Global Gel Stent Market

Market Size in USD Billion

USD

1.60 Billion

USD

2.57 Billion

2025

2033

USD

1.60 Billion

USD

2.57 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.60 Billion | |

| USD 2.57 Billion | |

| % | |

|

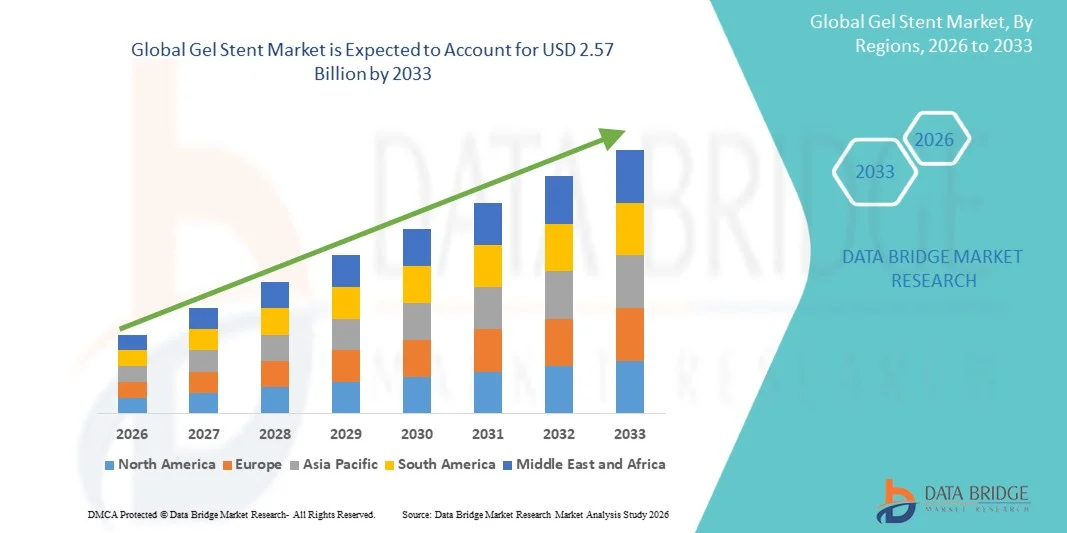

Gel Stent Market Size

- The global gel stent market size was valued at USD 1.60 billion in 2025 and is expected to reach USD 2.57 billion by 2033, at a CAGR of 6.14% during the forecast period

- The market growth is largely fueled by the rising prevalence of glaucoma, increasing awareness about early disease management, and growing preference for minimally invasive glaucoma surgeries (MIGS) that offer effective intraocular pressure reduction with fewer complications

- Furthermore, increasing adoption of gel stent procedures by ophthalmologists, favorable clinical outcomes, shorter recovery times, and continuous advancements in implant design and surgical techniques are accelerating the uptake of Gel Stent solutions, thereby significantly boosting the industry’s growth

Gel Stent Market Analysis

- Gel stents, used in minimally invasive glaucoma surgery (MIGS) to reduce intraocular pressure, are becoming an essential treatment option in ophthalmology due to their safety profile, shorter recovery time, and effectiveness in managing open-angle glaucoma

- The increasing demand for gel stents is primarily driven by the rising global prevalence of glaucoma, growing preference for minimally invasive surgical procedures, increasing diagnosis rates due to better screening, and advancements in ophthalmic implant technologies

- North America dominated the gel stent market with the largest revenue share of 37.9% in 2025, supported by a well-established ophthalmology care infrastructure, high adoption of MIGS procedures, strong presence of leading ophthalmic device manufacturers, and increasing glaucoma patient pool, with the U.S. contributing the majority of regional revenue

- Asia-Pacific is expected to be the fastest-growing region in the gel stent market during the forecast period, driven by a rapidly aging population, rising glaucoma prevalence, improving access to advanced eye care, growing healthcare expenditure, and increasing adoption of minimally invasive glaucoma treatments in countries such as China, Japan, and India

- The clinical phase III segment dominated the largest market revenue share of 41.6% in 2025, driven by the increasing number of late-stage trials evaluating Gel Stents for the treatment of glaucoma

Report Scope and Gel Stent Market Segmentation

|

Attributes |

Gel Stent Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Gel Stent Market Trends

“Rising Adoption of Minimally Invasive Glaucoma Surgery (MIGS) Devices”

- A significant and accelerating trend in the global Gel Stent market is the increasing adoption of minimally invasive glaucoma surgery (MIGS) procedures aimed at effectively reducing intraocular pressure (IOP) while minimizing surgical trauma and postoperative complications

- Gel stents are gaining strong clinical acceptance due to their ability to provide sustained aqueous humor outflow with a less invasive implantation technique compared to traditional glaucoma surgeries such as trabeculectomy

- For instance, the XEN Gel Stent (Allergan, a AbbVie company) has been widely adopted in Europe and North America for early-to-moderate open-angle glaucoma

- Advancements in biocompatible materials and refined stent designs are improving safety profiles, implantation consistency, and long-term clinical outcomes, further supporting the growing use of gel stents in glaucoma management

- Ophthalmologists are increasingly incorporating gel stents into earlier lines of treatment, particularly for patients with mild-to-moderate open-angle glaucoma who are inadequately controlled with medications alone

- In addition, growing awareness among clinicians and patients regarding the benefits of MIGS—including shorter recovery times, reduced complication rates, and preservation of conjunctival tissue—is positively influencing gel stent adoption worldwide

- This shift toward less invasive, procedure-based glaucoma treatments is reshaping treatment paradigms and strengthening demand for gel stent technologies across both developed and emerging healthcare markets

Gel Stent Market Dynamics

Driver

“Increasing Prevalence of Glaucoma and Demand for Safer Surgical Alternatives”

- The rising global prevalence of glaucoma, driven by aging populations and increasing life expectancy, is a key driver of growth in the Gel Stent market. Glaucoma remains one of the leading causes of irreversible blindness, necessitating effective long-term intraocular pressure management

- A growing number of patients are becoming refractory or non-compliant to topical medications, creating a strong need for interventional solutions such as gel stents that offer sustained pressure reduction

- For instance, clinical studies in the United States have shown that patients receiving the iStent inject (Glaukos Corporation) achieved significant IOP reduction with fewer postoperative medications

- The demand for safer and less invasive surgical alternatives to conventional glaucoma surgeries is further accelerating market growth, as gel stents are associated with fewer complications, reduced hospitalization, and faster postoperative recovery

- Increasing adoption of outpatient ophthalmic surgeries and the expansion of specialized eye care centers are also contributing to higher procedural volumes involving gel stents

- Moreover, favorable clinical outcomes reported in long-term studies and the increasing training of ophthalmic surgeons in MIGS techniques are supporting broader market penetration

Restraint/Challenge

“High Procedure Costs and Limited Reimbursement Coverage”

- The relatively high cost associated with gel stent devices and implantation procedures represents a significant restraint to market growth, particularly in price-sensitive regions and developing healthcare systems

- Limited or inconsistent reimbursement policies for MIGS procedures in several countries can discourage adoption, especially when compared to more established glaucoma treatment options

- For instance, in many regions of Asia-Pacific, reimbursement for XEN® Gel Stent implantation is limited, resulting in slower uptake

- In addition, the requirement for specialized surgical expertise and training may restrict the use of gel stents to experienced ophthalmic surgeons, limiting availability in smaller or rural healthcare settings

- Potential postoperative complications, such as stent blockage, fibrosis, or hypotony, though less frequent than in traditional surgeries, may also create hesitation among some clinicians

- Overcoming these challenges through improved reimbursement frameworks, cost optimization, enhanced surgeon training, and continued clinical evidence generation will be essential for sustained growth of the global Gel Stent market

Gel Stent Market Scope

The market is segmented on the basis of clinical trials and end user.

• By Clinical Trials

On the basis of clinical trials, the Gel Stent market is segmented into preclinical, clinical phase I, clinical phase II, clinical phase I/II, clinical phase III, and research. The clinical phase III segment dominated the largest market revenue share of 41.6% in 2025, driven by the increasing number of late-stage trials evaluating Gel Stents for the treatment of glaucoma. Phase III trials are critical for regulatory approval and commercialization, leading to higher investments from medical device manufacturers and pharmaceutical companies. These trials involve large patient populations and multi-center studies, significantly increasing associated expenditures. Regulatory agencies place strong emphasis on Phase III outcomes, which further accelerates funding and participation. The growing prevalence of glaucoma globally has intensified the focus on advanced-stage trials. In addition, strong clinical efficacy and safety outcomes reported in Phase III studies have reinforced confidence among stakeholders. Increased collaboration between device developers and ophthalmology research centers also supports this dominance. As a result, Phase III trials continue to command the largest share of market revenue.

The clinical phase I/II segment is anticipated to witness the fastest CAGR of 13.8% from 2026 to 2033, owing to the rising pipeline of innovative minimally invasive glaucoma surgery (MIGS) Gel Stent technologies. Early-stage trials enable rapid evaluation of safety, dosing, and preliminary efficacy, encouraging manufacturers to accelerate development timelines. Increasing venture capital funding and government research grants are supporting early-phase clinical programs. Academic-industry collaborations are also driving growth in combined Phase I/II studies. These trials reduce development risk by integrating early safety and efficacy assessments. Growing interest in next-generation bioengineered Gel Stents further fuels this trend. Faster regulatory pathways for breakthrough ophthalmic devices also support early-stage trial expansion. Consequently, the Phase I/II segment is expected to grow at the fastest rate during the forecast period.

• By End User

On the basis of end user, the Gel Stent market is segmented into hospitals, eye clinics, eye research institutes, and others. The hospitals segment accounted for the largest market revenue share of 46.9% in 2025, driven by the high volume of glaucoma surgeries performed in hospital settings. Hospitals possess advanced surgical infrastructure, skilled ophthalmic surgeons, and access to integrated diagnostic facilities, making them the primary centers for Gel Stent implantation. The availability of reimbursement coverage in hospital settings further supports adoption. Hospitals also serve as key sites for clinical trials and post-market surveillance studies. Growing patient preference for hospital-based minimally invasive glaucoma procedures contributes to demand. In addition, hospitals manage complex and advanced glaucoma cases requiring surgical intervention. Strong referral networks and multidisciplinary care further strengthen hospital dominance. As a result, hospitals remain the leading end-user segment in terms of revenue.

The eye clinics segment is expected to witness the fastest CAGR of 14.5% from 2026 to 2033, driven by the rapid expansion of specialized ophthalmology clinics worldwide. Eye clinics offer focused glaucoma care, shorter waiting times, and cost-effective outpatient surgical procedures. The growing adoption of minimally invasive Gel Stent procedures aligns well with clinic-based surgical models. Technological advancements have enabled clinics to perform complex procedures previously limited to hospitals. Increasing patient awareness and preference for specialized eye care centers further accelerates growth. Rising investments in standalone ophthalmology clinics across emerging markets also support expansion. Clinics are increasingly participating in early adoption of innovative Gel Stent technologies. These factors collectively position eye clinics as the fastest-growing end-user segment over the forecast period.

Gel Stent Market Regional Analysis

- North America dominated the gel stent market with the largest revenue share of 37.9% in 2025, supported by a well-established ophthalmology care infrastructure, high adoption of MIGS procedures, strong presence of leading ophthalmic device manufacturers, and an increasing glaucoma patient pool, with the U.S. contributing the majority of regional revenue

- Consumers in the region highly value the convenience, advanced features, and clinical benefits offered by gel stents for minimally invasive glaucoma surgery

- This widespread adoption is further supported by high healthcare spending, strong physician awareness, and growing demand for innovative ophthalmic interventions, establishing gel stents as a preferred solution in both hospitals and specialized eye care centers

U.S. Gel Stent Market Insight

The U.S. gel stent market captured the largest revenue share within North America in 2025, fueled by high procedure volumes, early adoption of minimally invasive glaucoma surgery techniques, and the continuous introduction of next-generation devices. The growing preference for less invasive, outpatient glaucoma procedures, combined with the strong presence of leading ophthalmic device manufacturers and established reimbursement frameworks, further propels the U.S. market. Moreover, increasing awareness among patients and ophthalmologists regarding safety and efficacy benefits of gel stents significantly contributes to market expansion.

Europe Gel Stent Market Insight

Europe gel stent market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by an aging population, increasing prevalence of glaucoma, and rising adoption of minimally invasive glaucoma surgery techniques. The region is witnessing significant growth across hospitals, specialty clinics, and ophthalmology centers, supported by government initiatives promoting early glaucoma detection and treatment. European patients are also drawn to the reduced recovery times and improved safety profiles of gel stents.

U.K. Gel Stent Market Insight

The U.K. gel stent market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing glaucoma prevalence, rising patient awareness, and adoption of innovative, minimally invasive treatments. Additionally, a well-established ophthalmology infrastructure and supportive healthcare policies encourage both hospitals and specialty clinics to implement gel stent procedures.

Germany Gel Stent Market Insight

Germany gel stent market is expected to expand at a considerable CAGR during the forecast period, fueled by technological advancements in ophthalmic devices, high physician awareness, and strong hospital networks offering advanced glaucoma treatments. Germany’s emphasis on innovation and quality healthcare services promotes gel stent adoption, particularly in leading hospitals and specialized eye care centers.

Asia-Pacific Gel Stent Market Insight

Asia-Pacific gel stent market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by a rapidly aging population, rising glaucoma prevalence, improving access to advanced eye care, growing healthcare expenditure, and increasing adoption of minimally invasive glaucoma procedures in countries such as China, Japan, and India. The region’s expanding ophthalmology infrastructure and government initiatives to improve eye care accessibility are further supporting market growth. Moreover, increasing awareness among patients and ophthalmologists regarding the safety and efficacy of gel stents is boosting adoption across hospitals and specialized clinics.

Japan Gel Stent Market Insight

Japan gel stent market is gaining momentum due to the country’s high glaucoma prevalence, aging population, and increasing preference for minimally invasive ophthalmic procedures. The Japanese market places significant emphasis on early diagnosis and effective treatment, and gel stents are becoming a preferred option for ophthalmologists. Integration with advanced surgical techniques and training programs further fuels market growth.

China Gel Stent Market Insight

China gel stent market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising glaucoma incidence, expanding middle-class population, rapid urbanization, and improving access to advanced eye care. China’s increasing healthcare infrastructure, growing patient awareness, and adoption of minimally invasive glaucoma procedures are key factors propelling market growth. The presence of local and international gel stent manufacturers, along with supportive government policies, is further enhancing accessibility and adoption in hospitals and specialty ophthalmology clinics.

Gel Stent Market Share

The Gel Stent industry is primarily led by well-established companies, including:

- Santen (Japan)

- Ivantis (U.S.)

- Glaukos (U.S.)

- New World Medical (U.S.)

- Oertli Instrumente AG (Switzerland)

- AqueSys (U.S.)

- Lumenis (Israel)

- Carl Zeiss Meditec (Germany)

- MicroSurgical Technology (U.S.)

- Oculus Surgical (U.S.)

- Hoya Corporation (Japan)

- BVI Medical (U.S.)

- iSTAR Medical (Belgium)

- Ellex Medical Lasers (Australia)

- Optonol Ltd. (Israel)

- Katena Products (U.S.)

- SurgiTel (U.S.)

- Medennium (U.S.)

Latest Developments in Global Gel Stent Market

- In June 2025, Glaukos Corporation announced that its iStent infinite® and related MIGS (Micro‑Invasive Glaucoma Surgery) technologies received European Union Medical Device Regulation (EU MDR) certification, marking the company’s first regulatory approvals under the updated EU framework and enabling broader commercialization of its trabecular micro‑bypass stents across Europe. This milestone supports expansion of one of the leading gel stent families and reinforces Glaukos’ global leadership in minimally invasive glaucoma devices

- In May 2023, market intelligence publications noted that the global eye stent market saw significant product introductions and portfolio expansions, including next‑generation designs and MIGS devices, with companies such as Glaukos, Alcon (with Hydrus Microstent), and Santen driving innovation and competitive positioning in key regions. This period marked a wave of product activity that expanded clinical options for glaucoma surgery

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.