Global Generic Injectables For Infectious Diseases Market

Market Size in USD Billion

USD

117.40 Billion

USD

239.14 Billion

2024

2032

USD

117.40 Billion

USD

239.14 Billion

2024

2032

| 2025 - 2032 | |

| USD 117.40 Billion | |

| USD 239.14 Billion | |

| % | |

|

Generic Injectables for Infectious Diseases Market Size

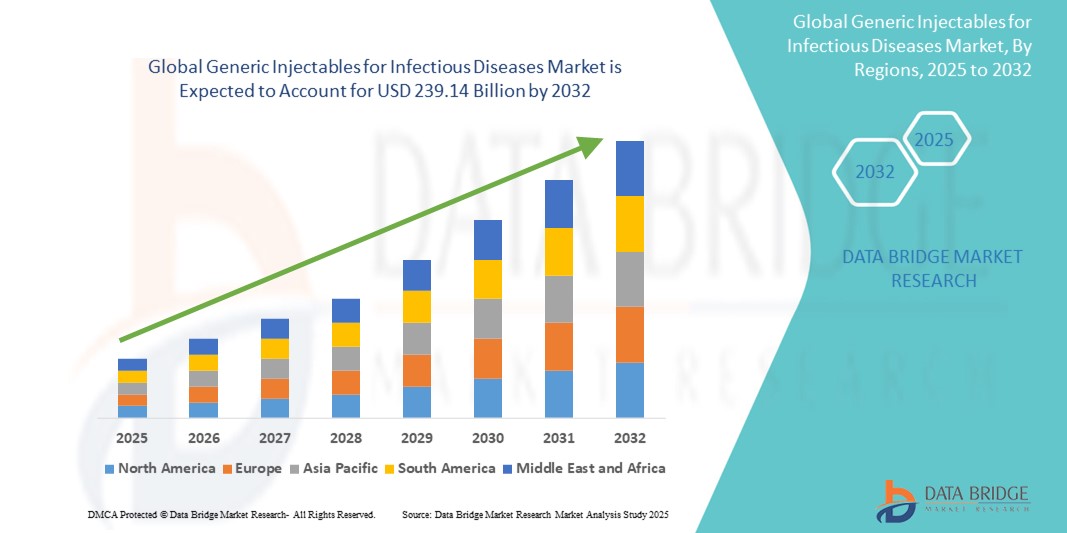

- The global generic injectables for infectious diseases market size was valued at USD 117.40 billion in 2024 and is expected to reach USD 239.14 billion by 2032, at a CAGR of 9.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of infectious diseases, coupled with the rising demand for cost-effective treatment options, leading to greater reliance on generic injectable formulations in both hospital and outpatient settings

- Furthermore, the widespread need for rapid-acting, reliable, and affordable therapies is positioning generic injectables as a critical component of infectious disease management. These combined factors are driving accelerated adoption of generic injectable solutions, thereby significantly propelling market expansion

Generic Injectables for Infectious Diseases Market Analysis

- Generic injectables, offering fast-acting and cost-effective treatments, are increasingly vital components in the global fight against infectious diseases across inpatient and outpatient settings, owing to their broad-spectrum efficacy, affordability, and critical role in antimicrobial and antiviral therapies

- The escalating demand for generic injectables is primarily fueled by the rising global burden of infectious diseases, healthcare cost-containment pressures, and increased adoption of generics by hospitals and public health systems for emergency preparedness and routine treatment

- North America dominated the generic injectables for infectious diseases market with the largest revenue share of 39.5% in 2024, driven by strong regulatory support, high generic penetration, and a mature pharmaceutical supply chain, with the U.S. showing increased reliance on injectable generics for hospital-acquired infections and outpatient parenteral antimicrobial therapy (OPAT)

- Asia-Pacific is expected to be the fastest growing region in the market during the forecast period due to expanding healthcare access, increased production capacity of generics, and a rising prevalence of infectious diseases in densely populated regions

- Small Molecule segment dominated the market with a market share of 42.8% in 2024, driven by their widespread use in treating bacterial infections, cost-efficiency, and critical inclusion in global health procurement programs and hospital formularies

Report Scope and Generic Injectables for Infectious Diseases Market Segmentation

|

Attributes |

Generic Injectables for Infectious Diseases Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Generic Injectables for Infectious Diseases Market Trends

“Increased Demand for Cost-Effective and Rapid-Action Therapies”

- A significant and accelerating trend in the global generic injectables for infectious diseases market is the rising demand for affordable, fast-acting treatments to combat both routine and emergent infectious outbreaks. This trend is driven by healthcare systems prioritizing access, cost control, and preparedness in response to increasing infection rates and global health emergencies

- For instance, Cipla and Aurobindo Pharma have rapidly expanded their portfolios of injectable antibiotics and antivirals, including generic versions of remdesivir and ceftriaxone, to serve hospitals and public health procurement programs worldwide

- The ability of generic injectables to provide immediate therapeutic impact, especially in intravenous form, makes them indispensable in managing hospital-acquired infections, sepsis, and pandemics. Manufacturers are increasingly focusing on ready-to-use formulations and extended shelf-life products to meet the operational needs of healthcare providers in both developed and developing countries

- Furthermore, global regulatory support for faster approval pathways for essential generics, particularly injectables, has strengthened market access. Initiatives such as the WHO’s prequalification program and the U.S. FDA’s Drug Shortage Assistance Program have accelerated the entry of generic injectable treatments in key markets

- This trend toward rapid availability, lower costs, and growing therapeutic equivalence of injectables is shaping procurement decisions among governments, hospitals, and NGOs. As a result, companies like Hikma Pharmaceuticals and Sandoz are focusing on expanding production capacities and establishing regional supply chains to reduce dependency on single-source APIs and improve time-to-market

Generic Injectables for Infectious Diseases Market Dynamics

Driver

“Rising Infectious Disease Burden and Pressure to Lower Healthcare Costs”

- The increasing global burden of infectious diseases including tuberculosis, pneumonia, bloodstream infections, and emerging viral threats is a primary driver for the rising demand for generic injectable therapeutics. Hospitals and healthcare systems are under constant pressure to deliver effective treatment quickly while controlling expenditures

- For instance, in 2024, Viatris Inc. partnered with several global health organizations to supply generic injectable antimicrobials at scale to address antimicrobial resistance (AMR) and pandemic preparedness

- Generic injectables offer rapid symptom relief, high bioavailability, and the flexibility to be used in critical care and emergency settings, making them the preferred therapeutic option for healthcare providers. Moreover, their affordability significantly eases the burden on public healthcare systems, particularly in low- and middle-income countries where out-of-pocket spending remains high

- The expansion of health insurance coverage, inclusion of generics in national essential medicines lists, and public procurement programs are further promoting the uptake of injectable generics in infectious disease treatment

Restraint/Challenge

“Manufacturing Complexities and Regulatory Compliance Barriers”

- Despite strong demand, the manufacturing of generic injectables poses notable challenges due to complex sterile production processes, stringent regulatory standards, and high initial capital investments. These factors can delay product launches and limit the number of market participants

- For instance, periodic facility inspections by the U.S. FDA, EMA, and other regulators have led to temporary plant closures or import alerts for several generic manufacturers, disrupting supply chains and causing shortages in key antibiotics and antivirals

- Moreover, batch failures, contamination risks, and cold chain requirements for certain biologics further increase production costs and logistical burdens. Small- and mid-sized firms often struggle to meet the rigorous Good Manufacturing Practice (GMP) requirements for sterile injectable drugs

- Additionally, price erosion due to intense market competition and government price caps can limit profit margins and discourage new entrants. Addressing these challenges through technological upgrades, strategic collaborations, and localized manufacturing will be essential to ensure consistent supply and sustained market growth

Generic Injectables for Infectious Diseases Market Scope

The market is segmented on the basis of product type, molecule type, application, route of administration, and distribution channel.

- By Product Type

On the basis of product type, the generic injectables for infectious diseases market is segmented into monoclonal antibodies, immunoglobulin, cytokines, insulin, peptide hormones, blood factors, vaccines, small molecule antibiotics, chemotherapy agents, and others. The small molecule antibiotics segment dominated the market with the largest market revenue share of 42.8% in 2024, attributed to its broad-spectrum use in treating bacterial infections and its widespread availability in cost-effective injectable forms. These drugs are essential in both emergency and routine care settings, especially in low- and middle-income regions, and are frequently included in hospital formularies and national essential medicines lists.

The monoclonal antibodies segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by rising demand for biosimilar therapies, increasing approvals of generic biologics, and their growing role in treating viral infections such as COVID-19 and RSV. With increasing cost pressures and patent expirations, biosimilar monoclonal antibodies are becoming more accessible in developing markets.

- By Molecule Type

On the basis of molecule type, the generic injectables for infectious diseases market is segmented into large molecule and small molecule. The small molecule segment held the largest revenue share of 58.7% in 2024, due to their simpler structure, lower production costs, and more established regulatory pathways. These drugs offer rapid therapeutic action and are often the first-line treatment for common infectious diseases.

The large molecule segment is expected to grow at a notable rate during the forecast period, supported by the increasing adoption of biosimilars and rising prevalence of complex infectious diseases that require targeted biologic interventions.

- By Application

On the basis of application, the generic injectables for infectious diseases market is segmented into infectious diseases, oncology, diabetes, blood disorders, hormonal disorders, musculoskeletal disorders, CNS diseases, pain management, and cardiovascular diseases. The infectious diseases segment dominated the market with the largest share of 47.9% in 2024, as it directly represents the core use case for this category of generics. The high global burden of infectious conditions such as pneumonia, tuberculosis, bloodstream infections, and viral outbreaks has fueled continuous demand for injectable formulations.

The oncology segment is projected to witness the fastest growth during the forecast period, due to opportunistic infections in immunocompromised patients and the need for injectable anti-infectives in cancer care settings.

- By Route of Administration

On the basis of route of administration, the generic injectables for infectious diseases market is segmented into intramuscular, intravenous, and subcutaneous. The intravenous segment dominated the market with the highest share of 61.4% in 2024, owing to its fast systemic action, precise dosing, and preference in hospital settings for critical care. IV administration is especially common for antibiotics, antivirals, and antifungals in intensive care and emergency situations.

The subcutaneous segment is expected to grow steadily during forecast period, supported by home-based treatments, ease of self-administration, and increasing availability of pre-filled syringe formats for long-term infectious disease management.

- By Distribution Channel

On the basis of distribution channel, the generic injectables for infectious diseases market is segmented into hospital pharmacies, online pharmacies, and retail pharmacies. The hospital pharmacies segment held the largest market revenue share of 64.8% in 2024, driven by the fact that most injectable therapies are administered under medical supervision, particularly in acute and critical care settings. Hospital procurement and bulk purchasing further bolster this segment's dominance.

The online pharmacies segment is anticipated to experience the fastest growth from 2025 to 2032, propelled by growing digital health platforms, increased access to prescription injectables via e-commerce in urban regions, and the expansion of telemedicine services.

Generic Injectables for Infectious Diseases Market Regional Analysis

- North America dominated the generic injectables for infectious diseases market with the largest revenue share of 39.5% in 2024, driven by strong regulatory support, high generic penetration, and a mature pharmaceutical supply chain, with the U.S. showing increased reliance on injectable generics for hospital-acquired infections and outpatient parenteral antimicrobial therapy (OPAT)

- Healthcare providers in the region prioritize fast-acting, cost-effective treatments, making injectable generics a preferred choice for managing both acute and chronic infections in clinical settings

- This dominance is further supported by favorable regulatory frameworks, robust supply chains, and increased government initiatives to address antimicrobial resistance and drug shortages, reinforcing North America’s position as a key market for injectable anti-infectives across both public and private healthcare sectors

U.S. Generic Injectables for Infectious Diseases Market Insight

The U.S. generic injectables for infectious diseases market captured the largest revenue share of 82.5% in 2024 within North America, fueled by a high incidence of hospital-acquired infections and robust demand for cost-effective, rapid-action therapies. Hospitals and public health programs increasingly rely on generic injectables for managing critical infectious diseases, supported by streamlined regulatory pathways and favorable reimbursement structures. Additionally, U.S.-based manufacturers continue to expand production capabilities to address drug shortages and meet pandemic preparedness goals, further propelling market growth.

Europe Generic Injectables for Infectious Diseases Market Insight

The Europe generic injectables for infectious diseases market is projected to grow at a solid CAGR throughout the forecast period, driven by a rising focus on antimicrobial resistance (AMR) control, stringent health regulations, and efforts to reduce healthcare costs. Increased hospital admissions related to infectious conditions and the adoption of injectable generics as first-line therapies support market expansion. The presence of strong public healthcare systems and pan-European procurement strategies, especially in countries like France and Italy, is facilitating broader access to essential injectable treatments.

U.K. Generic Injectables for Infectious Diseases Market Insight

The U.K. generic injectables for infectious diseases market is expected to grow at a noteworthy CAGR during the forecast period, driven by NHS initiatives promoting generic use and heightened demand for injectable antibiotics and antivirals. As healthcare providers seek affordable alternatives amid increasing infectious disease burden, generic injectables are becoming a central component of treatment regimens. Ongoing investments in local manufacturing and the prioritization of sterile injectable supplies under national emergency preparedness programs further stimulate market growth.

Germany Generic Injectables for Infectious Diseases Market Insight

The Germany generic injectables for infectious diseases market is projected to expand steadily, supported by the country's highly organized healthcare infrastructure and emphasis on high-quality, cost-effective care. A strong preference for locally manufactured and EU-compliant generics, along with rigorous infection control protocols in hospitals, is encouraging increased use of injectable generics. Additionally, the growing adoption of biosimilar injectable treatments for infectious and immunological disorders aligns with the country’s sustainability and efficiency goals.

Asia-Pacific Generic Injectables for Infectious Diseases Market Insight

The Asia-Pacific generic injectables market is poised to grow at the fastest CAGR of 24.6% during the forecast period of 2025 to 2032, driven by a growing infectious disease burden, urbanization, and improved healthcare access in countries like India, China, and Indonesia. Government initiatives to increase generic drug penetration and domestic manufacturing capabilities are accelerating market adoption. APAC’s emergence as a global hub for API and injectable manufacturing is enhancing supply chain efficiency and reducing costs.

Japan Generic Injectables for Infectious Diseases Market Insight

The Japan generic injectables for infectious diseases market is gaining momentum as aging demographics and a high prevalence of healthcare-associated infections drive the need for reliable, hospital-grade injectable treatments. Japan’s focus on antimicrobial stewardship and its well-regulated pharmaceutical sector are fostering demand for generic injectables, particularly in hospital and long-term care settings. The market is also benefiting from local partnerships to produce biosimilar injectables for infectious and immunological diseases.

India Generic Injectables for Infectious Diseases Market Insight

The India generic injectables for infectious diseases market accounted for the largest market revenue share in Asia Pacific in 2024, fueled by strong domestic manufacturing, expanding healthcare infrastructure, and rising public health expenditure. The country serves as a major global supplier of generic injectable antibiotics and antivirals. Government programs aimed at increasing access to essential medicines in rural areas and initiatives like "Make in India" are further promoting injectable generic adoption across hospitals and public health centers.

Generic Injectables for Infectious Diseases Market Share

The Generic Injectables for Infectious Diseases industry is primarily led by well-established companies, including:

- DR. Reddys Laboratries Ltd (India)

- Baxter International (U.S.)

- Teva Pharmaceuticals (Israel)

- Astra Zeneca (U.S.)

- Sanofi (France)

- Fresenius Kabi (Germany)

- Pfizer Inc (U.S.)

- Cipla Ltd (India)

- Merck & Co. Inc (U.S.)

- Novartis AG (Switzerland)

- Sun Pharmaceutical Industries Ltd (India)

- Aurobindo Pharma Limited (India)

- Samsung Biologics Co Ltd (South Korea)

- Biocon (India)

- Lupin, Ltd (India)

- Hikma Pharmaceuticals (U.K.)

- Johnson & Johnson Services, Inc (U.S.)

- Amgen Inc. (U.S.)

- Piramal Pharma Solutions (India)

- Merck KGaA (Germany)

What are the Recent Developments in Global Generic Injectables for Infectious Diseases Market?

- In April 2024, Viatris Inc. announced the expansion of its injectable antibiotics portfolio through a strategic collaboration with the Global Antibiotic Research and Development Partnership (GARDP), aiming to improve access to critical treatments for drug-resistant infections in low- and middle-income countries. This initiative reflects Viatris' commitment to global health by increasing the availability of essential generic injectables and addressing the escalating threat of antimicrobial resistance through sustainable and affordable solutions

- In March 2024, Cipla Limited launched a new line of ready-to-use injectable cephalosporins across Southeast Asia and Africa. These formulations, designed for improved stability and ease of administration in resource-limited settings, reinforce Cipla’s focus on addressing unmet needs in infectious disease treatment. The initiative highlights Cipla’s leadership in expanding access to quality injectable generics and enhancing treatment outcomes in high-burden regions

- In March 2024, Hikma Pharmaceuticals plc entered into an agreement with Melinta Therapeutics to commercialize a generic injectable version of meropenem-vaborbactam, a combination antibiotic for treating complicated infections. This move strengthens Hikma’s hospital injectable offerings and reflects the growing importance of combination generics in combating multidrug-resistant pathogens. The partnership underscores industry efforts to broaden access to advanced anti-infective therapies

- In February 2024, Fresenius Kabi announced the launch of its generic line of antiviral injectables, including remdesivir and acyclovir, for hospital use across Europe and Latin America. The products are manufactured in compliance with stringent global standards, highlighting the company’s commitment to delivering high-quality generics to support pandemic preparedness and ongoing treatment of viral infections. This expansion reflects Fresenius Kabi’s strategic focus on biologics and injectables for infectious diseases

- In January 2024, Sandoz revealed its investment in a new sterile injectables manufacturing facility in Slovenia, aimed at increasing the production capacity for critical anti-infective generics. This development supports Sandoz’s goal of strengthening supply chain resilience and meeting growing global demand for injectable antibiotics and antivirals. The facility is expected to play a key role in ensuring a stable supply of essential medicines in times of health crises

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.