Global Front E Axle Market

Market Size in USD Billion

USD

11.78 Billion

USD

58.19 Billion

2025

2033

USD

11.78 Billion

USD

58.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.78 Billion | |

| USD 58.19 Billion | |

| % | |

|

Front Electric Axle (E-Axle) Market Overview

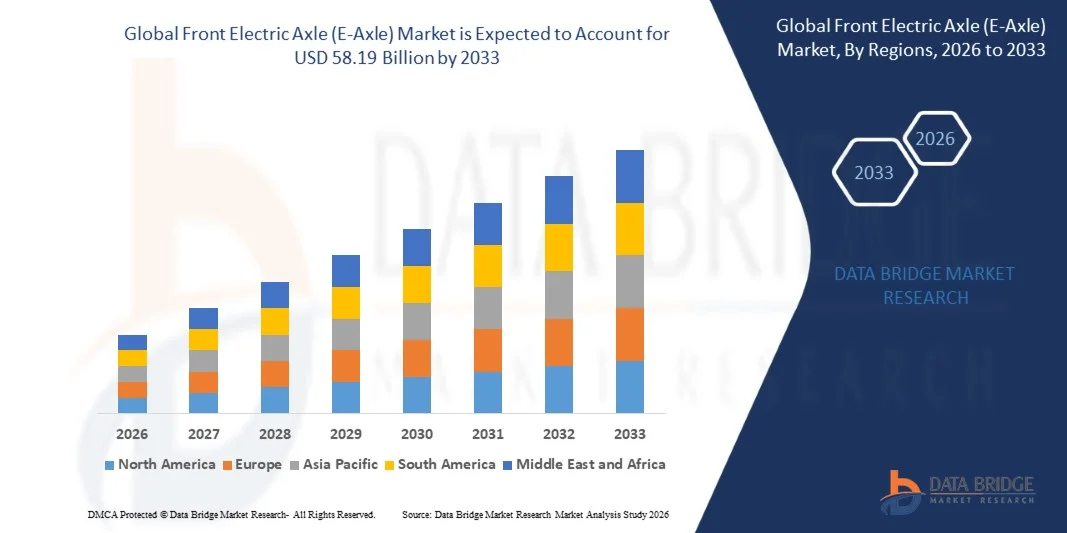

The Front Electric Axle (E-Axle) Market was valued at USD 11.78 billion in 2025 and is projected to reach USD 58.19 billion by 2033, growing at a CAGR of 22.10% from 2026 to 2033. Market growth is supported by accelerating electric vehicle adoption, stringent emission regulations, advancements in integrated powertrain technologies, and increasing investments by automakers in electrification strategies across passenger and commercial vehicle segments.

The growing emphasis on reducing carbon emissions and achieving net-zero targets is driving automotive manufacturers to transition from internal combustion engines to electric drivetrains, with e-axles serving as critical components that integrate the motor, power electronics, and transmission into a single compact unit. This integration reduces vehicle weight, improves energy efficiency, and simplifies vehicle architecture, making e-axles essential for next-generation electric vehicles. Technological advancements in silicon carbide (SiC) power electronics, high-speed electric motors, and advanced thermal management systems are enhancing e-axle performance, efficiency, and power density.

Rising consumer demand for electric vehicles across North America, Europe, and Asia-Pacific is creating substantial opportunities for e-axle manufacturers and suppliers. Government incentives, subsidies, and regulatory mandates supporting electric vehicle adoption are further accelerating market growth. The expansion of electric vehicle production facilities and the localization of e-axle manufacturing in key markets are enabling cost reductions and supply chain optimization.

Key Market Trends & Insights

- Asia-Pacific dominated the global front electric axle market with the largest revenue share of 48.6% in 2025, supported by high electric vehicle production volumes in China, Japan, and South Korea, along with strong government support for electrification initiatives.

- Europe is expected to be the fastest-growing region at a CAGR of 24.3% from 2026 to 2033, driven by stringent EU emission regulations, ambitious electrification targets, and substantial automaker investments in electric vehicle platforms.

- The Single Axle segment led the market with a 67.4% market share in 2025, reflecting widespread adoption in mainstream electric passenger vehicles requiring cost-effective and compact powertrain solutions.

- The Multiple Axle segment is anticipated to be the fastest-growing shaft type category, driven by increasing demand for all-wheel-drive electric vehicles and high-performance applications requiring enhanced traction and power distribution.

- The Electric Vehicle segment dominated the vehicle type category with a 52.8% market share in 2025, supported by the rapid expansion of battery electric vehicle (BEV) production and the central role of e-axles in electric powertrain architecture.

- The Combining Motors component segment dominated the component category with a 38.5% market share in 2025, driven by the integration of high-efficiency permanent magnet and induction motors within e-axle systems.

- The Alloys segment dominated the material category with a 71.2% market share in 2025, driven by favorable strength-to-weight ratios, cost-effectiveness, and established manufacturing processes for aluminum and steel alloy e-axle housings.

Market Size & Forecast

- Global Market Value (2025): USD 11.78 Billion

- Expected Market Value (2033): USD 58.19 Billion

- Forecast CAGR (2026–2033): 22.10%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: Europe

Report Scope and Front Electric Axle (E-Axle) Market Segmentation

|

Attributes |

Front Electric Axle (E-Axle) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Robert Bosch GmbH (Germany) · ZF Friedrichshafen AG (Germany) · Magna International Inc. (Canada) · BorgWarner Inc. (U.S.) · Nidec Corporation (Japan) · Schaeffler AG (Germany) · Continental AG (Germany) · Aisin Corporation (Japan) · GKN Automotive Limited (U.K.) · Dana Incorporated (U.S.) · Vitesco Technologies Group AG (Germany) · Linamar Corporation (Canada) |

|

Market Opportunities |

· Expansion of electric vehicle production capacity and localization of e-axle manufacturing in emerging markets with growing automotive electrification investments · Development of next-generation silicon carbide (SiC) power electronics and high-speed motors enabling higher efficiency and power density in compact e-axle designs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Front Electric Axle (E-Axle) Market Trends

Trend: Integration of Silicon Carbide Power Electronics for Enhanced Efficiency

Automotive manufacturers and e-axle suppliers are increasingly adopting silicon carbide (SiC) power electronics to improve energy efficiency, extend driving range, and reduce thermal management requirements in electric vehicles. SiC-based inverters offer higher switching frequencies, lower power losses, and improved thermal conductivity compared to traditional silicon-based components, enabling more compact and lightweight e-axle designs. The transition to SiC technology is accelerating as semiconductor manufacturing capacity expands and costs decline through economies of scale.

For instance,

In March 2025, BorgWarner Inc. announced the production launch of its next-generation integrated drive module (iDM) featuring silicon carbide inverter technology, delivering up to 8% improvement in system efficiency compared to previous-generation IGBT-based systems. The technology enables extended vehicle range and reduced battery size requirements for OEM partners.

The integration of SiC power electronics is expected to become standard in premium and high-performance e-axle applications, with broader adoption across mainstream electric vehicles as manufacturing costs continue to decline. This technological advancement is driving continued innovation and competitive differentiation in the global e-axle market.

Front Electric Axle (E-Axle) Market Dynamics

Key Market Driver: Accelerating Electric Vehicle Adoption and Stringent Emission Regulations

The global transition toward electric mobility, driven by increasingly stringent emission regulations and ambitious government electrification targets, is the primary driver of front electric axle market growth. Regulatory frameworks such as the European Union's CO2 emission standards, China's New Energy Vehicle (NEV) mandate, and U.S. Environmental Protection Agency (EPA) emissions rules are compelling automakers to accelerate electric vehicle development and production. E-axles serve as fundamental components enabling this transition by providing efficient, integrated powertrain solutions.

For instance,

According to the International Energy Agency (IEA) Global EV Outlook 2025, global electric vehicle sales exceeded 17 million units in 2024, representing approximately 20% of total passenger vehicle sales worldwide, with projections indicating continued acceleration through 2030.

As automakers expand electric vehicle portfolios and production volumes increase, demand for front e-axles is expected to grow substantially across passenger vehicle, commercial vehicle, and dedicated electric vehicle platforms. Regulatory pressure and consumer demand for zero-emission vehicles are expected to sustain strong market momentum throughout the forecast period.

Key Restraint/Challenge: High Development Costs and Supply Chain Constraints

The substantial research and development investments required for e-axle technology, combined with supply chain constraints affecting critical components such as rare earth magnets, power semiconductors, and specialty materials, present significant challenges to market growth. The complexity of integrating motors, power electronics, and transmissions into compact, high-performance e-axle systems requires substantial engineering expertise and capital investment. Supply chain disruptions affecting semiconductor availability and rare earth material sourcing can impact production timelines and cost structures.

For instance,

E-axle manufacturers face ongoing challenges related to rare earth magnet supply, with neodymium and dysprosium prices experiencing significant volatility due to concentrated production in limited geographic regions and increasing demand from the electric vehicle industry.

High development costs and supply chain vulnerabilities may constrain market expansion, particularly for smaller manufacturers and new entrants seeking to compete with established Tier 1 suppliers.

Key Market Opportunity: Expansion in Commercial Vehicle Electrification

The electrification of commercial vehicles, including light-duty trucks, delivery vans, and medium-duty commercial vehicles, represents a significant growth opportunity for front e-axle manufacturers. Fleet operators and logistics companies are increasingly adopting electric commercial vehicles to reduce operating costs, meet sustainability targets, and comply with urban emission regulations. E-axles designed for commercial vehicle applications require higher torque capacity, durability, and thermal management capabilities compared to passenger vehicle systems.

The commercial vehicle electrification segment is expected to drive substantial e-axle demand, with manufacturers developing specialized products tailored to fleet requirements and duty cycle characteristics. Expansion in commercial vehicle electrification represents a significant growth opportunity for e-axle manufacturers.

Front Electric Axle (E-Axle) Market Scope

The front electric axle (e-axle) market is segmented on the basis of shaft type, material, component, and vehicle type.

By Shaft Type

On the basis of shaft type, the global front electric axle market is segmented into single axle and multiple axle. The Single Axle segment dominated the market with a 67.4% market share in 2025, reflecting widespread adoption in mainstream electric passenger vehicles requiring cost-effective and compact powertrain solutions. Single axle configurations are preferred for front-wheel-drive and entry-level electric vehicles where simplicity, weight reduction, and manufacturing efficiency are prioritized. The concentration of single axle e-axle production within high-volume vehicle platforms contributes to segment leadership and economies of scale.

The Multiple Axle segment is expected to witness the fastest growth at a CAGR of 26.8% from 2026 to 2033, driven by increasing demand for all-wheel-drive electric vehicles and high-performance applications requiring enhanced traction, power distribution, and vehicle dynamics. Premium electric vehicles and performance-oriented platforms increasingly incorporate dual-motor configurations with front and rear e-axles, supporting segment expansion.

By Material

On the basis of material, the global front electric axle market is segmented into alloys and carbon fiber. The Alloys segment dominated the market with a 71.2% market share in 2025, driven by favorable strength-to-weight ratios, cost-effectiveness, and established manufacturing processes for aluminum and steel alloy e-axle housings and structural components. Aluminum alloys are particularly favored for e-axle applications due to their lightweight properties, thermal conductivity, and compatibility with high-volume die-casting processes. The mature supply chain and manufacturing infrastructure for alloy-based components support segment dominance.

The Carbon Fiber segment is expected to witness the fastest growth at a CAGR of 28.4% from 2026 to 2033, driven by increasing adoption in premium and performance electric vehicles where maximum weight reduction and structural rigidity are prioritized. Carbon fiber composite materials offer superior strength-to-weight ratios compared to traditional alloys, enabling enhanced vehicle efficiency and performance. Declining carbon fiber production costs and expanding manufacturing capabilities are supporting segment expansion.

By Component

On the basis of component, the global front electric axle market is segmented into combining motors, power electronics, transmission, and others. The Combining Motors segment dominated the market with a 38.5% market share in 2025, driven by the central role of electric motors in e-axle performance and the integration of high-efficiency permanent magnet synchronous motors (PMSM) and induction motors within e-axle systems. Motor technology directly influences e-axle power density, efficiency, and thermal characteristics, making it the primary value driver within integrated e-axle systems. Continued advancements in motor design, materials, and manufacturing are enhancing component performance and market value.

The Power Electronics segment is expected to witness the fastest growth at a CAGR of 25.6% from 2026 to 2033, driven by the transition to silicon carbide (SiC) and gallium nitride (GaN) semiconductor technologies that offer superior efficiency, power density, and thermal performance compared to traditional silicon-based components. The increasing complexity and value of power electronics within e-axle systems are driving segment expansion and technology investment.

By Vehicle Type

On the basis of vehicle type, the global front electric axle market is segmented into passenger vehicle, commercial vehicle, and electric vehicle. The Electric Vehicle segment dominated the market with a 52.8% market share in 2025, supported by the rapid expansion of battery electric vehicle (BEV) production and the central role of e-axles in electric powertrain architecture. Dedicated electric vehicle platforms are designed around integrated e-axle systems, with manufacturers optimizing vehicle architecture for efficiency, packaging, and performance. The concentration of e-axle procurement within high-volume electric vehicle programs contributes to segment leadership.

The Commercial Vehicle segment is expected to witness the fastest growth at a CAGR of 27.2% from 2026 to 2033, driven by accelerating electrification of light-duty trucks, delivery vans, and medium-duty commercial vehicles. Fleet operators and logistics companies are increasingly adopting electric commercial vehicles to reduce operating costs, meet sustainability targets, and comply with urban emission regulations. E-axle systems designed for commercial vehicle applications require higher torque capacity and durability, driving technology development and market expansion.

Front Electric Axle (E-Axle) Market Regional Analysis

Asia-Pacific dominated the front electric axle market with a revenue share of 48.6% in 2025, supported by high electric vehicle production volumes in China, Japan, and South Korea, along with strong government support for electrification initiatives. The concentration of battery electric vehicle manufacturing in China, combined with established automotive supply chains and domestic e-axle production capabilities, contributes to regional market leadership. Major automakers and Tier 1 suppliers including Nidec Corporation, Aisin Corporation, and BYD Auto are expanding e-axle production capacity to meet growing demand.

China Front Electric Axle (E-Axle) Market Insight

The China front electric axle market benefits from the world's largest electric vehicle market, strong government incentives for new energy vehicles, and established domestic manufacturing capabilities. China accounted for approximately 32.4% of the global market share in 2025, reflecting substantial electric vehicle production volumes and localized e-axle supply chains. Domestic manufacturers including Nidec (Dalian) and BorgWarner (China) are expanding production capacity to serve both domestic automakers and export markets.

Japan Front Electric Axle (E-Axle) Market Insight

The Japan front electric axle market benefits from advanced automotive technology capabilities, established Tier 1 supplier networks, and strong expertise in motor and power electronics development. Japanese manufacturers including Nidec Corporation and Aisin Corporation are global leaders in e-axle technology, supplying major automakers worldwide. The emphasis on compact, high-efficiency designs aligns with Japanese automotive engineering strengths.

Europe Front Electric Axle (E-Axle) Market Insight

Europe is expected to be the fastest-growing region, recording a CAGR of 24.3% from 2026 to 2033, driven by stringent EU emission regulations, ambitious electrification targets, and substantial automaker investments in electric vehicle platforms. The European Green Deal and CO2 emission standards are compelling automakers to accelerate electric vehicle adoption, with e-axles serving as critical enabling components. Germany accounted for approximately 14.8% of the global market share in 2025, reflecting the country's leading position in automotive manufacturing and electric vehicle development.

Germany Front Electric Axle (E-Axle) Market Insight

Germany's robust automotive industry and advanced engineering capabilities support comprehensive e-axle development and production programs. Leading suppliers including ZF Friedrichshafen AG, Schaeffler AG, and Continental AG are headquartered in Germany, with substantial investments in e-axle technology and manufacturing capacity. German automakers including Volkswagen, BMW, and Mercedes-Benz are major customers for front e-axle systems.

U.K. Front Electric Axle (E-Axle) Market Insight

The U.K. front electric axle market is characterized by expanding electric vehicle adoption, government incentives for zero-emission vehicles, and investments in domestic electric vehicle manufacturing. GKN Automotive Limited maintains significant e-axle development and production capabilities in the U.K., supporting both domestic and export markets.

North America Front Electric Axle (E-Axle) Market Insight

The North America front electric axle market benefits from accelerating electric vehicle adoption, substantial automaker investments in electric vehicle platforms, and expanding domestic e-axle manufacturing capabilities. The U.S. accounted for approximately 18.2% of the global market share in 2025, driven by electric vehicle production expansion from legacy automakers and new entrants. The Inflation Reduction Act and federal tax credits for electric vehicles are supporting market growth and domestic manufacturing investments.

U.S. Front Electric Axle (E-Axle) Market Insight

The U.S. front electric axle market benefits from substantial investments by automakers including General Motors, Ford, and Stellantis in electric vehicle platforms and domestic e-axle production. Tier 1 suppliers including BorgWarner Inc., Dana Incorporated, and Magna International are expanding U.S. manufacturing capacity to serve growing domestic demand and meet local content requirements.

Front Electric Axle (E-Axle) Market Share

The front electric axle industry is primarily led by well-established companies, including:

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Magna International Inc. (Canada)

- BorgWarner Inc. (U.S.)

- Nidec Corporation (Japan)

- Schaeffler AG (Germany)

- Continental AG (Germany)

- Aisin Corporation (Japan)

- GKN Automotive Limited (U.K.)

- Dana Incorporated (U.S.)

- Vitesco Technologies Group AG (Germany)

- Linamar Corporation (Canada)

Latest Developments in Front Electric Axle (E-Axle) Market

- In April 2026, ZF Friedrichshafen AG announced the expansion of its electric driveline production facility in Saarbrücken, Germany, increasing annual e-axle manufacturing capacity to over 1.5 million units. The expansion supports growing demand from European automakers transitioning to electric vehicle platforms and reinforces ZF's leadership in integrated e-axle systems.

- In February 2026, Nidec Corporation commenced production at its new e-axle manufacturing facility in Serbia, targeting European automotive customers with locally produced integrated drive systems. The facility features advanced automation and quality control systems designed to meet European OEM requirements for high-volume electric vehicle production.

- In December 2025, BorgWarner Inc. announced a strategic partnership with a leading Chinese electric vehicle manufacturer to supply next-generation silicon carbide-based integrated drive modules for new electric vehicle platforms launching in 2026. The partnership expands BorgWarner's presence in the world's largest electric vehicle market.

- In October 2025, Magna International Inc. launched its eBeam electric axle system designed specifically for light-duty commercial vehicles and delivery vans. The eBeam system features modular architecture enabling scalable power output and compatibility with multiple vehicle platforms.

- In August 2025, Schaeffler AG introduced its fourth-generation electric axle platform featuring integrated thermal management and optimized gear design for improved efficiency. The platform targets premium electric vehicles requiring high power density and compact packaging.

- In June 2025, Dana Incorporated announced the acquisition of a specialized power electronics company to strengthen its e-axle technology capabilities and accelerate development of next-generation silicon carbide inverter systems. The acquisition expands Dana's vertical integration in electric propulsion systems.

- In March 2025, Continental AG unveiled its enhanced PowerShift e-axle transmission system designed for high-performance electric vehicles requiring multi-speed capabilities. The system enables optimized motor operation across a wider speed range, improving efficiency and acceleration performance.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.