Global Glp 1gipglucagon Triple Agonist Drug Market

Market Size in USD Billion

USD

2.48 Billion

USD

9.77 Billion

2025

2033

USD

2.48 Billion

USD

9.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.48 Billion | |

| USD 9.77 Billion | |

| % | |

|

GLP-1/GIP/Glucagon Triple Agonist Drug Market Overview

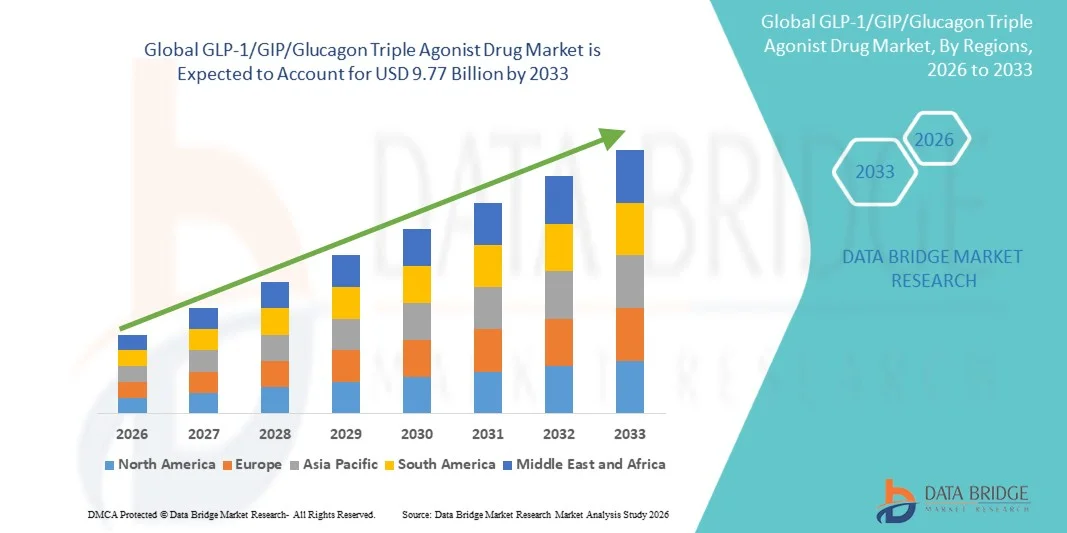

The GLP-1/GIP/Glucagon Triple Agonist Drug Market was valued at USD 2.48 billion in 2025 and is projected to reach USD 9.77 billion by 2033, growing at a CAGR of 18.70% from 2026 to 2033. The market is experiencing strong growth driven by the rising global prevalence of obesity, type 2 diabetes, and other cardiometabolic disorders, along with increasing demand for highly effective multi-target incretin-based therapies. GLP-1/GIP/Glucagon triple agonist drugs are gaining attention due to their ability to simultaneously regulate appetite, improve insulin sensitivity, enhance glucose control, and support significant weight reduction compared to traditional monotherapy treatments.

In addition, rapid advancements in peptide engineering, next-generation biologics development, and long-acting injectable formulations are accelerating drug innovation in this space. Pharmaceutical companies are increasingly investing in clinical trials and R&D pipelines focused on multi-agonist mechanisms to improve metabolic outcomes. Growing awareness of obesity as a chronic disease, rising adoption of precision medicine approaches, and expanding reimbursement support in developed healthcare systems are further driving market expansion across global regions.

Key Market Trends & Insights

- North America dominated the GLP-1/GIP/Glucagon Triple Agonist Drug Market with the largest revenue share of 39.26% in 2025, supported by high obesity and type 2 diabetes prevalence, strong penetration of advanced biologic therapies, early adoption of next-generation incretin-based drugs, and robust reimbursement frameworks. The region also benefits from strong presence of leading pharmaceutical companies and active clinical trial pipelines for multi-agonist therapies.

- The GIP/GLP-1 dual agonists segment dominated the market with a share of 52.64% in 2025 due to strong clinical validation, widespread physician adoption, and proven efficacy in improving glycemic control and inducing significant weight reduction.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 12.4% from 2026 to 2033, fueled by rising prevalence of obesity and diabetes, increasing healthcare access, expanding pharmaceutical manufacturing capabilities, and growing adoption of advanced metabolic disorder treatments across China, India, Japan, and South Korea.

- The obesity treatment application segment dominated the market with revenue share in 2025, driven by increasing global obesity rates, rising awareness of weight management therapies, and strong clinical adoption of GLP-1/GIP dual and triple agonist drugs for long-term weight reduction.

- The type 2 diabetes segment remains the second-largest application area, supported by growing patient population, increasing demand for improved glycemic control therapies, and strong clinical efficacy of multi-agonist incretin drugs in managing insulin resistance.

- The retail & online pharmacies segment is expected to be the fastest-growing distribution channel, driven by rising self-administration trends, expansion of digital pharmacy platforms, and increasing availability of prescription-based weight management drugs through regulated e-pharmacy networks.

Market Size & Forecast

- Global Market Value (2025): USD 2.48 Billion

- Expected Market Value (2033): USD 9.77 Billion

- Forecast CAGR (2026–2033): 18.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and GLP-1/GIP/Glucagon Triple Agonist Drug Market Segmentation

|

Attributes |

GLP-1/GIP/Glucagon Triple Agonist Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Eli Lilly and Company (U.S.) |

|

Market Opportunities |

· Expansion into Obesity and Metabolic Syndrome Treatment · Development of Next-Generation Precision Metabolic Therapies · Expansion of Clinical Applications Beyond Diabetes and Obesity |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

GLP-1/GIP/Glucagon Triple Agonist Drug Market Trends

Trend: Growth in Motorsports & Professional Training

Professional racing teams are increasingly adopting high-fidelity GLP-1/GIP/Glucagon Triple Agonist Drug to enhance driver skills, test vehicle performance, and develop race strategies without the cost and risk of physical track testing. The integration of real-time telemetry capture enables precise analysis of driving behavior and vehicle dynamics. Racing schools and academies are similarly leveraging simulators to train aspiring professional drivers through standardized, data-driven learning modules, while VR and AR technologies create immersive environments that closely replicate real-world racing conditions.

GLP-1/GIP/Glucagon Triple Agonist Drug Market Dynamics

Key Market Driver: Growing Adoption of Simulation in Autonomous Vehicle Development

The rapid development of autonomous vehicles and Advanced Driver Assistance Systems (ADAS) has created substantial demand for high-fidelity GLP-1/GIP/Glucagon Triple Agonist Drug that can validate AI algorithms, sensor models, and vehicle behavior in millions of virtual scenarios impossible to replicate through physical testing. Automotive OEMs, Tier-1 suppliers, and technology companies are deploying simulators as a core component of their development pipeline, reducing costs, accelerating iteration cycles, and improving system safety.

Key Restraint/Challenge: High Initial Investment Cost of Advanced Simulators

A significant restraint in the global driving simulator market is the high upfront capital required for advanced simulation systems. Modern platforms integrate high-fidelity graphics, realistic vehicle dynamics engines, motion platforms, and immersive virtual environments, demanding substantial investment in procurement, installation, and ongoing maintenance. The total cost of ownership extends to software licenses, periodic upgrades, and technical support, making adoption difficult for smaller driving schools, research institutions, and emerging-market organizations.

The October 2024 launch of the Dresden Driving Simulator (DDS), a world-first sustained acceleration simulator for ADAS and highly automated driving research developed by AMST and Technische University Dresden, illustrates the scale of capital commitment required for cutting-edge simulation infrastructure, reflecting the broader challenge of adoption beyond well-funded organizations.

Key Market Opportunity: Integration of AI and Autonomous Vehicle Validation Platforms

The integration of artificial intelligence in driving simulation presents a significant market opportunity. AI-enabled platforms can generate dynamic, adaptive scenario environments, provide real-time performance analytics, and support large-scale validation of autonomous driving algorithms. The development of multi-vehicle simulation environments and cloud-based deployment models is further democratizing access to advanced simulation, opening growth opportunities across cost-sensitive markets in Asia-Pacific, Latin America, and the Middle East.

GLP-1/GIP/Glucagon Triple Agonist Drug Market Scope

The GLP-1/GIP/Glucagon Triple Agonist Drug market is segmented on the basis of drug class, application, and distribution channel.

- By Drug Class

On the basis of drug class, the GLP-1/GIP/Glucagon Triple Agonist Drug Market is segmented into GLP-1 agonists, GIP/GLP-1 dual agonists, glucagon receptor agonists, and GLP-1/GIP/Glucagon triple agonists. The GIP/GLP-1 dual agonists segment dominated the market with a share of 52.64% in 2025 due to strong clinical validation, widespread physician adoption, and proven efficacy in improving glycemic control and inducing significant weight reduction. These therapies have become the standard of care in incretin-based metabolic treatment due to established regulatory approvals and strong commercial penetration. Pharmaceutical companies are increasingly leveraging dual agonists as a foundation for next-generation metabolic therapies. The segment benefits from strong demand in both diabetes and obesity management, supported by growing awareness of incretin biology. However, increasing R&D investments are accelerating innovation toward triple agonist molecules. Combination mechanisms targeting GLP-1, GIP, and glucagon receptors are showing superior metabolic outcomes in clinical trials. Expanding pipeline activity and strategic collaborations are strengthening market penetration. Rising prevalence of obesity and type 2 diabetes is further driving adoption. Healthcare providers prefer dual agonists due to favorable safety and efficacy profiles. Strong reimbursement support in developed regions continues to reinforce growth. Continuous product launches are expanding treatment accessibility globally.

The GLP-1/GIP/Glucagon triple agonists segment is expected to witness the fastest growth with a CAGR of 38.46% from 2026 to 2033, driven by superior multi-pathway metabolic action and strong clinical pipeline momentum. These drugs demonstrate enhanced weight reduction, improved insulin sensitivity, and better energy balance regulation compared to existing therapies. Pharmaceutical companies are heavily investing in late-stage clinical trials to validate long-term safety and efficacy. Increasing demand for next-generation obesity treatments is accelerating adoption. Expanding regulatory support for innovative metabolic drugs is further boosting development activity. Rising prevalence of severe obesity cases is creating strong unmet medical need. Advancements in peptide engineering are improving drug stability and duration of action. Strategic collaborations between biotech firms and large pharmaceutical companies are strengthening commercialization pathways. Growing focus on personalized metabolic therapies is supporting adoption. Strong investor interest in obesity drug pipelines is accelerating R&D funding. Expanding awareness of cardiometabolic risks is increasing prescription potential. This segment is expected to redefine future obesity and diabetes treatment standards.

- By Application

On the basis of application, the GLP-1/GIP/Glucagon Triple Agonist Drug Market is segmented into type 2 diabetes management, obesity management, cardiometabolic disorders, and others. The type 2 diabetes management segment dominated the market with a share of 46.18% in 2025 due to the high global burden of diabetes and widespread adoption of incretin-based therapies for glycemic control. Increasing patient population with uncontrolled blood glucose levels is driving prescription rates. Physicians prefer GLP-1 based therapies due to improved HbA1c reduction and weight benefits. Strong clinical guidelines supporting incretin therapy adoption are boosting usage. Rising awareness of diabetes complications is encouraging early treatment initiation. Hospitals and specialty clinics are key distribution points for these therapies. Expanding reimbursement coverage in developed economies supports patient access. Pharmaceutical companies are focusing on improving drug efficacy and patient adherence. Combination therapies are increasingly used for better metabolic control. Aging population trends are further contributing to demand. Lifestyle-related metabolic disorders are accelerating treatment uptake. Continuous innovation in injectable and oral formulations is improving compliance.

The obesity management segment is expected to witness the fastest growth with a CAGR of 41.72% from 2026 to 2033, driven by rapidly increasing global obesity prevalence and rising demand for effective pharmacological weight-loss solutions. GLP-1/GIP/glucagon triple agonists show strong appetite suppression and energy expenditure benefits. Growing clinical evidence supporting significant weight reduction is boosting adoption. Healthcare systems are increasingly recognizing obesity as a chronic disease requiring long-term treatment. Rising demand for non-surgical weight management therapies is accelerating prescriptions. Pharmaceutical companies are prioritizing obesity-focused drug pipelines. Expanding telehealth services are improving access to obesity treatments. Social awareness of metabolic health is increasing patient willingness to seek treatment. Clinical trials are demonstrating superior efficacy over existing therapies. Government initiatives promoting obesity prevention are supporting market expansion. Increasing healthcare expenditure is enabling broader treatment access. This segment is expected to become the dominant long-term revenue driver.

- By Distribution Channel

On the basis of distribution channel, the GLP-1/GIP/Glucagon Triple Agonist Drug Market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. The hospital pharmacies segment dominated the market with a share of 54.33% in 2025 due to high patient inflow for diabetes and obesity management treatments. Hospitals serve as primary prescription points for advanced injectable therapies. Physicians prefer initiating incretin-based therapies under clinical supervision. Availability of specialized endocrinology departments supports strong adoption. Hospital pharmacies ensure proper dose administration and monitoring. Strong procurement systems in hospitals improve drug availability. Increasing hospital admissions for metabolic disorders is driving demand. Reimbursement frameworks are more structured in hospital settings. Pharmaceutical companies prioritize hospital distribution channels for new launches. Clinical trial-linked prescriptions are concentrated in hospitals. High trust in hospital-based treatment enhances patient compliance. Advanced storage and handling infrastructure supports biologic drug distribution.

The online pharmacies segment is expected to witness the fastest growth with a CAGR of 44.28% from 2026 to 2033, driven by rising digital healthcare adoption and increasing preference for home delivery of chronic disease medications. Telemedicine expansion is enabling remote prescriptions for metabolic drugs. Patients are increasingly shifting toward convenient and discreet purchasing channels. Improved cold-chain logistics are supporting safe delivery of biologics. Digital pharmacy platforms are expanding access in urban and semi-urban regions. Growing smartphone penetration is enhancing online ordering adoption. Subscription-based drug delivery models are improving patient adherence. Regulatory support for e-pharmacy expansion is increasing accessibility. Pharmaceutical companies are partnering with online platforms for distribution. Rising healthcare digitalization is reducing dependency on physical pharmacies. Cost-effective pricing models are attracting patients. This segment is rapidly transforming drug accessibility globally.

GLP-1/GIP/Glucagon Triple Agonist Drug Market Regional Analysis

North America dominated the GLP-1/GIP/Glucagon Triple Agonist Drug Market with the largest revenue share of 39.26% in 2025, supported by high obesity and type 2 diabetes prevalence, strong penetration of advanced biologic therapies, early adoption of next-generation incretin-based drugs, and robust reimbursement frameworks. The region also benefits from a strong presence of leading pharmaceutical companies and active clinical trial pipelines for multi-agonist therapies targeting metabolic disorders. The increasing burden of obesity and cardiometabolic diseases, combined with strong healthcare spending and rapid uptake of innovative GLP-1-based therapies, continues to reinforce North America’s leadership position. Expanding use of combination incretin therapies and growing physician preference for highly effective weight management drugs are further supporting market growth.

U.S. GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The U.S. GLP-1/GIP/Glucagon Triple Agonist Drug market is witnessing strong growth, driven by rapid adoption of advanced obesity and diabetes treatments, high awareness of metabolic health therapies, and strong clinical pipeline activity. Pharmaceutical companies in the U.S. are leading global development of multi-agonist drugs, supported by extensive R&D investments and large-scale clinical trials. The country’s high obesity prevalence and increasing demand for long-term weight management solutions are significantly boosting uptake of GLP-1 and next-generation triple agonist therapies. In addition, strong insurance coverage and reimbursement support are accelerating patient access to these high-cost biologic treatments.

Europe GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The Europe GLP-1/GIP/Glucagon Triple Agonist Drug market remains a major contributor to global revenue, supported by strong healthcare systems, rising prevalence of obesity and type 2 diabetes, and increasing adoption of innovative metabolic therapies. The region is witnessing growing clinical interest in multi-agonist incretin-based treatments across endocrinology and obesity care. Increasing investments in precision medicine, expanding access to advanced biologics, and supportive regulatory frameworks are driving adoption across major European countries. Collaboration between pharmaceutical companies and research institutions is further strengthening the development of next-generation metabolic therapies.

U.K. GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The U.K. GLP-1/GIP/Glucagon Triple Agonist Drug market is experiencing steady growth, supported by increasing prevalence of obesity and diabetes, strong healthcare infrastructure, and growing adoption of innovative biologic therapies. The National Health Service (NHS) plays a key role in improving access to advanced metabolic treatments. Rising focus on preventive healthcare, early intervention in obesity management, and growing clinical research activities are further supporting market expansion in the U.K.

Germany GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The Germany GLP-1/GIP/Glucagon Triple Agonist Drug market is expanding steadily, driven by strong pharmaceutical manufacturing capabilities, advanced clinical research infrastructure, and rising burden of metabolic disorders. Germany is witnessing increasing adoption of GLP-1-based therapies in both hospital and specialty care settings. Strong regulatory frameworks, high healthcare expenditure, and growing focus on obesity management programs are supporting continued market growth in the country.

Asia-Pacific GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

Asia-Pacific is expected to be the fastest-growing region in the GLP-1/GIP/Glucagon Triple Agonist Drug Market, registering a CAGR of 12.4% from 2026 to 2033, fueled by rising prevalence of obesity and diabetes, increasing healthcare access, expanding pharmaceutical manufacturing capabilities, and growing adoption of advanced metabolic disorder treatments across China, India, Japan, and South Korea. The region is experiencing rapid healthcare modernization, improving diagnosis rates for metabolic diseases, and increasing availability of innovative biologic therapies. Growing investments from global pharmaceutical companies and expanding clinical trial activity are further accelerating regional market growth.

Japan GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The Japan GLP-1/GIP/Glucagon Triple Agonist Drug market is witnessing consistent growth, driven by an aging population, rising incidence of type 2 diabetes, and strong healthcare infrastructure. Japan is increasingly adopting advanced metabolic therapies for long-term chronic disease management. Strong clinical research capabilities and early adoption of innovative biologic treatments are supporting market expansion in the country.

China GLP-1/GIP/Glucagon Triple Agonist Drug Market Insight

The China GLP-1/GIP/Glucagon Triple Agonist Drug market is growing rapidly, supported by rising prevalence of obesity and diabetes, expanding healthcare infrastructure, and increasing access to advanced pharmaceutical therapies. Government initiatives aimed at improving chronic disease management are also supporting adoption. China’s growing pharmaceutical manufacturing ecosystem and increasing participation in global clinical trials are positioning it as a key high-growth market for next-generation incretin therapies.

GLP-1/GIP/Glucagon Triple Agonist Drug Market Share

The GLP-1/GIP/Glucagon Triple Agonist Drug industry is primarily led by well-established companies, including:

- Eli Lilly and Company (U.S.)

- Novo Nordisk A/S (Denmark)

- AstraZeneca plc (UK)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- Sanofi S.A. (France)

- Boehringer Ingelheim (Germany)

- Roche Holding AG (Switzerland)

- Merck & Co., Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Viking Therapeutics, Inc. (U.S.)

- Zealand Pharma A/S (Denmark)

- Structure Therapeutics Inc. (U.S.)

- Terns Pharmaceuticals, Inc. (U.S.)

- Altimmune, Inc. (U.S.)

- Biomea Fusion, Inc. (U.S.)

- Hanmi Pharmaceutical Co., Ltd. (South Korea)

- Jiangsu Hengrui Pharmaceuticals Co., Ltd. (China)

- Innovent Biologics, Inc. (China)

- Sino Biopharmaceutical Limited (China)

- Ascletis Pharma Inc. (China)

- Rhythm Pharmaceuticals, Inc. (U.S.)

- Lexicon Pharmaceuticals, Inc. (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Bristol Myers Squibb (U.S.)

Latest Developments in GLP-1/GIP/Glucagon Triple Agonist Drug Market

- In May 2022, Eli Lilly and Company announced FDA approval of Mounjaro (tirzepatide), the first dual GIP and GLP-1 receptor agonist for the treatment of type 2 diabetes. This landmark approval marked the beginning of next-generation incretin-based therapies and laid the clinical foundation for future triple agonist development targeting GLP-1, GIP, and glucagon receptors

- In October 2022, Eli Lilly published Phase 1b clinical trial results for retatrutide (LY3437943), a first-in-class triple agonist targeting GLP-1, GIP, and glucagon receptors. The study demonstrated significant improvements in glycemic control and substantial weight reduction, establishing proof-of-concept for triple receptor agonism in metabolic disease management

- In November 2024, Amgen announced Phase 2 clinical data for its investigational obesity drug maridebart cafraglutide (MariTide), a long-acting incretin-based therapy targeting GLP-1 and GIP pathways. The study showed strong and sustained weight reduction over 52 weeks, intensifying competition in next-generation multi-agonist metabolic therapies, including triple agonist programs

- In February 2024, Viking Therapeutics reported positive Phase 2 results for VK2735, a dual GLP-1/GIP receptor agonist demonstrating statistically significant weight loss versus placebo. The findings reinforced strong clinical and commercial interest in multi-receptor incretin therapies and accelerated development pipelines toward more advanced triple agonist mechanisms

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.