Global Food Grade Polyols Market

Market Size in USD Billion

USD

6.03 Billion

USD

11.59 Billion

2024

2032

USD

6.03 Billion

USD

11.59 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.03 Billion | |

| USD 11.59 Billion | |

| % | |

|

Food Grade Polyols Market Size

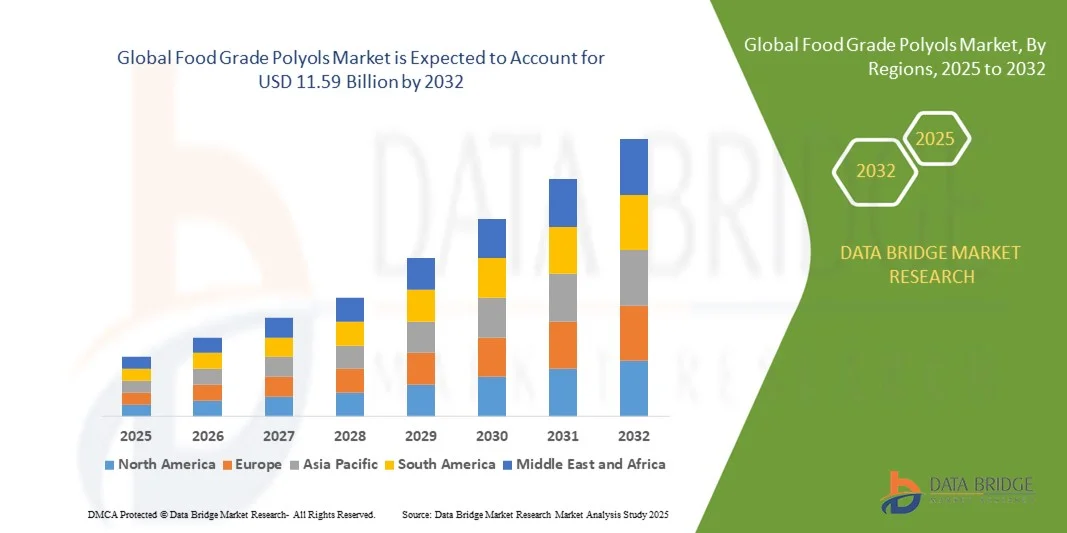

- The global food grade polyols market size was valued at USD 6.03 billion in 2024 and is expected to reach USD 11.59 billion by 2032, at a CAGR of 8.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for low-calorie and sugar-free food and beverage products, driven by rising health awareness and growing incidence of diabetes and obesity

- Rising adoption of polyols in confectionery, bakery, dairy, and beverage applications is further supporting market expansion, owing to their ability to provide sweetness without the caloric impact of traditional sugars

Food Grade Polyols Market Analysis

- Growing consumer preference for healthier diets and sugar-reduced products is driving innovation and formulation of polyol-based alternatives

- Expanding use of polyols in functional foods, beverages, and specialty dietary products is opening new growth avenues and increasing market penetration across regions

- North America dominated the food grade polyols market with the largest revenue share of 38.75% in 2024, driven by increasing demand for low-calorie, sugar-free, and functional food products, as well as rising health awareness among consumers

- Asia-Pacific region is expected to witness the highest growth rate in the global food grade polyols market, driven by rapid urbanization, growing demand for sugar-free and low-calorie products, and supportive government initiatives promoting healthier diets

- The sugarcane and molasses segment held the largest market revenue share in 2024, driven by the wide availability of raw materials and cost-effective production processes. Polyols derived from sugarcane and molasses are highly versatile, offering consistent sweetness, bulk, and moisture retention, making them a preferred choice for manufacturers across various food and beverage applications

Report Scope and Food Grade Polyols Market Segmentation

|

Attributes |

Food Grade Polyols Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Food Grade Polyols Market Trends

Increasing Adoption of Polyols in Sugar-Free and Low-Calorie Products

- The growing shift toward polyols in food and beverage applications is transforming the sugar-reduction landscape by enabling low-calorie, sugar-free alternatives. The versatility of polyols allows manufacturers to maintain sweetness, texture, and taste while reducing caloric content, meeting the demands of health-conscious consumers and diabetics. In addition, polyols help in maintaining product stability, enhancing shelf-life, and supporting clean-label trends that appeal to modern consumers

- Rising demand for sugar-free products in confectionery, bakery, dairy, and beverage industries is accelerating the adoption of polyols. These ingredients are particularly effective in delivering bulk, sweetness, and moisture retention without the negative effects of traditional sugars, supporting product innovation and variety. This adoption is further encouraged by consumers’ preference for functional foods that offer health benefits without compromising on taste or indulgence

- The functional benefits of polyols, such as low glycemic index, non-cariogenic properties, and compatibility with clean-label formulations, are making them attractive for manufacturers. Polyols also contribute to product stability and shelf-life enhancement, improving overall consumer satisfaction. In addition, their ability to blend with other natural sweeteners offers formulation flexibility for diverse product lines

- For instance, in 2023, several European and North American confectionery companies reported successful launches of sugar-free chocolate and bakery items using erythritol and maltitol, which maintained taste and texture while reducing calories and sugar content. The successful integration of polyols in multiple product categories reinforced their commercial viability and encouraged further research and product development initiatives

- While polyols are accelerating the shift toward healthier food products, their impact depends on continued innovation, regulatory approval, and cost competitiveness. Manufacturers must focus on product-specific formulations and scalable solutions to fully leverage market potential. In addition, partnerships with ingredient suppliers and investment in consumer education campaigns can further drive market penetration and acceptance

Food Grade Polyols Market Dynamics

Driver

Rising Health Awareness and Demand for Sugar Reduction

- Increasing awareness about obesity, diabetes, and other lifestyle-related diseases is pushing both consumers and manufacturers to adopt sugar alternatives such as polyols. The demand for healthier sweeteners is boosting R&D investments and product launches across functional food segments. Moreover, evolving dietary guidelines and health campaigns are reinforcing consumer preference for reduced-sugar and low-calorie products

- Food and beverage manufacturers are increasingly aware of the dual benefits of polyols—taste preservation and calorie reduction—which are driving wider adoption across bakery, confectionery, dairy, and beverage industries. This trend aligns with evolving consumer preferences and regulatory guidelines promoting reduced sugar intake. In addition, manufacturers are leveraging polyols to develop innovative formats, flavors, and textures that meet the expectations of modern consumers

- Government initiatives and health campaigns advocating sugar reduction are further supporting polyol usage. Policies encouraging healthier diets and front-of-pack labeling are creating an enabling environment for polyol adoption globally. Incentives, subsidies, and partnerships with food associations are also contributing to the accelerated adoption of polyols in commercial and industrial food production

- For instance, in 2022, several North American and European food companies reformulated popular confectionery and snack products with polyols, resulting in increased market penetration and improved consumer trust. The reformulations not only reduced sugar content but also allowed companies to market products as healthier, catering to a growing health-conscious demographic and strengthening brand reputation

- While demand and awareness are strong, there is still a need to address cost, formulation compatibility, and consumer sensory acceptance to ensure long-term adoption and sustained market growth. In addition, ongoing product education and marketing initiatives are essential to bridge the knowledge gap and drive wider acceptance in emerging regions

Restraint/Challenge

High Cost of Polyols and Limited Consumer Awareness in Emerging Markets

- The higher cost of polyols compared to traditional sugars limits adoption, especially among small and mid-sized food manufacturers in price-sensitive regions. Cost remains a significant barrier to large-scale usage and reformulation efforts. This challenge is compounded by import dependency and fluctuating raw material prices, which increase overall production costs

- In many emerging markets, limited consumer understanding of polyols and their benefits reduces demand. Lack of education on sugar alternatives can hinder widespread adoption despite the availability of polyol-based products. This also impacts manufacturers’ willingness to invest in reformulation and marketing efforts in these regions, slowing market growth

- Supply chain and availability issues, including sourcing of specialty polyols and storage requirements, further restrict market penetration in developing regions. Dependence on imports for high-quality polyols adds to production costs and delays. In addition, logistical challenges in maintaining product stability and compliance with local food safety regulations exacerbate market entry barriers

- For instance, in 2023, several small-scale bakery and confectionery manufacturers in Southeast Asia reported limited access to erythritol and maltitol, citing cost and supply chain gaps as primary barriers. These limitations hinder timely production, product launches, and scaling opportunities, affecting overall market expansion in the region

- While polyol technologies continue to evolve, addressing affordability, availability, and consumer education remains crucial. Market stakeholders must focus on localized production, scalable supply chains, and awareness campaigns to unlock long-term growth. In addition, strategic partnerships, cost-optimization techniques, and innovation in polyol blends can enhance accessibility and stimulate adoption across both developed and emerging markets

Food Grade Polyols Market Scope

The market is segmented on the basis of source, application, and functionality.

- By Source

On the basis of source, the food grade polyols market is segmented into sugarcane and molasses, grains, fruits, and others. The sugarcane and molasses segment held the largest market revenue share in 2024, driven by the wide availability of raw materials and cost-effective production processes. Polyols derived from sugarcane and molasses are highly versatile, offering consistent sweetness, bulk, and moisture retention, making them a preferred choice for manufacturers across various food and beverage applications.

The grains segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by technological advancements in enzymatic conversion and extraction methods. Grain-derived polyols are gaining popularity due to their functional benefits, clean-label compatibility, and suitability for sugar-free, low-calorie, and diabetic-friendly products, making them increasingly adopted in both commercial and industrial food production.

- By Application

On the basis of application, the market is segmented into food, healthcare and pharmaceutical, and beverages. The food segment captured the largest market share in 2024, attributed to rising demand for sugar-free, low-calorie, and functional food products. Polyols are extensively used in bakery, confectionery, and dairy applications, helping maintain taste, texture, and shelf-life while supporting healthier formulations.

The healthcare and pharmaceutical segment is projected to witness the fastest growth from 2025 to 2032, driven by the increasing incorporation of polyols in tablets, syrups, and nutraceuticals. Their non-cariogenic, low-calorie, and stabilizing properties make them ideal for sugar-free formulations in medical and nutritional products.

- By Functionality

On the basis of functionality, the market is segmented into preservative, coloring or flavouring agent, coatings, and others. The coatings segment accounted for the largest market share in 2024, driven by polyols’ ability to enhance product texture, gloss, and shelf-life in confectionery and bakery applications.

The flavoring agent segment is expected to register the highest growth rate from 2025 to 2032, owing to the rising demand for sugar-free and clean-label products with improved taste profiles. Polyols function as effective carriers for flavors and sweeteners, enabling manufacturers to create innovative and appealing formulations across food, beverage, and pharmaceutical products.

Food Grade Polyols Market Regional Analysis

- North America dominated the food grade polyols market with the largest revenue share of 38.75% in 2024, driven by increasing demand for low-calorie, sugar-free, and functional food products, as well as rising health awareness among consumers

- Consumers in the region highly value the benefits of polyols, such as low glycemic index, non-cariogenic properties, and clean-label compatibility, which are increasingly incorporated in confectionery, bakery, dairy, and beverage applications

- This widespread adoption is further supported by high disposable incomes, a health-conscious population, and government initiatives promoting sugar reduction and healthier diets, establishing polyols as a preferred sugar alternative across food and beverage segments

U.S. Food Grade Polyols Market Insight

The U.S. food grade polyols market captured the largest revenue share in 2024 within North America, fueled by growing adoption in sugar-free confectionery, bakery, and beverage products. Manufacturers are increasingly prioritizing healthier formulations to meet consumer demand for reduced-calorie and low-sugar options. The rising focus on functional ingredients, combined with the expansion of clean-label and diabetic-friendly products, further drives market growth. Moreover, government guidelines on sugar reduction and front-of-pack labeling are significantly contributing to increased polyol adoption across the country.

Europe Food Grade Polyols Market Insight

The Europe food grade polyols market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by rising consumer awareness of obesity and diabetes, coupled with regulatory support for sugar reduction initiatives. The demand for sugar-free and low-calorie products in bakery, confectionery, and beverages is accelerating polyol adoption. European consumers are also drawn to clean-label, non-cariogenic, and functional ingredients, supporting market expansion in both retail and foodservice applications.

U.K. Food Grade Polyols Market Insight

The U.K. food grade polyols market is expected to witness rapid growth from 2025 to 2032, driven by increasing health-consciousness and preference for sugar-free and low-calorie food products. Consumer demand for healthier alternatives, combined with government policies encouraging reduced sugar consumption, is boosting polyol usage. The rising popularity of functional foods and beverages, alongside expanding food innovation and reformulation trends, is expected to sustain market growth in the U.K.

Germany Food Grade Polyols Market Insight

The Germany food grade polyols market is expected to witness significant growth from 2025 to 2032, fueled by growing awareness of sugar reduction, rising prevalence of diabetes, and a strong food innovation ecosystem. German consumers increasingly prefer functional, sugar-free, and low-calorie products, supporting polyol adoption across bakery, confectionery, and beverage applications. Moreover, stringent labeling regulations and health campaigns promoting reduced sugar intake are further driving market expansion.

Asia-Pacific Food Grade Polyols Market Insight

The Asia-Pacific food grade polyols market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid urbanization, rising disposable incomes, and increasing adoption of sugar-free and low-calorie products in countries such as China, Japan, and India. Growing health awareness, along with government initiatives promoting healthier diets, is accelerating polyol adoption across food, beverage, and pharmaceutical segments. Furthermore, as APAC emerges as a manufacturing hub for polyols, affordability and accessibility are expanding to a broader consumer base.

Japan Food Grade Polyols Market Insight

The Japan food grade polyols market is expected to witness rapid growth from 2025 to 2032 due to the country’s high focus on health, longevity, and dietary management. Japanese consumers are increasingly seeking sugar-free and low-calorie alternatives, supporting polyol usage in confectionery, dairy, and functional food products. Moreover, government campaigns promoting healthier eating habits, combined with the rising number of functional and clean-label products, are driving market growth.

China Food Grade Polyols Market Insight

The China food grade polyols market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s growing middle class, increasing health awareness, and strong demand for sugar-free and low-calorie food and beverage products. China stands as one of the largest markets for polyols, with rising incorporation in bakery, confectionery, and beverage segments. The expanding production capabilities, presence of domestic manufacturers, and initiatives promoting sugar reduction and functional foods are key factors propelling the market in China.

Food Grade Polyols Market Share

The Food Grade Polyols Market industry is primarily led by well-established companies, including:

• Cargill, Incorporated (U.S.)

• ADM (U.S.)

• Roquette Frères (France)

• MGP (U.S.)

• Wilmar International Ltd (Singapore)

• Manildra Group (Australia)

• A. B. Enterprises (U.K.)

• AVATAR CORPORATION (India)

• Tereos (France)

• Gulshan Polyols Ltd. (India)

• TREDIS (India)

• Gujarat Ambuja Exports Limited (India)

• Sunar Misir (India)

• Tata Chemicals Ltd. (India)

• Shandong Futaste Co. (China)

• Jungbunzlauer Suisse AG (Switzerland)

• Cristalco (France)

• Grain Processing Corporation (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Food Grade Polyols Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Food Grade Polyols Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Food Grade Polyols Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.