Global Gastroesophageal Reflux Disease Market

Market Size in USD Billion

USD

5.24 Billion

USD

6.56 Billion

2025

2033

USD

5.24 Billion

USD

6.56 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.24 Billion | |

| USD 6.56 Billion | |

| % | |

|

Gastroesophageal Reflux Disease Market Size

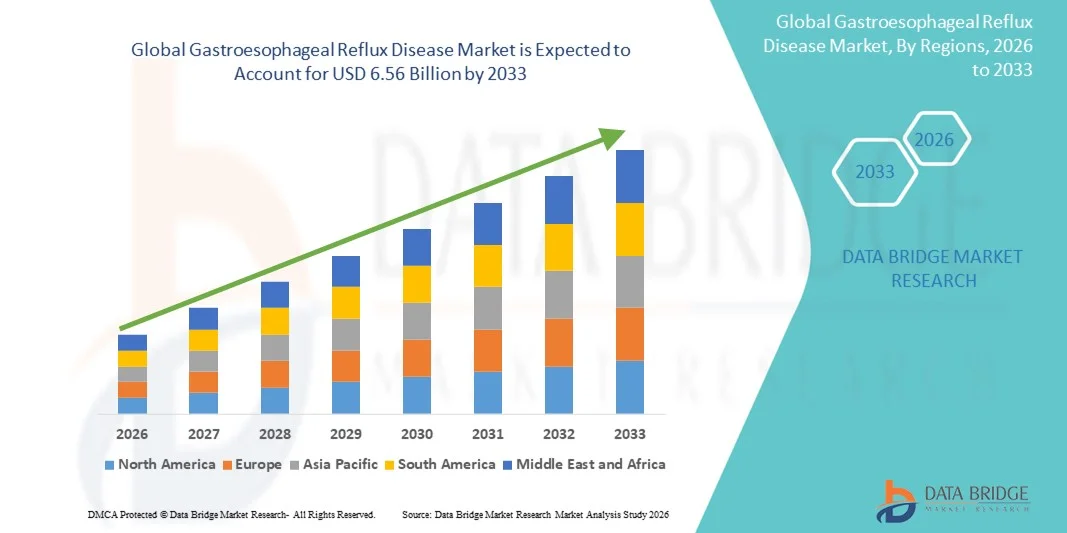

- The global gastroesophageal reflux disease market size was valued at USD 5.24 billion in 2025 and is expected to reach USD 6.56 billion by 2033, at a CAGR of 2.85% during the forecast period

- The market growth is largely fueled by the increasing prevalence of gastrointestinal disorders, changing dietary patterns, and rising awareness about digestive health, driving higher diagnosis and treatment rates globally

- Furthermore, the development of advanced therapeutic options, including proton pump inhibitors, minimally invasive procedures, and targeted drug delivery systems, is improving patient outcomes and convenience. These factors, combined with the rising demand for effective and accessible gastroesophageal reflux disease management solutions, are accelerating market adoption and driving the industry’s expansion

Gastroesophageal Reflux Disease Market Analysis

- Gastroesophageal Reflux Disease, characterized by the backflow of stomach acid into the esophagus, is increasingly recognized as a major gastrointestinal disorder affecting both adults and children, due to its impact on quality of life and potential for complications such as esophagitis and Barrett’s esophagus

- The escalating prevalence of gastroesophageal reflux disease is primarily fueled by changing dietary habits, obesity, sedentary lifestyles, and rising awareness of digestive health, which are driving higher diagnosis rates and increasing demand for effective treatment options

- North America dominated the gastroesophageal reflux disease market with the largest revenue share of 39.6% in 2025, driven by high awareness levels, widespread healthcare access, advanced diagnostic facilities, and the presence of key pharmaceutical companies developing innovative therapies

- Asia-Pacific is expected to be the fastest-growing region in the gastroesophageal reflux disease market during the forecast period due to increasing urbanization, rising disposable incomes, and growing awareness about gastrointestinal disorders

- Proton pump inhibitors (PPIs) segment dominated the gastroesophageal reflux disease market with a market share of 45.7% in 2025, driven by their established efficacy, safety profile, and widespread adoption as a first-line therapy for managing gastroesophageal reflux disease symptoms

Report Scope and Gastroesophageal Reflux Disease Market Segmentation

|

Attributes |

Gastroesophageal Reflux Disease Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Gastroesophageal Reflux Disease Market Trends

Rising Adoption of Minimally Invasive and Endoscopic Procedures

- A significant and accelerating trend in the global gastroesophageal reflux disease market is the increasing adoption of minimally invasive and endoscopic interventions, improving patient outcomes and reducing recovery times

- For instance, the LINX Reflux Management System provides a magnetic sphincter augmentation procedure as a less invasive alternative to traditional surgery, offering symptom relief and faster recovery

- These procedures enable gastroenterologists to address reflux symptoms more effectively with reduced postoperative complications, shorter hospital stays, and quicker return to daily activities, enhancing patient satisfaction

- The integration of advanced imaging and endoscopic technologies facilitates precise targeting of affected areas, enabling tailored interventions and improved long-term efficacy of gastroesophageal reflux disease treatments

- This trend towards less invasive yet highly effective treatment options is reshaping patient expectations and encouraging healthcare providers to adopt innovative therapeutic approaches

- The demand for minimally invasive gastroesophageal reflux disease management solutions is growing rapidly across both adult and pediatric populations, as patients and physicians increasingly prioritize safety, convenience, and long-term symptom control

- In addition, the rise of wearable and remote monitoring devices that track GERD symptoms and patient response is creating opportunities for more personalized and data-driven management strategies

- Increased collaborations between medical device companies and healthcare providers to develop next-generation endoscopic tools are further accelerating technological innovation and market expansion

Gastroesophageal Reflux Disease Market Dynamics

Driver

Increasing Prevalence of GERD and Rising Awareness of Digestive Health

- The growing incidence of gastroesophageal reflux disease, combined with heightened awareness of gastrointestinal health, is a significant driver for the expanding market demand

- For instance, in March 2025, Takeda Pharmaceuticals highlighted initiatives to improve awareness and early diagnosis of GERD through educational campaigns and physician outreach programs

- As lifestyle-related risk factors such as obesity, poor dietary habits, and sedentary behavior continue to rise, more individuals are seeking effective diagnostic and treatment solutions for gastroesophageal reflux disease

- Furthermore, improved access to healthcare facilities and advanced treatment options, including proton pump inhibitors and endoscopic procedures, is making GERD management more accessible to a wider population

- The increasing focus on early diagnosis, patient education, and long-term disease management is driving higher adoption rates of therapies and interventions, boosting the overall market growth

- The demand for comprehensive gastroesophageal reflux disease solutions, including medications, procedures, and monitoring, is further supported by the growing emphasis on improving patient quality of life and reducing disease-related complication

- Expanding research and development initiatives by pharmaceutical and medical device companies to create novel therapies are expected to generate new growth avenues in the gastroesophageal reflux disease market

- Growing government support and healthcare reimbursement policies for GERD management in key markets are further facilitating market expansion and accessibility

Restraint/Challenge

Drug Side Effects and Limited Awareness in Emerging Regions

- Concerns about the side effects of long-term GERD medications, such as proton pump inhibitors, pose a significant challenge to broader market adoption

- For instance, reports of kidney disease, nutrient deficiencies, and other complications associated with prolonged PPI use have made some patients hesitant to continue therapy without careful medical supervision

- Addressing these concerns through safer formulations, alternative therapies, and patient education is crucial for sustaining consumer confidence and treatment adherence

- In addition, limited awareness and insufficient healthcare infrastructure in emerging regions can delay diagnosis and restrict access to advanced gastroesophageal reflux disease treatments, hampering market penetration

- The relatively high cost of certain innovative therapies and procedures compared to standard medication can also act as a barrier for price-sensitive patients, particularly in developing countries

- Overcoming these challenges through improved patient education, regional awareness programs, and the development of affordable treatment options will be vital for sustained growth in the gastroesophageal reflux disease market

- Variability in patient response to existing therapies and the chronic nature of GERD can result in inconsistent treatment outcomes, creating hurdles for market expansion

- Regulatory approvals for new drugs and devices can be time-consuming and costly, delaying product launches and limiting immediate availability in certain regions

Gastroesophageal Reflux Disease Market Scope

The market is segmented on the basis of drug class, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the gastroesophageal reflux disease market is segmented into antacids, proton pump inhibitors (PPIs), H2 receptor blockers, pro-kinetic agents, and others. The proton pump inhibitors (PPIs) segment dominated the market with the largest market revenue share of 45.7% in 2025, owing to their established efficacy in suppressing gastric acid production and widespread adoption as a first-line therapy for GERD. PPIs are preferred by physicians for both acute symptom management and long-term treatment, supported by strong clinical evidence and patient familiarity. The segment also benefits from a broad range of formulations, including delayed-release tablets and oral suspensions, enhancing patient adherence. Brand awareness, extensive insurance coverage in developed markets, and ongoing R&D for next-generation PPIs further consolidate its dominance. In addition, PPIs are increasingly incorporated into combination therapies for patients with severe or refractory GERD, driving higher usage.

The H2 receptor blockers segment is expected to witness the fastest growth from 2026 to 2033, fueled by their affordability, OTC availability, and efficacy in mild to moderate GERD management. These drugs are also favored in emerging markets due to lower costs and ease of administration. H2 receptor blockers are increasingly recommended as step-down therapy post-PPI treatment, expanding their patient base. In addition, the introduction of novel H2 blockers with improved safety profiles and fewer drug interactions is supporting market adoption. Patient preference for self-administered, fast-acting remedies is further accelerating demand in this segment.

- By Route of Administration

On the basis of route of administration, the gastroesophageal reflux disease market is segmented into oral, parenteral, and others. The oral segment dominated the market with the largest share of 87% in 2025, driven by ease of use, patient compliance, and suitability for long-term therapy. Oral administration allows patients to self-manage symptoms conveniently at home and provides flexibility across various drug classes, including PPIs, H2 blockers, and antacids. Pharmaceutical companies are also introducing novel oral formulations, such as effervescent tablets and capsules with faster onset, to meet consumer preferences. The cost-effectiveness and wide availability of oral medications further contribute to their market dominance. Furthermore, oral administration is preferred in both hospital and homecare settings, consolidating its leading position.

The parenteral segment is expected to witness the fastest growth from 2026 to 2033, primarily driven by hospitalized or critically ill GERD patients requiring intravenous therapy. Parenteral formulations offer rapid symptom relief and precise dosing, particularly in acute cases or patients with swallowing difficulties. Increasing adoption in specialty clinics and ICU settings is expanding market opportunities. Advancements in IV delivery systems and improved safety profiles of injectable drugs also support growth in this segment.

- By End-Users

On the basis of end-users, the gastroesophageal reflux disease market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest share of 52% in 2025, owing to the high number of diagnosed GERD cases requiring professional monitoring and treatment. Hospitals provide access to a wide range of therapeutic options, including prescription PPIs, endoscopic procedures, and inpatient care for severe cases. In addition, hospitals are often the first point of care for GERD patients, increasing drug utilization and adoption of advanced therapies. Presence of gastroenterologists, diagnostic facilities, and integrated care pathways further reinforce dominance. Strategic collaborations with pharmaceutical companies also enhance hospital procurement of GERD medications.

The homecare segment is expected to witness the fastest growth from 2026 to 2033, fueled by the rising demand for self-management of GERD symptoms and the convenience of OTC medications and home-based therapies. Increasing awareness of lifestyle modifications, telemedicine consultations, and remote monitoring tools are contributing to the growth of homecare treatment. Patient preference for non-invasive, easy-to-administer therapies in home settings is expanding market opportunities. Growth in digital health platforms providing medication guidance and symptom tracking further supports this segment.

- By Distribution Channel

On the basis of distribution channel, the gastroesophageal reflux disease market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The retail pharmacy segment dominated the market with the largest share of 44% in 2025, driven by the widespread availability of GERD medications, including OTC and prescription drugs, and ease of access for patients. Retail pharmacies also offer counseling services and product variety, enhancing consumer convenience. The segment benefits from strong brand presence and trust among patients, particularly for commonly used therapies such as PPIs and H2 blockers. Marketing campaigns, discount programs, and loyalty initiatives further strengthen retail pharmacy dominance. Moreover, the presence of pharmacies in both urban and semi-urban regions ensures broad reach across patient populations.

The online pharmacy segment is expected to witness the fastest growth from 2026 to 2033, fueled by increasing e-commerce penetration, convenience of home delivery, and rising consumer comfort with digital transactions. Online platforms allow patients to access a wide range of GERD medications, including prescription refills and specialty drugs, with discreet delivery and privacy. Telemedicine integration with online pharmacies further facilitates prescription fulfillment. Growth in smartphone adoption, internet penetration, and digital healthcare initiatives is accelerating this trend globally.

Gastroesophageal Reflux Disease Market Regional Analysis

- North America dominated the gastroesophageal reflux disease market with the largest revenue share of 39.6% in 2025, driven by high awareness levels, widespread healthcare access, advanced diagnostic facilities, and the presence of key pharmaceutical companies developing innovative therapies

- Consumers and patients in the region highly value access to advanced diagnostic tools, effective treatment options such as proton pump inhibitors, and minimally invasive procedures, contributing to higher adoption rates

- This widespread adoption is further supported by strong healthcare reimbursement policies, high disposable incomes, and a growing focus on early diagnosis and long-term disease management, establishing North America as a key market for gastroesophageal reflux disease therapies

U.S. Gastroesophageal Reflux Disease Market Insight

The U.S. gastroesophageal reflux disease market captured the largest revenue share of 82% in 2025 within North America, fueled by the high prevalence of GERD and widespread access to advanced healthcare services. Patients are increasingly prioritizing effective treatment options, including proton pump inhibitors, H2 receptor blockers, and minimally invasive procedures. The growing preference for home-based care and telemedicine consultations, combined with robust demand for OTC medications and personalized therapy, further propels the GERD market. Moreover, the increasing awareness of lifestyle modifications and early diagnosis is significantly contributing to the market’s expansion.

Europe Gastroesophageal Reflux Disease Market Insight

The Europe gastroesophageal reflux disease market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of GERD and the growing demand for effective treatments in both residential and clinical settings. The increase in urbanization, along with rising healthcare expenditure, is fostering the adoption of innovative therapies. European patients are also drawn to advanced medications and minimally invasive procedures due to their convenience and efficacy. The region is experiencing significant growth across hospitals, specialty clinics, and homecare applications, with GERD management increasingly incorporated into routine healthcare practices.

U.K. Gastroesophageal Reflux Disease Market Insight

The U.K. gastroesophageal reflux disease market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on digestive health and early diagnosis of GERD. In addition, concerns regarding long-term complications such as esophagitis and Barrett’s esophagus are encouraging both patients and healthcare providers to adopt effective treatments. The U.K.’s strong healthcare infrastructure, alongside its robust pharmacy and online healthcare systems, is expected to continue stimulating market growth. The adoption of lifestyle modification programs and patient education initiatives further supports the expansion of GERD management solutions.

Germany Gastroesophageal Reflux Disease Market Insight

The Germany gastroesophageal reflux disease market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of digestive health and the demand for technologically advanced diagnostic and treatment options. Germany’s well-developed healthcare infrastructure, combined with its focus on innovation and preventive care, promotes the adoption of effective GERD therapies in hospitals and specialty clinics. The integration of telemedicine and homecare management systems is also becoming increasingly prevalent, with patients showing a strong preference for accessible and personalized treatment options.

Asia-Pacific Gastroesophageal Reflux Disease Market Insight

The Asia-Pacific gastroesophageal reflux disease market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by rising prevalence of GERD, increasing urbanization, and growing healthcare expenditure in countries such as China, Japan, and India. The region's expanding healthcare infrastructure, coupled with awareness campaigns and lifestyle disease management initiatives, is driving the adoption of GERD treatments. Furthermore, the development of affordable medications and minimally invasive procedures is increasing accessibility to a wider patient base.

Japan Gastroesophageal Reflux Disease Market Insight

The Japan gastroesophageal reflux disease market is gaining momentum due to the country’s high awareness of digestive health, aging population, and increasing prevalence of GERD. Japanese patients prioritize early diagnosis and effective treatment options, which is driving the adoption of proton pump inhibitors, endoscopic procedures, and homecare therapies. The integration of digital health monitoring and telemedicine platforms with GERD management is fueling growth. Moreover, Japan’s focus on preventive healthcare and chronic disease management is expected to further expand the market across hospitals and homecare settings.

India Gastroesophageal Reflux Disease Market Insight

The India gastroesophageal reflux disease market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the growing prevalence of GERD, rapid urbanization, and increasing healthcare awareness. India represents a large and expanding patient population seeking effective and affordable treatment options. The push towards telemedicine, digital health solutions, and the availability of cost-effective medications are key factors propelling market growth. In addition, increasing adoption of lifestyle modification programs and homecare management solutions is supporting the expansion of GERD management across both urban and semi-urban regions.

Gastroesophageal Reflux Disease Market Share

The Gastroesophageal Reflux Disease industry is primarily led by well-established companies, including:

- AstraZeneca (U.K.)

- Pfizer Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- GSK plc (U.K.)

- Eisai Co., Ltd. (Japan)

- Johnson & Johnson Services, Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sanofi (France)

- Bayer AG (Germany)

- Dr. Reddy’s Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Perrigo Company plc (Ireland)

- Aurobindo Pharma Limited (India)

- Cipla (India)

- Lupin (India)

- Cadila Healthcare Ltd. (India)

- Bausch Health (Canada.)

- HK inno.N Corporation (South Korea)

- Sebela Pharmaceuticals, Inc. (U.S.)

What are the Recent Developments in Global Gastroesophageal Reflux Disease Market?

- In October 2025, a notable development came from Akums Drugs and Pharmaceuticals Ltd. which secured a 20‑year patent (granted by the Indian Patent Office) for a “Dual‑Release Gastro‑Resistant Composition” a next‑generation PPI formulation aimed at providing extended acid suppression and improved therapeutic action for moderate‑to‑severe or treatment‑resistant GERD

- In March 2025, the American Society for Gastrointestinal Endoscopy (ASGE) updated its clinical practice guideline to formally include and recommend Transoral Incisionless Fundoplication (TIF 2.0) and its variant, cTIF as evidence‑based, endoscopic treatment options for selected GERD patients, offering a less invasive alternative to long-term medical therapy or traditional surgery

- In August 2024, the FDA authorized a labeling update for the LINX Reflux Management System (a magnetic‑sphincter augmentation device) to expand its indication to include patients with Barrett’s esophagus (BE) experiencing GERD thereby making this mechanical reflux control option available to a broader and higher‑risk patient subset

- In July 2024, the FDA expanded approval of vonoprazan to include heartburn associated with non‑erosive GERD in adults providing a new, first‑in‑class potassium‑competitive acid blocker (PCAB) option and broadening treatment beyond traditional proton‑pump inhibitors (PPIs)

- In November 2023, the VOQUEZNA (vonoprazan) tablet was approved by the U.S. Food and Drug Administration (FDA) for treatment of all grades of erosive GERD (erosive esophagitis), marking the first major innovation in the U.S. GERD treatment landscape in over 30 years.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.