Global Fluorotelomers Market

Market Size in USD Billion

USD

8.96 Billion

USD

21.26 Billion

2024

2032

USD

8.96 Billion

USD

21.26 Billion

2024

2032

| 2025 - 2032 | |

| USD 8.96 Billion | |

| USD 21.26 Billion | |

| % | |

|

Fluorotelomers Market Size

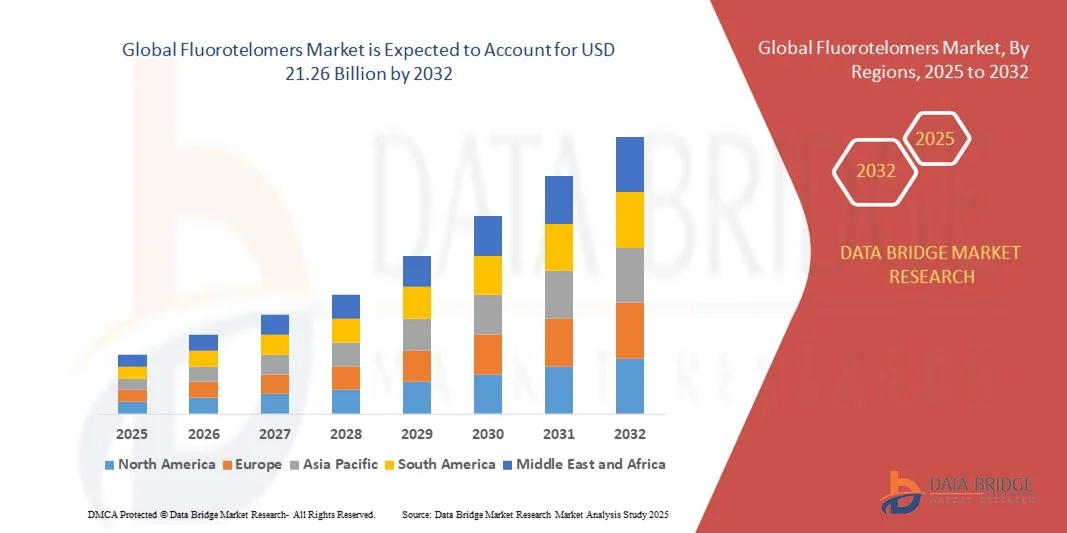

- The global fluorotelomers market size was valued at USD 8.96 billion in 2024 and is expected to reach USD 21.26 billion by 2032, at a CAGR of 11.4% during the forecast period

- The market growth is largely fueled by increasing demand for high-performance and low-surface-energy materials across textiles, packaging, and coatings industries, as fluorotelomers offer superior stain, water, and oil resistance. Growing awareness regarding sustainable fluorinated materials and their ability to enhance durability and performance is further driving market expansion across industrial applications

- Furthermore, rising investments in developing eco-friendly, PFAS-free fluorotelomer alternatives and expanding applications in food packaging and firefighting foams are strengthening market prospects. These converging factors are positioning fluorotelomers as essential components in advanced surface protection technologies, thereby significantly boosting the industry’s growth

Fluorotelomers Market Analysis

- Fluorotelomers, a class of fluorinated compounds used in coatings, surfactants, and repellents, play a critical role in enhancing the performance of textiles, packaging, and industrial materials through superior resistance to stains, water, and chemicals. Their versatility and stability make them key ingredients in high-value applications across multiple industries

- The rising demand for sustainable and high-performance surface treatment solutions, along with advancements in fluorochemical synthesis, is propelling the global fluorotelomers market. Ongoing regulatory shifts and technological innovations promoting safer, low-toxicity formulations are further driving adoption and supporting long-term market growth

- Asia-Pacific dominated the fluorotelomers market with a share of 46.9% in 2024, due to the expanding textile and paper manufacturing sectors, rising use of fluorinated surfactants, and a strong presence of specialty chemical producers

- North America is expected to be the fastest growing region in the fluorotelomers market during the forecast period due to strong demand for fluorotelomer-based repellents, coatings, and surfactants across textiles, construction, and packaging sectors

- Textiles segment dominated the market with a market share of 35.8% in 2024, due to the extensive use of fluorotelomers in providing durable water, oil, and stain resistance to fabrics and garments. Their superior repellency properties enhance fabric longevity and reduce maintenance needs, making them highly preferred in apparel, upholstery, and industrial fabrics. Growing consumer demand for high-performance and easy-care textiles, along with expanding applications in outdoor clothing and technical textiles, further contributed to the segment’s dominance

Report Scope and Fluorotelomers Market Segmentation

|

Attributes |

Fluorotelomers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Fluorotelomers Market Trends

Adoption of Eco-Friendly, PFAS-Free Fluorotelomer Coatings

- The market is witnessing a shift towards the adoption of eco-friendly and PFAS-free fluorotelomer coatings due to growing environmental concerns and regulatory pressures. Manufacturers are focusing on developing sustainable alternatives that maintain performance benefits such as stain, oil, and water resistance while minimizing harmful emissions and bioaccumulation risks

- For instance, The Chemours Company has been investing in developing next-generation fluorotelomer-based coatings that meet environmental safety standards and align with global sustainability initiatives. These PFAS-free products are designed to deliver equivalent functionality while reducing long-term ecological impact

- The growing preference for PFAS-free formulations is encouraging innovation across industries such as textiles, packaging, and automotive. Companies are channeling research and development efforts into enhancing product stability and performance under diverse conditions without compromising environmental safety

- The adoption of green chemistry principles in fluorotelomer production is supporting the transition to sustainable coatings. These new formulations aim to reduce carbon footprint while ensuring durability and functional effectiveness, aligning with the sustainability goals of end-use industries

- Several manufacturers are expanding product portfolios through collaboration and partnerships to develop eco-conscious solutions. Such initiatives are helping them strengthen market positioning and comply with evolving global regulations related to per- and polyfluoroalkyl substances

- This trend highlights the industry’s commitment to balancing environmental responsibility with product innovation. The increasing focus on PFAS-free fluorotelomers marks a key step toward achieving sustainability and long-term market growth in performance coatings

Fluorotelomers Market Dynamics

Driver

Rising Demand for Stain, Water, and Oil-Resistant Materials

- The growing demand for high-performance materials that offer protection against stains, water, and oil is a major driver for the fluorotelomers market. Industries such as textiles, paper, and packaging are increasingly using fluorotelomer-based coatings to enhance product longevity and functionality

- For instance, Daikin Industries Ltd. has been developing advanced fluorotelomer products used in textiles and nonwoven materials to improve water and oil repellency while maintaining breathability and softness. Such developments are meeting the rising demand for durable, protective, and easy-to-maintain products across consumer and industrial sectors

- The growing awareness of surface protection benefits is pushing manufacturers to adopt fluorotelomer-based materials that provide superior barrier properties without affecting aesthetic appeal or texture. These coatings are gaining preference due to their excellent chemical stability and long-lasting performance

- Expanding applications in construction and automotive sectors are further supporting the demand for fluorotelomer-based protective coatings. Their ability to enhance durability and resistance against environmental factors is driving adoption across industrial uses

- The rising consumer inclination toward premium, easy-care products coupled with industry efforts to improve product safety and sustainability is expected to continue driving fluorotelomer demand. The shift toward high-performance, multifunctional materials reinforces the market’s steady growth trajectory

Restraint/Challenge

Stringent Environmental Regulations on Fluorinated Compounds

- Stringent environmental regulations imposed on fluorinated compounds present a major challenge to the fluorotelomers market. Global authorities are increasingly enforcing limits on PFAS emissions due to concerns over persistence, toxicity, and environmental accumulation

- For instance, the U.S. Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA) have introduced restrictions and monitoring programs targeting long-chain fluorinated compounds. These actions are compelling manufacturers to reformulate products and adopt safer alternatives to comply with evolving regulations

- The high cost and complexity of transitioning production processes to meet sustainability standards pose additional challenges for manufacturers. Research and development investments are required to create eco-friendly formulations that deliver equivalent performance while adhering to environmental norms

- Manufacturers also face difficulties in balancing product efficiency and environmental safety during product reformulation. Ensuring compliance while maintaining stain, oil, and water-resistant properties remains a key technical challenge for industry participants

- Overcoming these challenges requires continuous innovation and collaboration with regulatory authorities to achieve sustainable production. The industry’s ability to develop compliant, PFAS-free fluorotelomer solutions will determine its long-term growth and regulatory resilience

Fluorotelomers Market Scope

The market is segmented on the basis of product and application.

- By Product

On the basis of product, the fluorotelomers market is segmented into fluorotelomer alcohol, fluorotelomer acrylate, and fluorotelomer iodide. The fluorotelomer alcohol segment dominated the market with the largest revenue share 33.1% in 2024 due to its extensive use as a key intermediate in the production of surfactants and coatings. Its excellent oil and water repellency properties make it highly suitable for applications in textiles, carpets, and paper coatings. The segment’s dominance is further supported by growing demand from industrial and commercial sectors seeking high-performance materials with enhanced chemical stability and low surface energy characteristics. Moreover, ongoing R&D efforts to develop eco-friendly fluorotelomer alcohols with reduced bioaccumulation potential are contributing to sustained market growth.

The fluorotelomer acrylate segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by its increasing use in surface coatings, paints, and sealants to impart stain resistance and durability. Rising adoption in the construction and automotive industries for protective finishes is propelling demand. Its compatibility with polymer matrices enhances coating adhesion and longevity, which aligns with growing consumer and industrial preferences for durable and easy-to-clean surfaces. In addition, advancements in environmentally safer formulations are further stimulating the segment’s growth prospects during the forecast period.

- By Application

On the basis of application, the fluorotelomers market is segmented into fire fighting foams, food packaging, stain resistants, textiles, and others. The textiles segment held the largest market revenue share of 35.8% in 2024, driven by the extensive use of fluorotelomers in providing durable water, oil, and stain resistance to fabrics and garments. Their superior repellency properties enhance fabric longevity and reduce maintenance needs, making them highly preferred in apparel, upholstery, and industrial fabrics. Growing consumer demand for high-performance and easy-care textiles, along with expanding applications in outdoor clothing and technical textiles, further contributed to the segment’s dominance.

The food packaging segment is projected to record the fastest CAGR from 2025 to 2032, fueled by increasing demand for grease-resistant and moisture-proof packaging materials. Fluorotelomers are extensively used to produce coatings for paper and cardboard used in food wraps, take-out containers, and bakery packaging. With the rapid expansion of the global packaged food industry and rising emphasis on food safety and quality preservation, demand for fluorotelomer-based coatings is surging. Moreover, ongoing innovations in developing PFAS-free or low-toxicity alternatives are expected to further boost growth in this segment.

Fluorotelomers Market Regional Analysis

- Asia-Pacific dominated the fluorotelomers market with the largest revenue share of 46.9% in 2024, driven by the expanding textile and paper manufacturing sectors, rising use of fluorinated surfactants, and a strong presence of specialty chemical producers

- The region’s competitive manufacturing costs, rapid industrialization, and growing investments in sustainable fluorochemical production are accelerating market growth

- Favorable trade policies and increasing domestic demand from construction, automotive, and consumer goods industries further reinforce Asia-Pacific’s leading position in the market

China Fluorotelomers Market Insight

China held the largest share in the Asia-Pacific fluorotelomers market in 2024, supported by its extensive chemical production capacity and leadership in textile and paper coating applications. The nation’s robust infrastructure for fluorochemical synthesis, availability of low-cost raw materials, and government support for industrial modernization are major growth factors. Rising exports of fluorotelomer-based repellents and continued investments in eco-friendly alternatives to PFAS compounds are further boosting market development.

India Fluorotelomers Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by a surging textile industry, growing adoption of stain-resistant and water-repellent coatings, and expanding chemical manufacturing capabilities. Increasing foreign investments in specialty chemicals and strong government initiatives promoting domestic production are driving market expansion. Rising demand from the packaging and construction sectors, along with rapid industrialization, is further propelling India’s fluorotelomers market growth.

Europe Fluorotelomers Market Insight

The Europe fluorotelomers market is growing steadily, driven by stringent environmental regulations, strong demand for low-toxicity coatings, and innovation in sustainable fluorinated materials. The region’s emphasis on high-quality and compliant chemical production, coupled with increasing R&D investments in advanced polymer and textile coatings, is shaping market dynamics. Demand from sectors such as automotive, food packaging, and electronics continues to support regional growth.

Germany Fluorotelomers Market Insight

Germany leads the European market due to its advanced specialty chemical industry, focus on eco-friendly formulations, and robust presence of leading fluorochemical manufacturers. The country’s high R&D intensity and collaborations between industry and research institutions foster continuous innovation in surface protection and performance coatings. Demand is particularly strong from textile, automotive, and packaging sectors seeking sustainable high-performance materials.

U.K. Fluorotelomers Market Insight

The U.K. market benefits from growing investments in sustainable chemistry, increased regulatory focus on PFAS alternatives, and strong demand from the packaging and textile industries. The country’s emphasis on green innovation and chemical safety compliance supports the development of next-generation fluorotelomer-based coatings. Expanding production capabilities for specialty and niche chemicals further enhance the U.K.’s position within the European fluorotelomers landscape.

North America Fluorotelomers Market Insight

North America is projected to grow at the fastest CAGR from 2025 to 2032, driven by strong demand for fluorotelomer-based repellents, coatings, and surfactants across textiles, construction, and packaging sectors. Increasing regulatory shifts toward PFAS-free technologies, rising R&D investments, and a growing focus on sustainable material innovation are key growth drivers. The region’s advanced infrastructure for specialty chemical production and strong collaboration between manufacturers and research institutions support rapid market development.

U.S. Fluorotelomers Market Insight

The U.S. accounted for the largest share in the North America fluorotelomers market in 2024, underpinned by its leadership in textile finishing, packaging, and performance coating industries. The country’s robust R&D ecosystem, presence of key manufacturers, and ongoing innovation in safer fluorinated compounds are fueling demand. Increased government and corporate focus on environmental compliance and green chemistry initiatives further strengthen the U.S.’s dominant role in the regional fluorotelomers market.

Fluorotelomers Market Share

The fluorotelomers industry is primarily led by well-established companies, including:

- AIKIN INDUSTRIES, Ltd. (Japan)

- Clariant (Switzerland)

- Archroma (Switzerland)

- DYNAX (U.S.)

- AGC Inc. (Japan)

- Santa Cruz Biotechnology, Inc. (U.S.)

- DuPont (U.S.)

- Fluoryx Labs (U.S.)

- INDOFINE Chemical Company, Inc. (U.S.)

- Wilshire Technologies (U.S.)

- Fluorous Technologies Inc. (U.S.)

- TCI Chemicals (India) Pvt. Ltd. (India)

- Daikin America, Inc. (U.S.)

- Merck KGaA (Germany)

Latest Developments in Global Fluorotelomers Market

- In September 2024, Chemours Company announced the expansion of its fluorotelomer production facility in Fayetteville, U.S., aimed at addressing the rising global demand for low-toxicity and PFAS-free alternatives. The expansion focuses on sustainable fluorochemical development, supporting Chemours’ strategy to strengthen its position in eco-friendly fluorotelomer supply. This move is expected to enhance product availability across coatings, textiles, and packaging industries while aligning with tightening environmental regulations

- In June 2024, 3M Company unveiled a new range of next-generation fluorotelomer-based repellents designed for high-performance textile and paper coatings. The innovation emphasizes reduced environmental persistence and improved safety profiles, reflecting the company’s transition toward sustainable chemistry. This development is anticipated to boost 3M’s competitiveness in the global market by catering to industries shifting toward environmentally compliant and high-durability coating materials

- In March 2024, Daikin Industries was selected for the “Innovation Momentum 2024: The Global Top 100” award, recognizing its patent leadership and technological excellence in sustainable fluorochemical and HVAC&R innovations. The recognition reinforces Daikin’s position as a pioneer in eco-friendly materials and encourages further investment in fluorotelomer-based technologies for industrial applications

- In January 2024, Asahi India Glass Limited completed the acquisition of AIS Adhesives Limited from Map Auto Ltd, strengthening its market reach through expanded customer access and distribution networks. This acquisition supports AIS’s diversification into specialty materials, potentially enhancing its involvement in fluorochemical applications within coatings and surface treatment segments

- In March 2023, AGC announced a significant expansion of its fluorochemical production capacity at its Chiba Plant, Japan, to meet growing demand from the semiconductor and specialty materials sectors. The 35 billion yen investment is expected to elevate AGC’s Performance Chemicals business revenue beyond 200 billion yen by 2024, solidifying its leadership in high-value fluorotelomer intermediates for advanced industrial applications

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Fluorotelomers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Fluorotelomers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Fluorotelomers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.