefits from a highly developed home improvement retail infrastructure, strong contractor and plumber distribution networks, and active consumer renovation spending supported by solid residential real estate market fundamentals.

U.S. Faucets Market Insight

The U.S. faucets market captured the largest revenue share in North America in 2025, driven by the country's large residential housing stock generating strong replacement and renovation demand, high consumer spending on home improvement projects, and the presence of leading global faucet brands including Moen, Kohler, and Delta Faucet Company with well-established retail distribution and professional contractor relationships. Growing consumer adoption of smart and touchless kitchen and bathroom faucet technologies, supported by strong brand marketing investment and expanding product portfolio development, is further driving premium segment market value growth. The U.S. Environmental Protection Agency's WaterSense program continues to accelerate adoption of water-efficient faucet products across both residential and commercial market segments.

Canada Faucets Market Insight

The Canada faucets market is expected to witness steady growth from 2026 to 2033, driven by increasing residential renovation activities, rising adoption of smart and water-efficient plumbing fixtures, and growing consumer preference for premium kitchen and bathroom interiors. Government regulations promoting water conservation and sustainable building standards are encouraging the installation of low-flow and sensor-based faucet systems across residential and commercial properties. In addition, expanding urban housing developments, rising disposable incomes, and strong demand for modern home improvement products are supporting market expansion. The growing presence of organized retail channels and e-commerce platforms is further improving accessibility to branded faucet products across both metropolitan and suburban regions in Canada

Europe Faucets Market Insight

The Europe faucets market is expected to witness steady growth from 2026 to 2033, driven by ongoing bathroom and kitchen renovation activity across mature Western European housing markets, stringent EU water efficiency and lead-free material regulations driving product upgrade and replacement cycles, and strong consumer preference for premium designer faucet products from established European brands including Hansgrohe, Grohe, and Dornbracht. The region benefits from sophisticated consumer demand for design-led faucet aesthetics, strong specification culture in commercial and institutional construction projects, and growing adoption of water-efficient faucet technologies driven by water scarcity concerns and environmental sustainability commitments across national and European regulatory frameworks.

U.K. Faucets Market Insight

The U.K. faucets market is expected to witness steady growth from 2026 to 2033, driven by ongoing residential renovation activity in a mature housing stock with significant fixture replacement and upgrade demand, growing consumer preference for premium bathroom and kitchen faucet designs, and increasing adoption of water-efficient faucet products supported by WRAS approval requirements and Waterwise water efficiency labeling programs. The U.K.'s well-developed home improvement retail sector, including B&Q, Screwfix, and specialist bathroom and kitchen showroom networks, provides strong distribution infrastructure for both mainstream and premium faucet product segments.

Germany Faucets Market Insight

The Germany faucets market is expected to witness strong growth from 2026 to 2033, supported by a large and quality-conscious residential renovation market, strong commercial construction activity in the hospitality and office sectors, and the country's position as home to leading global faucet manufacturers including Hansgrohe and Grohe with significant domestic and export market influence. German consumer and commercial specification emphasis on product quality, engineering precision, water efficiency, and design innovation supports above-average market penetration of premium faucet product categories. Growing adoption of touchless commercial faucet technologies in German healthcare, corporate, and hospitality facility construction and renovation projects is further expanding premium electronic faucet market opportunity.

Global Faucets Market Share

The Faucets industry is primarily led by well-established companies, including:

- Masco Corporation (U.S.)

- Kohler Co. (U.S.)

- Grohe AG (Germany)

- Moen Incorporated (U.S.)

- Hansgrohe SE (Germany)

- American Standard Brands (U.S.)

- LIXIL Corporation (Japan)

- Roca Sanitario S.A. (Spain)

- Geberit AG (Switzerland)

- Toto Ltd. (Japan)

- Watts Water Technologies Inc. (U.S.)

- Spectrum Brands Holdings Inc. (U.S.)

- Elkay Manufacturing Company (U.S.)

- Jaquar Group (India)

- Hindware Home Innovation Limited (India)

Latest Developments in Global Faucets Market

- In March 2025, Moen Incorporated (U.S.) launched an expanded range of smart kitchen and bathroom faucets integrating enhanced voice control compatibility with Amazon Alexa and Google Assistant, along with a new companion mobile application enabling real-time water usage monitoring, leak detection alerts, and automated shut-off scheduling. The new smart faucet product line targets premium residential renovation and new construction markets, offering homeowners comprehensive water management visibility and control from connected devices, supporting both convenience enhancement and household water conservation objectives.

- In January 2025, Kohler Co. (U.S.) announced the introduction of its next-generation Sensate touchless kitchen faucet series featuring an advanced sensor activation system with extended detection range, improved response time, and integrated response-pause technology preventing unintended activation during food preparation activities. The updated Sensate series incorporates a new precision spray technology delivering enhanced water flow efficiency performance, achieving WaterSense certification compliance while maintaining consumer-preferred spray pattern strength and coverage, targeting the premium North American kitchen renovation market.

- In November 2024, Hansgrohe SE (Germany) unveiled its new Vivenis faucet collection at ISH 2025, featuring an innovative EcoSmart flow restrictor technology achieving 60% water savings compared to conventional faucet flow rates without perceptible reduction in consumer-experienced water pressure performance. The Vivenis collection incorporates Hansgrohe's CoolStart technology ensuring the mixer defaults to cold water positioning to prevent unnecessary water heater activation, contributing to both water and energy conservation performance in residential bathroom applications.

- In September 2024, LIXIL Corporation (Japan) announced a strategic expansion of its American Standard brand commercial faucet portfolio across Southeast Asian markets, introducing a new range of sensor-activated commercial basin faucets specifically designed for healthcare, hospitality, and corporate office building applications. The commercial touchless faucet series incorporates infrared sensor technology with adjustable detection sensitivity, battery or AC power supply flexibility, and antimicrobial surface treatment, targeting growing commercial construction faucet specification demand across rapidly developing Southeast Asian markets.

- In July 2024, Jaquar Group (India) announced a significant capital investment in expanding its faucet manufacturing facility in Rajasthan, India, adding automated cartridge assembly and precision chrome plating production lines to increase manufacturing capacity and improve quality consistency across its mid-range and premium faucet product ranges. The expansion also includes a new product innovation center dedicated to smart faucet technology development, reflecting Jaquar's strategic commitment to developing IoT-enabled faucet products targeting the rapidly growing premium Indian residential and commercial construction market segments.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.