Global Food Inclusions Market

Market Size in USD Billion

USD

14.99 Billion

USD

28.66 Billion

2025

2033

USD

14.99 Billion

USD

28.66 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.99 Billion | |

| USD 28.66 Billion | |

| % | |

|

Food Inclusions Market Overview

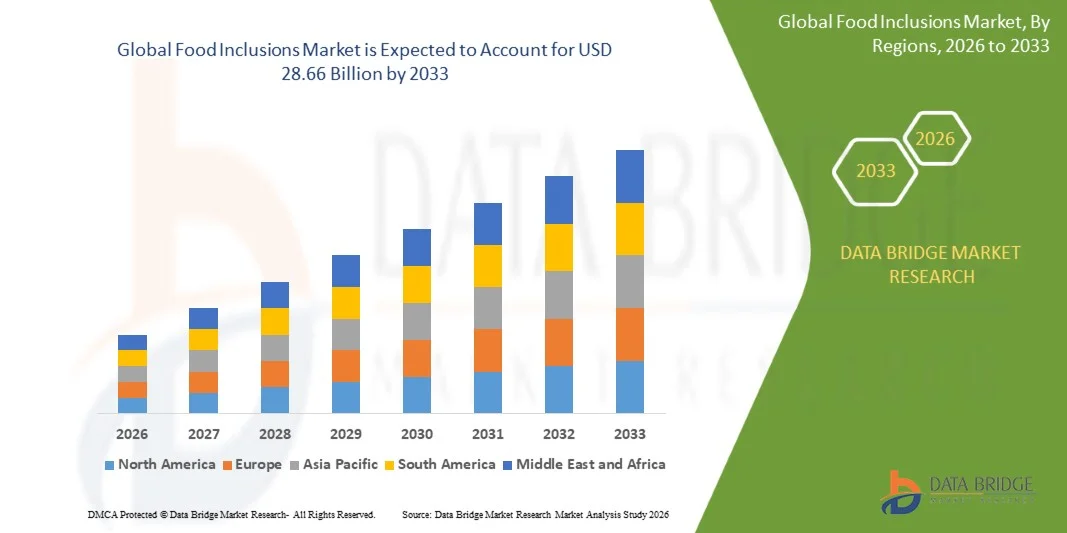

The global food inclusions market was valued at USD 14.99 billion in 2025 and is projected to reach USD 28.66 billion by 2033, growing at a CAGR of 8.44% from 2026 to 2033. The market is experiencing strong growth driven by rising demand for premium and visually appealing food products, increasing consumption of bakery and confectionery items, and expanding applications of inclusions across dairy, snacks, cereals, and frozen desserts. Growing consumer preference for innovative textures, flavors, and indulgent eating experiences is encouraging food manufacturers to incorporate ingredients such as chocolate chips, nuts, fruits, caramel, and flavored pieces into a wide range of processed food products.

The increasing demand for convenience foods and ready-to-eat snacks globally, combined with rapid product innovation in the food and beverage sector, is accelerating adoption of food inclusions across industrial food processing applications. Manufacturers are increasingly utilizing natural, clean-label, and functional inclusions to improve product differentiation, nutritional value, and visual appeal. In addition, rising health consciousness among consumers is supporting demand for fruit-, nut-, and protein-based inclusions in cereals, yogurt, energy bars, and plant-based food products. Technological advancements in freeze-drying, flavor encapsulation, and ingredient stabilization are further enhancing the shelf life, texture retention, and functionality of food inclusions across global food manufacturing industries

Key Market Trends & Insights

- North America dominated the food inclusions market with the largest revenue share of in 2025, supported by strong demand for premium bakery, confectionery, dairy, and snack products enriched with innovative texture and flavor ingredients.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of from 2026 to 2033. Growth is driven by rapid urbanization, rising disposable incomes, and increasing consumption of processed and convenience foods across countries such as China, Japan, and India.

- The Chocolate segment held the largest market revenue share of approximately 36.9% in 2025 driven by its extensive use across bakery products, ice creams, confectionery items, cookies, and premium desserts. Manufacturers increasingly prefer chocolate inclusions due to strong consumer demand for indulgent flavors, texture enhancement, and premium product positioning across packaged food categories.

- The Fruit and Nut segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by rising consumer preference for natural, protein-rich, and clean-label ingredients. Increasing demand for functional snacks, granola bars, breakfast cereals, and healthy bakery products is accelerating adoption of dried fruit and nut inclusions globally.

- The Solid and Semi-Solid segment accounted for the largest market revenue share of nearly 71.5% in 2025 driven by widespread utilization in chocolates, cookies, cereal bars, frozen desserts, and dairy applications. Solid inclusions provide improved texture, visual appeal, and flavor consistency, making them highly suitable for large-scale processed food manufacturing operations.

- The Liquid segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033 due to increasing usage in flavored beverages, dessert fillings, syrups, dairy products, and ready-to-eat applications. Rising innovation in flavored sauces, caramel fillings, and fruit-based liquid inclusions is supporting segment expansion across premium food categories.

- The Chocolate and Caramel segment dominated the market with a revenue share of approximately 42.6% in 2025 driven by strong consumer demand for rich indulgent flavors in confectionery, bakery, and frozen dessert products. Premiumization trends and increasing launches of gourmet desserts and chocolates are further strengthening segment growth globally.

- The Fruit Flavours segment is anticipated to register the fastest growth at a CAGR of 9.1% during the forecast period due to rising preference for refreshing, natural, and clean-label flavor profiles. Increasing demand for tropical fruit inclusions in yogurts, beverages, cereal products, and snack bars is supporting strong segment expansion among health-conscious consumers.

- The Bakery Products segment held the largest market revenue share of approximately 31.8% in 2025 driven by growing consumption of premium cakes, pastries, muffins, cookies, and artisanal baked goods containing chocolate chips, fruit pieces, caramel, and nut inclusions. Rising urbanization and increasing preference for convenient indulgent snacks are supporting sustained segment demand.

- The Dairy and Frozen Desserts segment is projected to witness the fastest CAGR of 9.7% from 2026 to 2033 driven by increasing demand for premium ice creams, flavored yogurts, frozen snacks, and dairy-based desserts with enhanced texture and flavor combinations. Manufacturers are increasingly incorporating innovative inclusions such as cookie chunks, fruit swirls, and caramel fillings to improve product differentiation and consumer appeal.

Market Size & Forecast

- Global Market Value (2025): USD 14.99 Billion

- Expected Market Value (2033): USD 28.66 Billion

- Forecast CAGR (2026–2033): 8.44%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Food Inclusions Market Segmentation

|

Attributes |

Food Inclusions Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Sensient Colors LLC (U.S.) |

|

Market Opportunities |

• Rising Demand For Clean-Label And Functional Food Ingredients |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Food Inclusions Market Trends

Trend: Rising Demand For Premium Texture And Functional Ingredient Innovation

Increasing consumer preference for indulgent, visually appealing, and multi-texture food products is driving strong demand for advanced food inclusions across bakery, dairy, confectionery, cereals, and snack industries. Traditional processed food products are increasingly being enhanced with chocolate chips, flavored nuts, fruit pieces, caramel chunks, cookie bits, and protein inclusions to improve taste, texture, and product differentiation in highly competitive food markets.

Food manufacturers are actively incorporating natural and functional inclusions, For instance freeze-dried fruits, plant-based protein crisps, and probiotic inclusions, to align with growing clean-label and health-conscious consumption trends. In bakery and confectionery applications, inclusions are being widely used to create premium sensory experiences and customized flavor combinations that appeal to younger consumers seeking innovative food products.

The rapid expansion of ready-to-eat snacks, premium ice creams, and fortified breakfast cereals is also increasing demand for stable and visually attractive food inclusions capable of maintaining texture and flavor consistency during processing and storage. In addition, the global growth of artisanal and premium food categories continues to encourage manufacturers to launch limited-edition and seasonal inclusion-based products across retail and foodservice channels. Industry product launches during 2025 integrating high-protein cookie inclusions and fruit-based superfood pieces into cereal and snack bars demonstrated nearly 12–15% higher consumer engagement compared to standard formulations in premium retail categories.

Global Food Inclusions Market Dynamics

Key Market Driver: Rising Demand For Premium And Functional Processed Food Products

Consumers worldwide are increasingly seeking premium food experiences that combine indulgence, convenience, nutrition, and visual appeal. Food inclusions are becoming essential ingredients across processed food manufacturing because they improve flavor complexity, texture contrast, appearance, and product customization while supporting premium product positioning.

Industries such as bakery, dairy, cereals, confectionery, and frozen desserts are increasingly utilizing inclusions to enhance consumer appeal and support product innovation strategies. Manufacturers are actively incorporating inclusions, For instance chocolate chunks, fruit preparations, granola crisps, and nut blends, into yogurts, cakes, protein bars, and ice cream products to attract health-conscious and younger consumer demographics.

Similarly, plant-based food manufacturers are integrating functional inclusions containing proteins, fibers, and probiotics into alternative dairy and snack products to improve nutritional value and sensory appeal. Real-world product launches across Europe and North America during 2024 integrating freeze-dried berry inclusions into yogurt and breakfast cereals reported sales growth improvements of approximately 8–10% in premium retail food categories.

Key Restraint/Challenge: High Ingredient Costs And Shelf-Life Stability Issues

Food inclusions often require specialized processing technologies, temperature-controlled storage, and advanced stabilization methods to maintain texture, moisture balance, flavor integrity, and visual quality during food manufacturing and distribution. Sensitive ingredients such as fruits, nuts, chocolates, and flavored inclusions can experience degradation, moisture migration, and texture loss under varying processing conditions.

In addition, fluctuating raw material prices for cocoa, nuts, dairy ingredients, and fruit concentrates increase manufacturing costs and create pricing challenges for food producers operating in cost-sensitive markets. Complex supply chains and stringent food safety regulations further increase operational complexity for manufacturers seeking consistent ingredient quality and long shelf-life stability.

Commercial industry assessments indicate that premium freeze-dried fruit and chocolate inclusions can increase overall product manufacturing costs by approximately 15–20% compared to standard processed food formulations, limiting affordability across certain mass-market food applications.

Key Market Opportunity: Expansion Of Clean-Label, Plant-Based, And Personalized Nutrition Products

Modern consumers increasingly demand clean-label, organic, protein-rich, and customized food products that provide both nutritional benefits and enhanced eating experiences. Food inclusions are emerging as critical ingredients in supporting personalized nutrition trends by enabling manufacturers to create differentiated products with unique flavor, texture, and health-focused characteristics.

Food companies are increasingly exploring inclusion technologies, For instance plant-protein crisps, superfood blends, functional seeds, and probiotic inclusions, to improve nutritional profiles across snacks, cereals, bakery products, and dairy alternatives. In sports nutrition and wellness food applications, manufacturers are utilizing nutrient-dense inclusions to improve product functionality while maintaining premium taste and texture experiences.

In addition, advancements in encapsulation technology, freeze-drying methods, and sugar-reduction ingredient systems are improving inclusion stability and expanding opportunities across vegan desserts, fortified snacks, and low-sugar confectionery products in Asia-Pacific and North America. Consumer product testing programs conducted during 2025 across functional snack categories reported flavor acceptance and texture satisfaction improvements of nearly 10–14% after integrating customized protein and fruit-based food inclusions into health-oriented formulations.

Global Food Inclusions Market Scope

The market is segmented on the basis of type, form, flavour, and application.

• By Type

On the basis of type, the food inclusions market is segmented into Chocolate, Fruit and Nut, Cereal, Flavored Sugar and Caramel, Confectionery, and Other. The Chocolate segment held the largest market revenue share of approximately 36.9% in 2025 driven by its extensive use across bakery products, ice creams, confectionery items, cookies, and premium desserts. Manufacturers increasingly prefer chocolate inclusions due to strong consumer demand for indulgent flavors, texture enhancement, and premium product positioning across packaged food categories.

The Fruit and Nut segment is projected to register the fastest growth at a CAGR of 9.4% from 2026 to 2033, driven by rising consumer preference for natural, protein-rich, and clean-label ingredients. Increasing demand for functional snacks, granola bars, breakfast cereals, and healthy bakery products is accelerating adoption of dried fruit and nut inclusions globally.

• By Form

On the basis of form, the food inclusions market is segmented into Solid and Semi-Solid, and Liquid. The Solid and Semi-Solid segment accounted for the largest market revenue share of nearly 71.5% in 2025 driven by widespread utilization in chocolates, cookies, cereal bars, frozen desserts, and dairy applications. Solid inclusions provide improved texture, visual appeal, and flavor consistency, making them highly suitable for large-scale processed food manufacturing operations.

The Liquid segment is expected to witness the fastest CAGR of 8.9% from 2026 to 2033 due to increasing usage in flavored beverages, dessert fillings, syrups, dairy products, and ready-to-eat applications. Rising innovation in flavored sauces, caramel fillings, and fruit-based liquid inclusions is supporting segment expansion across premium food categories.

• By Flavour

On the basis of flavour, the food inclusions market is segmented into Fruit Flavours, Nut, Savory, and Chocolate and Caramel. The Chocolate and Caramel segment dominated the market with a revenue share of approximately 42.6% in 2025 driven by strong consumer demand for rich indulgent flavors in confectionery, bakery, and frozen dessert products. Premiumization trends and increasing launches of gourmet desserts and chocolates are further strengthening segment growth globally.

The Fruit Flavours segment is anticipated to register the fastest growth at a CAGR of 9.1% during the forecast period due to rising preference for refreshing, natural, and clean-label flavor profiles. Increasing demand for tropical fruit inclusions in yogurts, beverages, cereal products, and snack bars is supporting strong segment expansion among health-conscious consumers.

• By Application

On the basis of application, the food inclusions market is segmented into Cereal Products, Snacks and Bars, Bakery Products, Dairy and Frozen Desserts, Chocolate and Confectionery Products, and Other. The Bakery Products segment held the largest market revenue share of approximately 31.8% in 2025 driven by growing consumption of premium cakes, pastries, muffins, cookies, and artisanal baked goods containing chocolate chips, fruit pieces, caramel, and nut inclusions. Rising urbanization and increasing preference for convenient indulgent snacks are supporting sustained segment demand.

The Dairy and Frozen Desserts segment is projected to witness the fastest CAGR of 9.7% from 2026 to 2033 driven by increasing demand for premium ice creams, flavored yogurts, frozen snacks, and dairy-based desserts with enhanced texture and flavor combinations. Manufacturers are increasingly incorporating innovative inclusions such as cookie chunks, fruit swirls, and caramel fillings to improve product differentiation and consumer appeal.

Global Food Inclusions Market Regional Analysis

• North America dominated the food inclusions market with the largest revenue share of 38.74% in 2025, driven by strong demand for premium bakery, confectionery, dairy, and snack products enriched with innovative texture and flavor ingredients

• Consumers in the region highly value indulgent food experiences, clean-label ingredients, and functional inclusions such as nuts, fruits, chocolate chips, caramel, and cereal blends across packaged food products

• This widespread adoption is further supported by high consumption of convenience foods, strong presence of large food processing companies, and increasing demand for premium ready-to-eat snacks, establishing food inclusions as an essential ingredient category across commercial food manufacturing applications

U.S. Food Inclusions Market Insight

The U.S. food inclusions market captured the largest revenue share in 2025 within North America, fueled by increasing demand for premium bakery products, protein snacks, frozen desserts, and customized confectionery products. Consumers are increasingly seeking innovative textures and flavor combinations in packaged foods, encouraging manufacturers to launch products containing fruit pieces, chocolate chunks, nuts, and caramel inclusions. The growing popularity of clean-label and plant-based foods, combined with rising demand for functional snack products, is further propelling the market. Moreover, strong innovation in premium desserts, cereals, and dairy products is significantly contributing to industry expansion.

Europe Food Inclusions Market Insight

The Europe food inclusions market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing demand for artisanal bakery products, premium confectionery, and healthier snacking options. The rising preference for natural ingredients, coupled with growing consumption of organic and clean-label foods, is fostering the adoption of high-quality food inclusions across the region. European consumers are also attracted toward innovative flavor profiles and texture-rich products in chocolates, yogurts, and desserts. The market is experiencing strong growth across bakery, cereal, dairy, and frozen dessert applications, supported by continuous product innovation and premiumization trends.

U.K. Food Inclusions Market Insight

The U.K. food inclusions market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing consumption of premium snacks, desserts, and bakery products with enhanced texture and flavor appeal. Rising consumer preference for indulgent yet healthier food products is encouraging manufacturers to incorporate nuts, fruits, seeds, and chocolate inclusions into various applications. In addition, growing demand for convenient on-the-go snacks, protein bars, and innovative breakfast products is accelerating market expansion. The country’s strong retail infrastructure and rapid product launches in confectionery and bakery categories are expected to continue supporting growth.

Germany Food Inclusions Market Insight

The Germany food inclusions market is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for functional foods, premium confectionery products, and clean-label bakery applications. Germany’s highly developed food processing industry, combined with strong consumer preference for high-quality and sustainable ingredients, is promoting adoption of innovative inclusion products across dairy, cereal, and snack categories. The integration of fruit, nut, and chocolate inclusions into protein-rich and organic food products is becoming increasingly prevalent. Furthermore, increasing investment in healthier snacking and premium packaged food innovation is supporting long-term market growth.

Asia-Pacific Food Inclusions Market Insight

The Asia-Pacific food inclusions market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and increasing consumption of processed and convenience foods across countries such as China, Japan, and India. The region’s growing demand for premium bakery products, chocolates, frozen desserts, and cereal snacks is accelerating the adoption of food inclusions. Furthermore, expanding western food consumption patterns, rising middle-class population, and strong growth in foodservice and retail sectors are significantly contributing to market expansion across APAC.

Japan Food Inclusions Market Insight

The Japan food inclusions market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s strong demand for premium confectionery, innovative desserts, and aesthetically appealing packaged foods. Japanese consumers place significant emphasis on product quality, flavor precision, and texture enhancement, encouraging manufacturers to develop advanced inclusion-based food products. The growing popularity of premium chocolates, dairy desserts, and functional snack products is fueling market demand. Moreover, increasing adoption of healthier ingredients such as nuts, seeds, and fruit inclusions in convenience foods is expected to support sustained market growth.

China Food Inclusions Market Insight

The China food inclusions market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid urbanization, rising disposable incomes, and strong expansion of the processed food and bakery industries. China represents one of the largest markets for confectionery, dairy products, bakery applications, and ready-to-eat snacks, significantly increasing demand for chocolate, fruit, nut, and cereal inclusions. The rapid expansion of modern retail channels, increasing westernization of food consumption habits, and strong domestic food manufacturing capabilities are major factors propelling market growth in China.

Global Food Inclusions Market Share

The Food Inclusions industry is primarily led by well-established companies, including:

• Sensient Colors LLC (U.S.)

• PURATOS (Belgium)

• Taura Natural Ingredients Ltd (New Zealand)

• Georgia Nut Company (U.S.)

• Symrise (Germany)

• Nimbus Foods Ltd (U.K.)

• Cargill, Incorporated (U.S.)

• Barry Callebaut (Switzerland)

• Kerry Group plc (Ireland)

• Tate & Lyle (U.K.)

• AGRANA Beteiligungs AG (Austria)

• TruFoodMfg (U.S.)

• FoodFlo International Ltd. (U.K.)

• ADM (U.S.)

Latest Developments in Global Food Inclusions Market

- In November 2025, Barry Callebaut, a Switzerland-based chocolate and cocoa manufacturer, announced the launch of a new portfolio of organic chocolate inclusions targeting the premium food and bakery segment. The development focuses on meeting rising consumer demand for clean-label, sustainable, and organically sourced ingredients across confectionery and dessert applications. The company aims to strengthen its premium product positioning while enhancing sustainability commitments across its supply chain operations. The expansion is expected to support growing demand for healthier indulgence products and increase competition within the premium food inclusions market. The launch also reinforces the industry trend toward organic and ethically sourced inclusion ingredients globally.

- In October 2024, Cargill, Incorporated, a U.S.-based food ingredient manufacturer, expanded its partnership network with local farmers across Southeast Asia to strengthen cocoa and specialty inclusion sourcing operations. The initiative is designed to improve raw material traceability, secure long-term supply stability, and enhance sustainable sourcing practices across food inclusion manufacturing. The collaboration also supports local agricultural economies while improving supply chain efficiency and product consistency for bakery, dairy, and confectionery applications. The development is expected to strengthen Cargill’s sustainability positioning and improve competitive advantage in the global inclusions market. Rising consumer awareness regarding ingredient sourcing and transparency is further supporting such strategic investments.

- In September 2024, Ingredion Incorporated, a U.S.-based ingredient solutions provider, launched a new range of plant-based food inclusions developed specifically for vegan and vegetarian food applications. The product portfolio includes texture-enhancing inclusions designed for dairy alternatives, snack bars, frozen desserts, and bakery products. The company aims to capitalize on rising consumer preference for plant-based and functional foods while expanding its clean-label ingredient offerings. This development is expected to accelerate innovation across the alternative protein and healthy snacking sectors globally. Increasing adoption of vegan diets and sustainable food ingredients is further contributing to market expansion.

- In July 2023, Dr. Oetker, a Germany-based food manufacturing company, expanded its food inclusions portfolio through the introduction of Billionaire’s Chocolate Chips Mix and Rainbow Chocolate Chips Mix for bakery and dessert applications. The newly launched products combine multiple inclusions such as dark chocolate chips, white chocolate chips, toffee chunks, strawberry-flavored crunch, and decorative pearls to enhance texture and visual appeal. The expansion supports rising consumer demand for premium home-baking products and customized dessert experiences. The company also aims to strengthen its retail presence in the premium bakery ingredient segment through innovative flavor combinations. This development is expected to support growth in artisanal and convenience baking applications globally.

- In March 2023, Kellogg’s Company, a U.S.-based multinational food manufacturer, launched a new Barista Edition crunchy granola cereal featuring chocolate mocha flavored inclusions and coffee-infused almond slices. The product development focuses on delivering premium breakfast experiences while targeting consumers seeking café-style flavors in ready-to-eat cereals and snack products. The launch supports growing demand for indulgent yet convenient breakfast solutions with enhanced flavor and texture combinations. The company aims to strengthen its premium cereal portfolio while increasing consumer engagement in the healthy snacking category. Rising demand for innovative breakfast products is expected to further drive food inclusion adoption globally.

- In May 2022, Mars, Incorporated, a U.S.-based confectionery and snack manufacturer, introduced a healthier chocolate snack product named Mars Triple Treat containing nuts, raisins, and date paste inclusions. The product launch focuses on addressing increasing consumer demand for healthier indulgent snacks with natural and functional ingredients. The company aims to diversify its confectionery offerings while strengthening its position in the better-for-you snacking segment. The launch is expected to support wider adoption of nutrient-rich inclusions across premium chocolate and snack products. Growing health awareness and demand for functional confectionery products continue to positively influence market growth.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Food Inclusions Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Food Inclusions Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Food Inclusions Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.