Global Flame Retardants Market

Market Size in USD Billion

USD

15.34 Billion

USD

24.82 Billion

2024

2032

USD

15.34 Billion

USD

24.82 Billion

2024

2032

| 2025 - 2032 | |

| USD 15.34 Billion | |

| USD 24.82 Billion | |

| % | |

|

Flame Retardants Market Size

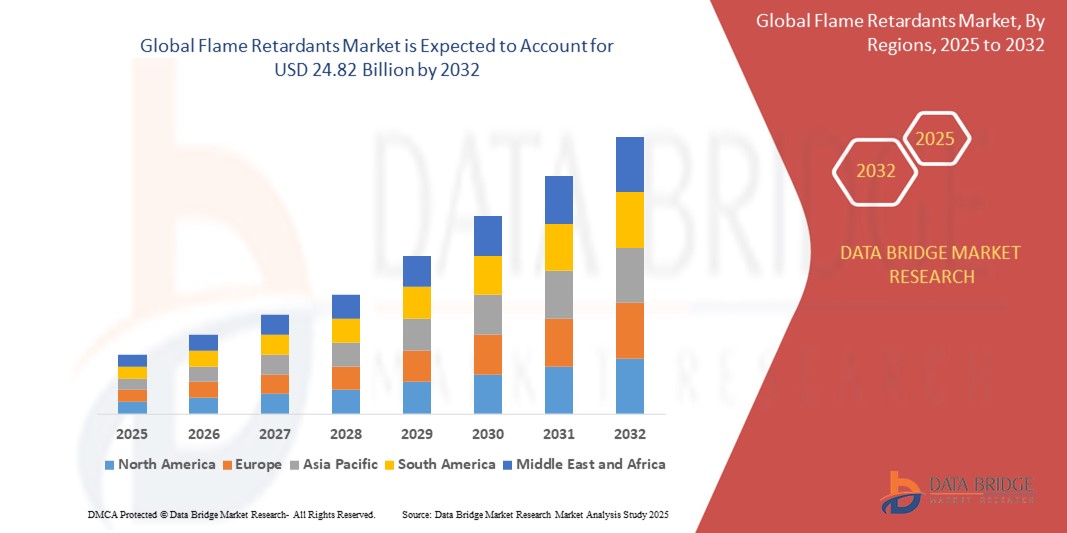

- The global flame retardants market size was valued at USD 15.34 billion in 2024 and is expected to reach USD 24.82 billion by 2032, at a CAGR of 6.20% during the forecast period

- The market growth is largely fueled by increasing fire safety regulations across construction, transportation, and electrical industries, prompting widespread incorporation of flame retardant materials in compliance with safety standards

- Furthermore, the rising demand for lightweight, high-performance polymers in automotive and electronics sectors is driving the need for efficient flame retardant additives, especially non-halogenated options, thereby significantly boosting the industry's growth

Flame Retardants Market Analysis

- Flame retardants are chemical substances added to materials to reduce their flammability and slow down the spread of fire. These additives can be incorporated into various materials, including plastics, textiles, and construction materials, to enhance their fire resistance

- The escalating demand for flame retardants is primarily fueled by stricter fire safety regulations, rapid urbanization, growth in electrical and electronics manufacturing, and a rising emphasis on sustainable, halogen-free flame retardant solutions across industries

- Asia-Pacific dominated the flame retardants market with a share of 56.6% in 2024, due to industrial expansion, rising construction activities, and robust demand from electronics manufacturing hubs

- North America is expected to be the fastest growing region in the flame retardants market during the forecast period due to stringent flammability standards in construction materials, electronics, and transportation equipment

- Non-halogenated segment dominated the market with a market share of 61.4%% in 2024, due to stringent environmental regulations and growing concerns over toxic emissions from halogenated compounds. Non-halogenated flame retardants such as aluminium hydroxide and organophosphorus compounds are gaining traction for their lower toxicity and better recyclability, especially in green building materials and sustainable product designs

Report Scope and Flame Retardants Market Segmentation

|

Attributes |

Flame Retardants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Flame Retardants Market Trends

“Rising Awareness of Environmentally Friendly Alternatives”

- A significant and accelerating trend in the global flame retardants market is the rising awareness and adoption of environmentally friendly alternatives to traditional halogenated flame retardants. This shift is driven by growing regulatory pressure, increasing environmental consciousness, and demand for sustainable material solutions across key industries such as construction, automotive, and electronics

- For instance, Clariant has introduced its Exolit range of phosphorus-based, halogen-free flame retardants, which are designed to meet stringent fire safety standards while reducing environmental and health risks. Similarly, Lanxess is focusing on non-halogenated solutions such as Disflamoll and Levagard, targeting applications in engineering plastics and flexible polyurethane foams

- These eco-friendly flame retardants offer comparable performance to traditional additives and also align with global trends toward recyclability and reduced toxic emissions. For instance, Israel Chemicals Ltd. (ICL) has expanded its non-halogenated offerings under the Fyrolflex brand, which are widely used in insulation and transportation applications due to their lower smoke and corrosive gas output

- The push for sustainable flame retardants is gaining traction as manufacturers and end-users seek to comply with international standards such as RoHS and REACH while maintaining product performance and durability. This has led to increased R&D investment and innovation across the supply chain, from raw material processing to end-product development

- Consequently, major players are prioritizing green chemistry and circular economy principles in their flame retardant portfolios. Companies such as Albemarle Corporation are advancing their product lines to include eco-conscious options that meet evolving environmental standards and customer demands for safer, sustainable fire protection

- The demand for environmentally friendly flame retardants is growing rapidly across sectors, reshaping market dynamics and setting a new benchmark for product development in fire safety technology

Flame Retardants Market Dynamics

Driver

“Growth in Construction and Infrastructure”

- The growth in construction and infrastructure activities worldwide is a significant driver for the increasing demand for flame retardants, as fire safety compliance becomes a critical requirement in modern building materials and design

- For instance, in February 2024, Clariant expanded its Exolit flame retardant production capacity to meet the rising demand from the global construction sector, especially for applications in insulation materials, cable sheathing, and structural components. Such strategic expansions by major companies are expected to drive the flame retardants market forward during the forecast period

- As governments and regulatory bodies enforce stricter fire safety codes in residential, commercial, and industrial buildings, there is growing pressure on material suppliers and contractors to use flame retardant-treated polymers and composites

- The use of flame retardants in construction elements such as polyurethane foam insulation, roofing membranes, wall panels, and electrical wiring enhances fire resistance and also contributes to safer, more resilient infrastructure

- With increasing investment in green buildings and sustainable urban development, demand is also rising for halogen-free and eco-friendly flame retardants, prompting key players such as Lanxess and ICL Group to innovate new formulations that deliver both safety and environmental performance, reinforcing the market's long-term growth trajectory

Restraint/Challenge

“High Cost of Advanced Flame Retardants”

- The high cost of advanced flame retardants poses a significant challenge to broader market adoption. As industries transition from traditional halogenated options to more environmentally friendly, high-performance alternatives, the price gap becomes a barrier, particularly for cost-sensitive applications and markets

- For instance, non-halogenated flame retardants such as Clariant’s Exolit and Lanxess’s Disflamoll are often more expensive due to the complexity of their production processes and the specialized performance attributes they offer. This price disparity discourages small- to mid-sized manufacturers in sectors such as construction and textiles from fully adopting these advanced materials

- Addressing this cost challenge through scale-driven price reductions, technological innovation, and supportive regulatory incentives is critical for accelerating adoption. Companies such as ICL and Albemarle are investing in R&D to improve cost efficiency and expand the applicability of their sustainable flame retardant portfolios. However, until such innovations reach commercial scale, the elevated price point remains a limiting factor in high-volume, price-competitive industries

- While awareness of environmental and health impacts is growing, the immediate financial burden associated with switching to advanced flame retardants often delays procurement decisions, especially in developing economies and sectors with thin margins

- Bridging this gap through collaboration between regulatory bodies, manufacturers, and end-users—via subsidies, incentives, or shared innovation—will be essential to overcome pricing constraints and drive sustainable market growth

Flame Retardants Market Scope

The market is segmented on the basis of type, product, application, and end-use industry.

• By Type

On the basis of type, the flame retardants market is segmented into alumina trihydrate, brominated flame retardants, antimony trioxide, phosphorus flame retardants, and others. The alumina trihydrate segment accounted for the largest market revenue share in 2024, driven by its low cost, environmental friendliness, and widespread applicability in plastics, rubbers, and textiles. Its smoke suppression capabilities and thermal stability have positioned it as a go-to option in the building and construction sector. Demand is further bolstered by regulatory pressures against halogenated compounds, favoring safer alternatives such as alumina trihydrate.

The phosphorus flame retardants segment is anticipated to witness the fastest CAGR from 2025 to 2032, owing to its effectiveness in both gas-phase and condensed-phase mechanisms. Its compatibility with a wide range of polymers, particularly engineering plastics and epoxy resins, drives adoption in high-performance applications such as electronics and automotive. Growing awareness of eco-friendly and halogen-free solutions is expected to boost demand for phosphorus-based formulations.

• By Product

On the basis of product, the flame retardants market is segmented into halogenated and non-halogenated. The non-halogenated segment held the largest market revenue share of 61.4% in 2024, attributed to stringent environmental regulations and growing concerns over toxic emissions from halogenated compounds. Non-halogenated flame retardants such as aluminum hydroxide and organophosphorus compounds are gaining traction for their lower toxicity and better recyclability, especially in green building materials and sustainable product designs.

The halogenated segment is projected to grow at the fastest CAGR from 2025 to 2032, driven by its superior flame-retardant efficiency, lower dosage requirements, and strong performance in electrical and electronic applications. Brominated flame retardants, a major subcategory, continue to see significant use in printed circuit boards and insulation materials due to their cost-effectiveness and proven efficacy.

• By Application

On the basis of application, the flame retardants market is segmented into epoxy, unsaturated polyester, polyolefins, polyvinyl chloride, acrylonitrile butadiene styrene (ABS), polyamide, polystyrene, polyurethane (PU), polyethylene terephthalate (PET), and polybutylene terephthalate (PBT). The polyurethane (PU) segment dominated the market share in 2024, driven by its extensive usage in building insulation, furniture, and automotive interiors. The flammability of PU foam has led to increased adoption of flame retardants to comply with fire safety standards.

The polyolefins segment is anticipated to witness the fastest growth rate during the forecast period, as these materials are extensively used in packaging, cables, and textiles. With increasing pressure to replace halogenated systems, the demand for effective flame retardant formulations compatible with polyolefins is surging, supported by rising industrial and infrastructural development globally.

• By End-Use Industry

On the basis of end-use industry, the flame retardants market is segmented into building and construction, electronics and appliances, automotive and transportation, wires and cables, textiles, and others. The building and construction segment captured the largest market share in 2024, driven by strict fire safety regulations and the need for non-combustible materials in residential and commercial infrastructure. Flame retardants are essential for treating insulation materials, structural components, and decorative panels to meet safety codes.

The electronics and appliances segment is expected to register the fastest CAGR from 2025 to 2032, owing to the growing production of consumer electronics and the need for enhanced fire resistance in circuit boards, casings, and wiring insulation. The miniaturization of devices and rising adoption of flame-retardant thermoplastics are fueling demand in this segment, particularly in emerging markets with rapid technological adoption.

Flame Retardants Market Regional Analysis

- Asia-Pacific dominated the flame retardants market with the largest revenue share of 56.6% in 2024, driven by industrial expansion, rising construction activities, and robust demand from electronics manufacturing hubs

- The region’s strong manufacturing base, rapid urbanization, and increasing awareness of fire safety standards in infrastructure and consumer electronics are key growth drivers

- Supportive fire safety regulations, increasing use of engineering plastics, and the presence of local raw material suppliers are further boosting adoption across various end-use sectors

Japan Flame Retardants Market Insight

The Japan flame retardants market is expanding steadily due to stringent building codes and fire safety regulations, particularly in public infrastructure and transportation sectors. The country’s advanced electronics industry also drives demand for halogen-free flame retardants in circuit boards and consumer devices. Local players focus on developing high-performance, environmentally friendly additives to comply with global standards and cater to export markets.

China Flame Retardants Market Insight

China held the largest share in the Asia-Pacific flame retardants market in 2024, backed by its dominant position in electronics, automotive, and construction industries. Government mandates on fire safety in public buildings and increasing production of flame-retardant polymers for domestic and international consumption are fueling growth. Chinese manufacturers are rapidly investing in non-halogenated alternatives to align with global environmental expectations.

Europe Flame Retardants Market Insight

The Europe flame retardants market is projected to grow at a notable CAGR over the forecast period, driven by stringent REACH regulations and growing preference for sustainable, non-toxic flame-retardant solutions. The demand is particularly strong in automotive and electronics applications, where flame retardants enhance safety without compromising recyclability. The region’s push toward halogen-free materials and high adoption of innovative polymer technologies support market expansion.

U.K. Flame Retardants Market Insight

The U.K. market is set to grow consistently, fueled by increasing implementation of fire safety codes in residential and commercial construction. Rising demand for energy-efficient buildings and sustainable materials is pushing the use of halogen-free flame retardants. The growth of electric vehicle manufacturing and strict standards in the public transport sector are also encouraging investment in advanced fire-resistant polymers.

Germany Flame Retardants Market Insight

Germany’s flame retardants market is expected to expand significantly, underpinned by a strong focus on safety in automotive, electronics, and industrial manufacturing. Environmental compliance and innovation in additive technologies are encouraging a transition to phosphorus-based and mineral flame retardants. The country's leadership in eco-design and engineering drives adoption in construction and cable insulation applications.

North America Flame Retardants Market Insight

North America is projected to register the fastest CAGR from 2025 to 2032, driven by stringent flammability standards in construction materials, electronics, and transportation equipment. The region’s growing demand for sustainable building practices and the increasing adoption of electric vehicles are boosting the use of high-efficiency, non-halogenated flame retardants. Regulatory alignment with global safety and environmental standards further supports market expansion.

U.S. Flame Retardants Market Insight

The U.S. captured the largest revenue share in North America in 2024, supported by strict fire safety codes in residential, commercial, and industrial applications. High consumption of flame-retardant plastics in electronics, automotive interiors, and building insulation is driving demand. A shift toward eco-friendly materials and increased R&D in polymer additives are further propelling the growth of halogen-free and phosphorus-based solutions.

Flame Retardants Market Share

The flame retardants industry is primarily led by well-established companies, including:

- DuPont (U.S.)

- SOLVAY (Belgium)

- DAIKIN (Japan)

- Dow (U.S.)

- Huntsman International LLC (U.S.)

- Bostik (France)

- H.B. Fuller Company (U.S.)

- Sika AG (Switzerland)

- Cardolite Corporation (U.S.)

- Kukdo Chemical Co., Ltd., (South Korea)

- BASF SE (Germany)

- Freudenberg SE (Germany)

- Covestro AG (Germany)

- LANXESS (Germany)

- Mitsui Chemicals Inc. (Japan)

- Wanhua (China)

- Arkema (France)

- Hexion (U.S.)

- Woodbridge (Canada)

Latest Developments in Global Flame Retardants Market

- In January 2022, Huber Engineered Materials completed the acquisition of MAGNIFIN Magnesiaprodukte GmbH & Co KG (MAGNIFIN). The product range formerly managed by MAGNIFIN and represented by Martinswerk GmbH has now been fully integrated into Huber's Fire Retardant Additives (FRA) strategic business unit. This acquisition significantly strengthens Huber's global presence in the market, expanding its portfolio of halogen-free fire retardants, smoke suppressants, and specialty aluminum oxides

- In December 2021, Clariant began construction of a new flame retardant production facility at its Daya Bay site in Guangdong Province, China. This expansion is designed to boost production capacity and enhance Clariant’s ability to meet the rising regional demand for flame retardant solutions

- In November 2021, Italmatch Chemicals SpA launched “Liquid Masteret,” a new phosphorus-based flame retardant. The product features concentrated blends of stabilized and micro-encapsulated red phosphorus (RP), addressing the growing market demand for halogen-free fire protection solutions across various industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Flame Retardants Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Flame Retardants Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Flame Retardants Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.