Global Gene Therapy Vector Production Systems Market

Market Size in USD Billion

USD

2.86 Billion

USD

10.88 Billion

2025

2033

USD

2.86 Billion

USD

10.88 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.86 Billion | |

| USD 10.88 Billion | |

| % | |

|

Gene Therapy Vector Production Systems Market Overview

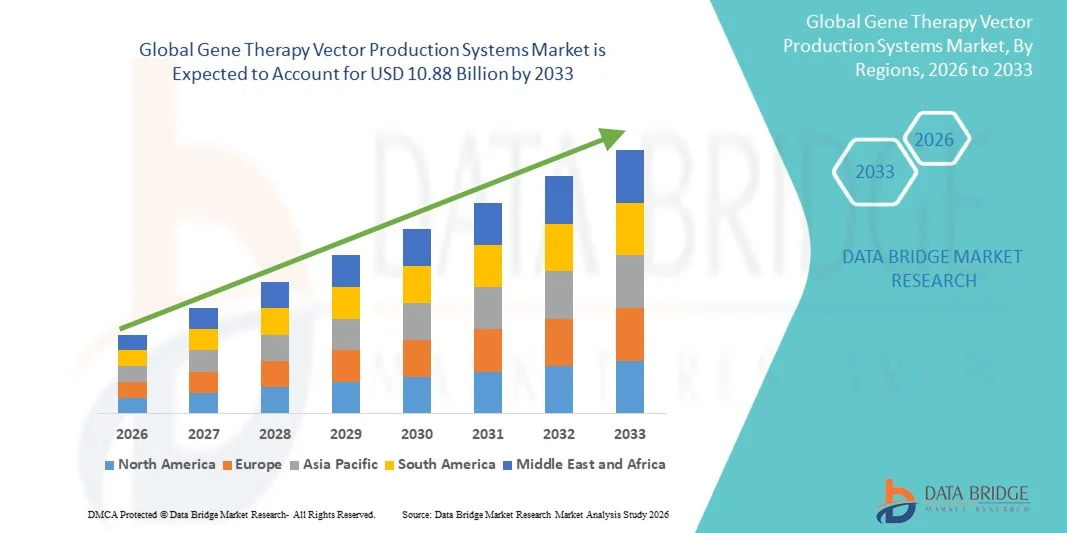

The Gene Therapy Vector Production Systems Market was valued at USD 2.86 Billion in 2025 and is projected to reach USD 10.88 Billion by 2033, growing at a CAGR of 18.20% from 2026 to 2033. The market is witnessing robust growth driven by the increasing commercialization of gene therapies, expanding clinical pipelines, rising investments in advanced biomanufacturing infrastructure, and growing demand for high-quality viral vector production technologies.

The rapid increase in regulatory approvals for gene and cell therapies, coupled with advancements in scalable vector manufacturing platforms and automation technologies, is encouraging biopharmaceutical companies and CDMOs to expand production capacities. Growing demand for high-yield, GMP-compliant manufacturing systems and innovations in upstream and downstream processing continue to accelerate market expansion worldwide.

Key Market Trends & Insights

- North America dominated the Gene Therapy Vector Production Systems Market with the largest revenue share of 39.12% in 2025, supported by strong biotechnology investments, advanced manufacturing infrastructure, and a large number of ongoing gene therapy clinical programs.

- The Viral Vector Production Systems segment led the market with a 68.45% share in 2025, driven by widespread adoption of AAV and lentiviral vectors for approved and pipeline gene therapies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 18.5% from 2026 to 2033, fueled by expanding biopharmaceutical manufacturing capabilities, increasing government funding, and growing clinical research activities across China, Japan, South Korea, and India.

- Stable Producer Cell Line Systems are the fastest-growing technology segment, projected to register a CAGR of 18.3%, reflecting increasing demand for scalable, reproducible, and cost-efficient commercial manufacturing.

- The Biopharmaceutical Companies segment dominates the end-user category with a 43.76% revenue share in 2025, supported by rising investments in in-house vector manufacturing and commercial-scale production facilities.

- Commercial Scale Production accounts for 46.81% of the market, driven by increasing approvals of gene therapies and the transition of multiple pipeline products toward commercialization.

- The Automation Solutions & Manufacturing Software segment is the fastest-growing component category, with a CAGR of 18.1%, driven by increasing adoption of digital bioprocessing, AI-enabled quality monitoring, and automated manufacturing workflows.

Market Size & Forecast

- Global Market Value (2025): USD 2.86 Billion

- Expected Market Value (2033): USD 10.88 Billion

- Forecast CAGR (2026–2033): 18.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Gene Therapy Vector Production Systems Market Segmentation

|

Attributes |

Gene Therapy Vector Production Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Thermo Fisher Scientific Inc. (U.S.) · Danaher Corporation (U.S.) · Merck KGaA (Germany) · Sartorius AG (Germany) · Cytiva (U.S.) · Lonza Group AG (Switzerland) · FUJIFILM Holdings Corporation (Japan) · Charles River Laboratories International, Inc. (U.S.) · Catalent, Inc. (U.S.) · Oxford Biomedica plc (U.K.) · REGENXBIO Inc. (U.S.) · Andelyn Biosciences, Inc. (U.S.) · Forge Biologics, Inc. (U.S.) · Genezen Laboratories, Inc. (U.S.) · WuXi Advanced Therapies (U.S.) · SK pharmteco (South Korea) · Yposkesi (France) · Miltenyi Biotec B.V. & Co. KG (Germany) · Bio-Techne Corporation (U.S.) · Eppendorf SE (Germany) · Asahi Kasei Corporation (Japan) · Takara Bio Inc. (Japan) · VectorBuilder Inc. (U.S.) · Cell and Gene Therapy Catapult (U.K.) · Batavia Biosciences B.V. (Netherlands) · Viralgen Vector Core S.L. (Spain) · Samsung Biologics Co., Ltd. (South Korea) · AGC Biologics (U.S.) · BioCentriq (U.S.) · Novartis AG (Switzerland) · ElevateBio, LLC (U.S.) · RoslinCT (U.K.) · KBI Biopharma Inc. (U.S.) · Resilience (National Resilience, Inc.) (U.S.) |

|

Market Opportunities |

· Expansion of commercial-scale manufacturing capacity for gene therapies · Increasing adoption of automated and closed-system vector production platforms · Rising outsourcing of vector manufacturing to specialized CDMOs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework |

Gene Therapy Vector Production Systems Market Trends

Trend: Growing Adoption of Automated and Closed-System Manufacturing

Gene therapy manufacturers are increasingly adopting automated and closed-system production platforms to improve manufacturing efficiency, minimize contamination risks, and ensure batch-to-batch consistency. The integration of single-use bioreactors, automated cell culture systems, digital bioprocess monitoring, and AI-enabled manufacturing analytics is streamlining upstream and downstream workflows while reducing production costs. Continuous manufacturing technologies and real-time quality monitoring are further enhancing scalability, enabling manufacturers to meet the rapidly growing demand for commercial gene therapies while complying with stringent GMP requirements.

Gene Therapy Vector Production Systems Market Dynamics

Key Market Driver: Rising Commercialization of Gene Therapies and Expanding Clinical Pipeline

The growing number of approved gene therapies and late-stage clinical programs has significantly increased demand for scalable vector production systems. Biopharmaceutical companies are expanding manufacturing capacity to support commercial launches while improving production yields and regulatory compliance. Continuous investments in viral vector manufacturing technologies, coupled with increasing funding for rare disease and oncology gene therapy research, are accelerating adoption of advanced production platforms across both in-house facilities and contract manufacturing organizations.

Key Restraint/Challenge: High Capital Investment and Complex Manufacturing Processes

A major restraint in the Gene Therapy Vector Production Systems Market is the substantial investment required to establish GMP-compliant manufacturing facilities. Advanced production systems require specialized cleanroom infrastructure, high-performance bioreactors, purification technologies, analytical testing equipment, and highly skilled personnel. In addition, complex manufacturing workflows, stringent regulatory requirements, and challenges associated with scaling viral vector production continue to increase operational costs and limit market entry for smaller biotechnology companies.

The expansion of several commercial viral vector manufacturing facilities across North America and Europe during 2025, featuring large-scale automated production lines and advanced quality control laboratories, highlights the significant financial commitment required for state-of-the-art gene therapy manufacturing infrastructure, underscoring the ongoing challenge for emerging manufacturers.

Key Market Opportunity: Expansion of CDMO Services and Next-Generation Vector Manufacturing Technologies

The rapid growth of contract development and manufacturing organizations (CDMOs) presents a significant opportunity for the market. Increasing outsourcing of viral vector manufacturing enables biotechnology companies to accelerate clinical development while avoiding substantial capital investments in production facilities. Furthermore, advances in suspension cell culture, stable producer cell lines, continuous bioprocessing, AI-driven process optimization, and modular manufacturing platforms are improving production efficiency, reducing costs, and expanding global manufacturing capacity. These innovations are expected to create substantial growth opportunities across North America, Europe, and rapidly developing biotechnology markets in Asia-Pacific.

Gene Therapy Vector Production Systems Market Scope

The gene therapy vector production systems market is segmented on the basis of vector type, viral vector type, production system, workflow, application, end user, technology, scale of production, deployment, and component.

- By Vector Type

On the basis of vector type, the Gene Therapy Vector Production Systems Market is segmented into viral vector production systems and non-viral vector production systems. The viral vector production systems segment dominated the market with a 68.45% share in 2025, owing to their widespread use in commercial gene therapy manufacturing, high transduction efficiency, and strong regulatory acceptance for approved therapies. Viral vectors, particularly AAV and lentiviral systems, have become the preferred platform for delivering therapeutic genes across oncology, rare diseases, and inherited genetic disorders. Increasing investments in commercial manufacturing facilities and expanding clinical pipelines continue to reinforce the leadership of this segment.

The non-viral vector production systems segment is projected to register the fastest growth at a CAGR of 18.1% from 2026 to 2033, driven by growing research into safer and cost-effective gene delivery technologies. Advances in lipid nanoparticles, polymer-based delivery systems, and electroporation technologies are supporting broader adoption of non-viral manufacturing platforms, particularly for genome editing applications and next-generation nucleic acid therapies.

- By Viral Vector Type

On the basis of viral vector type, the Gene Therapy Vector Production Systems Market is segmented into Adeno-Associated Viral (AAV) Vector Systems, Lentiviral Vector Systems, Adenoviral Vector Systems, Retroviral Vector Systems, Baculoviral Vector Systems, and Others. The Adeno-Associated Viral (AAV) Vector Systems segment led the market with a 39.84% share in 2025, supported by its extensive use in approved gene therapies, favorable safety profile, and long-term gene expression capabilities. Pharmaceutical companies continue expanding AAV manufacturing capacity to meet increasing commercial demand for therapies targeting neurological, ophthalmic, and rare genetic diseases.

The Lentiviral Vector Systems segment is expected to experience the fastest growth at a CAGR of 18.4% from 2026 to 2033, driven by increasing utilization in CAR-T cell therapies, stem cell engineering, and ex vivo gene-modified cell therapies. Continuous improvements in vector yield, manufacturing scalability, and biosafety technologies are further accelerating adoption.

- By Production System

On the basis of production system, the Gene Therapy Vector Production Systems Market is segmented into mammalian cell-based systems, insect cell-based systems, suspension cell culture systems, adherent cell culture systems, and cell-free production systems. The mammalian cell-based systems segment dominated the market with a 44.28% share in 2025 due to their ability to produce high-quality viral vectors with appropriate post-translational modifications required for clinical applications. These systems remain the industry standard for manufacturing GMP-compliant viral vectors used in commercial gene therapy production.

The suspension cell culture systems segment is anticipated to witness the fastest CAGR of 18.3% from 2026 to 2033, driven by increasing adoption of scalable bioreactor technologies that enable higher production volumes, improved process consistency, and reduced manufacturing costs. Growing investments in large-scale commercial manufacturing facilities continue to support segment expansion.

- By Workflow

On the basis of workflow, the Gene Therapy Vector Production Systems Market is segmented into upstream processing, downstream processing, fill-finish & packaging, and quality control & analytical testing. The upstream processing segment dominated the market with a share of 36.92% in 2025 due to increasing investments in cell culture optimization, transient transfection technologies, and high-density bioreactor systems that maximize vector yield and manufacturing efficiency. The growing number of commercial manufacturing facilities worldwide continues to strengthen demand for advanced upstream production solutions.

The quality control & analytical testing segment is anticipated to witness the fastest CAGR of 18.4% from 2026 to 2033, driven by increasingly stringent global regulatory requirements for vector characterization, potency testing, sterility assurance, and product consistency. The adoption of automated analytical technologies and digital quality management platforms is further supporting segment growth.

- By Application

On the basis of application, the Gene Therapy Vector Production Systems Market is segmented into gene therapy development, cell therapy manufacturing, vaccine development, research applications, clinical trials, and commercial manufacturing. The gene therapy development segment dominated the market with a share of 31.47% in 2025 due to the rapidly expanding pipeline of gene therapies targeting rare diseases, oncology, cardiovascular disorders, and neurological conditions. Increasing investments by biotechnology companies and pharmaceutical manufacturers in clinical development programs continue to drive demand for advanced vector production systems.

The commercial manufacturing segment is expected to witness the fastest CAGR of 118.2% from 2026 to 2033, driven by the growing number of regulatory approvals for gene therapies and expanding commercialization activities worldwide. Large-scale manufacturing capacity expansion, automation technologies, and process optimization are enabling manufacturers to meet increasing global demand while maintaining product quality and regulatory compliance.

- By End User

On the basis of end user, the Gene Therapy Vector Production Systems Market is segmented into biopharmaceutical companies, contract development & manufacturing organizations (CDMOs), academic & research institutes, biotechnology companies, and hospitals & clinical research organizations. The biopharmaceutical companies segment dominated the market with a 43.76% share in 2025 due to increasing investments in commercial gene therapy manufacturing, expanding in-house production capabilities, and the growing number of approved gene therapy products. Major pharmaceutical companies are establishing dedicated vector production facilities to strengthen supply chain resilience, improve manufacturing efficiency, and accelerate product commercialization. Rising investment in advanced bioprocess technologies and automation is further reinforcing the segment's leading market position.

The contract development & manufacturing organizations (CDMOs) segment is expected to witness the fastest CAGR of 18.1% from 2026 to 2033, driven by increasing outsourcing of viral vector manufacturing by biotechnology companies seeking to reduce capital expenditure and accelerate clinical development timelines. Growing demand for GMP-compliant manufacturing, specialized production expertise, and flexible manufacturing capacity is significantly boosting the adoption of CDMO services worldwide.

- By Technology

On the basis of technology, the Gene Therapy Vector Production Systems Market is segmented into transient transfection systems, stable producer cell line systems, plasmid production systems, and automated manufacturing platforms. The transient transfection systems segment dominated the market with a 38.64% share in 2025 due to their widespread application in clinical-stage vector production, operational flexibility, and relatively short development timelines. These systems are extensively used for manufacturing AAV and lentiviral vectors across research, clinical, and early commercial production.

The automated manufacturing platforms segment is expected to witness the fastest CAGR of 18.3% from 2026 to 2033, driven by increasing adoption of digital manufacturing technologies, robotic process automation, and AI-enabled bioprocess monitoring. Automated production systems improve manufacturing consistency, reduce contamination risks, minimize labor requirements, and enable continuous production, making them increasingly attractive for commercial-scale manufacturing.

- By Scale of Production

On the basis of scale of production, the Gene Therapy Vector Production Systems Market is segmented into preclinical scale, clinical scale, and commercial scale. The commercial scale segment dominated the market with a 46.81% share in 2025 due to the growing commercialization of gene therapies, increasing regulatory approvals, and expanding global manufacturing infrastructure. Pharmaceutical manufacturers continue investing in high-capacity production facilities equipped with advanced bioreactors, purification systems, and automated quality control technologies to support large-volume production.

The clinical scale segment is expected to register the fastest CAGR of 18.2% from 2026 to 2033, driven by the rapidly expanding number of Phase I, II, and III gene therapy clinical trials worldwide. Rising demand for flexible manufacturing platforms capable of supporting multiple clinical programs is contributing significantly to market growth.

- By Deployment

On the basis of deployment, the Gene Therapy Vector Production Systems Market is segmented into in-house manufacturing and outsourced manufacturing. The in-house manufacturing segment dominated the market with a 58.37% share in 2025 due to increasing investments by leading pharmaceutical and biotechnology companies in dedicated GMP manufacturing facilities. In-house production provides greater process control, intellectual property protection, supply chain security, and regulatory compliance while enabling manufacturers to optimize production efficiency and reduce long-term manufacturing costs.

The outsourced manufacturing segment is expected to witness the fastest CAGR of 18.5% from 2026 to 2033, driven by growing dependence on specialized CDMOs offering scalable manufacturing capabilities, regulatory expertise, and reduced time-to-market. Small and mid-sized biotechnology companies are increasingly outsourcing vector production to avoid high capital investment and operational complexity.

- By Component

On the basis of component, the Gene Therapy Vector Production Systems Market is segmented into bioreactors, filtration systems, chromatography systems, cell culture media & reagents, analytical instruments, and software & automation solutions. The cell culture media & reagents segment dominated the market with a 27.54% share in 2025 due to continuous consumption throughout upstream manufacturing processes and increasing demand for high-performance media formulations that improve cell growth and vector productivity. The growing number of commercial manufacturing facilities and expanding clinical research activities continue to drive demand for high-quality reagents and consumables.

The software & automation solutions segment is anticipated to witness the fastest CAGR of 9.1% from 2026 to 2033, driven by increasing adoption of digital manufacturing platforms, AI-enabled process optimization, electronic batch records, predictive maintenance, and real-time production monitoring. These technologies enhance manufacturing efficiency, improve regulatory compliance, and support the transition toward Industry 4.0-enabled biopharmaceutical manufacturing.

Gene Therapy Vector Production Systems Market Regional Analysis

North America dominated the gene therapy vector production systems market and accounted for the largest revenue share of 39.12% in 2025, supported by a strong biotechnology ecosystem, increasing regulatory approvals for gene therapies, and substantial investments in advanced biomanufacturing infrastructure. The region benefits from the presence of leading pharmaceutical companies, contract development and manufacturing organizations (CDMOs), and research institutions actively engaged in gene and cell therapy development. Continuous expansion of GMP manufacturing facilities, favorable government funding, and rapid adoption of automation technologies further strengthen North America's leadership in the global market.

U.S. Gene Therapy Vector Production Systems Market Insight

The U.S. gene therapy vector production systems market is witnessing significant growth due to rising investments in gene and cell therapy research, expanding commercial manufacturing capacity, and increasing regulatory approvals for innovative therapies. The country's well-established biotechnology sector, combined with strong venture capital funding and strategic collaborations between pharmaceutical companies and CDMOs, continues to drive demand for advanced vector manufacturing systems. Furthermore, increasing adoption of automated bioprocessing technologies, single-use manufacturing platforms, and AI-enabled quality monitoring is enhancing manufacturing efficiency while supporting rapid commercialization of gene therapies.

Europe Gene Therapy Vector Production Systems Market Insight

The Europe gene therapy vector production systems market represents a substantial share of global revenue, driven by increasing investments in advanced biopharmaceutical manufacturing, supportive regulatory initiatives, and strong academic research capabilities. Growing demand for viral vector manufacturing technologies, expanding clinical trial activity, and increasing collaborations between biotechnology companies and research organizations are accelerating market growth across the region. In addition, continuous investments in GMP production facilities and process innovation are strengthening Europe's position as a leading hub for advanced therapy manufacturing.

U.K. Gene Therapy Vector Production Systems Market Insight

The U.K. gene therapy vector production systems market is experiencing steady expansion, supported by strong government initiatives promoting advanced therapy medicinal products (ATMPs), increasing biotechnology investments, and world-class biomedical research infrastructure. Growing collaboration between academic institutions, biotechnology companies, and contract manufacturers is accelerating the development and commercialization of innovative gene therapies. Moreover, increasing adoption of automated manufacturing systems and advanced analytical technologies is improving production efficiency and regulatory compliance across the country.

Germany Gene Therapy Vector Production Systems Market Insight

The Germany gene therapy vector production systems market is expanding steadily due to the country's advanced pharmaceutical manufacturing capabilities, highly developed biotechnology sector, and increasing investments in precision medicine. German manufacturers and research organizations are adopting next-generation bioprocessing technologies to improve vector production efficiency and product quality. Rising demand for scalable manufacturing platforms, coupled with continuous innovation in cell culture technologies, purification systems, and digital manufacturing solutions, continues to drive market growth across the country.

Asia-Pacific Gene Therapy Vector Production Systems Market Insight

The Asia-Pacific gene therapy vector production systems market is expected to witness the fastest growth, with a projected CAGR of 18.5% from 2026 to 2033, driven by rapidly expanding biotechnology industries, increasing government funding for life sciences, and growing investments in advanced manufacturing infrastructure across China, Japan, South Korea, and India. Rising clinical trial activity, increasing outsourcing of vector manufacturing, and the establishment of new GMP production facilities are significantly contributing to regional market expansion. In addition, favorable government policies supporting biotechnology innovation and growing healthcare expenditure continue to accelerate market development throughout the region.

Japan Gene Therapy Vector Production Systems Market Insight

The Japan gene therapy vector production systems market is witnessing consistent growth due to increasing investments in regenerative medicine, precision healthcare, and advanced biopharmaceutical manufacturing. The country's strong focus on research and innovation, combined with supportive regulatory pathways for regenerative therapies, is encouraging the adoption of advanced viral vector production technologies. Furthermore, collaborations between pharmaceutical companies, research institutes, and manufacturing organizations are enhancing domestic production capabilities while supporting the commercialization of next-generation gene therapies.

China Gene Therapy Vector Production Systems Market Insight

The China gene therapy vector production systems market is growing rapidly, driven by substantial government investments in biotechnology, expanding pharmaceutical manufacturing capabilities, and increasing clinical research activities. The country is witnessing significant growth in local biotechnology companies developing gene and cell therapies, creating strong demand for scalable vector manufacturing systems. In addition, increasing adoption of automated production platforms, expansion of GMP-certified manufacturing facilities, and growing partnerships with global biotechnology firms are positioning China as one of the fastest-growing markets for gene therapy vector production systems worldwide.

Gene Therapy Vector Production Systems Market Share

The Gene Therapy Vector Production Systems industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific Inc. (U.S.)

- Danaher Corporation (U.S.)

- Merck KGaA (Germany)

- Sartorius AG (Germany)

- Cytiva (U.S.)

- Lonza Group AG (Switzerland)

- FUJIFILM Holdings Corporation (Japan)

- Charles River Laboratories International, Inc. (U.S.)

- Catalent, Inc. (U.S.)

- Oxford Biomedica plc (U.K.)

- REGENXBIO Inc. (U.S.)

- Andelyn Biosciences, Inc. (U.S.)

- Forge Biologics, Inc. (U.S.)

- Genezen Laboratories, Inc. (U.S.)

- WuXi Advanced Therapies (U.S.)

- SK pharmteco (South Korea)

- Yposkesi (France)

- Miltenyi Biotec B.V. & Co. KG (Germany)

- Bio-Techne Corporation (U.S.)

- Eppendorf SE (Germany)

- Asahi Kasei Corporation (Japan)

- Takara Bio Inc. (Japan)

- VectorBuilder Inc. (U.S.)

- Cell and Gene Therapy Catapult (U.K.)

- Batavia Biosciences B.V. (Netherlands)

- Viralgen Vector Core S.L. (Spain)

- Samsung Biologics Co., Ltd. (South Korea)

- AGC Biologics (U.S.)

- BioCentriq (U.S.)

- Novartis AG (Switzerland)

- ElevateBio, LLC (U.S.)

- RoslinCT (U.K.)

- KBI Biopharma Inc. (U.S.)

- Resilience (National Resilience, Inc.) (U.S.)

Latest Developments in Gene Therapy Vector Production Systems Market

- In October 2025, Thermo Fisher Scientific Inc. expanded its viral vector manufacturing portfolio by introducing an advanced single-use bioprocessing platform designed for commercial-scale AAV and lentiviral vector production. The platform integrates automated upstream and downstream processing technologies, enabling higher production yields, improved process consistency, and reduced contamination risks. This development strengthens Thermo Fisher Scientific's position in the gene therapy manufacturing market by supporting scalable, GMP-compliant production for clinical and commercial applications.

- In September 2025, Sartorius AG launched a next-generation automated bioreactor platform specifically optimized for viral vector manufacturing. The new system features integrated process analytics, real-time monitoring, and digital bioprocess control to improve manufacturing efficiency and product quality. The launch enhances Sartorius' portfolio of advanced manufacturing technologies while helping biopharmaceutical companies accelerate gene therapy development and commercialization.

- In July 2025, Cytiva introduced an integrated downstream purification workflow for viral vector production, combining high-performance chromatography systems with automated filtration technologies. The solution improves vector recovery, shortens purification timelines, and enhances overall manufacturing productivity. This innovation strengthens Cytiva's capabilities in supporting large-scale commercial gene therapy manufacturing while improving operational efficiency.

- In April 2025, Lonza Group AG expanded its global viral vector manufacturing network by increasing GMP production capacity for AAV and lentiviral vectors at its advanced biomanufacturing facilities. The expansion supports growing customer demand for commercial-scale vector manufacturing and provides additional capacity for clinical-stage and commercial gene therapy programs worldwide.

- In November 2024, Merck KGaA introduced new analytical technologies for viral vector characterization and quality control, enabling faster product release testing and improved regulatory compliance. The enhanced analytical platform supports comprehensive vector identity, purity, potency, and safety assessment, helping manufacturers improve production reliability while accelerating commercialization of gene therapies.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.