Global Field Emission Display Market

Market Size in USD Billion

USD

5.37 Billion

USD

10.00 Billion

2025

2033

USD

5.37 Billion

USD

10.00 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.37 Billion | |

| USD 10.00 Billion | |

| % | |

|

Field Emission Display Market Overview

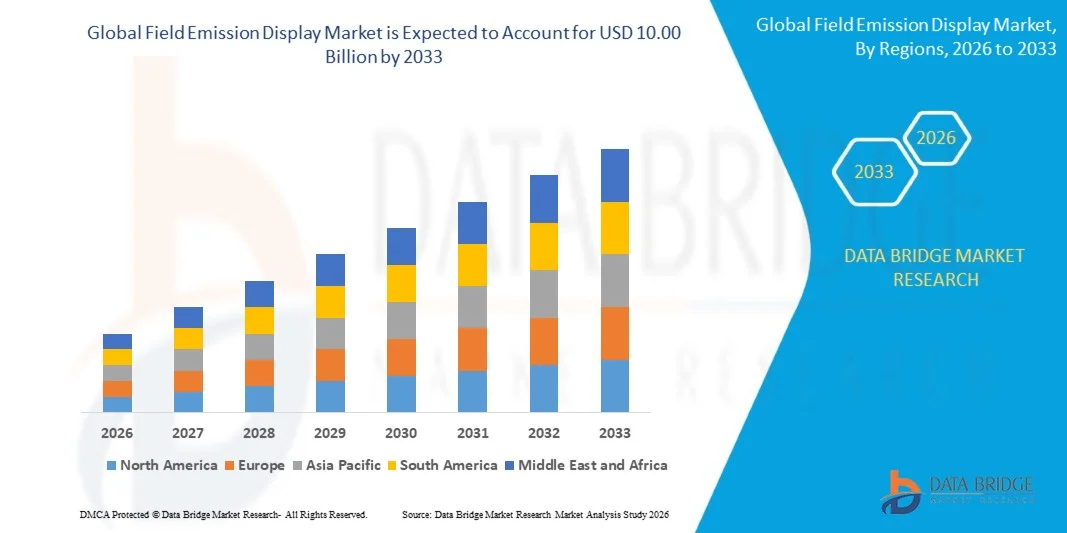

The Field Emission Display Market was valued at USD 5.37 billion in 2025 and is projected to reach USD 10.00 billion by 2033, growing at a CAGR of 8.10% from 2026 to 2033. The market is experiencing steady growth driven by increasing demand for high-resolution, energy-efficient, and ultra-thin display technologies, along with expanding applications across consumer electronics, automotive displays, medical imaging, and industrial visualization systems.

The growing preference for displays offering high brightness, fast response times, wide viewing angles, and low power consumption is encouraging manufacturers to explore field emission display technologies as alternatives to conventional LCD and plasma display systems. Field emission displays use electron emission from microscopic emitters to produce high-quality images with reduced energy requirements, making them suitable for applications requiring enhanced contrast, rapid image rendering, and reliable performance in compact electronic devices.

The expansion of smart consumer electronics, advanced driver assistance systems, digital dashboards, and professional imaging equipment is further supporting market demand. In addition, increasing investment in nanomaterials, carbon nanotube emitters, and vacuum microelectronics is improving field emission display performance and manufacturing scalability, creating opportunities for adoption across next-generation televisions, wearable devices, aerospace displays, defense visualization systems, and high-performance medical diagnostic equipment.

Key Market Trends & Insights

- North America dominated the field emission display market with the largest revenue share of 37.4% in 2025, supported by strong investments in advanced electronics, defense visualization systems, aerospace displays, medical imaging equipment, and continuous research in nanomaterials and vacuum microelectronics.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.2% from 2026 to 2033. Growth is driven by rapid expansion of consumer electronics manufacturing, increasing demand for smartphones and televisions, rising automotive display adoption, and strong investment in semiconductor and display panel production.

- The Conductive Layer segment held the largest market revenue share of approximately 36.8% in 2025 driven by its essential role in enabling electron transport and uniform emission across field emission display panels. Conductive layers are increasingly manufactured using indium tin oxide, graphene, carbon nanotubes, and other advanced nanomaterials to improve display brightness, electrical conductivity, and image uniformity across high-performance display applications.

- The Organic Material segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing investment in organic conductive compounds, flexible substrates, and hybrid display architectures. Rising demand for lightweight, bendable, and energy-efficient display technologies across consumer electronics, automotive interfaces, and wearable devices is accelerating segment expansion.

- The Smartphones segment held the largest market revenue share of approximately 31.6% in 2025 driven by high global smartphone shipment volumes and growing demand for slim, high-resolution, and power-efficient display panels. Smartphone manufacturers are increasingly evaluating advanced display technologies that offer fast response times, high brightness, and improved outdoor visibility while supporting compact device designs and extended battery performance.

- The OLED Display segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing development of hybrid field emission and OLED display structures. Rising demand for premium televisions, foldable smartphones, automotive cockpit displays, and high-contrast consumer electronics is supporting investment in next-generation display technologies with enhanced brightness, durability, and energy efficiency.

- The Less Than 10 Inches segment held the largest market revenue share of approximately 34.7% in 2025 driven by widespread use of compact display panels in smartphones, wearable devices, handheld industrial equipment, portable medical devices, and military communication systems. Smaller displays are preferred due to their lower material requirements, compact form factor, and suitability for high-volume consumer electronics manufacturing.

- The Above 60 Inches segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising demand for large-format displays in digital signage, command centers, educational institutions, entertainment venues, and commercial visualization systems. Increasing investment in smart classrooms, public information displays, and high-resolution video walls is accelerating demand for large-sized field emission display panels.

- The Consumer Electronic segment held the largest market revenue share of approximately 43.5% in 2025 driven by growing demand for smartphones, televisions, tablets, laptops, gaming devices, and wearable electronics. Consumers are increasingly seeking display devices with high brightness, improved color quality, fast response times, and lower energy consumption, supporting the adoption of advanced display technologies across mass-market electronic products.

- The Automotive segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033, driven by increasing integration of digital instrument clusters, infotainment systems, head-up displays, rear-seat entertainment systems, and advanced driver assistance interfaces. Rising production of electric and connected vehicles is accelerating demand for durable, high-brightness, and fast-response display technologies capable of supporting real-time navigation, safety alerts, and vehicle performance information.

Market Size & Forecast

- Global Market Value (2025): USD 5.37 Billion

- Expected Market Value (2033): USD 10.00 Billion

- Forecast CAGR (2026–2033): 8.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Field Emission Display Market Segmentation

|

Attributes |

Field Emission Display Key Market Insights |

|

Segments Covered |

· By Component: Conductive Layer, Organic Material, Backlight Panel and Other Components · By Application: Smartphones, Tablets, laptops, TVs, OLED Display · By Display Size: Less Than 10 Inches, 10 - 20 Inches, 20 – 30 Inches, 30 - 40 Inches, 40 - 50 Inches, 50 – 60 Inches, Above 60 Inches · By End User: Consumer Electronic, Healthcare, Automotive, Education, Military, and Defence |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Samsung Electronics Co., Ltd. (South Korea) |

|

Market Opportunities |

• Integration Of Field Emission Displays In Automotive Head-Up Displays • Growing Adoption Of Carbon Nanotube-Based Display Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Field Emission Display Market Trends

Trend: Growing Development Of Carbon Nanotube-Based Field Emission Displays

Increasing demand for ultra-thin, high-brightness, and energy-efficient display technologies across consumer electronics, automotive, aerospace, and industrial sectors is supporting research and development in field emission displays. Conventional LCD displays require backlighting and multiple optical layers, while OLED displays can face limitations related to burn-in, brightness degradation, and manufacturing costs in certain large-format applications. These factors are encouraging manufacturers and research organizations to develop field emission display technologies capable of delivering fast response times, wide viewing angles, high contrast, and reduced power consumption.

In field emission displays, microscopic electron emitters generate electrons that strike phosphor-coated screens to create images, enabling high-quality visual output without requiring conventional backlighting systems. Carbon nanotubes are increasingly being evaluated as electron emitter materials due to their high electrical conductivity, strong mechanical properties, and ability to emit electrons at relatively low voltages. For instance, research published by the U.S. Department of Energy’s Oak Ridge National Laboratory demonstrated that carbon nanotube cathodes can produce high current density electron emission suitable for vacuum electronic and display applications.

The expansion of advanced cockpit displays, medical imaging systems, military visualization equipment, and industrial control panels is also increasing demand for displays capable of operating under high brightness, temperature variation, and vibration conditions. Field emission display technologies can provide response times in the nanosecond range, substantially faster than conventional LCD technologies that typically operate in millisecond ranges. Growing investment in nanomaterials, vacuum microelectronics, and flexible electronics is supporting further development of scalable field emission display solutions for next-generation high-performance visualization systems.

Field Emission Display Market Dynamics

Key Market Driver: Rising Demand For High-Brightness And Energy-Efficient Display Technologies

Industries worldwide are increasingly seeking display technologies that offer improved brightness, high image clarity, lower power consumption, and enhanced durability. The rapid expansion of consumer electronics, automotive infotainment systems, smart manufacturing interfaces, and digital signage is creating strong demand for displays that can deliver clear visual performance across indoor and outdoor operating environments. Field emission displays are gaining attention because they can offer wide viewing angles, high contrast ratios, and rapid image rendering while reducing dependence on energy-intensive backlighting components.

Automotive manufacturers are increasingly integrating advanced display systems into digital instrument clusters, head-up displays, infotainment units, and rear-seat entertainment systems. For instance, global vehicle production reached approximately 93.5 million units in 2023, increasing the addressable market for automotive display technologies across passenger vehicles and commercial fleets. The growing use of advanced driver assistance systems and connected vehicle platforms is further increasing demand for bright and responsive displays capable of presenting real-time navigation, safety alerts, and vehicle performance information.

Similarly, the global consumer electronics sector continues to support demand for compact and high-resolution display technologies. Worldwide smartphone shipments reached approximately 1.24 billion units in 2024, while global television shipments exceeded 200 million units during the same period. These high shipment volumes are encouraging display manufacturers to invest in technologies that improve visual quality, energy efficiency, and device design flexibility, supporting potential commercialization opportunities for field emission display systems.

Key Restraint/Challenge: High Manufacturing Complexity And Competition From Established Display Technologies

Field emission displays require precise fabrication of electron emitters, vacuum sealing structures, phosphor layers, and control electronics, creating significant manufacturing complexity. Maintaining uniform electron emission across large display surfaces remains technically challenging because variation in emitter performance can affect brightness consistency, image quality, and operational lifespan. These production requirements increase capital expenditure and limit large-scale commercialization compared with established LCD, OLED, microLED, and quantum dot display technologies.

In addition, the field emission display market faces strong competition from mature display technologies that benefit from large-scale manufacturing capacity, established supply chains, and continuous performance improvements. LCD technology remains widely used due to its cost competitiveness, while OLED technology is increasingly adopted in premium smartphones, televisions, and automotive displays because of its thin form factor and high contrast performance. This competitive environment makes it difficult for field emission display manufacturers to achieve sufficient production scale and pricing advantages.

Display manufacturing facilities require substantial investment, with advanced generation display fabrication plants often requiring capital expenditure exceeding USD 1 billion depending on substrate size and production capacity. In comparison, field emission display technologies remain at an earlier commercialization stage, and limited large-scale production infrastructure increases unit costs. In addition, carbon nanotube emitter fabrication and vacuum encapsulation processes require specialized equipment, restricting adoption among cost-sensitive consumer electronics manufacturers.

Key Market Opportunity: Adoption In Automotive, Aerospace, And Specialized Industrial Applications

Modern vehicles, aerospace platforms, defense systems, and industrial equipment increasingly require durable display technologies capable of operating in demanding environmental conditions. Conventional display technologies can experience reduced visibility under direct sunlight, performance limitations at extreme temperatures, and durability concerns in high-vibration environments. This is creating opportunities for field emission displays that can offer high brightness, rapid response, and stable image performance for mission-critical visualization applications.

Automotive companies are increasingly exploring high-performance display technologies for head-up displays, digital cockpits, advanced driver assistance systems, and electric vehicle interfaces. For instance, the global head-up display market is supported by growing installation rates in premium vehicles, with more than 10 million automotive head-up display units estimated to be shipped annually by the mid-2020s. Field emission displays can support clear projection and rapid image updates for navigation guidance, collision warnings, and real-time vehicle data, creating opportunities for use in next-generation connected and autonomous vehicles.

In addition, aerospace and defense organizations require display systems with high reliability, low power consumption, and strong resistance to electromagnetic interference. Field emission display technologies are being explored for cockpit instrumentation, portable military equipment, radar interfaces, and satellite ground control systems because vacuum-based display structures can offer operational advantages in harsh conditions. Continued advancement in carbon nanotube cathodes and flexible vacuum electronic components is expected to create opportunities for field emission display suppliers across specialized industrial, defense, and medical imaging applications.

Field Emission Display Market Scope

The market is segmented on the basis of component, application, display size, and end user.

- By Component

On the basis of component, the field emission display market is segmented into Conductive Layer, Organic Material, Backlight Panel, and Other Components. The Conductive Layer segment held the largest market revenue share of approximately 36.8% in 2025 driven by its essential role in enabling electron transport and uniform emission across field emission display panels. Conductive layers are increasingly manufactured using indium tin oxide, graphene, carbon nanotubes, and other advanced nanomaterials to improve display brightness, electrical conductivity, and image uniformity across high-performance display applications.

The Organic Material segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by increasing investment in organic conductive compounds, flexible substrates, and hybrid display architectures. Rising demand for lightweight, bendable, and energy-efficient display technologies across consumer electronics, automotive interfaces, and wearable devices is accelerating segment expansion.

- By Application

On the basis of application, the field emission display market is segmented into Smartphones, Tablets, Laptops, TVs, and OLED Display. The Smartphones segment held the largest market revenue share of approximately 31.6% in 2025 driven by high global smartphone shipment volumes and growing demand for slim, high-resolution, and power-efficient display panels. Smartphone manufacturers are increasingly evaluating advanced display technologies that offer fast response times, high brightness, and improved outdoor visibility while supporting compact device designs and extended battery performance.

The OLED Display segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing development of hybrid field emission and OLED display structures. Rising demand for premium televisions, foldable smartphones, automotive cockpit displays, and high-contrast consumer electronics is supporting investment in next-generation display technologies with enhanced brightness, durability, and energy efficiency.

- By Display Size

On the basis of display size, the field emission display market is segmented into Less Than 10 Inches, 10 - 20 Inches, 20 – 30 Inches, 30 - 40 Inches, 40 - 50 Inches, 50 – 60 Inches, and Above 60 Inches. The Less Than 10 Inches segment held the largest market revenue share of approximately 34.7% in 2025 driven by widespread use of compact display panels in smartphones, wearable devices, handheld industrial equipment, portable medical devices, and military communication systems. Smaller displays are preferred due to their lower material requirements, compact form factor, and suitability for high-volume consumer electronics manufacturing.

The Above 60 Inches segment is projected to register the fastest growth at a CAGR of 9.8% from 2026 to 2033, driven by rising demand for large-format displays in digital signage, command centers, educational institutions, entertainment venues, and commercial visualization systems. Increasing investment in smart classrooms, public information displays, and high-resolution video walls is accelerating demand for large-sized field emission display panels.

- By End User

On the basis of end user, the field emission display market is segmented into Consumer Electronic, Healthcare, Automotive, Education, Military, and Defence. The Consumer Electronic segment held the largest market revenue share of approximately 43.5% in 2025 driven by growing demand for smartphones, televisions, tablets, laptops, gaming devices, and wearable electronics. Consumers are increasingly seeking display devices with high brightness, improved color quality, fast response times, and lower energy consumption, supporting the adoption of advanced display technologies across mass-market electronic products.

The Automotive segment is projected to register the fastest growth at a CAGR of 10.6% from 2026 to 2033, driven by increasing integration of digital instrument clusters, infotainment systems, head-up displays, rear-seat entertainment systems, and advanced driver assistance interfaces. Rising production of electric and connected vehicles is accelerating demand for durable, high-brightness, and fast-response display technologies capable of supporting real-time navigation, safety alerts, and vehicle performance information.

Field Emission Display Market Regional Analysis

North America Field Emission Display Market Insight

North America dominated the field emission display market with the largest revenue share of 37.4% in 2025, supported by strong investment in advanced electronics, aerospace, defense, medical imaging, and automotive display technologies. Organizations in the region are increasingly exploring high-brightness, energy-efficient, and fast-response display solutions for specialized visualization applications. The presence of established semiconductor manufacturers, defense technology providers, research institutions, and consumer electronics companies is further supporting development and adoption of carbon nanotube-based field emission display technologies across commercial and mission-critical applications.

U.S. Field Emission Display Market Insight

The U.S. field emission display market captured the largest revenue share in 2025 within North America, fueled by increasing demand for advanced cockpit displays, defense visualization systems, medical diagnostic equipment, and high-performance consumer electronics. Manufacturers are increasingly investing in display technologies that offer enhanced brightness, high contrast, low power consumption, and reliable operation in demanding environments. The growing use of digital dashboards, head-up displays, simulation systems, and portable military electronics is further propelling the market. Moreover, rising investment in nanotechnology research and vacuum microelectronics is significantly contributing to field emission display development in the U.S..

Europe Field Emission Display Market Insight

The Europe field emission display market is expected to witness significant growth from 2026 to 2033, primarily driven by increasing demand for energy-efficient display technologies, advanced automotive electronics, and industrial automation systems. The region’s emphasis on sustainable manufacturing, energy efficiency, and high-performance engineering is encouraging investment in next-generation display technologies. Growing adoption across automotive instrument clusters, medical equipment, smart manufacturing interfaces, and public information systems is fostering market expansion. In addition, rising investment in research related to carbon nanomaterials and flexible electronics is supporting the development of advanced field emission display solutions.

U.K. Field Emission Display Market Insight

The U.K. field emission display market is expected to witness strong growth from 2026 to 2033, driven by expanding aerospace, defense, healthcare, and advanced electronics sectors. Organizations are increasingly seeking high-resolution and durable display technologies for flight simulation, command-and-control systems, medical imaging equipment, and industrial monitoring applications. The U.K.’s established research ecosystem and increasing investment in advanced materials are supporting development of carbon nanotube emitters and vacuum electronic components. In addition, demand for compact, low-power, and high-brightness displays is expected to continue stimulating market growth across specialized commercial and defense applications.

Germany Field Emission Display Market Insight

The Germany field emission display market is expected to witness strong growth from 2026 to 2033, fueled by increasing adoption of advanced automotive displays, industrial automation systems, and precision engineering technologies. Germany’s well-developed automotive and manufacturing industries are encouraging demand for durable display solutions capable of delivering high visibility, rapid response times, and reliable operation under vibration and temperature variation. The integration of field emission displays into digital cockpits, head-up displays, industrial control panels, and medical equipment is becoming increasingly relevant. Growing focus on energy-efficient manufacturing and advanced nanomaterial research is also supporting market development.

Asia-Pacific Field Emission Display Market Insight

The Asia-Pacific field emission display market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid expansion of consumer electronics manufacturing, increasing demand for smartphones and televisions, and growing investment in automotive and industrial display technologies. Countries such as China, Japan, South Korea, India, and Taiwan are major centers for display panel manufacturing, semiconductor production, and consumer electronics assembly, creating a strong base for field emission display development. Rising demand for energy-efficient, ultra-thin, and high-resolution displays, combined with expanding smart city and digitalization initiatives, is further supporting market growth across the region.

Japan Field Emission Display Market Insight

The Japan field emission display market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced electronics industry, high investment in display research, and growing demand for precision visualization technologies. Japanese manufacturers are increasingly focusing on high-quality display systems for automotive electronics, medical imaging, industrial automation, and consumer devices. The integration of field emission displays with advanced nanomaterials and vacuum microelectronics is supporting development of high-brightness and low-power display solutions. Moreover, Japan’s strong focus on robotics, aerospace systems, and compact electronic devices is expected to increase demand for durable and fast-response display technologies.

China Field Emission Display Market Insight

The China field emission display market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large-scale consumer electronics manufacturing base, expanding display panel production capacity, and growing investment in semiconductor and nanomaterial technologies. China is one of the largest markets for smartphones, televisions, tablets, and digital signage systems, increasing demand for advanced display technologies with improved energy efficiency and image quality. The expansion of electric vehicles, smart manufacturing, and smart city infrastructure is encouraging adoption of high-performance display solutions across automotive, industrial, and commercial applications. Strong domestic display manufacturers and government support for advanced electronics development are key factors propelling market growth in China.

Field Emission Display Market Share

The Field Emission Display industry is primarily led by well-established companies, including:

• Samsung Electronics Co., Ltd. (South Korea)

• LG Display Co., Ltd. (South Korea)

• NEC Corporation (Japan)

• Sharp NEC Display Solutions of America, Inc. (U.S.)

• Leyard Europe (Germany)

• Barco NV (Belgium)

• Sony Group Corporation (Japan)

• E Ink Holdings Inc. (Taiwan)

• AUO Corporation (Taiwan)

• DEEPSKY Corporation Ltd. (Hong Kong)

• VTRON Technologies Ltd. (China)

• AOTO Electronics Co., Ltd. (China)

• Unilumin Group Co., Ltd. (China)

• ViewSonic Corporation (U.S.)

• Koninklijke Philips N.V. (Netherlands)

Latest Developments in Field Emission Display Market

- In October 2024, industry analysts reported rising demand for high-resolution and energy-efficient display technologies. The development highlights increasing market momentum for field emission displays, driven by applications requiring ultra-thin form factors, high brightness, and low power consumption, which is expected to strengthen overall adoption across consumer electronics and advanced visualization systems

- In December 2023, display manufacturers advanced the development of transparent and flexible field emission display panels for automotive and industrial signage applications. This innovation is expected to enhance display versatility, enabling integration into curved surfaces, smart dashboards, and public information systems, while improving durability, energy efficiency, and expanding use cases across transportation and industrial environments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Field Emission Display Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Field Emission Display Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Field Emission Display Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.