Global Geothermal Orc Market

Market Size in USD Billion

USD

6.17 Billion

USD

18.10 Billion

2024

2032

USD

6.17 Billion

USD

18.10 Billion

2024

2032

| 2025 - 2032 | |

| USD 6.17 Billion | |

| USD 18.10 Billion | |

| % | |

|

Geothermal ORC Market Size

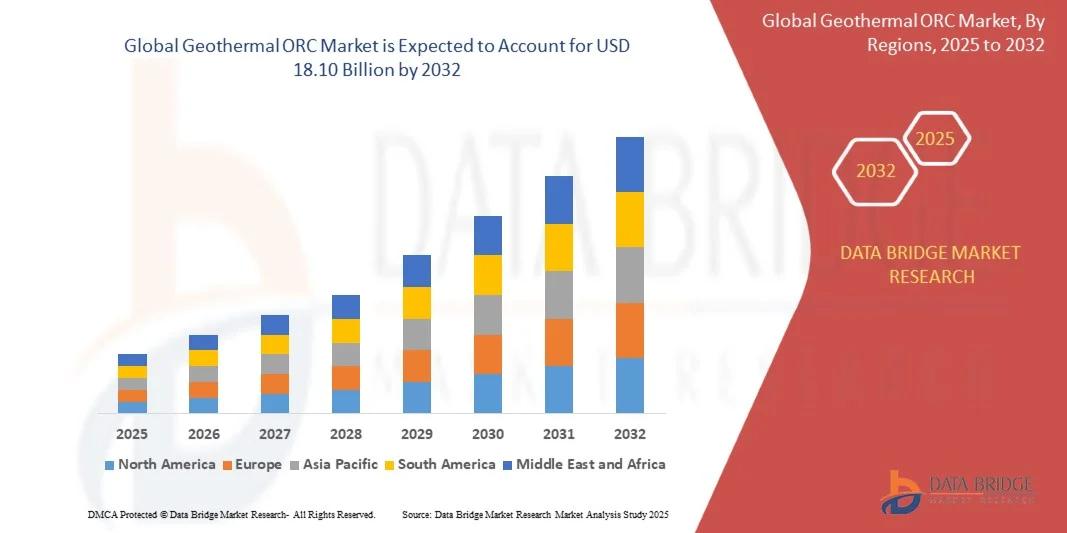

- The global geothermal ORC market size was valued at USD 6.17 billion in 2024 and is expected to reach USD 18.10 billion by 2032, at a CAGR of 14.4% during the forecast period

- The market growth is largely fueled by the increasing deployment of low- to medium-temperature geothermal resources and technological advancements in Organic Rankine Cycle (ORC) systems, enabling efficient power generation from previously untapped geothermal sites

- Furthermore, rising global demand for clean, baseload renewable energy and supportive government policies promoting decarbonization are driving investments in ORC-based geothermal projects, significantly boosting market expansion

Geothermal ORC Market Analysis

- Geothermal ORC systems utilize a closed-loop cycle to convert low- and medium-enthalpy geothermal heat into electricity, allowing power generation in areas where conventional geothermal technologies are not viable. This capability expands the geographical reach of geothermal energy, making it suitable for diverse regions worldwide

- The escalating demand for geothermal ORC solutions is primarily fueled by the need for stable, renewable baseload power, increasing pressure to reduce carbon emissions, and the growing cost-competitiveness of ORC technology compared to fossil-fuel-based generation

- North America dominated the geothermal ORC market with a share of 40.5% in 2024, due to strong investments in renewable energy infrastructure, abundant low- to medium-temperature geothermal resources, and supportive government policies promoting clean energy adoption

- Asia-Pacific is expected to be the fastest growing region in the geothermal ORC market during the forecast period due to rising energy demand, rapid industrialization, and the abundance of untapped geothermal resources in countries such as Indonesia, Japan, and the Philippines

- Electricity generation segment dominated the market with a market share of 60.5% in 2024, due to the global shift toward renewable energy and the need for stable, baseload power. Geothermal ORC systems provide reliable electricity output irrespective of weather conditions, positioning them as a key solution for grid stability and energy transition goals. The segment benefits from supportive government policies, subsidies for renewable installations, and technological innovations enhancing energy conversion efficiency. Its adoption is particularly strong in countries with abundant geothermal resources and established energy infrastructure

Report Scope and Geothermal ORC Market Segmentation

|

Attributes |

Geothermal ORC Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Geothermal ORC Market Trends

“Growth of Binary ORC Systems for Low-Temperature Geothermal Sources”

- The geothermal ORC market is increasingly adopting binary Organic Rankine Cycle (ORC) systems as they are well-suited for generating electricity from low-to-medium temperature geothermal sources. These systems expand the applicability of geothermal energy by utilizing reservoirs traditionally considered unsuitable for power generation

- For instance, Ormat Technologies has established itself as a market leader by deploying binary ORC geothermal power plants in regions with moderate geothermal resources such as the United States and Turkey. Companies such as Turboden are also scaling binary cycle solutions to broaden geothermal utilization globally

- Binary ORC systems use secondary organic fluids with low boiling points, allowing efficient energy extraction from geothermal brine at lower temperatures. This technology maximizes available resources and demonstrates feasibility in diverse geological conditions, expanding the range of viable geothermal projects

- The rising adoption of binary ORC plants also reflects growing interest in decentralization of power generation in areas where high-temperature geothermal resources are not abundant. Smaller-scale binary installations in remote or developing regions enable localized and sustainable energy supply

- The ability of binary ORC systems to integrate with heat recovery and hybrid renewable solutions boosts their competitive edge. By combining with technologies such as solar thermal or biomass, these systems add flexibility and enhance baseload generation potential beyond conventional geothermal

- The growth of binary ORC systems underscores how advancements in turbine technology, working fluids, and project finance are transforming the geothermal energy landscape. By unlocking low-temperature reservoirs, binary ORC systems are propelling wider geothermal adoption and long-term expansion of clean baseload energy supply

Geothermal ORC Market Dynamics

Driver

“Rising Demand for Renewable Baseload Power”

- The increasing need for reliable and renewable baseload electricity is a major driver of growth in the geothermal ORC market. Unlike intermittent renewable sources such as wind and solar, geothermal power delivers consistent and stable output, making it highly valuable for energy security and grid stability

- For instance, Ormat Technologies operates binary geothermal plants that provide continuous baseload electricity to regional grids in countries such as Kenya and Indonesia, proving the technology’s capability to meet industrial and residential energy needs while cutting emissions. Companies such as Cyrq Energy in the United States are also investing in expanding binary ORC projects to ensure long-term supply of clean baseload power

- Geothermal ORC plants offer sustainability advantages by producing electricity with minimal greenhouse gas emissions. This makes them crucial for addressing carbon-reduction targets worldwide, particularly as governments enforce stricter mandates to phase out fossil-fuel-based baseload power sources

- The scalability of ORC systems allows integration into diverse power grids, supporting both large-scale utilities and decentralized applications. Their ability to provide round-the-clock output aligns with energy policies focused on stabilizing renewable contributions within national electricity mixes

- The surging demand for decarbonized power supplies, coupled with the need for grid reliability, positions geothermal ORC technologies as vital resources for the future of sustainable electricity systems. Their dependable output makes them indispensable for achieving net-zero energy transition goals

Restraint/Challenge

“High Initial Investment”

- Geothermal ORC development requires significant upfront capital investments, which remain a major restraint on broader market penetration. Costs related to geological exploration, drilling, and infrastructure development are substantially higher compared to certain other renewable technologies, limiting entry for smaller firms or regions with constrained finance

- For instance, companies such as AltaRock Energy and other geothermal developers have highlighted cost challenges during preliminary drilling where resource uncertainty adds substantial financial risk. Even successful projects often require strong government incentives or international funding to progress past the exploration stage

- Complexity in site development increases project costs, as specialized expertise, drilling equipment, and long lead times are necessary to evaluate and construct geothermal ORC facilities. These factors often extend return-on-investment periods compared to technologies such as wind or solar

- The financing challenge is compounded by geographical risks, where the viability of geothermal reservoirs cannot be fully confirmed without significant exploration expenditures. This uncertainty makes investors cautious and limits the pace of large-scale deployments

- Addressing the high initial cost barrier will require innovative financing models, public-private partnerships, and continued efforts at reducing drilling costs and technological risks. Successfully overcoming these hurdles will be key for the geothermal ORC market to achieve wider adoption and sustainable long-term growth

Geothermal ORC Market Scope

The market is segmented on the basis of process type, application, capacity, end user, and technology.

• By Process Type

On the basis of process type, the geothermal ORC market is segmented into Dry Steam, Flash, and Binary. The Binary segment dominated the largest market revenue share in 2024, owing to its ability to efficiently utilize low- to medium-temperature geothermal resources, which are abundant in many regions. Binary systems are favored for their high efficiency, flexible site applicability, and environmentally friendly operation, as they minimize emissions and reduce the need for water-intensive processes. Their closed-loop design allows for continuous power generation while maintaining sustainability, making them highly attractive for both utility-scale and decentralized power projects. The segment also benefits from technological advancements that enhance heat exchange efficiency and reliability.

The Flash segment is anticipated to witness the fastest growth rate from 2025 to 2032, driven by its capability to handle high-temperature geothermal reservoirs for large-scale electricity generation. Flash systems are increasingly adopted in regions with deep geothermal resources, offering high energy output and reduced operational costs. Investments in expanding geothermal infrastructure, coupled with growing demand for renewable power, are expected to propel the segment’s adoption. Flash technology also appeals to developers aiming to integrate scalable and efficient geothermal plants into national grids.

• By Application

On the basis of application, the market is segmented into Electricity Generation, Direct Heat, and Others. The Electricity Generation segment dominated the largest market revenue share of 60.5% in 2024, fueled by the global shift toward renewable energy and the need for stable, baseload power. Geothermal ORC systems provide reliable electricity output irrespective of weather conditions, positioning them as a key solution for grid stability and energy transition goals. The segment benefits from supportive government policies, subsidies for renewable installations, and technological innovations enhancing energy conversion efficiency. Its adoption is particularly strong in countries with abundant geothermal resources and established energy infrastructure.

The Direct Heat segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing industrial and district heating applications. Industries such as food processing, agriculture, and chemical manufacturing are progressively integrating geothermal heat for process efficiency and cost savings. Direct heat applications also contribute to decarbonization goals by reducing dependence on fossil fuels. The growth is further supported by expanding urban heating networks and the development of small-scale decentralized heating projects in emerging markets.

• By Capacity

On the basis of capacity, the geothermal ORC market is segmented into 5 MW, 5–20 MW, 20–50 MW, and >50 MW. The 5–20 MW segment dominated the largest market revenue share in 2024, as it offers an optimal balance between installation cost, energy output, and operational efficiency. This mid-scale capacity range is particularly suitable for regional utilities and small industrial applications, allowing developers to leverage moderate geothermal resources without the significant capital expenditure associated with larger plants. The segment also benefits from modular design options, easier permitting, and faster deployment timelines compared to larger capacities.

The >50 MW segment is anticipated to witness the fastest growth from 2025 to 2032, driven by the increasing demand for large-scale renewable power integration and government-backed renewable energy targets. High-capacity geothermal ORC plants are favored in regions with extensive geothermal reservoirs, enabling economies of scale and competitive levelized cost of electricity (LCOE). Expansion of national grids, coupled with rising industrial electricity demand, is expected to further accelerate the adoption of large-capacity plants.

• By End User

On the basis of end user, the market is segmented into Utilities, Industrial, Residential, and Commercial. The Utilities segment dominated the largest market revenue share in 2024, owing to their role in implementing large-scale geothermal ORC projects for baseload electricity generation. Utility companies benefit from economies of scale, access to government incentives, and integration with existing power grids. The segment is further supported by the need for reliable, low-carbon energy sources to meet renewable energy targets and reduce dependence on fossil fuels.

The Industrial segment is expected to witness the fastest growth from 2025 to 2032, driven by increasing adoption of geothermal heat and electricity for process industries such as food, paper, and chemical manufacturing. Industrial end users prioritize cost savings, sustainability, and operational efficiency, which geothermal ORC systems can provide. Growing awareness of carbon footprint reduction and energy efficiency regulations is also fueling this segment’s expansion.

• By Technology

On the basis of technology, the geothermal ORC market is segmented into Organic Rankine Cycle (ORC) and Kalina Cycle. The Organic Rankine Cycle segment dominated the largest market revenue share in 2024, due to its widespread adoption, technical maturity, and ability to efficiently convert low- to medium-temperature geothermal heat into electricity. ORC systems offer flexible design, high reliability, and relatively lower installation costs, making them suitable for both small and large-scale projects. Continuous innovations in ORC components, such as heat exchangers and turbines, further enhance efficiency and expand applicability.

The Kalina Cycle segment is anticipated to witness the fastest growth from 2025 to 2032, driven by its higher thermal efficiency and suitability for high-temperature geothermal resources. The technology is gaining attention in regions seeking maximum energy extraction and improved plant performance. Research and development initiatives, combined with pilot project deployments, are expected to accelerate the adoption of Kalina Cycle technology in large-scale geothermal power plants.

Geothermal ORC Market Regional Analysis

- North America dominated the geothermal ORC market with the largest revenue share of 40.5% in 2024, driven by strong investments in renewable energy infrastructure, abundant low- to medium-temperature geothermal resources, and supportive government policies promoting clean energy adoption

- The region benefits from advanced technological expertise, favorable regulatory frameworks, and increasing demand for stable, baseload renewable power, encouraging the development of binary and flash ORC plants

- The growing focus on decarbonization and grid reliability, combined with public–private partnerships, continues to strengthen North America’s leadership in geothermal ORC projects

U.S. Geothermal ORC Market Insight

The U.S. geothermal ORC market captured the largest revenue share in 2024 within North America, fueled by a well-established geothermal resource base and continuous federal incentives for renewable energy deployment. Rising electricity demand, combined with state-level renewable portfolio standards, has accelerated investments in mid-scale and large-scale ORC plants. Ongoing technological improvements, along with the presence of key developers and manufacturers, further reinforce the country’s dominant position in the region.

Europe Geothermal ORC Market Insight

The Europe geothermal ORC market is projected to expand at a substantial CAGR during the forecast period, supported by the European Union’s decarbonization targets and strong policy frameworks promoting sustainable power generation. Countries such as Italy, Turkey, and Germany are increasingly adopting ORC technology for both electricity generation and district heating. Rising energy security concerns and the availability of favorable feed-in tariffs are boosting the development of small- and mid-scale geothermal projects across the region.

U.K. Geothermal ORC Market Insight

The U.K. geothermal ORC market is anticipated to grow at a notable CAGR during the forecast period, driven by government initiatives aimed at achieving net-zero carbon emissions. Increasing exploration of deep geothermal resources and pilot ORC projects for combined heat and power applications are fostering market development. The country’s strong focus on innovation and renewable integration into national grids further enhances growth opportunities.

Germany Geothermal ORC Market Insight

The Germany geothermal ORC market is expected to grow steadily, supported by the country’s ambitious energy transition policies and significant investment in low-carbon technologies. Germany’s emphasis on sustainable heating solutions and its advanced engineering capabilities are accelerating the adoption of binary ORC systems for electricity and district heating. Strong environmental regulations and public funding programs continue to attract developers to geothermal energy projects.

Asia-Pacific Geothermal ORC Market Insight

The Asia-Pacific geothermal ORC market is poised to grow at the fastest CAGR from 2025 to 2032, fueled by rising energy demand, rapid industrialization, and the abundance of untapped geothermal resources in countries such as Indonesia, Japan, and the Philippines. Government-backed renewable energy targets, coupled with increasing foreign investments, are driving the expansion of large-scale ORC power plants across the region. The growing presence of regional manufacturers and lower development costs further enhance market potential.

Japan Geothermal ORC Market Insight

The Japan geothermal ORC market is gaining traction due to the country’s need for stable, non-intermittent renewable energy sources to reduce dependence on imported fossil fuels. High geothermal potential, combined with strong government support for clean energy projects, is spurring investments in binary and flash ORC technologies. Japan’s technological expertise and focus on efficient, compact power systems make it a key market in the region.

China Geothermal ORC Market Insight

The China geothermal ORC market accounted for the largest revenue share in Asia-Pacific in 2024, driven by rapid urbanization, large-scale renewable energy initiatives, and extensive geothermal resource exploration. Supportive government policies, cost-competitive project development, and the presence of leading domestic equipment suppliers are fueling market growth. China’s focus on district heating and the expansion of clean power capacity position it as a central hub for geothermal ORC adoption.

Geothermal ORC Market Share

The geothermal ORC industry is primarily led by well-established companies, including:

- Ormat Technologies, Inc. (U.S.)

- Turboden (Italy)

- Mitsubishi Heavy Industries (Japan)

- Toshiba Corporation (Japan)

- Ecopiezo (Turkey)

- Hitachi Zosen (Japan)

- Siemens Energy (Germany)

- Gradient (U.S.)

- Nuovo Pignone (Italy)

- Fuji Electric (Japan)

- Baker Hughes (U.S.)

- IHI Corporation (Japan)

- GE Renewable Energy (France)

- Enexor (U.S.)

- Exergy (Italy)

Latest Developments in Geothermal ORC Market

- In June 2024, Turboden commissioned a large-scale Organic Rankine Cycle (ORC) geothermal plant in Turkey, specifically designed to harness low- to medium-temperature geothermal resources for electricity generation. This project represents a significant step forward in expanding geothermal power capacity in Europe and the Middle East, where demand for clean, baseload renewable energy is surging. By demonstrating the economic viability of utilizing medium-enthalpy resources, Turboden is strengthening its competitive position in the global market while encouraging other regional players to adopt ORC technology for efficient, cost-effective geothermal power generation

- In February 2024, Ormat Technologies secured a landmark contract to supply advanced ORC equipment for a new high-capacity geothermal power plant in Indonesia. Indonesia, which holds one of the world’s largest untapped geothermal reserves, is rapidly emerging as a key growth hub for the ORC market. This contract enhances Ormat’s market footprint in Southeast Asia and also underscores the growing attractiveness of ORC systems for countries seeking reliable renewable energy solutions to meet rising electricity demand and ambitious decarbonization targets

- In October 2023, Exergy International successfully deployed its next-generation binary geothermal power unit in Italy, integrating state-of-the-art heat exchanger and turbine technology to achieve higher thermal efficiency and lower operating costs. This installation aligns with Europe’s energy transition goals and reinforces Exergy’s ability to deliver innovative, high-performance ORC systems capable of optimizing energy extraction from low-enthalpy geothermal sources. The project demonstrates how advanced engineering can drive profitability and scalability for geothermal plants across Europe’s evolving renewable energy landscape

- In March 2023, Toshiba Energy Systems unveiled an upgraded ORC module featuring enhanced thermal efficiency, a more compact footprint, and simplified maintenance requirements to serve small- to mid-scale geothermal projects. This development expands Toshiba’s product portfolio and enables utilities, independent power producers, and industrial players to deploy flexible, cost-effective geothermal power solutions in remote or resource-limited areas. By addressing the need for adaptable and efficient systems, Toshiba is helping accelerate ORC adoption in markets where traditional large-scale geothermal installations may not be feasible

- In September 2022, Mitsubishi Heavy Industries introduced a binary power generation system leveraging ORC technology to capture waste heat from sulfur-free fuel-burning engines and convert it into usable energy. Offering outputs ranging from 200 kW to 700 kW, this advanced system provides high thermal efficiency, complete sealing, and minimal maintenance requirements. By extending ORC applications beyond traditional geothermal sources into waste-heat-to-energy markets, Mitsubishi has significantly strengthened its competitive positioning and opened new revenue opportunities for ORC technology in the maritime and industrial sectors

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.