Global Gastric Cancer Market

Market Size in USD Billion

CAGR :

%

USD

7.24 Billion

USD

23.73 Billion

2025

2033

USD

7.24 Billion

USD

23.73 Billion

2025

2033

| 2026 –2033 | |

| USD 7.24 Billion | |

| USD 23.73 Billion | |

| % | |

|

Gastric Cancer Market Size

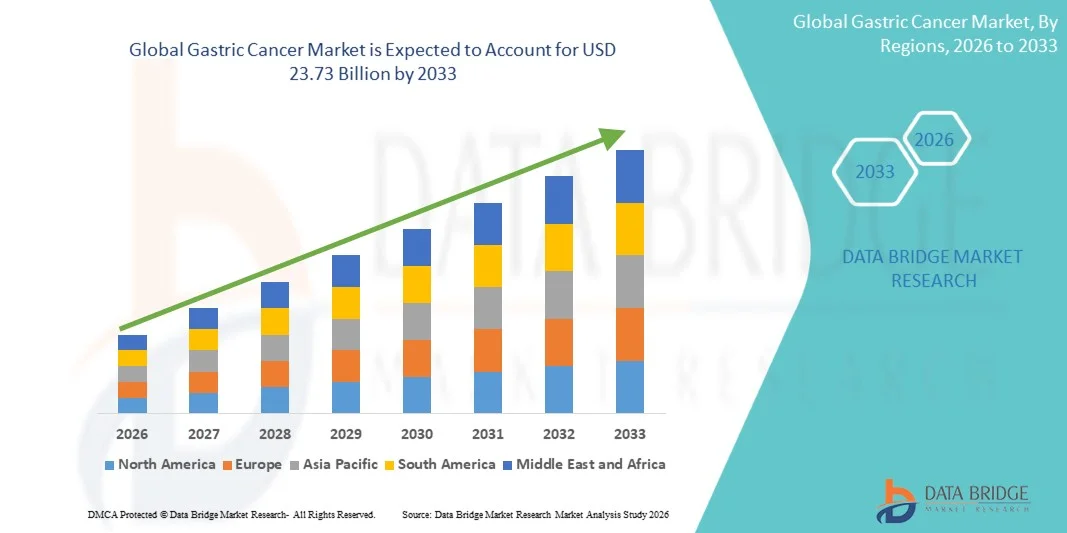

- The global gastric cancer market size was valued at USD 7.24 billion in 2025 and is expected to reach USD 23.73 billion by 2033, at a CAGR of 16.00% during the forecast period

- The market growth is largely driven by increasing prevalence of gastric cancer, rising awareness of early detection methods, and advancements in targeted therapies and minimally invasive treatment options, improving patient outcomes

- Furthermore, expanding healthcare infrastructure, growing adoption of novel immunotherapies, and rising investment in research and development are positioning advanced treatment options as the preferred choice for managing gastric cancer. These converging factors are accelerating the adoption of innovative therapies, thereby significantly boosting the industry's growth

Gastric Cancer Market Analysis

- Gastric cancer, encompassing malignant tumors of the stomach lining, remains a critical health concern worldwide, with diagnosis and treatment increasingly supported by advanced imaging, endoscopic technologies, and precision medicine approaches in both clinical and hospital settings due to improved survival outcomes and personalized therapy options

- The rising prevalence of gastric cancer is primarily fueled by aging populations, increasing adoption of early screening programs, and growing awareness of risk factors such as H. pylori infection, dietary habits, and genetic predispositions

- North America dominated the gastric cancer market with the largest revenue share of 37.5% in 2025, characterized by high healthcare expenditure, advanced oncology infrastructure, and widespread adoption of early detection and targeted treatment options, with the U.S. showing substantial growth in targeted therapies, immunotherapies, and minimally invasive procedures driven by innovation from both established pharmaceutical companies and biotech startups

- Asia-Pacific is expected to be the fastest-growing region in the gastric cancer market during the forecast period due to increasing healthcare access, rising awareness of gastric cancer, and expansion of screening and treatment programs

- Targeted therapy segment dominated the gastric cancer market in 2025, with a market share of 43.2%, driven by its proven efficacy, integration into clinical guidelines, and growing preference among oncologists for precision oncology approaches that improve patient outcomes

Report Scope and Gastric Cancer Market Segmentation

|

Attributes |

Gastric Cancer Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Gastric Cancer Market Trends

“Advancements in Precision Medicine and Targeted Therapies”

- A significant and accelerating trend in the global gastric cancer market is the increasing adoption of precision medicine approaches, including targeted therapies and biomarker-driven treatment strategies, which are enhancing treatment efficacy and personalization for patients

- For instance, trastuzumab-based therapies for HER2-positive gastric cancer enable oncologists to specifically target tumor cells, improving survival outcomes while minimizing systemic toxicity compared to conventional chemotherapy

- Integration of molecular diagnostics with treatment planning allows clinicians to tailor therapy regimens based on genetic mutations, tumor profiling, and patient-specific biomarkers, facilitating better response rates and fewer adverse effects

- Furthermore, combination therapies involving targeted agents and immunotherapies are gaining traction, offering new hope for patients with advanced or refractory gastric cancer, thereby reshaping standard-of-care protocols

- This trend towards personalized, biomarker-guided treatment is fundamentally transforming patient expectations and clinical approaches, with pharmaceutical companies such as Roche and Takeda developing next-generation therapies targeting specific gastric cancer subtypes

- The demand for targeted and precision-based therapies is growing rapidly across both early- and late-stage gastric cancer patient populations, as healthcare providers increasingly prioritize treatment effectiveness and reduced toxicity

- The growing focus on minimally invasive surgical techniques, such as laparoscopic and robotic-assisted gastrectomies, is improving patient recovery times and driving the adoption of advanced treatment protocols

Gastric Cancer Market Dynamics

Driver

“Increasing Incidence and Rising Awareness of Early Detection”

- The growing prevalence of gastric cancer worldwide, coupled with enhanced awareness and adoption of early detection and screening programs, is a significant driver for the rising demand for advanced treatment options

- For instance, national screening initiatives in countries such as Japan and South Korea have significantly improved early diagnosis rates, enabling timely intervention and better patient outcomes

- As patients and healthcare providers become more aware of risk factors such as H. pylori infection, dietary habits, and family history, early detection and preventive measures are increasingly emphasized, driving demand for diagnostics and treatment

- In addition, technological advances in endoscopy, imaging, and molecular testing are facilitating early-stage detection, contributing to improved survival rates and higher adoption of innovative therapies

- The growing prevalence of gastric cancer in both developed and developing regions, combined with patient demand for effective and personalized treatment solutions, is propelling market growth

- Rising investment in research and development by pharmaceutical and biotech companies is accelerating the discovery of novel drugs and combination therapies, further boosting market expansion

- Government initiatives and public-private partnerships promoting awareness campaigns, screening programs, and funding for oncology care are supporting increased early diagnosis and treatment adoption

Restraint/Challenge

“High Treatment Costs and Limited Access to Advanced Therapies”

- The high cost of targeted therapies, immunotherapies, and advanced diagnostics remains a significant challenge, limiting accessibility for patients, particularly in low- and middle-income regions

- For instance, the price of trastuzumab or ramucirumab-based regimens can be prohibitively expensive, restricting uptake despite proven clinical efficacy

- Limited healthcare infrastructure and uneven distribution of oncology centers in developing regions further constrain patient access to timely and effective treatment

- In addition, regulatory hurdles, complex clinical trial requirements, and slow approval processes for new drugs can delay market entry, impacting the availability of cutting-edge therapies

- While efforts are being made to introduce biosimilars and improve healthcare coverage, the combination of high costs and limited access continues to challenge widespread adoption of advanced gastric cancer treatments

- Patient hesitation and lack of awareness regarding advanced treatment options, particularly in rural areas, can delay care and limit market growth potential

- Variability in reimbursement policies and insurance coverage across regions further restricts patient access to high-cost therapies, impacting overall market penetration

Gastric Cancer Market Scope

The market is segmented on the basis of type, stages, diagnosis, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the gastric cancer market is segmented into adenocarcinoma, lymphoma, gastrointestinal stromal tumor (GIST), carcinoid tumor, and others. The adenocarcinoma segment dominated the market with the largest revenue share of 65% in 2025, driven by its high prevalence globally as it accounts for the majority of gastric cancer cases. Adenocarcinoma often requires multi-modal treatment approaches, including surgery, chemotherapy, and targeted therapy, increasing its market impact. The high incidence in regions such as East Asia and North America further reinforces its dominance. Rising awareness about early detection and improved diagnostic facilities for adenocarcinoma is also contributing to greater market adoption. Pharmaceutical companies prioritize the development of targeted therapies for adenocarcinoma due to the large patient population and potential for high treatment efficacy. Its established clinical protocols and strong research focus continue to sustain its leading market position.

The gastrointestinal stromal tumor (GIST) segment is anticipated to witness the fastest growth rate of 18.5% from 2026 to 2033, fueled by advancements in molecular-targeted therapies and growing awareness of rare gastric tumor subtypes. GISTs, though rare, respond well to targeted drugs such as imatinib, which has boosted market adoption. Increasing screening and molecular diagnostic capabilities are enabling earlier identification and treatment of GISTs. Growing R&D efforts in novel therapies and combination treatment regimens further drive growth. Rising investments by biotech companies in personalized treatment options for GISTs contribute to the accelerated adoption of these therapies. Furthermore, patient advocacy and awareness campaigns are enhancing diagnosis and treatment rates globally.

- By Stages

On the basis of stage, the market is segmented into Stage I, Stage II, Stage III, Stage IV, and others. The Stage III segment dominated the market with a revenue share of 37% in 2025, as patients in this stage typically require intensive treatment combining surgery, chemotherapy, and targeted therapy. Stage III gastric cancer presents significant clinical intervention opportunities, making it a key revenue-generating segment for pharmaceutical and diagnostic companies. Advanced diagnostic tools such as endoscopy and imaging tests are commonly utilized at this stage, boosting market adoption. Increasing survival rates due to early detection in preceding stages also expand the number of patients progressing to Stage III therapies. Pharmaceutical players focus on developing combination regimens for Stage III patients, further strengthening its market dominance. This stage also drives demand for hospital-based treatment infrastructure, increasing end-user market share.

The Stage I segment is expected to witness the fastest growth rate of 20.1% from 2026 to 2033, due to rising awareness of early detection programs, preventive screening, and minimally invasive treatment options. Early-stage gastric cancer allows for surgical resection and localized therapies, encouraging adoption of advanced diagnostics. Governments and healthcare organizations are promoting screening campaigns, increasing the patient pool for Stage I interventions. Technological advancements in imaging and endoscopic procedures support accurate early diagnosis. The growing preference for less aggressive, patient-friendly treatments further accelerates market growth.

- By Diagnosis

On the basis of diagnosis, the market is segmented into endoscopy, biopsy, imaging tests, exploratory surgery, and others. The endoscopy segment dominated the market with a revenue share of 42% in 2025, as it is the gold standard for detecting gastric cancer and enables both diagnosis and therapeutic intervention. Endoscopy provides real-time visualization and facilitates early detection, critical for improving survival rates. The procedure’s ability to perform biopsies simultaneously contributes to its high adoption. Increasing availability of advanced endoscopic technologies, including high-definition and AI-assisted scopes, further strengthens market dominance. Healthcare facilities prioritize endoscopy for its accuracy, cost-effectiveness, and widespread acceptance. Training programs for gastroenterologists and increased accessibility in hospitals further support adoption.

The imaging tests segment is anticipated to witness the fastest growth rate of 19.3% from 2026 to 2033, driven by technological advances such as PET-CT and MRI, which provide detailed tumor visualization and staging information. Imaging tests are increasingly integrated with AI and machine learning tools to improve diagnostic accuracy. Rising use of non-invasive diagnostics and patient preference for less discomfort contribute to market growth. Imaging enables precise treatment planning and monitoring, increasing adoption among hospitals and specialty centers. Research initiatives and clinical trials promoting imaging-based assessments further accelerate uptake.

- By Treatment

On the basis of treatment, the market is segmented into surgery, radiation therapy, chemotherapy, targeted therapy, palliative care, and others. The targeted therapy segment dominated the market with a share of 43.2% in 2025, driven by its effectiveness in treating specific gastric cancer subtypes, such as HER2-positive tumors. Targeted therapies improve patient outcomes, reduce systemic toxicity, and integrate well with personalized medicine approaches. The increasing number of approvals for new biologics and combination therapies further strengthens market dominance. Rising awareness among oncologists and patients about precision oncology supports adoption. Pharmaceutical investments in research and clinical trials for novel targeted drugs contribute to market growth. Availability of companion diagnostics also reinforces targeted therapy uptake.

The immunotherapy segment is expected to witness the fastest growth rate of 22.5% from 2026 to 2033, fueled by increasing clinical evidence supporting its use in advanced or refractory gastric cancer. Immune checkpoint inhibitors, alone or in combination with other therapies, are expanding treatment options. Growing investment by biotech companies and clinical trial activity accelerates adoption. Patients with limited response to traditional therapies increasingly opt for immunotherapy. Support from regulatory approvals and guideline inclusion further enhances market potential.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with a revenue share of 51% in 2025, driven by intravenous administration of chemotherapy, targeted therapy, and immunotherapy agents, which ensures higher bioavailability and efficacy. Parenteral administration is preferred for hospital-based treatment protocols and advanced-stage patients. Frequent monitoring and dose adjustments require clinical supervision, increasing hospital dependency. Rising adoption of biologics, monoclonal antibodies, and combination regimens supports market dominance. Pharmaceutical innovation in parenteral formulations further strengthens its position. Hospitals and specialty centers prefer parenteral delivery for controlled treatment outcomes.

The oral segment is expected to witness the fastest growth rate of 20.7% from 2026 to 2033, driven by the development of oral targeted therapies and chemotherapeutic agents. Oral administration offers patient convenience, supports homecare treatment, and improves adherence. Increasing availability of oral formulations for early- and mid-stage gastric cancer encourages adoption. Pharmaceutical companies are prioritizing oral drug development for ease of use. Patient preference for non-invasive treatment options further fuels market growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty centers, and others. The hospitals segment dominated the market with a revenue share of 58% in 2025, as hospitals provide comprehensive diagnostic and treatment facilities for gastric cancer, including surgery, chemotherapy, and targeted therapy. Hospitals also serve as primary sites for clinical trials and advanced treatment administration. The concentration of oncology specialists, diagnostic tools, and infrastructure in hospitals drives adoption. Institutional procurement and government healthcare programs further strengthen market dominance. Hospitals play a critical role in integrating multi-modal therapies and follow-up care.

The homecare segment is anticipated to witness the fastest growth rate of 19.8% from 2026 to 2033, driven by increasing availability of oral therapies and supportive care options that enable treatment in patient homes. Rising preference for home-based monitoring, telemedicine, and palliative care services supports growth. Convenience, cost savings, and reduced hospital visits encourage adoption. The COVID-19 pandemic accelerated the adoption of homecare services for cancer patients. Pharmaceutical companies are developing patient-friendly regimens suitable for home administration.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with a revenue share of 55% in 2025, due to direct access to patients receiving treatment in hospitals and centralized procurement of high-cost therapies. Hospital pharmacies ensure timely availability of drugs for inpatient and outpatient care. Collaboration with oncology departments and patient support programs reinforces adoption. Bulk purchasing agreements and insurance coverage facilitate affordability and access. Hospitals provide education and counseling on drug administration, improving patient adherence.

The online pharmacy segment is expected to witness the fastest growth rate of 21.2% from 2026 to 2033, driven by increasing e-commerce penetration, patient preference for home delivery, and growing awareness of online platforms offering prescription and supportive care products. Convenience, accessibility, and privacy considerations fuel online adoption. Integration with telemedicine and homecare services accelerates growth. Online pharmacies expand market reach to remote and underserved regions. Marketing initiatives and digital platforms increase patient engagement and awareness.

Gastric Cancer Market Regional Analysis

- North America dominated the gastric cancer market with the largest revenue share of 37.5% in 2025, characterized by high healthcare expenditure, advanced oncology infrastructure, and widespread adoption of early detection and targeted treatment options

- Patients and healthcare providers in the region highly value access to targeted therapies, immunotherapies, minimally invasive surgical procedures, and comprehensive oncology care, which improve survival outcomes and quality of life

- This widespread adoption is further supported by government healthcare programs, strong R&D investment by pharmaceutical and biotech companies, and a well-established network of hospitals and specialty centers, establishing North America as a leading market for gastric cancer treatment

U.S. Gastric Cancer Market Insight

The U.S. gastric cancer market captured the largest revenue share of 32% in 2025 within North America, driven by advanced healthcare infrastructure, high awareness of early detection programs, and widespread adoption of targeted therapies and immunotherapies. Patients increasingly prioritize access to precision medicine, minimally invasive surgeries, and comprehensive oncology care. The growing integration of molecular diagnostics, AI-assisted imaging, and personalized treatment protocols further propels market growth. Moreover, government healthcare initiatives and substantial R&D investment by pharmaceutical and biotech companies continue to expand the availability and adoption of innovative gastric cancer therapies.

Europe Gastric Cancer Market Insight

The Europe gastric cancer market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising awareness of early screening programs, stringent healthcare regulations, and an increasing demand for advanced oncology treatments. Urbanization, improved healthcare infrastructure, and growing accessibility to innovative therapies are fostering market adoption. European patients are increasingly drawn to targeted therapies and minimally invasive surgical procedures. The region is witnessing notable growth across hospitals, specialty centers, and cancer clinics, with early-stage detection and precision medicine approaches being increasingly implemented.

U.K. Gastric Cancer Market Insight

The U.K. gastric cancer market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising adoption of advanced diagnostics, early detection programs, and targeted therapies. Growing concerns regarding cancer incidence and patient survival are encouraging both healthcare providers and patients to pursue personalized treatment approaches. The U.K.’s strong healthcare system, coupled with well-established oncology research initiatives, supports the introduction of novel therapies. Increased awareness campaigns, integration of molecular diagnostics, and accessibility to specialty care are expected to sustain market growth.

Germany Gastric Cancer Market Insight

The Germany gastric cancer market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cancer prevention, advanced diagnostic facilities, and the demand for personalized treatment protocols. Germany’s well-developed healthcare infrastructure, emphasis on precision oncology, and robust hospital networks promote the adoption of advanced gastric cancer therapies. Integration of immunotherapy, targeted therapy, and minimally invasive surgery is increasingly prevalent. The focus on patient-centered care and government initiatives supporting cancer research also enhance market growth potential.

Asia-Pacific Gastric Cancer Market Insight

The Asia-Pacific gastric cancer market is poised to grow at the fastest CAGR of 18% during the forecast period of 2026 to 2033, driven by high gastric cancer prevalence in countries such as China, Japan, and South Korea. Rising awareness of early detection programs, increasing healthcare access, and technological advancements in diagnostics and treatments are key growth factors. The region’s growing emphasis on screening programs and government initiatives promoting cancer care are accelerating adoption. Furthermore, expanding hospital networks and specialty centers improve accessibility to advanced therapies for a larger patient population.

Japan Gastric Cancer Market Insight

The Japan gastric cancer market is gaining momentum due to the country’s high gastric cancer incidence, advanced healthcare infrastructure, and emphasis on early detection and prevention. Adoption of minimally invasive surgery, targeted therapies, and immunotherapies is increasing rapidly. Japan’s aging population further drives demand for effective and patient-friendly treatment options. Integration of molecular diagnostics and precision medicine into standard clinical practice enhances treatment outcomes. Government-led screening programs and well-established oncology centers continue to support market expansion.

India Gastric Cancer Market Insight

The India gastric cancer market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing awareness of cancer prevention, expanding healthcare infrastructure, and growing adoption of targeted and supportive therapies. India’s rising incidence of gastric cancer, coupled with government initiatives promoting cancer screening and treatment accessibility, is driving market growth. Expansion of specialty hospitals, oncology centers, and affordable therapy options further supports adoption. Growing patient awareness and domestic pharmaceutical manufacturing contribute to the increasing availability of advanced therapies across residential and commercial healthcare settings.

Gastric Cancer Market Share

The Gastric Cancer industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol Myers Squibb Company (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Celltrion, Inc. (South Korea)

- Daiichi Sankyo Company, Limited (Japan)

- Ono Pharmaceutical Co., Ltd. (Japan)

- Ipsen Pharma (France)

- Takeda Pharmaceutical Company Limited (Japan)

- GSK plc (U.K.)

- AbbVie Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Eisai Co., Ltd. (Japan)

What are the Recent Developments in Global Gastric Cancer Market?

- In November 2025, the U.S. Food and Drug Administration (FDA) granted approval to durvalumab (Imfinzi) plus FLOT chemotherapy as the first perioperative immunotherapy regimen for adults with resectable, early‑stage and locally advanced gastric and gastroesophageal junction (GEJ) cancers, marking a new standard of care that significantly improves survival outcomes in this setting

- In June 2025, Amgen announced positive Phase III results for its experimental targeted antibody bemarituzumab combined with chemotherapy, showing a statistically significant improvement in overall survival for patients with unresectable, locally advanced or metastatic FGFR2b‑positive gastric/GEJ cancer in the FORTITUDE‑101 trial, representing a potential advancement in targeted treatment option

- In August 2024, the UK’s Medicines and Healthcare products Regulatory Agency (MHRA) licensed a new targeted therapy, zolbetuximab (Vyloy), for adults with gastric or gastro‑oesophageal junction cancer whose tumors express the CLDN18.2 protein, expanding treatment options for biomarker‑defined patient subgroups

- In November 2023, the FDA amended the indication for pembrolizumab (Keytruda) in gastric or gastroesophageal junction adenocarcinoma, refining its use with trastuzumab and chemotherapy specifically for PD‑L1 (CPS ≥ 1) expressing tumors and approving a companion diagnostic to guide patient selection

- In April 2021, the FDA approved nivolumab (Opdivo) in combination with chemotherapy as the first immunotherapy‑based initial treatment for advanced or metastatic gastric, GEJ and related cancers, significantly extending median survival compared with chemotherapy alone and establishing immunotherapy as a key first‑line option

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.