Global Food Automation Market

Market Size in USD Billion

USD

8.56 Billion

USD

15.38 Billion

2025

2033

USD

8.56 Billion

USD

15.38 Billion

2025

2033

| 2026 - 2033 | |

| USD 8.56 Billion | |

| USD 15.38 Billion | |

| % | |

|

Food Automation Market Overview

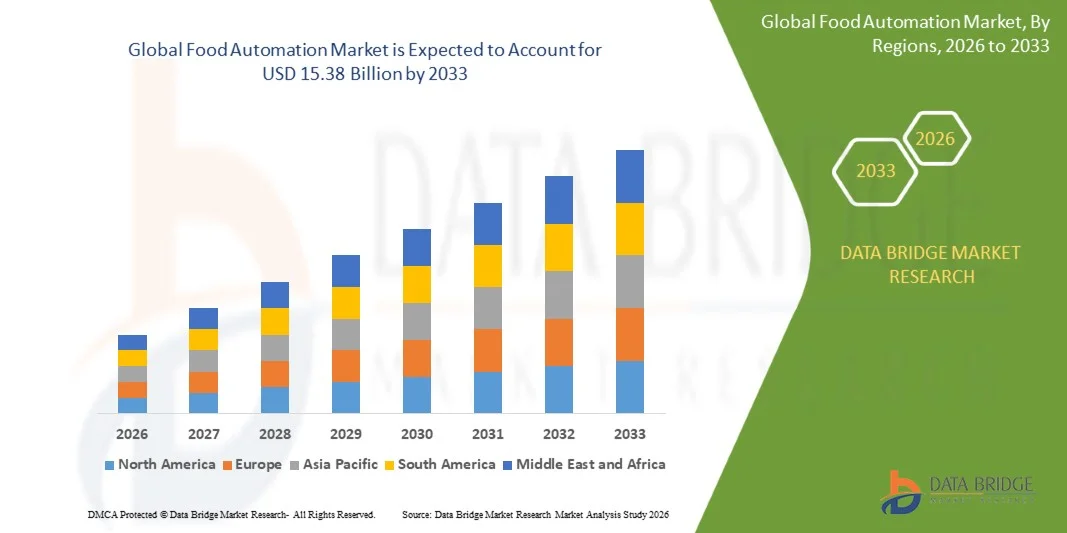

The Food Automation Market was valued at USD 8.56 billion in 2025 and is projected to reach USD 15.38 billion by 2033, growing at a CAGR of 7.60% from 2026 to 2033. The market is experiencing strong growth driven by increasing demand for operational efficiency in food processing facilities, rising labor shortages across the food manufacturing sector, rapid advancements in robotics and industrial automation technologies, and growing emphasis on food safety and quality control. The adoption of automated processing, packaging, palletizing, sorting, and inspection systems is expanding across food and beverage manufacturers as companies seek to improve productivity, reduce operational costs, and ensure consistent product quality.

The growing global demand for packaged, processed, and convenience foods, combined with stringent food safety regulations and increasing pressure to optimize production efficiency, is encouraging food manufacturers to invest in advanced automation solutions. Robotic systems, automated conveyors, machine vision technologies, AI-powered quality inspection platforms, and smart manufacturing solutions are increasingly replacing labor-intensive processes in many facilities. These technologies enable higher production throughput, improved traceability, reduced product waste, enhanced hygiene standards, and real-time monitoring of production operations. In addition, the integration of Industrial Internet of Things (IIoT), artificial intelligence, and predictive maintenance capabilities is transforming food manufacturing environments into highly connected and efficient smart factories, further accelerating the adoption of food automation solutions worldwide.

Key Market Trends & Insights

- North America dominated the Food Automation Market with the largest revenue share of 36.92% in 2025, driven by widespread adoption of industrial automation technologies, strong presence of leading food processing companies, increasing investments in smart manufacturing facilities, and rising demand for labor-efficient production systems. Growing implementation of robotics, AI-enabled processing equipment, and automated packaging solutions across the U.S. and Canada continues to strengthen the region’s leadership position.

- The Packaging and Repackaging segment dominated the market with a 34.12% share in 2025, due to its critical role in ensuring food safety, shelf-life extension, and compliance with hygiene standards.

- Asia-Pacific is expected to be the fastest-growing regional market at a CAGR of 8.9% from 2026 to 2033, fueled by rapid industrialization of food processing industries, expanding packaged food consumption, increasing automation investments, and growing food safety requirements across China, India, Japan, and Southeast Asia.

- The Linear Products segment is projected to register the fastest CAGR of 9.4% during the forecast period, driven by increasing deployment of precision motion systems in automated food handling, packaging, sorting, and inspection applications. Growing demand for high-speed production lines and enhanced operational efficiency is supporting segment growth.

- The Beverages segment dominated the application category with a revenue share of 27.63% in 2025, owing to extensive automation adoption in bottling, filling, labeling, packaging, and quality inspection processes. Rising global demand for soft drinks, functional beverages, dairy drinks, and alcoholic beverages continues to support automation investments within the segment.

- Processing accounted for the largest share of 34.58% in 2025 within the function segment, driven by increasing implementation of automated mixing, blending, cutting, cooking, and ingredient handling systems. Food manufacturers are investing heavily in automated processing technologies to improve productivity, consistency, and food safety compliance.

- Packaging and Repackaging is anticipated to be the fastest-growing function segment, registering a CAGR of 9.2% from 2026 to 2033, supported by growing demand for packaged food products, increasing adoption of robotic packaging systems, and rising focus on reducing operational costs while improving packaging accuracy and throughput.

Market Size & Forecast

- Global Market Value (2025): USD 8.56 Billion

- Expected Market Value (2033): USD 15.38 Billion

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Food Automation Market Segmentation

|

Attributes |

Food Automation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Siemens AG (Germany) |

|

Market Opportunities |

· Expansion of AI-Driven Smart Food Factories · Rising Demand for Robotic Packaging and High-Speed Processing Systems · Growth of Automation in Emerging Markets and SME Food Industries |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Food Automation Market Trends

Trend: Growth in Smart Manufacturing and AI-Driven Food Processing Automation

Food manufacturing companies are increasingly adopting high-level Food Automation systems to improve production efficiency, ensure consistent food quality, and reduce operational costs. The integration of AI-powered robotics, IoT-enabled sensors, and real-time production monitoring is enabling precise control over processing, packaging, and quality inspection. Food processing plants are leveraging automated production lines to handle large-scale demand in dairy, beverages, bakery, and meat industries while maintaining strict hygiene and safety standards. In addition, the growing use of predictive analytics and machine vision systems is helping manufacturers detect defects, optimize resource utilization, and minimize food wastage across global supply chains.

Food Automation Market Dynamics

Key Market Driver: Rising Demand for Large-Scale Automated Food Production and Supply Chain Efficiency

The rapid growth of global food consumption, coupled with increasing labor shortages and rising production costs, has created strong demand for advanced Food Automation systems. Food manufacturers are increasingly deploying robotics, automated processing equipment, and intelligent control systems to streamline production workflows and enhance output efficiency. According to industry estimates, automated food production lines can reduce operational costs by 20–35% while significantly improving product consistency and safety compliance. Companies across dairy, beverages, bakery, and packaged food sectors are adopting fully automated systems to meet rising demand from retail and e-commerce channels. The expansion of smart factories and Industry 4.0 initiatives is further accelerating the adoption of automation technologies across food manufacturing facilities worldwide.

Key Restraint/Challenge: High Capital Investment and Integration Complexity of Automation Systems

A significant challenge in the Food Automation Market is the high initial investment required for deploying advanced automation infrastructure. Modern food automation systems integrate robotics, AI-based control systems, precision sensors, and high-speed packaging machinery, requiring substantial capital expenditure for installation, maintenance, and system upgrades. In addition, integrating automation solutions with existing legacy production lines and ensuring compliance with stringent food safety regulations increases implementation complexity. Small and medium-sized food manufacturers often face financial and technical barriers, limiting large-scale adoption. Furthermore, ongoing maintenance costs, workforce training requirements, and system downtime risks add to the total cost of ownership, making adoption more challenging for cost-sensitive markets.

Key Market Opportunity: Expansion of AI-Enabled Smart Food Factories and Sustainable Automation Solutions

The integration of artificial intelligence, machine learning, and IoT technologies into Food Automation systems presents a major market opportunity. AI-enabled platforms can optimize production scheduling, monitor real-time quality control, and enable predictive maintenance, significantly improving operational efficiency. The development of smart food factories equipped with fully automated production lines is transforming the industry by enabling end-to-end digital control of manufacturing processes. In addition, increasing demand for sustainable food production practices is driving investment in energy-efficient automation systems and waste-reduction technologies. Emerging markets in Asia-Pacific, Latin America, and the Middle East are expected to witness strong growth as food manufacturers modernize production infrastructure to meet rising domestic demand and global export standards.

Food Automation Market Scope

The Food Automation market is segmented on the basis of type, application, and function.

- By Type

On the basis of type, the Food Automation Market is segmented into motors and generators, motor controls, discrete controllers and visualization, rotary products, linear products, and others. The Motor Controls segment dominated the market with a 32.64% share in 2025, driven by its extensive use in regulating and optimizing automated food processing equipment across production lines. These systems enable precise speed regulation, torque control, and energy-efficient operations in continuous manufacturing environments. Increasing deployment of PLC-based automation systems and smart motor control units across dairy, bakery, and meat processing industries is further strengthening segment dominance. Rising adoption of Industry 4.0 technologies and integration with IoT-enabled monitoring systems is improving operational efficiency and reducing downtime. Food manufacturers are increasingly investing in advanced motor control solutions to enhance productivity and maintain consistent product quality. Demand is also rising due to stringent food safety regulations requiring precise process control. Automation upgrades in large-scale production facilities are further supporting segment growth. Growing focus on energy optimization and predictive maintenance is also contributing to adoption. In addition, expanding adoption in emerging markets is accelerating market penetration. Strong demand from packaged food manufacturers continues to reinforce the leadership of this segment globally.

The Discrete Controllers and Visualization segment is expected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by rising adoption of smart automation interfaces and digital control systems. Increasing demand for real-time production monitoring and centralized control systems is boosting adoption. Food manufacturers are rapidly deploying HMI-based visualization tools for improved process transparency. Integration of AI and machine learning into control systems is enhancing predictive capabilities. Growing use of IoT-enabled sensors is enabling better data-driven decision-making. Cloud-based monitoring platforms are supporting remote access to production systems. Rising focus on smart factory transformation is accelerating segment growth. Demand for automated quality inspection systems is also increasing. Small and mid-sized food processors are adopting cost-efficient digital control solutions. Expanding investments in Industry 4.0 infrastructure are supporting deployment. Increasing need for reduced operational errors is further driving adoption. Overall, digital transformation in food manufacturing is a key growth driver for this segment.

- By Application

On the basis of application, the Food Automation Market is segmented into dairy, bakery, confectionery, fruit and vegetable, meat, poultry, and seafood, and beverages. The Meat, Poultry, and Seafood segment dominated the market with a 29.87% share in 2025, driven by high automation requirements in processing, cutting, sorting, and packaging operations. Increasing demand for hygienic and contamination-free processing is supporting adoption of automated systems. Strict food safety regulations are pushing manufacturers toward robotic processing lines. High-volume production needs in meat processing plants are accelerating automation deployment. Labor shortages in processing facilities are also encouraging robotic integration. Cold-chain automation requirements are further strengthening segment growth. Advanced vision systems are improving quality inspection accuracy. Automation helps reduce operational costs and increase throughput efficiency. Growing global consumption of processed protein products is reinforcing demand. Large-scale industrial food processors are heavily investing in robotics. Export-oriented meat industries are adopting automation for compliance. Technological advancements in robotic cutting and sorting systems are enhancing efficiency.

The Beverages segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by rising consumption of bottled and functional beverages globally. Increasing demand for high-speed filling and packaging lines is boosting automation adoption. Beverage manufacturers are investing in smart bottling and labeling systems. Expansion of soft drink and energy drink production is supporting market growth. Automation in mixing, filling, and capping processes is improving efficiency. Rising health-conscious consumer trends are driving product diversification. Smart factories in beverage plants are adopting AI-driven quality inspection systems. Increasing adoption of robotic palletizing systems is improving logistics efficiency. Growth of e-commerce beverage sales is accelerating automated packaging demand. Investments in sustainable beverage production lines are increasing. Emerging markets are witnessing rapid beverage industry expansion. Overall, modernization of beverage manufacturing facilities is driving strong growth.

- By Function

On the basis of function, the Food Automation Market is segmented into processing, packaging and repackaging, palletizing, sorting and grading, picking and placing, and others. The Packaging and Repackaging segment dominated the market with a 34.12% share in 2025, due to its critical role in ensuring food safety, shelf-life extension, and compliance with hygiene standards. Increasing adoption of automated sealing, wrapping, and labeling systems is driving segment growth. Food manufacturers are investing in high-speed packaging lines for large-scale production. Demand for flexible packaging solutions is further supporting automation adoption. Integration of robotic packaging arms is improving efficiency and consistency. Rising focus on reducing packaging waste is encouraging smart packaging systems. Automation in packaging helps reduce human contamination risks. Growing demand for ready-to-eat and packaged foods is strengthening segment leadership. Advanced vision inspection systems are improving packaging accuracy. Increasing use of AI-driven packaging optimization tools is boosting productivity. Expanding cold-chain logistics is further enhancing demand. Strong retail and export demand is reinforcing segment dominance globally.

The Picking and Placing segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by rapid adoption of AI-powered robotic systems. Increasing use of machine vision technologies is enabling precise handling of food products. Labor shortages in food manufacturing are accelerating automation deployment. Rising demand for high-speed sorting and packaging is boosting adoption. Collaborative robots are being widely used in food processing lines. Integration of smart sensors is improving accuracy in picking operations. Growing e-commerce food delivery is increasing automation needs. AI-based robotic arms are enhancing flexibility and efficiency. Automated warehouse systems are supporting faster order fulfillment. Demand for precision handling of delicate food items is rising. Investments in smart logistics infrastructure are increasing globally. Overall, digital transformation in food supply chains is driving strong growth.

Food Automation Market Regional Analysis

North America dominated the Food Automation Market and accounted for the largest revenue share of 36.92% in 2025, driven by widespread adoption of industrial automation technologies, strong presence of leading food processing companies, increasing investments in smart manufacturing facilities, and rising demand for labor-efficient production systems. The region benefits from advanced manufacturing infrastructure, high penetration of robotics in food processing lines, and early adoption of AI-enabled quality control systems. Growing implementation of automated packaging, sorting, and palletizing solutions across large-scale food production plants in the U.S. and Canada is further strengthening regional dominance. Increasing focus on food safety compliance, hygiene standards, and production efficiency is accelerating adoption of smart automation technologies. Rising labor cost pressures are encouraging manufacturers to deploy end-to-end automation systems. Strong presence of global automation vendors and system integrators is supporting technology deployment. Expanding use of IoT-enabled monitoring in food plants is improving operational visibility. Investments in smart factories and Industry 4.0 transformation initiatives are further boosting market growth. Continuous upgrades in processing and packaging automation are enhancing productivity. Demand for high-speed production lines in packaged food segments is reinforcing regional leadership. Overall, technological maturity and strong industrial base continue to sustain North America’s dominance.

U.S. Food Automation Market Insight

The U.S. Food Automation market is witnessing strong growth due to rising investments in advanced food processing technologies, automation-driven production systems, and smart manufacturing infrastructure. The country’s well-established food and beverage industry, along with high adoption of robotics, AI-based quality inspection systems, and automated packaging lines, is driving market expansion. Food manufacturers are increasingly focusing on reducing operational costs and improving production efficiency through end-to-end automation. Growing demand for packaged and processed food products is further accelerating adoption. In addition, strict food safety regulations from agencies such as the FDA are pushing companies toward advanced automated monitoring and traceability systems. Expansion of large-scale food processing facilities and warehouses is supporting deployment of robotic palletizing and sorting systems. Increasing use of machine vision in quality inspection is improving consistency and reducing wastage. Strong presence of leading automation solution providers is accelerating technology adoption. Rising labor shortages in the food processing sector are further encouraging automation investments. Integration of IoT and cloud-based monitoring platforms is enhancing real-time production control. Overall, the U.S. remains a key innovation hub for food automation technologies.

Europe Food Automation Market Insight

The Europe Food Automation market remains a major contributor to global revenue, driven by strong regulatory frameworks, advanced manufacturing capabilities, and increasing demand for sustainable food production systems. The region has a well-established food processing industry that is rapidly adopting robotics and automation technologies to improve efficiency and ensure compliance with strict hygiene and safety standards. Food manufacturers across Germany, France, Italy, and the Netherlands are investing heavily in automated processing and packaging systems. Increasing focus on reducing food waste and improving supply chain efficiency is further supporting market growth. Adoption of AI-powered production monitoring systems is enhancing operational accuracy and traceability. Rising labor costs and workforce shortages are accelerating automation deployment across food factories. Strong emphasis on sustainability is encouraging energy-efficient and resource-optimized production systems. Expansion of smart factories across Europe is driving integration of digital control systems. Increasing use of collaborative robots in food handling is improving flexibility in production lines. Growth in packaged and ready-to-eat food consumption is further boosting demand. Government initiatives supporting Industry 4.0 adoption are strengthening technological transformation. Overall, Europe continues to maintain a strong position due to innovation and regulatory support.

U.K. Food Automation Market Insight

The U.K. Food Automation market is experiencing steady growth, supported by increasing adoption of robotics in food processing, rising demand for packaged food products, and strong focus on manufacturing efficiency. Food companies in the country are investing in automated packaging, sorting, and quality inspection systems to reduce operational costs and improve productivity. Growing labor shortages in food manufacturing are further accelerating automation adoption. Integration of AI and machine vision technologies is improving accuracy in quality control processes. Increasing investment in smart factories and digital transformation initiatives is supporting market expansion. The U.K. benefits from strong presence of advanced food manufacturing companies and automation solution providers. Rising demand for traceability and food safety compliance is driving adoption of intelligent monitoring systems. Expansion of cold-chain logistics is further supporting automated handling systems. Growing use of robotics in bakery and beverage production is enhancing efficiency. Adoption of cloud-based production monitoring tools is improving operational visibility. Continuous innovation in food processing equipment is strengthening the industry. Overall, the U.K. is emerging as a key hub for advanced food automation adoption.

Germany Food Automation Market Insight

The Germany Food Automation market is expanding steadily due to the country’s strong industrial manufacturing base, advanced engineering capabilities, and high adoption of Industry 4.0 technologies. Food manufacturers are increasingly implementing robotics and automated systems across processing, packaging, and logistics operations. Strong focus on precision engineering and quality standards is driving deployment of advanced automation systems. Rising demand for efficiency and productivity in food production is encouraging investments in smart manufacturing facilities. Integration of AI-driven quality inspection systems is improving product consistency. Germany’s emphasis on sustainability is promoting energy-efficient automation solutions. Increasing use of robotic arms in food handling and packaging is enhancing operational speed. Strong presence of global automation equipment manufacturers is supporting technology deployment. Growth in export-oriented food production is reinforcing automation needs. Expansion of digital factories is improving real-time production monitoring. Labor shortages in industrial sectors are further accelerating automation adoption. Continuous innovation in robotics and control systems is strengthening market growth.

Asia-Pacific Food Automation Market Insight

The Asia-Pacific Food Automation market is expected to witness rapid growth, driven by increasing industrialization of food processing, rising demand for packaged food products, and expanding investments in automation technologies. Countries such as China, India, Japan, and South Korea are experiencing strong growth in food manufacturing capacity. Rising population and changing consumer lifestyles are boosting demand for processed and ready-to-eat foods. Food manufacturers are increasingly adopting robotics and automated packaging systems to improve efficiency and reduce costs. Rapid expansion of e-commerce food delivery is further supporting automation adoption in packaging and logistics. Government initiatives supporting smart manufacturing are accelerating Industry 4.0 adoption. Increasing focus on food safety and hygiene standards is driving investment in automated inspection systems. Growing presence of multinational food companies is boosting technology transfer. Rising labor cost pressures are encouraging automation deployment across production facilities. Expansion of cold-chain infrastructure is supporting automated handling systems. Increasing investments in smart factories are further strengthening market growth. Overall, Asia-Pacific is emerging as the fastest-growing region globally.

Japan Food Automation Market Insight

The Japan Food Automation market is witnessing steady growth due to strong technological advancement, high adoption of robotics, and increasing demand for efficient food production systems. The country’s well-developed manufacturing ecosystem is supporting integration of advanced automation technologies in food processing. Food companies are increasingly using robotics for packaging, sorting, and quality inspection. Rising labor shortages due to aging population are accelerating automation adoption. Strong focus on precision and quality is driving investment in AI-enabled monitoring systems. Integration of machine vision technologies is improving accuracy in food inspection. Japan’s emphasis on smart manufacturing is supporting digital transformation in food factories. Increasing demand for convenience and packaged foods is further boosting automation needs. Adoption of IoT-based monitoring systems is enhancing production efficiency. Growth in beverage and processed food industries is supporting automation deployment. Strong collaboration between technology providers and manufacturers is driving innovation. Overall, Japan continues to be a highly advanced and technology-driven market.

China Food Automation Market Insight

The China Food Automation market is growing rapidly, driven by large-scale industrial expansion, rising consumption of processed foods, and strong government support for smart manufacturing initiatives. Food manufacturers are increasingly investing in automated production lines to improve efficiency and meet rising demand. Growing adoption of robotics in packaging, sorting, and processing is significantly boosting productivity. Expansion of e-commerce and food delivery services is increasing demand for automated packaging systems. Strong focus on food safety regulations is driving adoption of advanced inspection technologies. Increasing labor cost pressures are encouraging large-scale automation deployment. Rapid urbanization and changing dietary habits are supporting growth in packaged food consumption. Rising investments in AI-enabled manufacturing systems are enhancing production efficiency. Expansion of domestic food processing companies is strengthening market development. Government initiatives promoting Industry 4.0 are accelerating digital transformation. Increasing use of smart logistics and cold-chain systems is improving supply chain efficiency. Overall, China is emerging as one of the fastest-growing and most dynamic markets globally.

Food Automation Market Share

The Food Automation industry is primarily led by well-established companies, including:

- Siemens AG (Germany)

- ABB Ltd. (Switzerland)

- Rockwell Automation Inc. (U.S.)

- Schneider Electric SE (France)

- Mitsubishi Electric Corporation (Japan)

- Omron Corporation (Japan)

- Yaskawa Electric Corporation (Japan)

- Emerson Electric Co. (U.S.)

- Honeywell International Inc. (U.S.)

- Bosch Rexroth AG (Germany)

- KUKA AG (Germany)

- FANUC Corporation (Japan)

- Tetra Pak International S.A. (Switzerland)

- Marel hf. (Iceland)

- JBT Corporation (U.S.)

- Alfa Laval AB (Sweden)

- GEA Group AG (Germany)

- Sidel Group (France)

- B&R Industrial Automation GmbH (Austria)

- Endress+Hauser Group (Switzerland)

- Key Technology Inc. (U.S.)

- Syntegon Technology GmbH (Germany)

- Ishida Co. Ltd. (Japan)

- Bühler Group (Switzerland)

- Lenze SE (Germany)

- Beckhoff Automation GmbH & Co. KG (Germany)

- Fortive Corporation (U.S.)

- Pentair plc (U.K.)

- Valmet Oyj (Finland)

- Duravant LLC (U.S.)

- Coesia S.p.A. (Italy)

- Barry-Wehmiller Companies Inc. (U.S.)

- Illinois Tool Works Inc. (U.S.)

- Rexnord Corporation (U.S.)

- Hitachi Industrial Equipment Systems Co., Ltd. (Japan)

- Toshiba Infrastructure Systems & Solutions (Japan)

- Siemens Food & Beverage Automation (Germany)

Latest Developments in Food Automation Market

- In September 2021, Soft Robotics Inc. announced the launch of SoftAI™ solutions, an AI-powered robotic automation platform designed to accelerate food processing automation. The system integrates machine vision, artificial intelligence, and soft-gripping robotics to handle delicate food items such as bakery products, meat, and fresh produce. The solution enables food manufacturers to improve pick-and-place efficiency, reduce labor dependency, and enhance production consistency. This launch highlights the growing adoption of AI-driven automation technologies in food manufacturing to address labor shortages and productivity challenges

- In January 2022, Pazzi Robotics introduced its fully automated kitchen and restaurant automation system in Paris, expanding the use of end-to-end robotics in food preparation and service operations. The system uses robotic arms and AI-driven cooking modules to prepare pizzas without human intervention, covering ordering, cooking, and delivery processes. This development reflects the increasing commercialization of fully automated food service models and the integration of robotics into consumer-facing food operations

- In April 2023, Doosan Robotics launched its NSF-certified E-Series collaborative robots (cobots) designed specifically for the food and beverage industry. These robots feature hygienic design standards, sealed joints, and flexible configurations for food handling tasks such as packaging, sorting, and processing. The launch strengthens automation adoption in food manufacturing by enabling safer human-robot collaboration and improving compliance with food safety regulations across production environment

- In April 2023, KUKA Robotics, in collaboration with system partner Projx, showcased advanced food and beverage automation solutions at FoodEx 2023, including robotic pick-and-place and processing systems. These solutions demonstrated how industrial robots can improve efficiency, hygiene, and consistency in food production workflows. The development highlights increasing integration of robotics, vision systems, and AI-based control in food processing automation systems

- In July 2024, Chef Robotics launched its AI-powered food robotics platform (ChefOS-based system) designed to automate large-scale food production tasks such as ingredient handling and meal assembly. The system uses machine learning and computer vision to adapt to different food types and production environments, helping manufacturers address labor shortages and scale production efficiency. This launch demonstrates the rising role of AI-enabled adaptive robotics in industrial food automation facilities

- In July 2025, ABB announced the expansion of its industrial robotics portfolio with new robot families (Lite+, PoWa, IRB 1200 series) targeting mid-market manufacturing sectors, including food and beverage production. These robots are designed for flexible deployment in packaging, handling, and light processing applications with improved AI-driven usability and faster setup times. The development reflects the growing shift toward accessible, scalable automation solutions in food manufacturing and processing industries

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Food Automation Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Food Automation Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Food Automation Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.