Global Flexible Lid Stock Packaging Market

Market Size in USD Billion

USD

1.51 Billion

USD

2.41 Billion

2024

2032

USD

1.51 Billion

USD

2.41 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.51 Billion | |

| USD 2.41 Billion | |

| % | |

|

Flexible Lid Stock Packaging Market Size

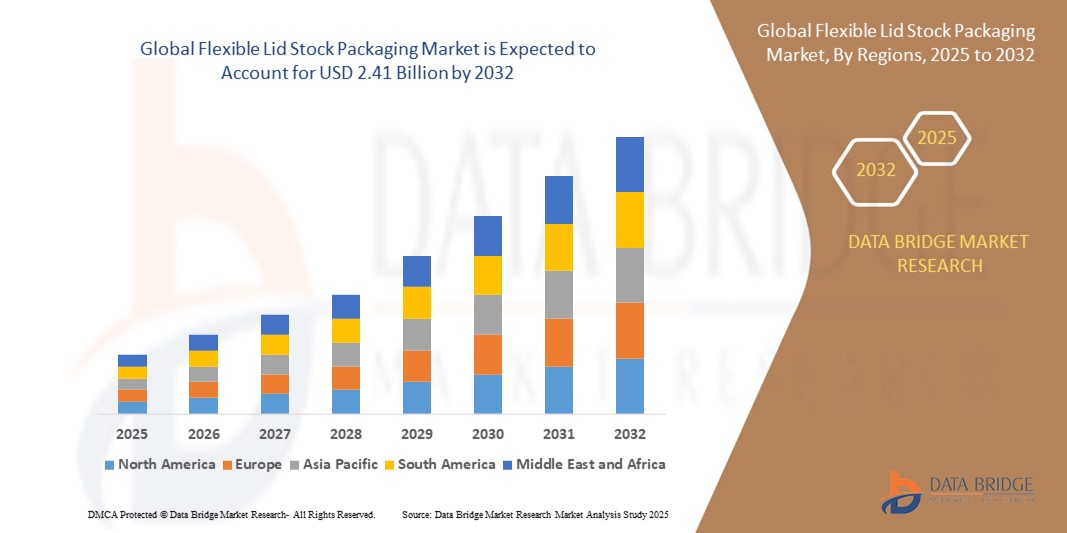

- The global flexible lid stock packaging market size was valued at USD 1.51 billion in 2024 and is expected to reach USD 2.41 billion by 2032, at a CAGR of 6.00% during the forecast period

- The market growth is primarily driven by increasing demand for convenient, lightweight, and sustainable packaging solutions across various industries, coupled with advancements in material technologies and manufacturing processes

- Rising consumer preference for eco-friendly packaging, along with the growing adoption of flexible lid stock in food, beverage, and healthcare sectors, is positioning it as a preferred packaging solution, significantly contributing to industry expansion

Flexible Lid Stock Packaging Market Analysis

- Flexible lid stock packaging, characterized by its lightweight, durable, and customizable properties, is a critical component in modern packaging solutions, offering enhanced product protection, extended shelf life, and consumer convenience across industries such as food and beverage, dairy, and healthcare

- The surge in demand is fueled by the global shift toward sustainable packaging, rising consumption of packaged goods, and the need for cost-effective, high-performance packaging solutions

- Asia-Pacific dominated the flexible lid stock packaging market with the largest revenue share of 42.5% in 2024, driven by rapid industrialization, a booming food and beverage sector, and increasing consumer demand for packaged products in countries such as China and India

- Europe is expected to be the fastest-growing region during the forecast period, attributed to stringent regulations promoting sustainable packaging, advancements in recycling technologies, and growing adoption in the dairy and personal care industries

- The Polymer Films segment dominated the largest market revenue share of approximately 40% in 2024, driven by its versatility, durability, and cost-effectiveness, making it ideal for a wide range of applications, particularly in food and beverage packaging

Report Scope and Flexible Lid Stock Packaging Market Segmentation

|

Attributes |

Flexible Lid Stock Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Flexible Lid Stock Packaging Market Trends

Increasing Adoption of Sustainable and Smart Packaging Solution

- The global flexible lid stock packaging market is experiencing a notable trend toward the integration of sustainable materials and smart packaging technologies

- Manufacturers are increasingly utilizing biodegradable, recyclable, and bio-based materials, such as paper and polymer films, to meet consumer demand for eco-friendly packaging and comply with stringent environmental regulations

- Smart packaging solutions, incorporating technologies such as QR codes, RFID tags, and sensors, are gaining traction to enhance traceability, ensure product authenticity, and provide consumers with interactive experiences

- For instances, companies are developing smart lids with embedded sensors to monitor product freshness, particularly for dairy and food products, improving shelf life and reducing waste

- This trend is strengthening the appeal of flexible lid stock packaging for both end-users and manufacturers, aligning with global sustainability goals and enhancing brand value

- The use of advanced digital printing technologies is also enabling high-quality, customizable designs, allowing brands to differentiate their products in competitive markets

Flexible Lid Stock Packaging Market Dynamics

Driver

Growing Demand for Convenience and Sustainable Packaging in Food and Beverage Industry

- The rising consumer preference for convenient, on-the-go packaging solutions, such as easy-to-open and resealable lids, is a key driver for the global flexible lid stock packaging market

- Flexible lid stock packaging enhances product protection by offering barriers against moisture, oxygen, and contamination, making it ideal for food and beverage, dairy, and personal care products

- Government regulations, particularly in Europe, promoting sustainable packaging and reducing single-use plastics are accelerating the adoption of eco-friendly materials such as paper and biodegradable polymer films

- The rapid growth of e-commerce and the expansion of retail sectors in Asia-Pacific are further boosting demand for lightweight, durable, and visually appealing packaging solutions

- Manufacturers are increasingly incorporating flexible lid stock as a standard feature in packaging to meet consumer expectations for convenience, hygiene, and sustainability

Restraint/Challenge

High Production Costs and Recycling Complexities

- The high initial costs associated with advanced manufacturing processes, such as extrusion coating and laminations, and the use of specialized materials such as metalized polymer films, can be a significant barrier to market adoption, particularly in cost-sensitive regions

- The integration of smart packaging technologies, such as sensors and RFID tags, further increases production expenses, limiting their scalability in emerging markets

- Recycling challenges pose a major restraint, as multi-layer flexible lid stock packaging, often combining materials such as aluminium foils and polymer films, is complex to separate and process, leading to lower recycling rates and environmental concerns

- The lack of standardized regulations across countries for sustainable packaging and recycling processes creates operational challenges for global manufacturers and service providers

- These factors may hinder market growth, especially in regions with stringent environmental policies or where consumer awareness of recycling limitations is high

Flexible Lid Stock Packaging market Scope

The market is segmented on the basis of material type, manufacturing process, and end use industry.

- By Material Type

On the basis of material type, the global flexible lid stock packaging market is segmented into paper, aluminium foils, non-woven, polymer films, and metalized polymer films. The polymer films segment dominated the largest market revenue share of approximately 40% in 2024, driven by its versatility, durability, and cost-effectiveness, making it ideal for a wide range of applications, particularly in food and beverage packaging. Polymer films provide excellent barrier properties, ensuring product freshness and extended shelf life.

The metalized polymer films segment is expected to witness the fastest growth rate from 2025 to 2032, with a projected CAGR of 7.2%. This growth is fueled by increasing demand for enhanced barrier properties, aesthetic appeal, and sustainability in packaging solutions. Metalized films, often coated with aluminum, offer superior protection against moisture, light, and oxygen, making them ideal for premium food, beverage, and pharmaceutical products.

- By Manufacturing Process

On the basis of manufacturing process, the global flexible lid stock packaging market is segmented into extruded films, extrusion coating, fluid coating, and laminations. The laminations segment accounted for the largest market revenue share of 45% in 2024, driven by its ability to combine multiple layers of materials to enhance barrier properties, strength, and flexibility. Laminated structures are widely used for their durability and ability to meet diverse packaging requirements across industries.

The extruded films segment is anticipated to experience the fastest growth rate of 6.8% from 2025 to 2032. This growth is driven by advancements in extrusion technology, enabling the production of high-performance, lightweight films that cater to the rising demand for sustainable and cost-effective packaging solutions. Extruded films are particularly favored in food and beverage applications for their clarity and sealability.

- By End Use Industry

On the basis of end use industry, the global flexible lid stock packaging market is segmented into food and beverage, dairy, chemicals, personal care, health care, specialties, and others. The food and beverage segment dominated the market with a revenue share of 50% in 2024, driven by the increasing demand for convenient, lightweight, and sustainable packaging solutions for products such as snacks, ready-to-eat meals, and beverages. Flexible lid stock packaging ensures product freshness, extends shelf life, and enhances brand visibility.

The health care segment is projected to witness the fastest growth rate of 7.5% from 2025 to 2032. The rising demand for secure and hygienic packaging for pharmaceuticals and medical products, coupled with advancements in tamper-evident and resealable lid stock solutions, is driving this segment's growth. Flexible lid stock packaging offers robust protection against contamination, making it critical for health care applications.

Flexible Lid Stock Packaging Market Regional Analysis

- Asia-Pacific dominated the flexible lid stock packaging market with the largest revenue share of 42.5% in 2024, driven by rapid industrialization, a booming food and beverage sector, and increasing consumer demand for packaged products in countries such as China and India

- Consumers prioritize flexible lid stock packaging for its lightweight properties, extended shelf life, and eco-friendly options, particularly in regions with high population density and diverse consumer preferences

- Growth is supported by advancements in material technologies, such as recyclable polymer films and metalized coatings, alongside increasing adoption in both food and non-food industries

Japan Flexible Lid Stock Packaging Market Insight

Japan’s flexible lid stock packaging market is expected to witness rapid growth due to strong consumer preference for high-quality, sustainable packaging solutions that enhance product preservation and convenience. The presence of major manufacturers and the integration of advanced materials in food and beverage packaging accelerate market penetration. Rising interest in customized packaging solutions also contributes to growth.

China Flexible Lid Stock Packaging Market Insight

China holds the largest share of the Asia-Pacific flexible lid stock packaging market, propelled by rapid urbanization, rising consumer demand for packaged goods, and increasing focus on sustainable packaging solutions. The country’s growing middle class and emphasis on smart manufacturing support the adoption of advanced materials such as metalized polymer films. Strong domestic production capabilities and competitive pricing enhance market accessibility.

U.S. Flexible Lid Stock Packaging Market Insight

The U.S. flexible lid stock packaging market is expected to witness significant growth, fueled by strong demand in the food and beverage sector and growing consumer preference for sustainable packaging. The trend towards convenience-driven packaging and stringent regulations promoting recyclable materials further boost market expansion. The integration of flexible lid stock in both OEM and aftermarket applications creates a diverse product ecosystem.

Europe Flexible Lid Stock Packaging Market Insight

The Europe flexible lid stock packaging market is expected to witness the fastest growth rate, supported by regulatory emphasis on sustainability and circular economy initiatives. Consumers seek packaging solutions that enhance product preservation while reducing environmental impact. Growth is prominent in food, dairy, and personal care industries, with countries such as Germany and France showing significant uptake due to rising environmental awareness and advanced manufacturing capabilities.

U.K. Flexible Lid Stock Packaging Market Insight

The U.K. market for flexible lid stock packaging is expected to experience rapid growth, driven by demand for sustainable and convenient packaging in urban and suburban settings. Increased interest in product aesthetics and rising awareness of eco-friendly materials encourage adoption. Evolving regulations promoting recyclable packaging influence consumer choices, balancing functionality with compliance.

Germany Flexible Lid Stock Packaging Market Insight

Germany is expected to witness the fastest growth rate in flexible lid stock packaging, attributed to its advanced manufacturing sector and high consumer focus on sustainability and efficiency. German consumers prefer technologically advanced materials, such as recyclable polymer films, that reduce waste and enhance product shelf life. The integration of these materials in premium packaging and aftermarket options supports sustained market growth.

Flexible Lid Stock Packaging Market Share

The flexible lid stock packaging industry is primarily led by well-established companies, including:

- Pactiv LLC (U.S.)

- Oji Holdings Corporation (Japan)

- DS Smith (U.K.)

- Chase Corp(U.S.)

- International Plastics Inc. (U.S.)

- Schur Flexibles Holding GesmbH (Austria)

- NIPPON PAPER INDUSTRIES CO., LTD. (Japan)

- Mondi (U.K.)

- 3M (U.S.)

- Bayer AG (Germany)

- Graphic Packaging International, LLC (U.S.)

- WestRock Company (U.S.)

- Smurfit Kappa (Ireland)

- Krones AG (Germany)

- Amcor plc (Australia)

- Graham Packaging Company (U.S.)

- Sonoco Products Company (U.S.)

- Parker Hannifin Corp (U.S.)

- Berry Global Inc. (U.S.)

- Merck KGaA (Germany)

What are the Recent Developments in Global Flexible Lid Stock Packaging Market?

- In March 2025, Parkside Flexibles introduced Popflex, a recyclable lidding film tailored for fresh produce packaging. Designed to be weld-sealed to PET trays, the film remains attached during recycling, preventing contamination of PP and PE streams and qualifying for OPRL-certified kerbside collection. Made from mono-PET with 30% post-consumer recycled content, Popflex™ reduces plastic use while maintaining recyclability. It also features ParkScribe™ laser-scored technology, enabling a simple “press, pop, and peel” opening for enhanced consumer convenience. Optional macro perforation improves breathability and shelf life, making it a sustainable and user-friendly solution

- In January 2025, Optimum Group and Packaging Partners formalized an exclusive long-term partnership focused on delivering innovative and sustainable packaging solutions. This collaboration combines Optimum Group’s strength in flexible packaging and self-adhesive labels with Packaging Partners’ expertise in sustainable paper and flexible materials, creating a comprehensive offering tailored to meet evolving regulatory standards such as the PPWR. By sharing resources, leads, and technical know-how, the alliance aims to provide future-proof, recyclable packaging that supports a circular economy and enhances both companies’ market positions

- In January 2025, Huhtamaki India, in collaboration with the Embassy of Finland, hosted the 2nd edition of the Think Circle event in New Delhi, unveiling the “Design for Recyclability Guidelines for Films & Flexible Packaging.” Developed under the CII-India Plastics Pact (IPP), these guidelines aim to transform India’s packaging landscape by promoting mono-material designs, minimizing carbon black pigments, and reducing ink and adhesive usage. The initiative supports a circular economy, helping brands and converters transition to recyclable formats and reduce plastic waste across food, personal care, and homecare sectors

- In September 2024, Marigold Health Foods partnered with Sonoco to introduce a fully recyclable paper-based packaging solution for its range of natural, plant-based food products. The new can body is made from 95% paper, with 60% sourced from post-consumer recycled fiber, and features a paper-based base that replaces the previous metal component. This design enables kerbside recycling in the UK and aligns with European sustainability regulations, significantly reducing the packaging’s environmental footprint. The innovation supports a circular economy while maintaining product protection and shelf-life performance

- In November 2024, Amcor plc announced an USD 8.4 billion all-stock acquisition of Berry Global Group, Inc., combining two major players in flexible and healthcare packaging. The merger aims to create a global leader in consumer packaging, with a projected $24 billion in annual revenue and enhanced capabilities in sustainability, innovation, and supply chain resilience. Berry shareholders will receive 7.25 Amcor shares per Berry share, resulting in a combined ownership split of 63% Amcor and 37% Berry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Flexible Lid Stock Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Flexible Lid Stock Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Flexible Lid Stock Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.