Global Fcrn Antagonist Autoimmune Therapy Market

Market Size in USD Billion

USD

1.86 Billion

USD

6.71 Billion

2025

2033

USD

1.86 Billion

USD

6.71 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.86 Billion | |

| USD 6.71 Billion | |

| % | |

|

FcRn Antagonist Autoimmune Therapy Market Overview

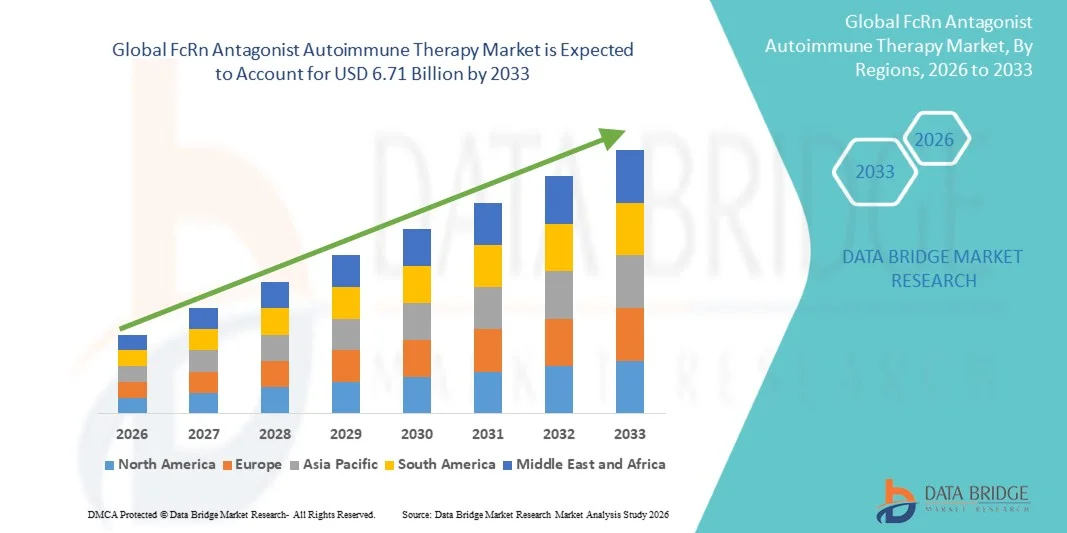

The FcRn Antagonist Autoimmune Therapy Market was valued at USD 1.86 billion in 2025 and is projected to reach USD 6.71 billion by 2033, growing at a CAGR of 17.40% from 2026 to 2033. The market is witnessing strong expansion driven by increasing prevalence of IgG-mediated autoimmune diseases, rising adoption of targeted biologic therapies, and rapid progress in FcRn-blocking drug development pipelines.

The growing burden of autoimmune conditions such as myasthenia gravis, immune thrombocytopenia, and chronic inflammatory demyelinating polyneuropathy, along with limited long-term treatment options in conventional immunosuppressants, is accelerating demand for FcRn antagonist therapies. These drugs offer a novel mechanism of action by reducing pathogenic IgG antibodies, enabling more precise and durable disease control. Additionally, increasing regulatory approvals and expanding clinical trial activity across monoclonal antibodies and next-generation FcRn inhibitors are further supporting market growth across hospitals and specialty care settings globally.

Key Market Trends & Insights

- North America dominated the FcRn Antagonist Autoimmune Therapy Market with the largest revenue share of 42.6% in 2025, supported by early biologics adoption, strong clinical pipeline activity, and high prevalence of autoimmune disorders.

- The Monoclonal anti-FcRn antibodies segment led the market with a 46.3% share in 2025, driven by strong clinical validation, robust efficacy in IgG reduction, and multiple regulatory approvals across major autoimmune indications.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by rising autoimmune disease diagnosis rates, improving biologics access, and expanding healthcare infrastructure in China, India, and Japan.

- Next-generation FcRn antagonists are the fastest-growing drug type, projected to register a CAGR of 10.4%, reflecting the surge in innovation in bispecific antibodies and engineered biologics with improved durability and selectivity.

- The Myasthenia Gravis segment dominated the indication category with a 34.8% revenue share in 2025, led by high clinical success rates of FcRn inhibitors and strong unmet need for targeted therapies.

- Intravenous (IV) accounted for 61.2% of the market, preferred by most first-generation FcRn therapies are administered in hospital or specialty clinic settings.

- The Subcutaneous (SC) segment is the fastest-growing route of administration category, with a CAGR of 11.3%, driven by the shift toward patient-centric and home-based treatment models.

Market Size & Forecast

- Global Market Value (2025): USD 1.86 Billion

- Expected Market Value (2033): USD 6.71 Billion

- Forecast CAGR (2026–2033): 17.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and FcRn Antagonist Autoimmune Therapy Market Segmentation

|

Attributes |

FcRn Antagonist Autoimmune Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· argenx (Belgium) · UCB S.A. (Belgium) · Johnson & Johnson Services, Inc. (U.S.) · Immunovant, Inc. (U.S.) · Roivant Sciences Ltd. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Genentech, Inc. (U.S.) · Novartis AG (Switzerland) · Sanofi (France) · Pfizer Inc. (U.S.) · AstraZeneca plc (U.K.) · Bristol Myers Squibb Company (U.S.) · Eli Lilly and Company (U.S.) · AbbVie Inc. (U.S.) · Biogen Inc. (U.S.) · Amgen Inc. (U.S.) · Zai Lab Limited (China) · HanAll Biopharma Co., Ltd. (South Korea) · Otsuka Pharmaceutical Co., Ltd. (Japan) · Kyowa Kirin Co., Ltd. (Japan) |

|

Market Opportunities |

· Expansion of FcRn antagonists into broader autoimmune indications beyond neuromuscular diseases · Growing shift toward subcutaneous self-administration therapies · Rapid advancement of next-generation FcRn bispecific antibodies and combination biologics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

FcRn Antagonist Autoimmune Therapy Market Trends

Trend: Expansion Across Multiple Autoimmune Indications

FcRn antagonist therapies are increasingly being evaluated and adopted beyond myasthenia gravis into broader IgG-mediated autoimmune diseases such as immune thrombocytopenia, lupus nephritis, and pemphigus vulgaris. The ability of these therapies to selectively reduce pathogenic IgG without broad immunosuppression is driving their use across multiple specialty care areas. This expansion is supported by strong late-stage clinical trials and regulatory approvals, while combination strategies with existing immunotherapies are improving long-term disease control outcomes. For instance, ongoing studies in systemic lupus erythematosus and dermatological autoimmune disorders are accelerating pipeline diversification and commercial adoption.

FcRn Antagonist Autoimmune Therapy Market Dynamics

Key Market Driver: Rising Demand for Targeted Immunoglobulin Reduction Therapies

The increasing prevalence of chronic autoimmune diseases and limitations of conventional immunosuppressants are driving strong demand for FcRn antagonist therapies that directly reduce circulating IgG antibodies. These therapies provide rapid and reversible disease control, improving patient outcomes in conditions with high relapse rates and treatment resistance. Biopharmaceutical companies and healthcare providers are increasingly adopting FcRn inhibitors as part of advanced biologic treatment regimens in hospital and specialty care settings. For instance, approvals of efgartigimod and rozanolixizumab have significantly expanded clinical adoption across neurology and immunology practices.

Key Restraint/Challenge: High Cost and Limited Patient Accessibility

A major challenge in the FcRn antagonist autoimmune therapy market is the high cost of biologic development and treatment, which limits accessibility in price-sensitive and developing healthcare systems. Complex manufacturing processes, frequent dosing requirements, and specialist administration in early-stage therapies increase overall treatment burden. Reimbursement limitations and unequal biologics infrastructure further restrict widespread adoption in emerging regions. For instance, access disparities in autoimmune biologic therapies across low- and middle-income countries continue to slow global penetration despite growing disease prevalence.

Key Market Opportunity: Expansion of Next-Generation FcRn Inhibitors and Combination Therapies

The development of next-generation FcRn antagonists, including bispecific antibodies and extended half-life molecules, presents significant growth opportunities in the autoimmune therapy landscape. These innovations aim to improve efficacy, reduce dosing frequency, and enhance patient convenience compared to first-generation biologics. Increasing research into combination therapies with B-cell targeted agents is also expanding clinical utility across refractory autoimmune conditions. For instance, pipeline programs exploring FcRn inhibitors in combination with complement inhibitors are strengthening long-term disease management strategies and market expansion potential.

FcRn Antagonist Autoimmune Therapy Market Scope

The FcRn antagonist autoimmune therapy market is segmented on the basis of drug type, indication, route of administration, and end user.

- By Drug Type

On the basis of drug type, the FcRn Antagonist Autoimmune Therapy Market is segmented into Fc fragment–based inhibitors, monoclonal anti-FcRn antibodies, next-generation FcRn antagonists, and emerging biologics. The Monoclonal anti-FcRn antibodies segment dominated the market with a 46.3% share in 2025, owing to strong clinical validation, robust efficacy in IgG reduction, and multiple regulatory approvals across major autoimmune indications. These therapies have become the backbone of FcRn-targeted treatment due to their predictable pharmacokinetics and established safety profiles. They are widely adopted in hospital-based specialty care for conditions such as myasthenia gravis and immune thrombocytopenia. Strong pipeline expansion and physician familiarity further reinforce their leadership position. Continuous clinical trial success across neurology and hematology indications is expanding their therapeutic footprint. High investment from biopharmaceutical companies continues to strengthen this segment’s dominance.

The Next-generation FcRn antagonists segment is expected to be the fastest-growing with a CAGR of 10.4% from 2026 to 2033, driven by innovation in bispecific antibodies and engineered biologics with improved durability and selectivity. These therapies aim to reduce dosing frequency and enhance long-term disease control compared to first-generation molecules. Increasing focus on combination therapies with B-cell and complement inhibitors is further expanding clinical potential. Rapid advancements in biologic engineering are improving safety and efficacy profiles. Expanding pipeline candidates across late-stage clinical trials are accelerating commercialization prospects. Rising demand for differentiated biologics in refractory autoimmune conditions is boosting adoption. Strong R&D investments from leading biotech firms are supporting rapid market growth.

- By Indication

On the basis of indication, the market is segmented into myasthenia gravis, immune thrombocytopenia, chronic inflammatory demyelinating polyneuropathy, warm autoimmune hemolytic anemia, pemphigus vulgaris, systemic lupus erythematosus, and other autoimmune disorders. The Myasthenia Gravis (gMG) segment dominated the market with a 34.8% share in 2025, due to high clinical success rates of FcRn inhibitors and strong unmet need for targeted therapies. Patients with gMG benefit significantly from rapid IgG reduction, leading to improved muscle strength and reduced relapse frequency. Strong regulatory approvals and early adoption in neurology clinics are reinforcing dominance. Expanding awareness and diagnosis rates are increasing patient pool size. Continuous clinical trial expansion is further strengthening therapeutic adoption. Hospital-based infusion therapy availability is also supporting segment leadership.

The Systemic Lupus Erythematosus (SLE) segment is expected to be the fastest-growing with a CAGR of 9.6% from 2026 to 2033, driven by high disease complexity and limited effectiveness of conventional therapies. FcRn antagonists are gaining attention for their ability to reduce autoantibody levels without broad immune suppression. Increasing clinical pipeline activity is expanding treatment potential across lupus nephritis and systemic manifestations. Rising prevalence of autoimmune disorders in younger populations is further supporting demand. Biopharma companies are increasingly investing in late-stage SLE trials. Growing physician interest in targeted immunotherapy is accelerating adoption. Expanding biologics reimbursement policies are also supporting market growth.

- By Route of Administration

On the basis of route of administration, the market is segmented into intravenous (IV), subcutaneous (SC), and hybrid regimens. The Intravenous (IV) segment dominated the market with a 61.2% share in 2025, as most first-generation FcRn therapies are administered in hospital or specialty clinic settings. IV delivery ensures rapid bioavailability and controlled dosing in acute autoimmune conditions. It is widely preferred for initial induction therapy in severe disease cases. Established hospital infrastructure supports widespread IV administration. Physician familiarity with IV biologics also reinforces dominance. However, treatment logistics and hospital dependency limit long-term convenience. Despite limitations, IV remains the primary mode for approved FcRn therapies.

The Subcutaneous (SC) segment is expected to be the fastest-growing with a CAGR of 11.3% from 2026 to 2033, driven by the shift toward patient-centric and home-based treatment models. SC formulations enable self-administration, reducing hospital burden and improving treatment adherence. Advances in formulation science are enabling higher bioavailability and longer dosing intervals. Growing demand for convenience in chronic autoimmune care is accelerating adoption. Healthcare systems are increasingly supporting outpatient biologic delivery models. Pharmaceutical companies are prioritizing SC pipeline development for competitive advantage. Expanding reimbursement support for home therapies is further boosting growth.

- By End User

On the basis of end user, the market is segmented into hospitals, specialty clinics, ambulatory surgical centers, and academic & research institutes. The Hospitals segment dominated the market with a 52.1% share in 2025, due to high patient inflow for autoimmune disease management and availability of infusion-based biologic administration. Hospitals serve as primary centers for diagnosis, treatment initiation, and monitoring of severe autoimmune conditions. Strong presence of specialist neurologists and immunologists supports adoption. Availability of advanced biologic handling infrastructure reinforces dominance. Hospitals also play a key role in early-stage therapy adoption. Centralized reimbursement systems further strengthen hospital utilization.

The Specialty Clinics segment is expected to be the fastest-growing with a CAGR of 10.1% from 2026 to 2033, driven by increasing shift toward outpatient and long-term autoimmune disease management. These clinics offer focused expertise in neurology and immunology care, improving treatment personalization. Rising preference for decentralized healthcare delivery is supporting growth. Increased adoption of SC therapies is reducing hospital dependency. Expanding network of specialty care centers in emerging markets is further accelerating uptake. Improved patient convenience and reduced treatment costs are key growth drivers. Growing integration of biologic therapy monitoring in outpatient settings is strengthening this segment.

FcRn Antagonist Autoimmune Therapy Market Regional Analysis

North America dominated the FcRn Antagonist Autoimmune Therapy Market with the largest revenue share of 42.6% in 2025, supported by early biologics adoption, strong clinical pipeline activity, and high prevalence of autoimmune disorders. The region benefits from a well-established regulatory pathway supporting rapid drug approvals for monoclonal antibodies and FcRn-targeting therapies. Strong reimbursement frameworks and high healthcare spending further accelerate patient access to premium biologic treatments. Extensive clinical trial activity and strong academic–industry collaboration are also supporting rapid pipeline development. Increasing diagnosis rates of conditions such as myasthenia gravis and immune thrombocytopenia continue to expand the patient pool. Presence of leading biotech companies and specialty care centers further reinforces North America’s market leadership in FcRn antagonist therapies.

U.S. FcRn Antagonist Autoimmune Therapy Market Insight

The U.S. FcRn antagonist autoimmune therapy market is witnessing strong growth due to high prevalence of autoimmune diseases, early adoption of advanced biologics, and robust clinical trial activity for FcRn-targeting therapies. The country’s strong pharmaceutical innovation ecosystem and presence of leading biotech companies are driving rapid commercialization of monoclonal anti-FcRn antibodies. In addition, favorable regulatory pathways and strong reimbursement systems are accelerating patient access to premium therapies across neurology and immunology indications. Increasing adoption in diseases such as myasthenia gravis and immune thrombocytopenia is expanding treatment penetration. Rising investment in precision medicine and targeted immunotherapy is further strengthening market growth. Moreover, growing use of subcutaneous formulations is improving long-term treatment convenience and adherence.

Europe FcRn Antagonist Autoimmune Therapy Market Insight

The Europe FcRn antagonist autoimmune therapy market remains a major contributor to global revenue, driven by strong healthcare systems, increasing biologics adoption, and expanding clinical research in autoimmune disorders. The region benefits from structured regulatory frameworks and rising use of FcRn inhibitors in neurology and dermatology indications. Increasing focus on rare disease management and patient-centric biologic therapies is supporting market expansion. Strong presence of academic–industry collaborations is accelerating innovation in next-generation FcRn antagonists. Growing demand for cost-effective healthcare solutions is encouraging adoption of efficient biologic treatment pathways. In addition, expanding reimbursement support across major European countries is enhancing therapy accessibility.

U.K. FcRn Antagonist Autoimmune Therapy Market Insight

The U.K. FcRn antagonist autoimmune therapy market is experiencing steady growth, supported by rising adoption of advanced biologics in autoimmune disease management and strong clinical research infrastructure. Increasing use of FcRn inhibitors in specialized neurology and immunology centers is driving demand across hospital settings. The country’s emphasis on rare disease diagnosis and early treatment intervention is further supporting market expansion. Growing participation in global clinical trials for FcRn-targeting therapies is enhancing innovation access. Integration of precision medicine approaches is improving treatment outcomes across complex autoimmune conditions. Additionally, strong public healthcare support is facilitating gradual uptake of high-cost biologic therapies.

Germany FcRn Antagonist Autoimmune Therapy Market Insight

The Germany FcRn antagonist autoimmune therapy market is expanding steadily due to its strong pharmaceutical manufacturing base, advanced clinical research ecosystem, and increasing adoption of biologics in autoimmune care. Hospitals and specialty clinics are increasingly utilizing FcRn inhibitors for conditions such as systemic lupus erythematosus and myasthenia gravis. Rising focus on innovation in immunology and antibody engineering is supporting pipeline development. Strong regulatory alignment within the European Union is enabling faster market entry of novel therapies. Growing investment in specialty biologics and rare disease treatment is further strengthening market demand. In addition, Germany’s emphasis on high-quality healthcare delivery is supporting sustained adoption of advanced therapies.

Asia-Pacific FcRn Antagonist Autoimmune Therapy Market Insight

The Asia-Pacific FcRn antagonist autoimmune therapy market is expected to witness rapid growth, driven by increasing autoimmune disease prevalence, improving healthcare infrastructure, and expanding biologics accessibility across emerging economies. Growing awareness of targeted immunotherapies is supporting early diagnosis and treatment adoption in countries such as China, India, and Japan. Rising investments in biotechnology and clinical research are accelerating pipeline development across the region. Increasing availability of specialty care centers is improving patient access to advanced therapies. Expanding government focus on rare and chronic disease management is further supporting market growth. Additionally, cost-sensitive markets are gradually adopting subcutaneous and outpatient biologic treatment models.

Japan FcRn Antagonist Autoimmune Therapy Market Insight

The Japan FcRn antagonist autoimmune therapy market is witnessing consistent growth due to strong emphasis on advanced biomedical research, aging population, and rising autoimmune disease burden. Japanese pharmaceutical companies and research institutes are actively involved in FcRn-targeted drug development and clinical trials. Increasing adoption of biologics in neurology and hematology indications is supporting market penetration. The country’s strong healthcare system enables early diagnosis and treatment initiation. Integration of advanced antibody engineering and precision medicine approaches is further enhancing therapeutic outcomes. Moreover, growing focus on reducing hospital burden is encouraging adoption of subcutaneous biologic therapies.

China FcRn Antagonist Autoimmune Therapy Market Insight

The China FcRn antagonist autoimmune therapy market is growing rapidly, driven by rising autoimmune disease incidence, expanding healthcare infrastructure, and increasing adoption of innovative biologic therapies. Government support for biotechnology development and clinical research is accelerating FcRn inhibitor pipeline advancement. Growing investment from domestic and global pharmaceutical companies is improving market accessibility. Increasing awareness of autoimmune disorders is supporting early diagnosis and treatment adoption. Expansion of specialty hospitals and immunology centers is enhancing biologic therapy delivery. In addition, rising focus on advanced antibody-based therapies is positioning China as one of the fastest-growing markets globally.

FcRn Antagonist Autoimmune Therapy Market Share

The FcRn antagonist autoimmune therapy industry is primarily led by well-established companies, including:

- argenx (Belgium)

- UCB S.A. (Belgium)

- Johnson & Johnson Services, Inc. (U.S.)

- Immunovant, Inc. (U.S.)

- Roivant Sciences Ltd. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Genentech, Inc. (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Bristol Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- AbbVie Inc. (U.S.)

- Biogen Inc. (U.S.)

- Amgen Inc. (U.S.)

- Zai Lab Limited (China)

- HanAll Biopharma Co., Ltd. (South Korea)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Kyowa Kirin Co., Ltd. (Japan)

Latest Developments in FcRn Antagonist Autoimmune Therapy Market

- In April 2025, the FDA approved nipocalimab (Imaavy), developed by Johnson & Johnson, for the treatment of generalized myasthenia gravis. This next-generation FcRn antagonist expanded therapeutic options for a wider patient population, including multiple autoantibody subtypes. The approval marked a significant advancement in FcRn-targeted therapy development, strengthening competition and supporting continued innovation in long-acting and highly selective IgG reduction treatments

- In January 2024, the European Medicines Agency (EMA) granted marketing authorization for Rystiggo (rozanolizumab) for generalized myasthenia gravis, extending its availability across Europe. This approval reinforced the global adoption of FcRn antagonists and supported broader clinical uptake in neurology and rare autoimmune diseases. It also demonstrated growing regulatory confidence in FcRn blockade as a validated and effective therapeutic strategy for IgG-mediated disorders

- In June 2023, the U.S. FDA approved Rystiggo (rozanolizumab), developed by UCB, for the treatment of generalized myasthenia gravis. This approval expanded the FcRn antagonist class with a monoclonal antibody that blocks IgG recycling through FcRn inhibition, providing an additional therapeutic option for patients with antibody-positive gMG. The launch strengthened competition within the FcRn space and further validated FcRn inhibition as an effective treatment approach for autoimmune neuromuscular disorder

- In June 2023, the FDA approved Vyvgart Hytrulo, a subcutaneous formulation of efgartigimod alfa combined with hyaluronidase, developed by argenx. This development marked a major shift from intravenous infusion to a more convenient subcutaneous administration route, significantly improving patient accessibility and enabling potential home-based treatment. It enhanced treatment adherence while reducing hospital dependency, thereby expanding the commercial and clinical reach of FcRn-targeting therapies

- In December 2021, the U.S. FDA approved Vyvgart (efgartigimod alfa), developed by argenx, marking the first FcRn antagonist therapy for generalized myasthenia gravis (gMG). This approval was a landmark event as it introduced a new mechanism of action targeting the neonatal Fc receptor to reduce pathogenic IgG antibodies, establishing FcRn inhibition as a novel therapeutic class in autoimmune disease management. It significantly accelerated global interest in FcRn-based biologics and opened the pathway for further drug development across multiple autoimmune indications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.