Global Gene Regulation Therapy Market

Market Size in USD Billion

USD

1.12 Billion

USD

5.14 Billion

2025

2033

USD

1.12 Billion

USD

5.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.12 Billion | |

| USD 5.14 Billion | |

| % | |

|

Gene Regulation Therapy Market Size

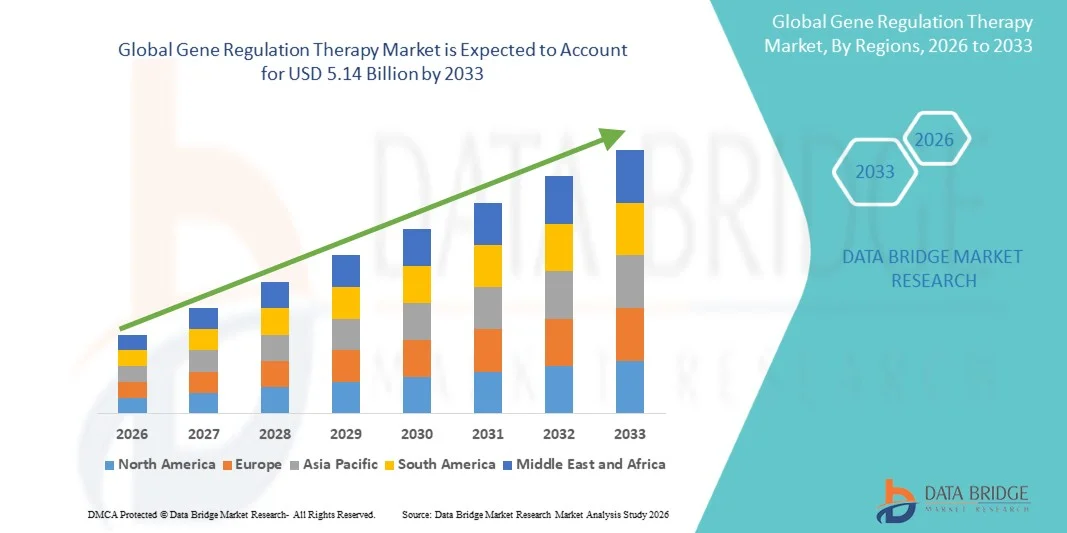

- The global Gene Regulation Therapy market size was valued at USD 1.12 billion in 2025 and is expected to reach USD 5.14 billion by 2033, at a CAGR of 21.00% during the forecast period

- The market growth is largely fueled by rapid advancements in genetic engineering, viral and non-viral vector technologies, and personalized medicine approaches, enabling more effective and targeted therapeutic interventions for rare and chronic diseases with previously unmet medical needs

- Furthermore, increasing prevalence of genetic disorders, growing regulatory support from agencies such as the FDA and EMA for accelerated approvals of advanced gene therapies, and rising investment from biopharmaceutical companies in gene therapy R&D pipelines are driving robust adoption. These converging factors are accelerating the uptake of gene regulation therapy solutions, thereby significantly boosting the industry's growth

Gene Regulation Therapy Market Analysis

- Gene regulation therapies, encompassing approaches such as gene silencing, gene augmentation, gene editing, and oncolytic immunotherapy, are increasingly recognized as transformative medical interventions capable of addressing the root genetic causes of diseases rather than merely managing symptoms, making them central to the evolution of precision medicine

- The escalating demand for gene regulation therapies is primarily fueled by rising oncology incidence, growing clinical success of CAR-T and viral vector-based gene therapies, expanding regulatory approvals for next-generation gene products, and increasing investment from both public and private stakeholders in gene therapy manufacturing and clinical development infrastructure

- North America dominated the gene regulation therapy market with the largest revenue share of 41.36% in 2025, supported by 45 new RMAT designations, the CMS Access Model easing Medicaid barriers, robust R&D infrastructure, and the presence of leading biopharmaceutical companies including Novartis, Bristol-Myers Squibb, and Sarepta Therapeutics. The U.S. accounted for the majority of regional revenues, driven by rapid FDA approvals and the highest concentration of gene therapy clinical trials globally

- Asia-Pacific is expected to be the fastest growing region in the gene regulation therapy market during the forecast period due to expanding healthcare investments, improving clinical trial activity, and a large patient population with high burden of genetic and oncological diseases

- The viral vectors segment dominated the gene regulation therapy market with a market share of 74.83% in 2025, driven by the high delivery efficiency of adeno-associated viruses (AAV) and lentiviral vectors across multiple therapeutic indications

Report Scope and Gene Regulation Therapy Market Segmentation

|

Attributes |

Gene Regulation Therapy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Gene Regulation Therapy Market Trends

“Accelerating CRISPR-Based Gene Editing Adoption and AI-Driven Vector Design Innovation”

- A significant and accelerating trend in the global gene regulation therapy market is the deepening integration of CRISPR-Cas9 genome editing with advanced AI-driven bioinformatics platforms, enabling unprecedented precision in gene targeting and substantially accelerating the development of next-generation gene regulation therapies for both rare and common diseases

- For instance, in January 2024, the FDA published two final guidance documents on human gene therapy products incorporating human genome editing and CAR T-cell development, providing regulatory clarity that is expected to accelerate the commercial development pipeline for CRISPR-based and other advanced gene regulation approaches

- AI integration in gene regulation therapy enables transformative capabilities including rapid identification of optimal gene targets, predictive modeling of off-target editing effects, personalized vector capsid engineering, and accelerated patient stratification for clinical trials. In addition, companies such as uniQure demonstrated a remarkable 79% huntingtin-protein knockdown using engineered AAV delivery, underscoring the clinical potential of AI-optimized vector design for neurological gene regulation applications

- The seamless integration of gene regulation therapies with multiomics data platforms and real-world evidence systems is enabling more precise patient identification, treatment personalization, and outcomes monitoring, creating a more comprehensive and scalable gene therapy ecosystem. Through unified genomic data platforms, researchers and clinicians can identify regulatory gene targets and optimize therapeutic delivery strategies with substantially reduced development timelines

- This trend toward more intelligent, precise, and clinically validated gene regulation modalities is fundamentally reshaping treatment paradigms across oncology, rare genetic diseases, and neurological disorders. Consequently, companies such as Editas Medicine and Intellia Therapeutics are advancing in vivo CRISPR-based gene regulation candidates into late-stage clinical trials across multiple indications

- The demand for CRISPR-based and AI-optimized gene regulation therapies is growing rapidly across both clinical and research settings, as biopharmaceutical companies and academic institutions increasingly prioritize one-time curative treatment approaches that address disease at the genetic regulatory level

Gene Regulation Therapy Market Dynamics

Driver

“Rising Genetic Disease Burden and Expanding Regulatory Approvals Driving Adoption”

- The escalating prevalence of genetic and oncological disorders globally, combined with an expanding pipeline of regulatory approvals for advanced gene therapy products, is a primary driver for the heightened demand for gene regulation therapies across multiple disease areas

- For instance, in February 2023, the FDA created a new Office of Therapeutic Products (OTP) within CBER to address the rapidly growing workload from cell and gene therapy submissions, reinforcing the regulatory authority's commitment to accelerating CGT review and approval timelines. Such structural investments by regulatory agencies are expected to drive gene regulation therapy market growth significantly throughout the forecast period

- As patients and clinicians increasingly recognize the potential of gene regulation therapies to provide durable or curative treatment outcomes, demand for approved products such as Zolgensma, Yescarta, Kymriah, and Luxturna continues to grow, while an expanding pipeline of late-stage gene regulation candidates across oncology, neurology, and rare disease indications signals sustained future market expansion

- Furthermore, the growing recognition of gene regulation therapies in emerging indications such as hemophilia, spinal muscular atrophy, and retinal dystrophies, supported by positive long-term durability data extending beyond five years post-treatment, is strengthening physician and payer confidence in the value proposition of advanced gene therapy interventions

- The trend toward outcomes-based reimbursement models and platform manufacturing efficiencies is transforming gene regulation therapy from a high-cost experimental modality into a commercially scalable and payer-accessible treatment category, further propelling adoption across both developed healthcare markets and increasingly in emerging economies

Restraint/Challenge

“High Therapy Costs, Manufacturing Complexity, and Regulatory Uncertainty”

- The high cost of gene regulation therapies, with approved products frequently priced at several hundred thousand to over one million USD per treatment, poses a significant barrier to patient access and broad commercial adoption, particularly in markets with underdeveloped reimbursement frameworks and limited payer coverage for advanced gene therapies

- For instance, the February 2025 discontinuation of Pfizer's fidanacogene elaparvovec (Beqvez) despite FDA approval in April 2024 highlighted the commercial viability challenges facing gene therapy products, with zero post-approval patients treated due to insufficient clinical community demand and reimbursement barriers, underscoring the significant gap between regulatory approval and real-world market access

- Manufacturing complexity associated with viral vector production, including the requirement for specialized GMP facilities, stringent quality control protocols, and limited global manufacturing capacity, continues to constrain the scalability of gene regulation therapy commercialization and contributes to premium pricing that limits patient accessibility

- Companies such as Massachusetts General Hospital are investing USD 50 million in dedicated cell-processing plants to address domestic manufacturing gaps, while MaxCyte's electroporation platform supporting over 50 active clinical trials represents the industry's response to expanding non-viral manufacturing scalability

- Overcoming these challenges through the development of outcome-based reimbursement models, platform manufacturing innovations, and regulatory harmonization across major markets will be critical for ensuring the sustained and equitable expansion of gene regulation therapy access globally

Gene Regulation Therapy Market Scope

The market is segmented on the basis of therapy type, vector type, disease indication, delivery method, and end-user.

By Therapy Type

On the basis of therapy type, the gene regulation therapy market is segmented into Gene Silencing, Gene Augmentation, Gene Editing, Oncolytic Immunotherapy, and Others. The gene silencing segment dominated the largest market revenue share of 20% in 2025, driven by the broad therapeutic applicability of RNA interference (RNAi), antisense oligonucleotides (ASO), and CRISPR-based transcriptional repression approaches across oncological, neurological, and rare disease indications. Gene silencing therapies targeting disease-causing gene overexpression represent a well-validated and expanding therapeutic modality, with approved products such as Alnylam's patisiran and givosiran demonstrating transformative clinical outcomes in hereditary transthyretin amyloidosis and acute hepatic porphyria respectively. The segment benefits from a large and growing pipeline of gene silencing candidates in late-stage clinical development targeting conditions ranging from hypercholesterolemia to amyotrophic lateral sclerosis, underscoring the broad disease applicability of silencing-based gene regulation approaches. In addition, Sanofi's fitusiran, an siRNA-based antithrombin-lowering therapy, received FDA approval in March 2025 for routine prophylaxis in hemophilia A and B, representing a landmark validation of RNA-based gene regulation in the coagulation disorders space. Moreover, the high degree of target specificity and well-characterized delivery mechanisms of siRNA and ASO platforms continue to attract significant R&D investment from major biopharmaceutical companies globally.

The gene editing segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapid clinical advancement of CRISPR-Cas9 and base editing approaches toward regulatory approval across multiple disease indications. The FDA approval of the first CRISPR-based therapy Casgevy for sickle cell disease in late 2023 established a landmark precedent for in vivo gene editing, with a substantial pipeline of editing candidates now in pivotal trials for hemoglobinopathies, inherited blindness, and neurodegenerative disorders. In addition, the fastest growing CAGR reflects the transformational potential of one-time curative gene editing interventions that are increasingly attracting regulatory fast-track and breakthrough designations, accelerating clinical timelines.

By Vector Type

On the basis of vector type, the gene regulation therapy market is segmented into Viral Vectors and Non-Viral Vectors. The viral vectors segment held the largest market revenue share of 74.83% in 2025, driven by the superior delivery efficiency, established safety profiles, and broad tissue tropism of adeno-associated virus (AAV) and lentiviral platforms across multiple therapeutic indications. AAV vectors have demonstrated robust in vivo transduction efficiency in liver, muscle, retina, and central nervous system targets, supporting their dominant adoption across gene augmentation and silencing applications. The Zolgensma segment alone, utilizing AAV9 for spinal muscular atrophy treatment, achieved an estimated USD 1.24 billion in revenue in 2025, exemplifying the commercial significance of viral vector-based gene regulation therapies. In addition, engineered AAV-PHP.B capsids entering first-in-human studies for Parkinson's disease highlight the ongoing innovation within next-generation viral vector platforms that is sustaining dominant segment share. Moreover, the broad and growing body of long-term clinical evidence supporting viral vector safety and durability provides substantial physician and payer confidence in viral-based gene regulation approaches.

The non-viral vectors segment is expected to witness the fastest CAGR of 23.41% from 2026 to 2033, driven by the rapid advancement of lipid nanoparticle (LNP) delivery platforms validated through mRNA vaccine programs and their increasing application to gene regulation therapeutics. Optimized LNP formulations delivering 40% to 60% editing rates in preclinical models, as demonstrated in Moderna and BioNTech programs, alongside Touchlight's enzymatic DNA platform offering contaminant-free vector alternatives, are positioning non-viral delivery as an increasingly viable and scalable approach for gene regulation. In addition, a CAGR of 23.41% reflects the strong innovation momentum and regulatory confidence building around non-viral gene delivery technologies.

By Disease Indication

On the basis of disease indication, the gene regulation therapy market is segmented into Oncological Disorders, Rare Diseases, Cardiovascular Diseases, Neurological Disorders, Infectious Diseases, and Others. The oncological disorders segment accounted for the largest market revenue share of 44.1% in 2025, driven by the increasing incidence of hematological and solid tumors, the demonstrated clinical success of CAR-T therapies such as Yescarta and Kymriah in relapsed and refractory blood cancers, and the strong and growing pipeline of oncolytic gene therapies and tumor suppressor gene augmentation strategies. Oncology gene regulation therapies benefit from favorable regulatory pathways including accelerated approvals, breakthrough therapy designation, and priority review vouchers, supporting rapid commercialization of innovative products. The segment further benefits from high R&D investment from both biopharmaceutical majors and specialized biotechs, ongoing clinical trials exploring gene regulation approaches in solid tumors, and expanding real-world evidence supporting the durability of CAR-T responses. In addition, rising adoption of personalized neoantigen-based gene regulatory approaches in oncology is creating new treatment paradigms that are expected to sustain dominant segment share through the forecast period.

The neurological disorders segment is expected to witness the fastest CAGR of 25.1% from 2026 to 2033, driven by the growing clinical pipeline for spinal muscular atrophy, Huntington's disease, Parkinson's disease, and other neurodegenerative conditions where gene regulation offers transformative therapeutic potential. Advances in intrathecal and intraocular AAV delivery that bypass the blood-brain barrier are enabling effective CNS gene regulation, while uniQure's demonstration of 79% huntingtin-protein knockdown and Neurocrine's GBA1 Parkinson's program represent pivotal clinical milestones validating neurological gene regulation approaches. In addition, a CAGR of 25.1% reflects the expanding clinical evidence base, accelerating regulatory approvals, and growing payer recognition of the substantial quality-of-life improvements delivered by neurological gene regulation therapies.

By Delivery Method

On the basis of delivery method, the gene regulation therapy market is segmented into In Vivo and Ex Vivo. The in vivo segment held the largest market revenue share of 23% in 2025, driven by the clinical simplicity of direct vector administration into the patient, elimination of complex cell manufacturing steps, and broad applicability across liver, muscle, CNS, and retinal targeting indications. In vivo gene regulation therapies benefit from streamlined manufacturing requirements compared to ex vivo cell therapy approaches and growing clinical evidence supporting durable therapeutic gene expression following single-dose administration. In addition, a growing pipeline of in vivo gene editing and silencing candidates in late-stage development across oncology, rare diseases, and neurology is sustaining dominant delivery method share.

The ex vivo segment is expected to witness the fastest CAGR during the forecast period, driven by the clinical success of ex vivo CAR-T and hematopoietic stem cell gene therapy products and the expanding pipeline of next-generation ex vivo platforms incorporating automated cell manufacturing and CRISPR-based editing of patient-derived cells. The high clinical response rates achieved with ex vivo gene-modified cell therapies in oncological and rare hematological indications are attracting substantial investment in dedicated GMP-grade cell processing facilities globally. In addition, ongoing innovations in ex vivo cell expansion, gene editing efficiency, and product cryopreservation are reducing manufacturing costs and improving scalability.

By End-User

On the basis of end-user, the gene regulation therapy market is segmented into Hospitals and Specialty Clinics, Academic and Research Institutes, and Others. The hospitals and specialty clinics segment captured the largest market revenue share of 53.66% in 2025, functioning as central commercial administration hubs equipped with GMP apheresis suites, specialized pharmacies for advanced therapy medicinal products, and multidisciplinary oncology and rare disease teams capable of managing complex gene therapy administration protocols. Hospitals act as the primary point of care for Phase III clinical trials and post-approval commercial gene therapy delivery, supported by comprehensive patient safety monitoring infrastructure. In addition, the growing establishment of Centers of Excellence for gene therapy administration at major academic medical centers is reinforcing hospital segment dominance across North America and Europe.

The academic and research institutes segment is expected to witness the fastest CAGR of 26.64% from 2026 to 2033, fueled by the fact that approximately 60% of active gene therapy trials originate from investigator-initiated protocols at academic institutions, highlighting their central role in advancing next-generation gene regulation approaches from bench to clinical proof-of-concept. In addition, a CAGR of 26.64% reflects the growing investment in academic gene therapy research programs, supported by NIH grants, EU Horizon funding, and industry-academic partnerships that are accelerating the translational pipeline.

Gene Regulation Therapy Market Regional Analysis

- North America dominated the gene regulation therapy market with the largest revenue share of 41.36% in 2025, driven by 45 new RMAT designations supporting accelerated development, the CMS Access Model easing Medicaid coverage barriers for approved gene therapies, and the presence of leading global gene therapy companies including Novartis, Bristol-Myers Squibb, Gilead Sciences, and Alnylam Pharmaceuticals

- Consumers and healthcare providers in the region benefit from the most advanced regulatory infrastructure for gene therapy globally, with FDA CBER processing over 2,500 active CGT INDs and eight novel CGT approvals awarded in 2024 alone, establishing North America as the leading commercial gene therapy market

- This widespread adoption is further supported by high levels of public and private R&D investment, a robust clinical trial infrastructure, and increasing payer recognition of the long-term value of one-time curative gene regulation therapies, establishing North America as the dominant and most rapidly commercializing gene therapy market globally

U.S. Gene Regulation Therapy Market Insight

The U.S. gene regulation therapy market captured the largest revenue share within North America in 2025, with the market valued at an estimated USD 4.34 billion and fueled by the rapid expansion of approved gene therapy products, a growing pipeline of late-stage candidates, and the establishment of outcome-based reimbursement models facilitating payer access to high-cost gene regulation therapies. The growing preference for one-time curative treatments, combined with robust FDA engagement through programs such as RMAT designation and the START program for rare disease gene therapies, is propelling commercial adoption across oncological, neurological, and rare disease indications.

Europe Gene Regulation Therapy Market Insight

The Europe gene regulation therapy market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the European Medicines Agency's growing approval pipeline for advanced therapy medicinal products (ATMPs), increasing harmonization of gene therapy clinical trial regulations across EU member states, and the establishment of European Reference Networks facilitating cross-border rare disease patient pooling for gene therapy clinical trials. European countries including Germany, France, and the United Kingdom are witnessing significant investment in gene therapy manufacturing infrastructure and dedicated ATMP clinical administration centers. In addition, Europe is expected to grow at a CAGR of approximately 20.93%, reflecting the region's strong clinical research base and growing commercial gene therapy ecosystem.

U.K. Gene Regulation Therapy Market Insight

The U.K. gene regulation therapy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the MHRA's progressive regulatory framework for advanced gene therapies, robust NHS investment in precision medicine programs, and the presence of leading gene therapy companies and academic research centers including University College London and the Wellcome Sanger Institute. In September 2022, a new consortium was established by UCL to ensure access to gene therapies for children with rare diseases, demonstrating the U.K.'s commitment to expanding equitable access to advanced gene regulation therapies.

Germany Gene Regulation Therapy Market Insight

The Germany gene regulation therapy market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing investment in gene therapy clinical research, strong pharmaceutical R&D infrastructure, and the growing adoption of precision medicine approaches within the German healthcare system. Germany's well-developed GMP manufacturing ecosystem and emphasis on clinical rigor in ATMP development are supporting the commercialization of advanced gene regulation therapies, particularly within academic medical centers in Munich, Berlin, and Frankfurt.

Asia-Pacific Gene Regulation Therapy Market Insight

The Asia-Pacific gene regulation therapy market is poised to grow at the fastest CAGR during the forecast period, driven by rapidly expanding clinical trial activity in China, Japan, South Korea, and India, increasing healthcare expenditure supporting access to advanced therapeutics, and a large underserved patient population with high burden of genetic and oncological diseases. Government initiatives such as China's National Gene Bank and Japan's national precision medicine program are creating enabling environments for gene regulation therapy development and adoption. In addition, the Asia-Pacific market is expected to grow at a CAGR exceeding 24%, reflecting the substantial investments in gene therapy manufacturing infrastructure and clinical research capacity building across the region.

Japan Gene Regulation Therapy Market Insight

The Japan gene regulation therapy market is gaining momentum due to the country's advanced regulatory framework under the Act on the Safety of Regenerative Medicine, a strong academic research culture in genetic medicine, and growing government investment in translational gene therapy research programs. Japan's National Institute of Biomedical Innovation supports a growing pipeline of domestically developed gene regulation candidates, while partnerships between Japanese universities and global gene therapy developers are accelerating clinical trial activities.

China Gene Regulation Therapy Market Insight

The China gene regulation therapy market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's large patient population with high oncological disease burden, the largest number of CAR-T clinical trials globally, and strong government support for gene therapy research through the National Key Research and Development Program. China's domestic gene therapy companies, including Shanghai Sunway Biotech, are commercializing locally developed gene regulation products while international partnerships with global biopharmaceutical leaders are expanding access to next-generation gene therapy platforms in the Chinese market.

Gene Regulation Therapy Market Share

The Gene Regulation Therapy industry is primarily led by well-established companies, including:

- Novartis AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- GSK plc (U.K.)

- Biogen Inc. (U.S.)

- Gilead Sciences Inc. (U.S.)

- Alnylam Pharmaceuticals (U.S.)

- Sarepta Therapeutics (U.S.)

- BioMarin Pharmaceuticals Inc. (U.S.)

- Orchard Therapeutics (U.K.)

- uniQure N.V. (Netherlands)

- Spark Therapeutics (U.S.)

- bluebird bio (U.S.)

- Sangamo Therapeutics (U.S.)

- Editas Medicine (U.S.)

- CRISPR Therapeutics (Switzerland)

- Intellia Therapeutics (U.S.)

- GenSight Biologics (France)

- Applied Genetic Technologies Corporation (U.S.)

- Dimension Therapeutics Inc. (U.S.)

- Shanghai Sunway Biotech Co. Ltd. (China)

Latest Developments in Global Gene Regulation Therapy Market

- In September 2022, a new consortium was established by University College London (UCL) to ensure access to gene therapies for children with rare diseases, marking a significant collaborative initiative to bridge the gap between gene regulation therapy innovation and equitable patient access in pediatric rare disease populations across Europe

- In January 2024, the FDA published two landmark final guidance documents on human gene therapy products incorporating human genome editing and CAR T-cell product development, providing critical regulatory clarity for sponsors advancing CRISPR-based and other advanced gene regulation therapies and expected to accelerate the commercial development of next-generation gene regulation platforms

- In February 2024, CBER selected four investigational CGTs for its Support for Clinical Trials Advancing Rare Disease Therapeutics (START) program, providing enhanced FDA communication and development support to promising gene regulation therapy candidates targeting rare pediatric diseases and demonstrating the regulatory agency's commitment to accelerating rare disease gene therapy timelines

- In March 2025, Sanofi's fitusiran (Qfitlia), an siRNA-based antithrombin-lowering gene regulation therapy, received FDA approval for routine prophylaxis in hemophilia A and B regardless of inhibitor status. The ATLAS program demonstrated that this RNA-based gene regulation approach reduced annualized bleeding rates by over 70%, representing a significant commercial milestone for RNA-based gene regulation therapies in the coagulation disorders market

- In May 2025, CureDuchenne invested USD 1.0 million in Entos Pharmaceuticals to support the development of a new gene therapy for Duchenne muscular dystrophy, aimed at overcoming the delivery and payload size limitations of existing gene regulation approaches. This initiative underscored the growing investment in next-generation gene therapy platforms targeting muscle disorders through innovative vector design

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.