Global Glaucoma Market

Market Size in USD Billion

USD

9.46 Billion

USD

16.31 Billion

2025

2033

USD

9.46 Billion

USD

16.31 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.46 Billion | |

| USD 16.31 Billion | |

| % | |

|

Glaucoma Market Size

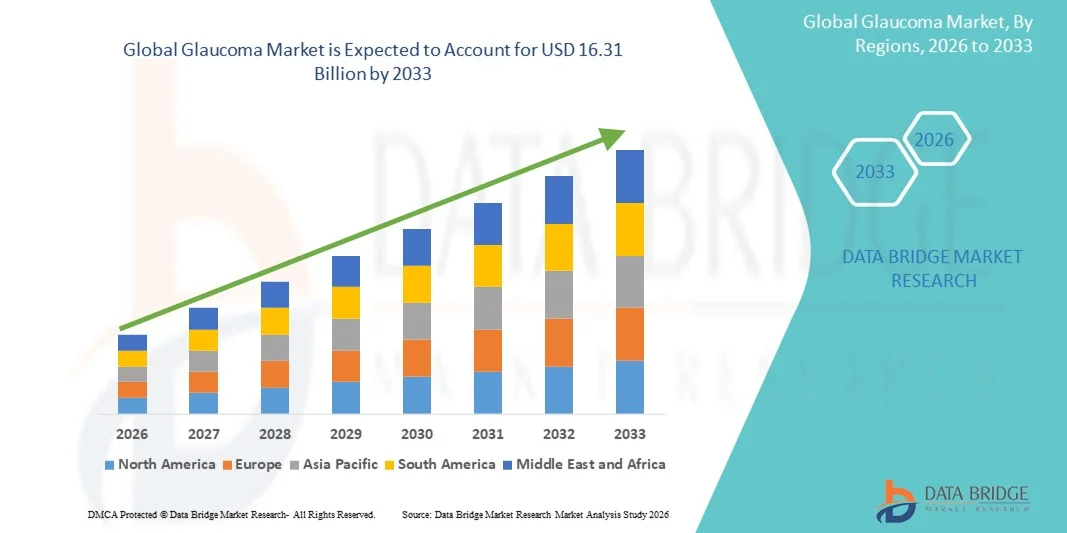

- The global glaucoma market size was valued at USD 9.46 billion in 2025 and is expected to reach USD 16.31 billion by 2033, at a CAGR of 7.05% during the forecast period

- The market growth is largely fueled by the rising prevalence of glaucoma due to ageing populations, increased awareness, and technological advancements in diagnostics and treatment, including minimally invasive surgeries and sustained‑release drug delivery systems

- Furthermore, growing demand for effective, safe, and patient-friendly glaucoma management solutions from both healthcare providers and patients is establishing modern therapies and devices as the preferred standard of care. These converging factors are accelerating the adoption of advanced glaucoma treatments, thereby significantly boosting the industry's growth

Glaucoma Market Analysis

- Glaucoma, encompassing optic nerve disorders that can lead to irreversible vision loss, is increasingly managed through medications, laser therapies, and minimally invasive surgeries, making it a critical segment within ophthalmic care

- The escalating demand for glaucoma treatments is primarily fueled by the rising prevalence of glaucoma due to ageing populations, diabetes, and other risk factors, coupled with improved screening, early diagnosis, and technological advancements in sustained‑release therapeutics and surgical implants

- North America dominated the glaucoma market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong R&D activity, with the U.S. experiencing substantial growth in glaucoma diagnosis and treatment, driven by innovations in both drug therapies and minimally invasive surgical devices

- Asia‑Pacific is expected to be the fastest growing region in the glaucoma market during the forecast period, due to increasing geriatric populations, rising healthcare awareness, improving access to care in emerging economies, and favourable government initiatives

- The open‑angle glaucoma segment dominated the glaucoma market with a market share of 55.4% in 2025, due its higher global prevalence, slow disease progression allowing for early diagnosis, and the availability of effective treatment options including medications and minimally invasive surgical procedures

Report Scope and Glaucoma Market Segmentation

|

Attributes |

Glaucoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Glaucoma Market Trends

Enhanced Convenience Through AI and Advanced Diagnostics

- A significant and accelerating trend in the global glaucoma market is the integration of artificial intelligence (AI) and advanced imaging diagnostics, such as optical coherence tomography (OCT) and AI‑enabled fundus analysis, into glaucoma screening and monitoring workflows to improve early detection and treatment precision

- For instance, AI‑powered fundus imaging systems can detect glaucomatous changes with high sensitivity and specificity, enabling mass screening in areas with limited access to ophthalmologists

- AI integration in glaucoma care allows features such as risk prediction for disease progression, remote monitoring of intraocular pressure fluctuations, and automated alerts for timely intervention, thereby improving patient convenience and outcomes

- The seamless integration of diagnostic platforms, AI analytics, surgical devices, and drug delivery systems is enabling a more unified and patient‑centric glaucoma care ecosystem, linking screenings, treatment adjustments, adherence monitoring, and outcomes tracking

- Increasing adoption of tele‑ophthalmology platforms is enhancing remote patient monitoring and consultations, reducing clinic visits, and improving treatment compliance, especially in rural and underserved regions

- Collaboration between ophthalmic device manufacturers, AI companies, and digital health startups is accelerating the development of smart, connected glaucoma solutions, driving market innovation and differentiation

- This trend towards intelligent, connected, and individualized glaucoma management is reshaping expectations for ophthalmic care and driving adoption of digital diagnostics and tele‑ophthalmology solutions alongside traditional therapies

Glaucoma Market Dynamics

Driver

Rising Prevalence Due to Ageing Populations & Better Diagnostics

- The increasing prevalence of glaucoma caused by ageing populations, diabetes, and other risk factors, along with improved screening and early diagnosis, is a primary driver for the glaucoma market

- For instance, epidemiological studies report glaucoma incidence rising to ~23.46 per 10,000 person‑years among adults aged 40‑79, particularly in older age groups, fueling demand for treatment and monitoring

- Healthcare providers are expanding routine glaucoma screening programmes, particularly in emerging markets with previously low diagnosis rates, increasing the patient pool for therapy

- More patients entering the glaucoma care pathway earlier is creating greater demand for pharmaceuticals, surgical interventions, and medical devices, contributing to market expansion

- Increasing awareness campaigns by healthcare organizations and governments about the importance of early glaucoma detection are encouraging more individuals to seek treatment

- Technological advancements in sustained‑release drug delivery and minimally invasive surgical options are improving treatment adherence and patient outcomes, further boosting market growth

- Therefore, the combination of higher disease prevalence and enhanced detection continues to provide strong growth momentum for the global glaucoma market

Restraint/Challenge

Adherence Issues, Side‑Effects & Regulatory Hurdles

- Patient non-adherence to topical glaucoma therapies, with many discontinuing within months, remains a major challenge, limiting effective disease management and overall market growth

- Adverse ocular or systemic side‑effects of medications, along with the need for long-term safety evidence for implants or minimally invasive surgical devices, can reduce uptake

- For instance, regulatory authorities require extensive post‑approval safety and efficacy data for sustained‑release implants and MIGS devices, prolonging development timelines and increasing costs

- Limited access, high treatment costs relative to traditional therapy, and insufficient ophthalmic infrastructure in emerging regions can constrain widespread adoption

- Complexity of treatment regimens, frequent dosing schedules, and lack of patient education can further exacerbate non-compliance issues

- Market entry barriers for new drug formulations and innovative devices due to stringent approvals and pricing regulations can slow growth for emerging players

- Collectively, these challenges adherence, side-effects, regulatory requirements, and access gaps pose significant hurdles to realizing the full potential of the glaucoma market

Glaucoma Market Scope

The market is segmented on the basis of type, drug class, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the glaucoma market is segmented into Closed Angle Glaucoma (CAG), Open Angle Glaucoma (OAG), Secondary Glaucoma, Congenital Glaucoma, and Others. The Open Angle Glaucoma (OAG) segment dominated the market with the largest revenue share of 55.4% in 2025, owing to its higher prevalence worldwide. OAG progresses slowly, allowing for earlier diagnosis and management, which increases the demand for both pharmacological and surgical treatments. The segment benefits from wide availability of effective medications such as prostaglandin analogs and beta-blockers, as well as minimally invasive surgical devices. Screening programs targeting adults over 40 years old further boost the adoption of OAG therapies. The segment also sees strong growth in developed countries due to advanced diagnostic infrastructure and greater patient awareness. Tele-ophthalmology platforms and AI-based screening tools are enhancing early detection, reinforcing the dominance of this segment.

The Closed Angle Glaucoma (CAG) segment is anticipated to witness the fastest growth rate of 6.2% from 2026 to 2033, driven by its acute presentation requiring rapid treatment and increasing awareness of emergency care. CAG can lead to sudden vision loss if untreated, which increases hospital visits and adoption of surgical interventions. Rising awareness campaigns and screening programs in Asia-Pacific and Latin America are contributing to faster diagnosis rates. Moreover, technological advancements in laser therapy and minimally invasive surgical options are improving treatment efficacy and patient compliance. Hospitals and specialty centers are increasingly adopting innovative devices to manage CAG, supporting segment growth. Early intervention strategies and patient education initiatives are expected to further accelerate adoption over the forecast period.

- By Drug Class

On the basis of drug class, the glaucoma market is segmented into beta blockers, prostaglandins, alpha adrenergic agonists, carbonic anhydrase inhibitors, combination drugs, and others. The Prostaglandins segment dominated the market with a revenue share of 48% in 2025 due to its once-daily dosing, high efficacy in reducing intraocular pressure (IOP), and better patient adherence. Prostaglandins are widely recommended as first-line therapy for OAG, supported by clinical evidence of superior IOP reduction. The segment is also favored in developed countries with robust prescription practices and patient awareness. Increasing geriatric populations and rising prevalence of chronic glaucoma cases are driving consistent demand. Pharmaceutical companies continue to develop new formulations and delivery systems, such as sustained-release implants, further reinforcing dominance. The segment also benefits from reimbursement policies in North America and Europe that facilitate access to advanced therapies.

The Combination Drugs segment is expected to witness the fastest CAGR of 6.5% from 2026 to 2033, driven by the growing demand for medications that improve efficacy while reducing the number of drops required daily. Combination therapies address patient adherence challenges and are particularly useful for patients with moderate-to-severe glaucoma. Launch of fixed-dose combinations and novel formulations is increasing convenience and reducing side-effects. Emerging markets with rising awareness and improving healthcare infrastructure are showing higher uptake of combination drugs. Hospitals and specialty clinics are increasingly recommending combination therapy to optimize treatment outcomes. The segment growth is further accelerated by increased regulatory approvals and clinical studies supporting combination drug efficacy.

- By Route of Administration

On the basis of route of administration, the glaucoma market is segmented into oral, injections, intravitreal, and others. The Oral route dominated the market with a revenue share of 50% in 2025, largely due to the widespread use of oral carbonic anhydrase inhibitors for controlling intraocular pressure. Oral medications are particularly important for patients not responsive to topical therapy or requiring systemic management. The route benefits from strong adoption in hospitals and specialty centers, with established prescription protocols and patient familiarity. Ongoing clinical research is improving formulations to minimize systemic side-effects. The segment also sees higher usage in regions with limited access to advanced surgical treatments. Patient compliance programs and educational initiatives enhance acceptance and sustained usage, reinforcing the segment’s dominance.

The Intravitreal route is expected to witness the fastest growth rate of 7.1% from 2026 to 2033, driven by innovations in sustained-release implants and injectable therapies. Intravitreal delivery enables targeted treatment for advanced or refractory glaucoma cases and reduces the burden of frequent eye drop administration. Technological advancements in biodegradable implants and microinjection devices are improving safety and efficacy. Hospitals and specialty ophthalmic centers are increasingly adopting intravitreal approaches for complex cases. Rising awareness about advanced therapies and patient willingness to opt for minimally invasive procedures further fuels segment growth. Expansion of reimbursement policies and clinical support for intravitreal therapies in developed regions accelerates adoption.

- By End-Users

On the basis of end-users, the glaucoma market is segmented into hospitals, specialty centers, and others. The Hospitals segment dominated the market with a revenue share of 60% in 2025, driven by high patient volumes, availability of advanced diagnostic tools, and the presence of specialized ophthalmology departments. Hospitals provide a one-stop solution for diagnosis, treatment, and follow-up care, attracting both early-stage and severe glaucoma patients. The segment also benefits from insurance coverage and reimbursement for hospital-based therapies. Collaborations between hospitals and device/pharma companies further improve access to innovative treatments. Patient education and outreach programs conducted by hospitals enhance treatment adherence. Hospitals also lead in adopting AI-enabled screening and tele-ophthalmology platforms, consolidating their dominance.

The Specialty Centers segment is expected to witness the fastest growth rate of 8.2% from 2026 to 2033, fueled by the increasing number of dedicated eye care clinics and high patient preference for personalized glaucoma management. These centers offer specialized services including MIGS, laser therapy, and sustained-release drug implants. Rising awareness about advanced treatment options encourages patients to seek care at specialty centers. Technological investments, staff training, and focused marketing by these centers drive patient trust and adoption. Growing urban populations and increased accessibility of specialty centers in developing countries also contribute to rapid growth. Teleconsultation and remote monitoring services offered by specialty centers further support adoption and expansion.

- By Distribution Channel

On the basis of distribution channel, the glaucoma market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The Hospital Pharmacy segment dominated the market with a revenue share of 57% in 2025 due to direct availability of prescribed glaucoma medications and medical devices to patients visiting hospitals. Hospital pharmacies facilitate adherence by ensuring patients receive recommended medications immediately after consultation. The segment benefits from insurance reimbursements and partnerships with pharmaceutical companies. Hospitals also provide counseling and guidance for proper administration of therapies. The convenience and trust associated with hospital pharmacies reinforce their dominant position. Adoption of integrated pharmacy systems in hospitals further streamlines supply and patient care.

The Online Pharmacy segment is expected to witness the fastest growth rate of 12% from 2026 to 2033, driven by the rising trend of e-commerce, increased smartphone penetration, and preference for home delivery of medications. Online pharmacies improve access for patients in remote areas, enhancing adherence to chronic glaucoma therapy. Availability of subscription-based refill programs and teleconsultation services complements online sales. Awareness campaigns and regulatory approvals for online medicine distribution in various countries support segment growth. Integration with mobile apps and reminder systems for dosage adherence further drives adoption. Growing comfort with digital health platforms among geriatric and tech-savvy populations accelerates online pharmacy uptake.

Glaucoma Market Regional Analysis

- North America dominated the glaucoma market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong R&D activity, with the U.S. experiencing substantial growth in glaucoma diagnosis and treatment, driven by innovations in both drug therapies and minimally invasive surgical devices

- Patients and healthcare providers in the region highly value early detection, advanced therapeutics, and minimally invasive surgical options, leading to higher adoption of medications, laser therapies, and device-based interventions

- This widespread adoption is further supported by strong government initiatives, high awareness of eye health, extensive insurance coverage, and the presence of key ophthalmic companies, establishing North America as a leading region for glaucoma care

U.S. Glaucoma Market Insight

The U.S. glaucoma market captured the largest revenue share of 37% in 2025 within North America, fueled by rising prevalence of glaucoma, advanced healthcare infrastructure, and early diagnosis initiatives. Patients and healthcare providers are increasingly prioritizing regular screenings, effective pharmacological therapies, and minimally invasive surgical interventions. The growing awareness of glaucoma risks, combined with technological advancements in AI-based diagnostics, tele-ophthalmology, and sustained-release drug delivery systems, further propels the market. Moreover, insurance coverage and reimbursement policies for glaucoma medications and devices are significantly contributing to market expansion.

Europe Glaucoma Market Insight

The Europe glaucoma market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by aging populations, high healthcare standards, and growing awareness about early diagnosis and treatment. The increase in urbanization, coupled with the demand for advanced therapies and minimally invasive procedures, is fostering the adoption of glaucoma treatments. European patients are drawn to innovative treatment options, including combination drugs and MIGS devices. The region is witnessing significant growth across hospitals, specialty centers, and clinics, with glaucoma care being incorporated into both routine health check-ups and advanced treatment plans.

U.K. Glaucoma Market Insight

The U.K. glaucoma market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of chronic eye disorders, rising awareness about early detection, and the adoption of advanced therapies. Concerns regarding vision loss and quality of life are encouraging patients and healthcare providers to seek timely intervention. The U.K.’s well-established healthcare system, along with the availability of innovative pharmaceuticals and minimally invasive devices, is expected to continue to stimulate market growth. Tele-ophthalmology and AI-assisted diagnostics are also contributing to higher patient engagement and treatment adherence.

Germany Glaucoma Market Insight

The Germany glaucoma market is expected to expand at a considerable CAGR during the forecast period, fueled by high awareness of eye health, strong healthcare infrastructure, and demand for technologically advanced treatment solutions. Germany’s emphasis on innovation and early diagnosis promotes the adoption of both pharmacological and surgical interventions. The integration of digital health solutions, such as AI-based monitoring, teleconsultation, and sustained-release drug delivery systems, is increasing efficiency and convenience in glaucoma management. Patients and physicians are increasingly choosing personalized treatment plans aligned with local regulatory standards and clinical best practices.

Asia-Pacific Glaucoma Market Insight

The Asia-Pacific glaucoma market is poised to grow at the fastest CAGR of 7.8% during the forecast period of 2026 to 2033, driven by rising geriatric populations, increasing prevalence of diabetes, and growing awareness of glaucoma symptoms in countries such as China, Japan, and India. The region’s expanding healthcare infrastructure, government initiatives promoting eye care, and adoption of advanced diagnostics and therapies are driving market growth. In addition, affordability of innovative drug formulations and surgical devices, coupled with increasing accessibility in urban and semi-urban areas, is contributing to rapid adoption.

Japan Glaucoma Market Insight

The Japan glaucoma market is gaining momentum due to the country’s aging population, high healthcare standards, and strong adoption of innovative diagnostic and treatment technologies. Japan places significant emphasis on preventive care and early disease management, driving adoption of AI-assisted diagnostics, tele-ophthalmology, and minimally invasive surgical procedures. The integration of advanced drug delivery systems, combined with patient education programs, is fueling growth. Moreover, Japan’s high-tech healthcare environment supports the widespread use of sustained-release implants and combination drug therapies in both hospitals and specialty clinics.

India Glaucoma Market Insight

The India glaucoma market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to increasing awareness of eye diseases, rising geriatric population, and growing healthcare access. India is witnessing expanding adoption of advanced diagnostic technologies, combination drug therapies, and minimally invasive surgical devices. The push towards improved healthcare infrastructure, government programs for eye care, and availability of affordable treatment options are key factors propelling the market. In addition, private hospitals and specialty eye centers are playing a major role in delivering timely diagnosis and effective glaucoma management across urban and semi-urban regions.

Glaucoma Market Share

The Glaucoma industry is primarily led by well-established companies, including:

- Glaukos Corporation (U.S.)

- Alcon Inc. (U.S.)

- Johnson & Johnson Vision Care, Inc. (U.S.)

- Santen Pharmaceutical Co., Ltd. (Japan)

- iSTAR Medical (Switzerland)

- New World Medical, Inc. (U.S.)

- Iridex Corporation (U.S.)

- Nova Eye Medical (U.S.)

- Iantrek (U.S.)

- Lumenis Ltd. (Israel)

- Carl Zeiss Meditec AG (Germany)

- Teva Pharmaceuticals Industries Ltd. (Israel)

- NicOx (France)

- Bausch + Lomb (U.S.)

- Sight Sciences, Inc. (U.S.)

- MicroSurgical Technology, Inc. (U.S.)

- Oertli Instrumente AG (Switzerland)

- Topcon Corporation (Japan)

- ASICO, LLC (U.S.)

What are the Recent Developments in Global Glaucoma Market?

- In June 2025, Glaukos announced that it had received European Union (EU) Medical Device Regulation (MDR) certification for its iStent infinite® and other micro‑invasive glaucoma surgery (MIGS) devices, marking its first approvals under the new, more rigorous European regulatory framework and positioning the company to expand commercial launch in Europe

- In April 2025, clinical evidence emerged supporting use of selective laser trabeculoplasty (SLT) as a first‑line treatment option for glaucoma, demonstrating significant intraocular pressure reductions and improved outcomes when used early in the disease course reflecting the shifting treatment paradigm away from reliance solely on topical medications

- In October 2024, a review published via Reuters highlighted that laser therapy (specifically selective laser trabeculoplasty) was more effective than eye‑drop treatment in slowing glaucoma disease progression, suggesting that early interventional and surgical approaches may increasingly become preferred over traditional topical medication regimens

- In December 2023, Glaukos received FDA approval for its iDose TR implant for a single administration per eye of 75 µg travoprost, indicated for reducing intraocular pressure (IOP) in patients with ocular hypertension or open‑angle glaucoma. The approval was based on two pivotal Phase 3 trials (1,150 subjects across 89 sites) showing comparable IOP reduction to timolol and a good safety profile. The product is seen as a paradigm shift from daily drops toward sustained‑release implants

- In February 2023, Glaukos Corporation submitted a New Drug Application (NDA) to the U.S. Food & Drug Administration for its iDose® TR (travoprost intracameral implant), a first‑of‑its‑kind long‑duration intra‑ocular implant designed to continuously deliver therapeutic levels of drug inside the eye for patients with open‑angle glaucoma or ocular hypertension. The company’s announcement emphasised the potential to address the longstanding issue of patient non‑compliance with topical therapies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.