Global Freestanding Emergency Department Market

Market Size in USD Billion

USD

13.70 Billion

USD

22.50 Billion

2025

2033

USD

13.70 Billion

USD

22.50 Billion

2025

2033

| 2026 - 2033 | |

| USD 13.70 Billion | |

| USD 22.50 Billion | |

| % | |

|

Freestanding Emergency Department Market Overview

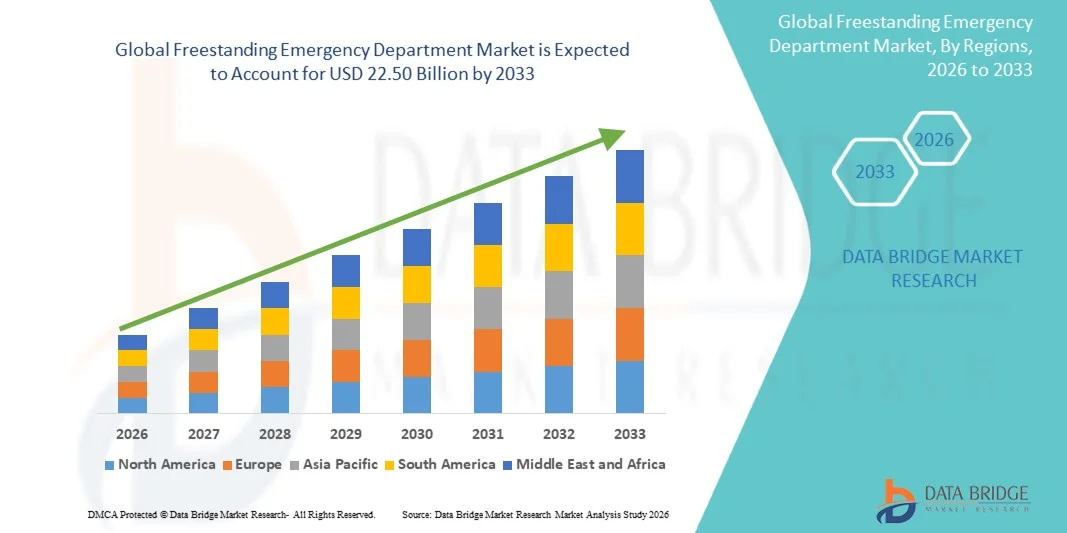

The Freestanding Emergency Department Market was valued at USD 13.70 billion in 2025 and is projected to reach USD 22.50 billion by 2033, growing at a CAGR of 6.40% from 2026 to 2033. The Global Freestanding Emergency Department (FSED) market is experiencing steady growth driven by rising demand for accessible and timely emergency care services, increasing patient burden on hospital emergency departments, and expanding healthcare infrastructure across developed and emerging regions. The growing need to reduce emergency room overcrowding in hospitals is encouraging healthcare providers to establish standalone emergency facilities that can deliver faster triage, diagnosis, and treatment services.

The increasing prevalence of chronic diseases, traumatic injuries, and acute medical emergencies, combined with rising healthcare awareness and patient preference for quicker service delivery, is accelerating the adoption of freestanding emergency departments. In addition, advancements in medical imaging, point-of-care diagnostics, and telemedicine integration are enhancing the operational efficiency of these facilities. Expanding investments by healthcare systems and private providers, along with supportive regulatory frameworks in several countries, are further driving market expansion by improving access to emergency care services outside traditional hospital settings.

Key Market Trends & Insights

- North America dominated the Freestanding Emergency Department Market with the largest revenue share of 39.12% in 2025, supported by a highly developed emergency care network, strong presence of hospital-affiliated FEDs, high healthcare spending, and increasing demand for faster, decentralized emergency services. The region also benefits from advanced diagnostic integration (CT, MRI, and point-of-care testing), strong insurance coverage, and rising emergency patient inflow.

- The hospital affiliated segment dominated the market with a 61.3% share in 2025, supported by strong brand trust, integrated healthcare networks, and streamlined patient referral systems.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.6% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising urban population, increasing emergency care demand, and growing investments in hospital networks across China, India, and Japan. Government initiatives aimed at improving emergency response systems and healthcare accessibility are further accelerating market expansion.

- The Ophthalmology segment is projected to grow at a CAGR of 7.9% from 2026 to 2033, supported by increasing incidence of eye trauma, infections, and acute vision-related emergencies, along with growing availability of specialized ophthalmic emergency services in FED facilities.

- Hospital Application dominated the market with a 54.27% revenue share in 2025, driven by strong expansion of hospital-affiliated freestanding emergency departments aimed at reducing emergency room overcrowding, improving patient flow, and increasing operational efficiency.

- Clinic-based applications are expected to register a CAGR of 8.1% from 2026 to 2033, supported by rising adoption of standalone urgent care models, increasing demand for cost-effective emergency services, and expansion of outpatient emergency treatment facilities.

- Hospital-affiliated ownership type accounted for 63.85% of the market share in 2025, supported by stronger funding capacity, integrated hospital referral systems, and higher patient trust in hospital-backed emergency care facilities.

- Independent freestanding emergency departments are projected to grow at a CAGR of 7.8% from 2026 to 2033, driven by increasing demand for accessible emergency care, faster service delivery, and expansion of private healthcare providers in urban and suburban regions.

- Emergency Care services dominated the service segment with a 49.33% revenue share in 2025, reflecting the core function of FEDs in providing immediate stabilization, trauma care, and acute treatment services for walk-in emergency patients.

- Imaging Services are expected to grow at a CAGR of 8.3% from 2026 to 2033, driven by rising integration of advanced diagnostic imaging technologies such as CT scans, ultrasound, and X-ray systems, enabling faster clinical decision-making in emergency cases.

Market Size & Forecast

- Global Market Value (2025): USD 13.70 Billion

- Expected Market Value (2033): USD 22.50 Billion

- Forecast CAGR (2026–2033): 6.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Freestanding Emergency Department Market Segmentation

|

Attributes |

Freestanding Emergency Department Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Envision Healthcare (U.S.) |

|

Market Opportunities |

· Expansion of Hospital Decongestion and Patient Flow Optimization Needs · Rising Demand for Standalone and Convenient Emergency Care Facilities · Integration of Advanced Diagnostic and Digital Healthcare Technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Freestanding Emergency Department Market Trends

Trend: Expansion of Integrated Diagnostic and High-Acuity Emergency Care Services

Freestanding Emergency Departments (FEDs) are increasingly evolving into fully equipped acute-care centers with advanced diagnostic capabilities, including CT imaging, ultrasound, point-of-care laboratory testing, and tele-emergency medicine integration. This shift is driven by rising patient demand for faster emergency care access and reduced wait times compared to traditional hospital emergency departments.

For instance, in the United States, hospital systems such as HCA Healthcare and Texas Health Resources have expanded FED networks to reduce ER congestion, with several facilities reporting 30–40% faster patient turnaround times compared to hospital-based emergency departments. Increasing adoption of digital triage systems and electronic health record (EHR) integration is further improving workflow efficiency and patient outcomes.

Freestanding Emergency Department Market Dynamics

Key Market Driver: Rising Emergency Care Demand and Hospital Overcrowding

The increasing burden on hospital emergency departments due to growing population density, chronic disease prevalence, and trauma cases is driving strong adoption of freestanding emergency departments. FEDs provide 24/7 emergency care access with shorter wait times, making them an important alternative care delivery model in urban and suburban healthcare systems.

For instance, in the United States alone, emergency department visits exceed 140 million annually, creating significant pressure on hospital infrastructure. FEDs help redistribute this patient load by handling non-critical and semi-critical emergencies, improving overall healthcare system efficiency. In addition, rising prevalence of cardiovascular diseases, respiratory conditions, and trauma-related emergencies continues to support demand for standalone emergency facilities.

Government initiatives in regions such as the U.S. and select Middle Eastern countries are also supporting emergency care decentralization by encouraging private investment in urgent care infrastructure.

Key Restraint/Challenge: Regulatory Variability and High Operational Costs

A major challenge in the Freestanding Emergency Department Market is the variability in regulatory frameworks across regions, particularly regarding licensing, reimbursement policies, and hospital affiliation requirements. In the United States, for instance, several states have imposed restrictions on independent FED development due to concerns over pricing transparency and billing practices.

In addition, the operational cost of maintaining 24/7 emergency staffing, advanced diagnostic imaging systems, and laboratory infrastructure remains high. Staffing shortages in emergency medicine—particularly in rural and semi-urban areas—further increase operational pressure. According to healthcare workforce studies, emergency medicine physician shortages are projected to persist through 2030, creating additional strain on FED scalability.

Key Market Opportunity: Expansion of Hospital-Affiliated FED Networks and Digital Emergency Care Models

The increasing integration of hospital systems with freestanding emergency departments presents a significant growth opportunity. Hospital-affiliated FEDs benefit from stronger referral networks, shared electronic medical records, and integrated billing systems, enabling improved patient continuity of care.

For instance, large healthcare systems such as AdventHealth and Kaiser Permanente have expanded distributed emergency care models combining FEDs with urgent care centers and telehealth triage services. The use of AI-powered triage systems and remote consultation platforms is further enhancing patient routing efficiency and reducing unnecessary hospital admissions. In addition, emerging markets across Asia-Pacific and the Middle East are increasingly investing in modular emergency care infrastructure, including hybrid emergency-urgent care facilities, to improve healthcare accessibility in rapidly urbanizing regions.

Freestanding Emergency Department Market Scope

The Freestanding Emergency Department market is segmented on the basis of type, application, ownership type, and service.

By Type

On the basis of type, the Freestanding Emergency Department Market is segmented into ophthalmology, internal medicine, otolaryngology, and other services. The internal medicine segment dominated the market with a 38.6% share in 2025, driven by the high patient inflow for acute and chronic condition management, increasing prevalence of lifestyle-related diseases, and the need for immediate diagnostic and therapeutic care. Freestanding emergency departments are increasingly serving as first-contact care centers for non-trauma emergencies, where internal medicine plays a critical role in stabilizing patients and providing rapid treatment. In addition, rising healthcare accessibility and expansion of emergency care infrastructure are strengthening segment dominance across urban and semi-urban regions. Hospitals and independent emergency centers are investing in advanced diagnostic tools and specialist availability to improve internal medicine service efficiency and patient outcomes. The growing burden of cardiovascular, respiratory, and metabolic disorders is further supporting demand for this segment across developed and emerging healthcare systems.

The ophthalmology segment is expected to register the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by increasing incidence of eye-related emergencies such as trauma, infections, and acute vision disorders. Rising awareness regarding early diagnosis of ocular conditions and expanding access to specialized emergency eye care services are accelerating segment growth. Freestanding emergency departments are increasingly integrating ophthalmic diagnostic equipment and on-call specialist support to handle urgent cases efficiently. In addition, the growing geriatric population, which is more prone to cataracts, glaucoma complications, and retinal disorders, is further boosting demand. Technological advancements in portable imaging systems and rapid screening tools are enhancing ophthalmology service capabilities in emergency settings, improving treatment speed and clinical outcomes.

By Application

On the basis of application, the Freestanding Emergency Department Market is segmented into hospital, clinic, and other applications. The hospital segment dominated the market with a 52.4% share in 2025, owing to strong integration of freestanding emergency departments with hospital networks, higher patient trust levels, and better access to advanced diagnostic and treatment infrastructure. Hospitals are increasingly establishing or affiliating with freestanding emergency units to reduce overcrowding in central emergency rooms and improve patient flow management. These facilities also benefit from seamless referral systems, enabling quick escalation of critical cases. In addition, hospitals leverage economies of scale and advanced medical staffing to deliver efficient emergency care services. Rising healthcare expenditure and expansion of hospital chains, particularly in urban regions, are further reinforcing segment leadership globally.

The clinic segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for accessible and community-based emergency care services. Clinics are expanding their capabilities to include urgent care and emergency stabilization services, especially in suburban and semi-urban areas. Lower waiting times, cost efficiency, and proximity to patients are key factors driving adoption of clinic-based freestanding emergency departments. In addition, rising investment in outpatient healthcare infrastructure and growing preference for decentralized care models are supporting segment expansion. Technological integration, such as digital triage systems and tele-emergency support, is further enhancing service efficiency and clinical decision-making in clinic settings.

By Ownership Type

On the basis of ownership type, the Freestanding Emergency Department Market is segmented into hospital affiliated and independent facilities. The hospital affiliated segment dominated the market with a 61.3% share in 2025, supported by strong brand trust, integrated healthcare networks, and streamlined patient referral systems. Hospital-owned freestanding emergency departments benefit from shared infrastructure, standardized clinical protocols, and access to specialized medical personnel. These facilities are increasingly preferred due to their ability to provide continuity of care and seamless transfer of critical patients to inpatient hospital settings when required. In addition, hospitals are expanding their geographic reach through affiliated emergency units to improve healthcare accessibility and reduce emergency room congestion.

The independent segment is expected to record the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing private investment in standalone emergency care facilities. Independent centers offer faster service delivery, shorter waiting times, and flexible operational models, making them attractive in underserved regions. Rising demand for localized emergency care and increasing patient preference for convenience-based healthcare services are supporting segment expansion. In addition, favorable regulatory frameworks in certain regions and growing entrepreneurial participation in healthcare infrastructure development are accelerating independent facility adoption.

By Service

On the basis of service, the Freestanding Emergency Department Market is segmented into laboratory service, imaging service, emergency care, and other services. The emergency care segment dominated the market with a 44.8% share in 2025, driven by the primary role of freestanding emergency departments in providing immediate treatment for acute medical conditions, trauma cases, and urgent health issues. These facilities are designed to deliver rapid stabilization, diagnostic evaluation, and early intervention, making emergency care the core service offering. Increasing incidence of accidents, cardiac emergencies, and sudden illnesses is significantly contributing to segment dominance. In addition, rising healthcare awareness and demand for 24/7 emergency services are further strengthening this segment across developed and emerging markets.

The imaging service segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing reliance on advanced diagnostic imaging for rapid clinical decision-making in emergency settings. Technologies such as CT scans, X-rays, and ultrasound systems are becoming essential components of freestanding emergency departments. The growing need for accurate and quick diagnosis of trauma, internal injuries, and acute conditions is fueling demand for imaging services. In addition, integration of digital imaging systems with electronic health records and AI-assisted diagnostics is improving efficiency, accuracy, and turnaround time, further accelerating segment growth.

Freestanding Emergency Department Market Regional Analysis

North America dominated the Freestanding Emergency Department Market with the largest revenue share of 39.12% in 2025, supported by a highly developed emergency care network, strong presence of hospital-affiliated FEDs, high healthcare spending, and increasing demand for faster, decentralized emergency services. The region also benefits from advanced diagnostic integration such as CT, MRI, ultrasound, and point-of-care testing, along with strong insurance coverage and rising emergency patient inflow. The growing burden of chronic diseases, trauma cases, and aging population is further increasing reliance on standalone emergency care facilities, strengthening North America’s leadership position in the global market.

U.S. Freestanding Emergency Department Market Insight

The U.S. Freestanding Emergency Department market is witnessing strong growth due to rising emergency care demand, hospital overcrowding, and increasing expansion of hospital-affiliated FED networks. The country records over 140 million emergency department visits annually, creating strong demand for decentralized emergency care infrastructure. Increasing investments by major healthcare providers in standalone emergency facilities are improving patient access, reducing wait times, and enhancing care efficiency. In addition, strong reimbursement systems and advanced healthcare infrastructure are supporting continued expansion of FED facilities across urban and suburban regions.

Europe Freestanding Emergency Department Market Insight

The Europe Freestanding Emergency Department market remains a significant contributor to global revenue, supported by strong public healthcare systems, increasing healthcare modernization, and growing demand for efficient emergency care delivery. Rising incidence of cardiovascular diseases, respiratory disorders, and age-related emergencies is increasing pressure on hospital emergency departments, supporting adoption of alternative care models. In addition, expansion of urgent care centers and integrated emergency networks is improving accessibility and reducing hospital congestion across key European countries.

U.K. Freestanding Emergency Department Market Insight

The U.K. Freestanding Emergency Department market is growing steadily due to increasing emergency care demand, pressure on National Health Service (NHS) hospitals, and rising adoption of urgent care and walk-in emergency models. Growing investments in healthcare infrastructure and digital triage systems are improving patient flow and reducing emergency department waiting times. Furthermore, integration of diagnostic services such as imaging and laboratory testing within emergency care centers is enhancing service efficiency and patient outcomes.

Germany Freestanding Emergency Department Market Insight

The Germany Freestanding Emergency Department market is expanding due to strong healthcare infrastructure, increasing hospital capacity constraints, and rising demand for faster emergency care services. Germany’s aging population and high prevalence of chronic diseases are contributing to increased emergency admissions. Investments in modern diagnostic equipment and expansion of outpatient emergency services are further supporting market growth. The country’s focus on healthcare efficiency and decentralized care delivery is strengthening adoption of freestanding emergency facilities.

Asia-Pacific Freestanding Emergency Department Market Insight

The Asia-Pacific Freestanding Emergency Department market is expected to witness rapid growth, registering the fastest CAGR of 8.6% from 2026 to 2033, driven by expanding healthcare infrastructure, rising urban population, increasing emergency care demand, and growing investments in hospital networks across China, India, and Japan. Government initiatives to improve emergency response systems, expand insurance coverage, and strengthen healthcare accessibility are further supporting regional expansion. Increasing private-sector participation in emergency care infrastructure is also accelerating market development.

Japan Freestanding Emergency Department Market Insight

The Japan Freestanding Emergency Department market is witnessing steady growth due to its rapidly aging population, increasing chronic disease burden, and strong healthcare system efficiency requirements. Demand for faster emergency care access and reduced hospital congestion is driving expansion of decentralized emergency care models. Advanced diagnostic technologies and integration of digital health systems are improving emergency care delivery and patient outcomes across the country.

China Freestanding Emergency Department Market Insight

The China Freestanding Emergency Department market is growing rapidly due to rising urbanization, increasing healthcare expenditure, and expansion of hospital infrastructure. Growing emergency case volumes, increasing awareness of urgent care services, and government healthcare reforms are supporting development of decentralized emergency care facilities. Expansion of private healthcare providers and improved access to diagnostic technologies are further strengthening market growth, positioning China as one of the fastest-growing FED markets globally.

Freestanding Emergency Department Market Share

The Freestanding Emergency Department industry is primarily led by well-established companies, including:

- Envision Healthcare (U.S.)

- TeamHealth (U.S.)

- Adeptus Health (U.S.)

- FastMed Urgent Care (U.S.)

- U.S. Acute Care Solutions (U.S.)

- HCA Healthcare (U.S.)

- Tenet Healthcare Corporation (U.S.)

- Community Health Systems (U.S.)

- Ascension Health (U.S.)

- Mayo Clinic (U.S.)

- Cleveland Clinic (U.S.)

- Kaiser Permanente (U.S.)

- CommonSpirit Health (U.S.)

- Baylor Scott & White Health (U.S.)

- Emory Healthcare (U.S.)

- AdventHealth (U.S.)

- Fresenius Medical Care (Germany)

- Ramsay Health Care (Australia)

- Spire Healthcare (U.K.)

- LifePoint Health (U.S.)

- Medica Health Group (U.S.)

- Apollo Hospitals (India)

- Fortis Healthcare (India)

- Manipal Hospitals (India)

- Narayana Health (India)

- Aster DM Healthcare (UAE)

- Mediclinic International (UAE)

- NMC Healthcare (UAE)

- Burjeel Holdings (UAE)

- Saudi German Health (Saudi Arabia)

- Dr. Sulaiman Al Habib Medical Group (Saudi Arabia)

- Sheikh Shakhbout Medical City (UAE)

Latest Developments in Freestanding Emergency Department Market

- In May 2021, HCA Healthcare expanded its network of freestanding emergency departments across the United States, adding multiple off-campus ER facilities in high-growth suburban regions of Texas and Florida. These expansions were aimed at reducing hospital emergency department congestion and improving patient access to 24/7 acute care services. The strategy strengthened HCA’s position as one of the largest operators of hospital-affiliated FED networks in the U.S., supporting faster emergency response times and improved patient throughput

- In January 2022, AdventHealth expanded its integrated emergency care footprint in Florida by opening new hospital-based emergency departments alongside freestanding and hybrid emergency facilities. The organization increasingly adopted distributed emergency care models combining full-service hospitals with standalone emergency units to address rising patient volumes and reduce overcrowding in central emergency departments

- In August 2022, Envision Healthcare (U.S.) expanded its partnership model with hospital systems to manage and staff freestanding emergency departments across multiple states. This expansion supported increased physician staffing in off-campus emergency facilities and improved access to emergency medicine specialists, particularly in underserved suburban healthcare markets

- In April 2023, Texas Health Resources continued expansion of its freestanding emergency department network across North Texas, adding new community-based emergency facilities integrated with imaging and laboratory services. These expansions focused on improving emergency care accessibility in rapidly growing suburban populations and reducing emergency room wait times in major hospital campuses

- In October 2023, AdventHealth broke ground on multiple hospital expansion projects in Florida that included integrated emergency department capacity enhancements and new emergency access points. These developments strengthened the system’s distributed emergency care model by improving patient routing between hospital-based emergency departments and standalone urgent care facilities

- In April 2024, AdventHealth opened expanded emergency care capacity at AdventHealth Kissimmee in Florida, adding new treatment rooms, trauma bays, and enhanced emergency service infrastructure. The expansion improved emergency department throughput, increased patient intake capacity, and supported rising demand for acute care services in the region

- In October 2024, AdventHealth Riverview Hospital officially opened in Florida, featuring a full-service emergency department designed to operate with high patient volume capacity and integrated diagnostic services. The facility was developed to support rapidly growing suburban populations and reduce dependency on overcrowded metropolitan hospital emergency departments

- In May 2024, Kaiser Permanente expanded its urgent care and emergency access network in the western United States by integrating digital triage systems across emergency care facilities. This initiative improved patient routing efficiency, allowing non-critical cases to be diverted to urgent care centers while preserving hospital emergency department capacity for high-acuity cases

- In November 2024, U.S. hospital systems increasingly adopted hybrid emergency care models combining freestanding emergency departments with micro-hospitals. These facilities integrated imaging, laboratory diagnostics, and inpatient stabilization services, improving care continuity and expanding access in suburban and semi-urban regions

- In January 2025, several U.S. healthcare providers, including regional hospital networks in Texas and Florida, announced continued expansion of freestanding emergency department capacity due to sustained emergency visit growth exceeding 140 million annual visits nationwide. These expansions focused on improving decentralized emergency care delivery and reducing hospital emergency department overcrowding

- In March 2025, independent emergency care operators in the United States expanded microhospital conversion projects, upgrading freestanding emergency departments into hybrid inpatient-capable facilities. These upgrades included advanced imaging systems, operating rooms, and extended observation units, reflecting a broader shift toward integrated emergency care delivery models

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.