Global Fda Cleared Pediatric Wearable Devices Market

Market Size in USD Million

USD

495.00 Million

USD

2,072.30 Million

2024

2032

USD

495.00 Million

USD

2,072.30 Million

2024

2032

| 2025 - 2032 | |

| USD 495.00 Million | |

| USD 2,072.30 Million | |

| % | |

|

FDA-Cleared Pediatric Wearable Devices Market Size

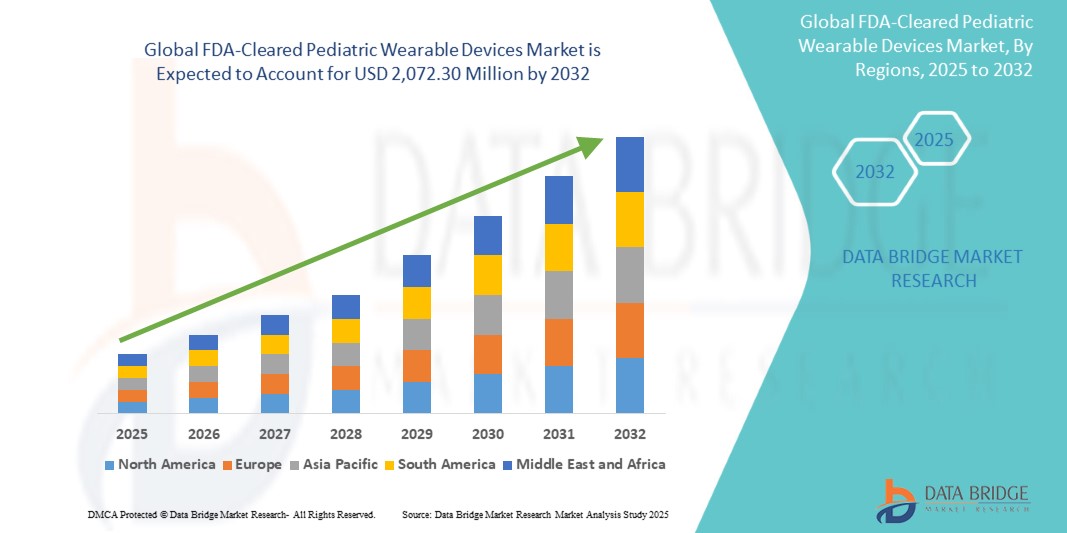

- The global FDA-cleared pediatric wearable devices market size was valued at USD 495.00 million in 2024 and is expected to reach USD 2,072.30 million by 2032, at a CAGR of 19.60% during the forecast period

- The market growth is largely fueled by increasing regulatory approvals of pediatric-focused wearables, alongside advancements in sensor technologies that enable accurate monitoring of vital signs, sleep, and respiratory functions in children

- Furthermore, rising demand from both caregivers and healthcare providers for safe, reliable, and real-time monitoring solutions is positioning FDA-cleared pediatric wearables as an essential tool in pediatric healthcare. These converging factors are accelerating adoption across clinical and homecare settings, thereby significantly boosting the industry’s growth

FDA-Cleared Pediatric Wearable Devices Market Analysis

- Pediatric wearable devices, designed to provide real-time monitoring of vital signs, sleep, respiratory health, and other pediatric conditions, are becoming increasingly vital in both clinical and homecare settings due to their ability to deliver accurate, continuous data and seamless integration with digital health platforms

- The escalating demand for pediatric wearables is primarily fueled by growing regulatory clearances from the FDA, technological advancements in sensors and connectivity, and rising awareness among parents and healthcare providers about the importance of proactive pediatric health monitoring

- North America dominated the pediatric wearable devices market with the largest revenue share of around 39% in 2024, characterized by favorable regulatory frameworks, strong adoption of digital health solutions, and the presence of pioneering players, with the U.S. experiencing substantial uptake in both hospital and homecare environments driven by innovations in infant monitoring and remote patient management

- Asia-Pacific is expected to be the fastest growing region in the pediatric wearable devices market during the forecast period due to rising healthcare expenditure, growing birth rates, and increasing adoption of child health monitoring technologies

- Pulse oximeter devices dominated the pediatric wearable devices market in 2024 with an estimated share of 40% of the market, driven by their critical role in monitoring oxygen saturation and heart rate in neonates and infants, along with expanding FDA clearances that support both prescription and over-the-counter use cases

Report Scope and FDA-Cleared Pediatric Wearable Devices Market Segmentation

|

Attributes |

FDA-Cleared Pediatric Wearable Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

FDA-Cleared Pediatric Wearable Devices Market Trends

Rising Adoption of Real-Time Pediatric Health Monitoring

- A significant and accelerating trend in the global pediatric wearable devices market is the growing integration of FDA-cleared technologies with digital health platforms and connected apps, enhancing real-time pediatric monitoring and caregiver engagement

- For instance, the Owlet Dream Sock received FDA De Novo clearance, enabling parents to monitor infant oxygen levels and heart rate through a connected mobile app, establishing trust in consumer-accessible, medically validated solutions

- FDA-cleared pediatric wearables now feature advanced sensors for continuous SpO₂, ECG, and respiratory monitoring, enabling proactive detection of anomalies and sending intelligent alerts to caregivers and clinicians in real time

- The seamless integration of these devices with telehealth platforms allows healthcare providers to remotely monitor pediatric patients, enabling centralized oversight and reducing the need for frequent hospital visits

- This trend towards clinically validated, digitally integrated wearables is fundamentally reshaping pediatric care delivery. Consequently, companies such as Masimo are developing FDA-cleared pediatric devices such as Stork, designed for both home and clinical use with connected monitoring capabilities

- The demand for pediatric wearables that combine FDA clearance, clinical accuracy, and caregiver convenience is growing rapidly across both hospital and homecare environments, as families and providers increasingly prioritize child safety and proactive health management

FDA-Cleared Pediatric Wearable Devices Market Dynamics

Driver

Growing Demand for Safe and Reliable Pediatric Monitoring Solutions

- The rising prevalence of neonatal and infant health risks, coupled with heightened awareness among caregivers, is a significant driver for the increasing adoption of FDA-cleared pediatric wearables

- For instance, in June 2023, Owlet, Inc. announced FDA clearance for its BabySat device, enabling prescription use for monitoring oxygen saturation in infants, marking a breakthrough in expanding clinical-grade monitoring to the home environment

- As parents and clinicians seek continuous, reliable health data for children, FDA-cleared wearables provide advanced features such as real-time monitoring, historical data tracking, and caregiver alerts, offering a compelling alternative to traditional intermittent monitoring methods

- Furthermore, the growing digital health ecosystem and integration with telemedicine services are making pediatric wearables an integral part of proactive care models, offering seamless connections between caregivers, children, and healthcare providers

- The convenience of home monitoring, reduced hospital dependency, and the ability to share real-time data with clinicians are key factors propelling adoption in both homecare and hospital settings. The trend towards remote patient monitoring programs and supportive regulatory pathways further contributes to market growth

Restraint/Challenge

Skin Sensitivity Issues and Regulatory Compliance Hurdles

- Concerns surrounding potential skin irritation from prolonged device use, especially in neonates and infants, pose a significant challenge to broader market penetration of pediatric wearables

- For instance, clinical reviews have highlighted that continuous use of adhesive-based monitoring patches in children may lead to skin discomfort or allergic reactions, creating hesitancy among parents and caregivers regarding daily adoption

- Addressing these concerns through the use of hypoallergenic materials, improved device ergonomics, and regular safety testing is crucial for building trust. Companies such as Masimo emphasize their pediatric-friendly design and comfort-focused features in their marketing to reassure caregivers

- In addition, the high regulatory standards for pediatric devices and lengthy FDA approval timelines can delay commercialization, creating barriers for smaller innovators in the space. While approvals are accelerating, compliance remains complex and resource-intensive

- The relatively higher cost of FDA-cleared pediatric wearables compared to basic consumer monitors can also hinder adoption among price-sensitive families, particularly in developing regions. Although prices are expected to decline, the perceived premium for clinical-grade devices remains a limiting factor

- Overcoming these challenges through improved pediatric-specific design, faster regulatory pathways, and development of more affordable options will be vital for sustained market growth

FDA-Cleared Pediatric Wearable Devices Market Scope

The market is segmented on the basis of device type, clinical use, technology, and application.

- By Device Type

On the basis of device type, the FDA-cleared pediatric wearable devices market is segmented into pulse oximeters, cardiac monitors/ECG wearables, respiratory monitors, multi-vital monitors, glucose monitoring wearables, and sleep trackers. The pulse oximeter segment dominated the market in 2024 with the largest market revenue share of 40%, driven by its critical role in neonatal and infant health monitoring. Pulse oximeters are widely used to track oxygen saturation and heart rate, parameters vital for detecting respiratory distress and congenital heart issues in pediatric populations. Their dominance is further reinforced by multiple FDA clearances of infant-focused devices such as Owlet BabySat and Masimo Stork, which have gained strong adoption in both clinical and homecare settings. The segment benefits from its non-invasive nature, compact design, and caregiver trust, making it the most widely adopted pediatric wearable type. As more hospitals and homecare users integrate oxygen monitoring into pediatric care protocols, pulse oximeters continue to lead the device type category.

The multi-vital monitors segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by advancements in wearable sensor fusion and growing demand for integrated monitoring solutions. These devices combine multiple parameters—such as SpO₂, heart rate, respiratory rate, and temperature—into a single wearable, providing comprehensive insights into a child’s health. Their ability to reduce the need for multiple devices improves caregiver convenience and enhances adoption in clinical settings, particularly for remote patient monitoring programs. The rising push for connected health and the need for continuous, real-time pediatric data collection are accelerating adoption. In addition, ongoing FDA approvals of multi-vital pediatric platforms are expected to expand clinical acceptance and reimbursement support, making this the fastest-growing device type.

- By Clinical Use

On the basis of clinical use, the FDA-cleared pediatric wearable devices market is segmented into cardiac monitoring, respiratory monitoring, glucose monitoring, temperature monitoring, and SIDS adjunct monitoring. The respiratory monitoring segment dominated the market in 2024, driven by the high prevalence of neonatal respiratory complications and the need for continuous monitoring to detect apnea and other conditions. Pediatric respiratory wearables play a critical role in both NICU settings and at-home monitoring, offering real-time alerts to caregivers and clinicians. Devices that track breathing patterns and oxygen levels are particularly vital for premature infants, where early intervention can be lifesaving. FDA-cleared solutions, such as those designed for infant respiratory surveillance, have cemented this segment’s leading role. Its dominance is also supported by strong clinical validation and widespread adoption in hospital neonatal care units worldwide.

The glucose monitoring segment is projected to grow at the fastest rate during the forecast period, fueled by the rising incidence of pediatric diabetes and increasing FDA approvals of continuous glucose monitoring (CGM) devices for children. CGMs provide real-time glucose readings, alerts for hypoglycemia or hyperglycemia, and integration with insulin delivery systems, making them indispensable for pediatric diabetes management. Parents and clinicians are increasingly adopting CGMs to reduce finger-stick testing and improve quality of life for children with Type 1 diabetes. FDA clearance of devices with pediatric-specific indications is boosting trust and adoption. With strong payer support and expanding clinical guidelines endorsing CGM use in children, this segment is set to grow at the fastest pace.

- By Technology

On the basis of technology, the FDA-cleared pediatric wearable devices market is segmented into optical (PPG), electrical (ECG), accelerometers, and bio-impedance. The optical (PPG) segment dominated the market in 2024, largely because of its use in pulse oximetry and heart rate monitoring for neonates and infants. PPG-based devices are central to most FDA-cleared pediatric wearables, offering non-invasive and continuous measurements of oxygen saturation and heart rate. The technology is well-established, reliable, and widely trusted by both caregivers and clinicians, making it the preferred choice for critical pediatric monitoring. Its dominance is further supported by its integration into leading FDA-approved devices and its role as the foundation for many connected home monitoring solutions. As PPG sensors become smaller and more accurate, they continue to drive the largest share of pediatric wearable adoption.

The bio-impedance segment is anticipated to record the fastest growth from 2025 to 2032, driven by its expanding applications in monitoring hydration, respiratory effort, and sleep quality in pediatric populations. Bio-impedance technology offers insights into multiple physiological functions that go beyond what traditional PPG and ECG sensors provide. The rising research focus on pediatric sleep health and respiratory monitoring is creating opportunities for bio-impedance-based wearables. FDA pathways are increasingly accommodating multi-parametric devices, opening the door for wider regulatory approvals. As these devices transition from research tools to mainstream clinical and consumer use, bio-impedance wearables are expected to see rapid uptake in the pediatric segment.

- By Application

On the basis of application, the FDA-cleared pediatric wearable devices market is segmented into hospitals, homecare/caregivers, and ambulatory/outpatient clinics. The hospital segment dominated the market in 2024, supported by the high demand for continuous monitoring in neonatal intensive care units (NICUs) and pediatric wards. Hospitals rely on FDA-cleared wearables to ensure accuracy, compliance, and integration with broader monitoring systems. The segment’s dominance stems from the critical need for reliable pediatric monitoring solutions in acute care, where timely interventions can significantly impact health outcomes. Hospitals also serve as early adopters of advanced FDA-cleared devices, setting the standard for clinical validation and trust. With strong reimbursement structures and clinical evidence, hospitals maintain the largest revenue share in this category.

The homecare/caregivers segment is expected to grow at the fastest rate during the forecast period, fueled by increasing FDA approvals for over-the-counter (OTC) pediatric wearables and growing caregiver preference for at-home monitoring. Devices such as Owlet Dream Sock and Masimo Stork highlight the shift toward empowering parents with reliable, FDA-cleared monitoring solutions outside the hospital environment. This segment’s growth is further supported by rising awareness of pediatric health risks, higher adoption of telehealth, and the convenience of continuous monitoring at home. As healthcare systems encourage remote patient monitoring to reduce hospital burden, the homecare segment is projected to be the fastest-growing application category.

FDA-Cleared Pediatric Wearable Devices Market Regional Analysis

- North America dominated the FDA-cleared pediatric wearable devices market with the largest revenue share of around 39% in 2024, characterized by favorable regulatory frameworks, strong adoption of digital health solutions, and the presence of pioneering players

- Caregivers and healthcare providers in the region highly value the accuracy, safety, and real-time insights offered by FDA-cleared pediatric wearables, along with their seamless integration into telehealth and remote patient monitoring platforms

- This widespread adoption is further supported by advanced healthcare infrastructure, high awareness of pediatric health monitoring, and favorable reimbursement programs, establishing FDA-cleared pediatric wearables as a trusted solution in both clinical and homecare environments

U.S. FDA-Cleared Pediatric Wearable Devices Market Insight

The U.S. FDA-cleared pediatric wearable devices market captured the largest revenue share of 79% in 2024 within North America, fueled by strong FDA regulatory support and rising parental demand for safe, clinically validated monitoring tools. Caregivers increasingly prioritize continuous monitoring of vital signs, sleep, and chronic conditions through FDA-cleared devices that ensure reliability over consumer-grade wearables. The trend toward telehealth integration, combined with insurance support for remote patient monitoring (RPM), is accelerating adoption. Moreover, strong collaboration between device manufacturers and leading children’s hospitals is further expanding the market footprint.

Europe FDA-Cleared Pediatric Wearable Devices Market Insight

The Europe FDA-cleared pediatric wearable devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing healthcare digitization, strict medical device safety standards, and rising investments in pediatric remote monitoring. Growing awareness among parents regarding sudden infant health risks and the importance of early detection is fueling adoption. The region is witnessing widespread uptake of FDA-cleared devices not only in hospitals but also in homecare settings, with reimbursement policies in certain countries supporting broader access. Pediatric wearables are increasingly integrated into chronic disease management programs, further strengthening market growth.

U.K. FDA-Cleared Pediatric Wearable Devices Market Insight

The U.K. FDA-cleared pediatric wearable devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the adoption of digital health solutions within the NHS and the growing emphasis on child wellness monitoring. Concerns regarding pediatric respiratory and cardiac conditions are encouraging hospitals and parents asuch as to adopt clinically approved devices. The U.K.’s rapid adoption of connected health systems and its strong regulatory alignment with international medical standards further support growth. The expansion of telehealth services and the trend toward home monitoring are expected to remain key growth accelerators.

Germany FDA-Cleared Pediatric Wearable Devices Market Insight

The Germany FDA-cleared pediatric wearable devices market is expected to expand at a considerable CAGR during the forecast period, fueled by strong demand for technologically advanced, clinically reliable monitoring systems. The country’s emphasis on healthcare innovation and digital health integration is driving adoption across both hospitals and homecare environments. German parents and providers value the safety, privacy, and precision of FDA-cleared pediatric wearables, aligning with the nation’s high standards for medical technology. The expansion of pediatric RPM programs and collaborations between hospitals and device manufacturers are further fostering growth.

Asia-Pacific FDA-Cleared Pediatric Wearable Devices Market Insight

The Asia-Pacific FDA-cleared pediatric wearable devices market is poised to grow at the fastest CAGR of 23.5% during the forecast period of 2025 to 2032, driven by rapid healthcare digitalization, rising awareness of pediatric health monitoring, and a surge in pediatric chronic conditions across countries such as China, Japan, and India. Government-backed smart healthcare initiatives and improving healthcare access are fueling device adoption. The region’s role as a manufacturing hub for medical wearables is also enabling affordability and accessibility, bringing pediatric wearables to both premium urban consumers and emerging middle-class populations.

Japan FDA-Cleared Pediatric Wearable Devices Market Insight

The Japan FDA-cleared pediatric wearable devices market is gaining momentum due to the country’s strong culture of medical innovation, advanced hospital systems, and high adoption of connected technologies. Japanese parents are increasingly embracing clinically validated devices for monitoring sleep apnea, respiratory distress, and cardiac health in children. The integration of pediatric wearables with IoT-based hospital and homecare platforms is accelerating adoption. In addition, Japan’s aging caregiver population is driving the need for convenient, automated monitoring solutions, strengthening the role of pediatric wearables in both household and clinical environments.

India FDA-Cleared Pediatric Wearable Devices Market Insight

The India FDA-cleared pediatric wearable devices market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, increasing birth rates, and strong demand for child health monitoring solutions among the expanding middle class. The government’s push for digital health and the growth of private pediatric hospitals are boosting adoption of FDA-cleared wearables. Affordability and localized production of monitoring devices further encourage uptake, especially in urban centers. Rising awareness of sudden infant health risks, combined with increasing acceptance of home-based health technologies, is expected to drive long-term market expansion.

FDA-Cleared Pediatric Wearable Devices Market Share

The FDA-cleared pediatric wearable devices industry is primarily led by well-established companies, including:

- Sibel Health, Inc. (U.S.)

- Strados Labs (U.S.)

- BioIntelliSense, Inc. (U.S.)

- Masimo (U.S.)

- Aevice Health Pte Ltd (Singapore)

- Empatica Inc. (U.S.)

- CardiacSense Ltd (Israel)

- Owlet (U.S.)

- Medtronic (Ireland)

- Fitbit LLC (U.S.)

- AMIT International Group FZE. (Switzerland)

- SAMSUNG. (South Korea)

- Abbott (U.S.)

- Dexcom, Inc. (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- NIHON KOHDEN CORPORATION (Japan)

- ResMed Inc. (U.S.)

- AliveCor, Inc. (U.S.)

- Withings (France)

What are the Recent Developments in Global FDA-Cleared Pediatric Wearable Devices Market?

- In June 2025, The FDA approved the Sonu Band by SoundHealth as the first wearable, drug-free treatment for moderate-to-severe nasal congestion in children aged 12 and older, expanding the pediatric indication for the device

- In May 2025, Aevice Health’s AeviceMD smart wearable stethoscope received clearance from the U.S. FDA for use in pediatric patients aged 3 years and older, making it a continuous‐monitoring home respiratory tool for children

- In November 2024, Theranica received an expanded FDA age indication for its Nerivio REN wearable device, allowing acute migraine treatment in children aged 8 and older. This made it the first FDA-cleared, non-drug neuromodulation therapy specifically indicated for pediatric migraine

- In July 2024, Strados Labs successfully completed a pediatric validation asthma study of its RESP Biosensor technology at Ann & Robert H. Lurie Children’s Hospital of Chicago to detect wheezing in children, a step toward securing pediatric-specific FDA clearance for the device

- In February 2024, Sibel Health announced its ANNE One wearable monitoring platform received its 4th FDA 510(k) clearance, extending continuous ambulatory ECG, SpO₂, temperature and non-invasive blood pressure measurements to adolescents aged 12 years and above for both hospital and home settings

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.