Global Glucose Analyzer Devices Market

Market Size in USD Billion

USD

16.62 Billion

USD

29.64 Billion

2025

2033

USD

16.62 Billion

USD

29.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 16.62 Billion | |

| USD 29.64 Billion | |

| % | |

|

Glucose Analyzer Devices Market Overview

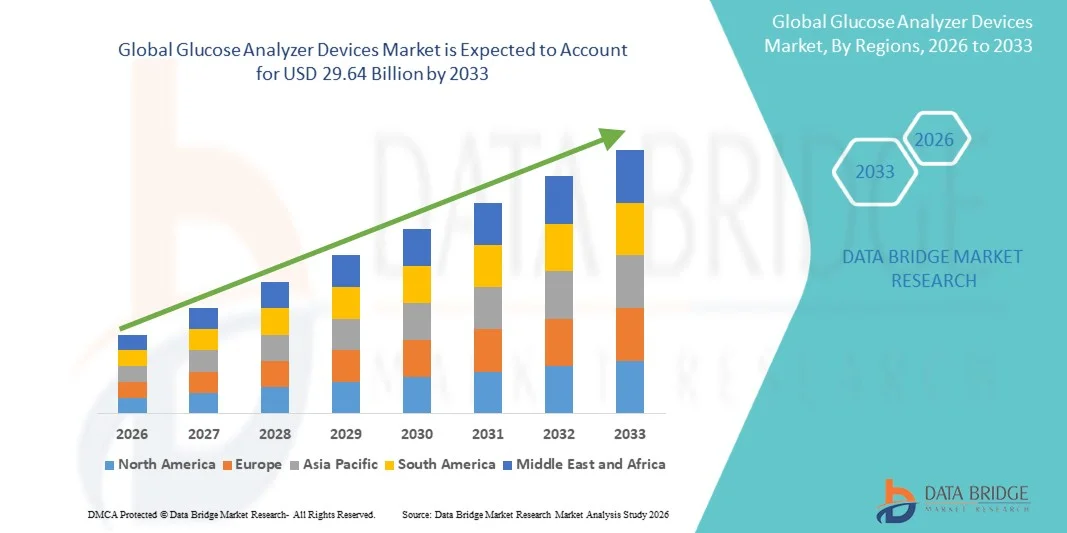

The Glucose Analyzer Devices Market was valued at USD 16.62 billion in 2025 and is projected to reach USD 29.64 billion by 2033, growing at a CAGR of 7.50% from 2026 to 2033. The Glucose Analyzer Devices Market is experiencing consistent growth driven by the rising prevalence of diabetes and increasing demand for rapid, accurate, and point-of-care glucose monitoring solutions. Expanding awareness about early disease diagnosis and continuous glucose monitoring (CGM) is further accelerating adoption across hospitals, diagnostic laboratories, home care settings, and specialty clinics. Technological advancements in biosensors, strip-based analyzers, and continuous monitoring systems are also enhancing accuracy, portability, and real-time data tracking capabilities.

The increasing global burden of diabetes, particularly type 1 and type 2 diabetes, along with a growing geriatric population and lifestyle-related metabolic disorders, is driving strong demand for glucose analyzer devices. Governments and healthcare organizations are promoting routine glucose screening programs and preventive healthcare initiatives to reduce diabetes-related complications. In addition, the shift toward home-based monitoring, integration of digital health platforms, and adoption of connected glucose monitoring devices are replacing traditional testing methods in many markets, offering faster results, improved patient compliance, and better long-term disease management.

Key Market Trends & Insights

- North America dominated the Glucose Analyzer Devices Market with the largest revenue share of 39.48% in 2025, supported by advanced healthcare infrastructure, high prevalence of diabetes, strong adoption of point-of-care (POC) diagnostic devices, and widespread availability of home-based glucose monitoring solutions. The region benefits from high healthcare expenditure, strong reimbursement frameworks, and increasing integration of digital diabetes management solutions such as connected glucose monitoring systems.

- The Blood segment dominated the market with a 92.1% share in 2025 due to its high diagnostic accuracy and strong clinical validation across healthcare systems. Blood-based glucose testing remains the gold standard for diabetes monitoring and management.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by the rapidly increasing diabetic population, improving healthcare infrastructure, rising awareness of early disease diagnosis, and expanding adoption of affordable point-of-care glucose monitoring devices across China, India, and Japan. Government initiatives supporting diabetes screening programs and expanding access to diagnostic services are further accelerating regional growth.

- The Blood sample segment dominated the market with a 78.36% revenue share in 2025, as blood-based glucose testing remains the clinical standard for accurate diabetes diagnosis and monitoring. Increasing adoption of capillary blood testing in home care and hospital settings continues to support strong demand for blood-based glucose analyzer devices.

Market Size & Forecast

- Global Market Value (2025): USD 16.62 Billion

- Expected Market Value (2033): USD 29.64 Billion

- Forecast CAGR (2026–2033): 7.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Glucose Analyzer Devices Market Segmentation

|

Attributes |

Glucose Analyzer Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Roche Diagnostics (Switzerland) |

|

Market Opportunities |

· Expansion of Continuous Glucose Monitoring (CGM) and Digital Health Integration · Growth of Home-Based and Point-of-Care Testing Solutions · Expansion in Emerging Markets and Preventive Healthcare Programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Glucose Analyzer Devices Market Trends

Trend: Rising Adoption of Digital and Connected Glucose Monitoring Systems

The Glucose Analyzer Devices Market is witnessing strong growth driven by the increasing shift toward connected and digital diabetes management solutions. Modern glucose analyzers are now integrated with mobile applications and cloud-based platforms, enabling real-time blood glucose tracking, trend analysis, and remote patient monitoring. For instance, continuous glucose monitoring (CGM) systems are increasingly being adopted in developed healthcare systems, with studies showing that CGM usage can improve glycemic control and reduce HbA1c levels by 0.5–1.0% in diabetic patients, supporting better long-term disease management. The rising prevalence of diabetes—affecting over 530 million adults globally—is significantly accelerating demand for advanced glucose monitoring technologies.

Glucose Analyzer Devices Market Dynamics

Key Market Driver: Rising Global Burden of Diabetes and Demand for Point-of-Care Testing

The increasing prevalence of diabetes is a major factor driving the growth of glucose analyzer devices worldwide. Growing sedentary lifestyles, obesity rates, and aging populations are contributing to a surge in Type 1 and Type 2 diabetes cases, increasing the need for frequent blood glucose monitoring. For instance, the International Diabetes Federation estimates that diabetes cases are projected to exceed 640 million by 2030, creating sustained demand for both handheld and benchtop glucose analyzers. Hospitals, clinics, and home care settings are increasingly adopting point-of-care (POC) glucose testing devices to enable rapid diagnosis, real-time monitoring, and improved treatment outcomes. In addition, rising awareness programs and government-led diabetes screening initiatives in countries such as the U.S., India, and China are further boosting adoption of glucose monitoring devices.

Key Restraint/Challenge: Accuracy Limitations and Device Cost Barriers in Low-Income Regions

A key challenge in the Glucose Analyzer Devices Market is the accuracy variability between different device types and testing environments, particularly in low-cost handheld analyzers used in home care settings. Improper usage and calibration issues can lead to inconsistent readings, affecting clinical decision-making.

In addition, the relatively high cost of advanced continuous glucose monitoring systems limits adoption in low- and middle-income countries. Despite improving affordability, many patients still rely on traditional blood glucose meters due to reimbursement limitations and lack of insurance coverage for advanced monitoring systems.

Key Market Opportunity: Expansion of Home-Based Diabetes Management and AI-Enabled Monitoring

The growing shift toward home-based healthcare presents a significant opportunity for glucose analyzer device manufacturers. Increasing preference for self-monitoring of blood glucose (SMBG) is driving demand for portable, user-friendly devices that provide instant readings and seamless smartphone connectivity.

For instance, adoption of home glucose monitoring has increased significantly in recent years, particularly in urban populations managing chronic diabetes conditions. AI-powered glucose tracking systems are also emerging, capable of predicting glucose fluctuations and providing personalized dietary and insulin recommendations. In addition, expanding telemedicine infrastructure—especially in North America and Asia-Pacific—is enabling remote diabetes management, improving patient adherence and reducing hospital visits, thereby supporting long-term market expansion.

Glucose Analyzer Devices Market Scope

The Glucose Analyzer Devices market is segmented on the basis of product type, sample, and end user.

- By Product Type

On the basis of product type, the Glucose Analyzer Devices Market is segmented into Handheld POC Glucose Analyzer and Benchtop POC Glucose Analyzer. The Handheld POC Glucose Analyzer segment dominated the market with a 58.4% share in 2025 due to rising demand for portable, rapid, and user-friendly glucose monitoring solutions. Increasing prevalence of diabetes and strong shift toward home-based testing are significantly driving adoption. These devices are widely preferred in emergency care, ambulatory settings, and patient self-monitoring due to quick results and ease of use. Growing awareness regarding early disease detection and continuous glucose monitoring is further strengthening market penetration. Integration with digital health platforms and mobile connectivity is improving real-time tracking. Hospitals and clinics also use handheld analyzers for fast bedside testing. Technological advancements in sensor accuracy are enhancing reliability. Lower cost compared to benchtop systems is increasing accessibility in emerging markets. Expanding diabetic population globally is a major demand driver. Rising preventive healthcare initiatives are supporting growth. Increasing focus on patient convenience is boosting adoption. Overall, portability and affordability are key factors sustaining dominance of this segment.

The Benchtop POC Glucose Analyzer segment is expected to witness the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for high-precision laboratory testing and advanced diagnostic workflows. These systems offer superior analytical accuracy and high throughput capabilities, making them ideal for hospitals and diagnostic laboratories. Rising hospitalization rates for diabetes-related complications are supporting adoption. Integration with laboratory information management systems (LIMS) is improving workflow efficiency. Growing demand for centralized diagnostic solutions is boosting usage. Increasing focus on quality control and accuracy is driving preference for benchtop systems. Technological advancements are improving processing speed and automation. Expansion of diagnostic centers in emerging economies is supporting demand. Rising healthcare infrastructure investments are further accelerating growth. Demand for multi-sample processing is increasing efficiency. Clinical research applications are expanding usage scope. Overall, accuracy and scalability are key growth drivers for this segment.

- By Sample

On the basis of sample, the Glucose Analyzer Devices Market is segmented into Blood and Saliva. The Blood segment dominated the market with a 92.1% share in 2025 due to its high diagnostic accuracy and strong clinical validation across healthcare systems. Blood-based glucose testing remains the gold standard for diabetes monitoring and management. It is widely used in hospitals, clinics, and home care settings. Strong regulatory approval and established testing protocols support dominance. Increasing diabetic population is driving continuous demand. High reliability and precision make it preferred by healthcare professionals. Integration with point-of-care devices enhances usability. Routine screening programs globally rely on blood-based testing. Emergency care settings extensively use blood glucose analyzers. Technological advancements are improving strip-based and sensor accuracy. Strong reimbursement frameworks in developed regions support adoption. Overall, clinical trust and accuracy sustain its leading position.

The Saliva segment is expected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by rising demand for non-invasive and pain-free diagnostic methods. Increasing research in biosensor technology is enabling accurate saliva-based glucose detection. Growing preference for user-friendly testing solutions is supporting adoption. Expanding focus on preventive healthcare is boosting demand. Saliva testing eliminates the need for blood sampling, improving patient comfort. Rising pediatric and geriatric patient demand is accelerating usage. Technological innovations in nano-sensors are enhancing feasibility. Increasing investment in alternative diagnostic biomarkers is supporting growth. Home healthcare adoption is further driving demand. Integration with wearable health devices is expanding applications. Growing awareness of non-invasive monitoring is boosting acceptance. Overall, convenience and innovation are key growth drivers.

- By End User

On the basis of end user, the Glucose Analyzer Devices Market is segmented into Hospitals, Office Based Setting, Home Care Setting, Clinics, Ambulatory Surgical Centers, and Others. The Hospitals segment dominated the market with a 38.6% share in 2025 due to high patient inflow and availability of advanced diagnostic infrastructure. Hospitals serve as primary centers for diabetes diagnosis and emergency glucose testing. Increasing prevalence of chronic diseases is driving demand. Strong presence of skilled healthcare professionals supports adoption. Integration with hospital information systems improves workflow efficiency. Rising admissions for diabetes complications is boosting usage. Availability of advanced point-of-care devices enhances testing speed. Government healthcare funding supports hospital infrastructure. Increasing focus on early diagnosis and monitoring is strengthening demand. Hospitals also conduct routine screening programs. Strong reimbursement policies in developed markets support adoption. Overall, hospitals remain the central hub for glucose testing services.

The Home Care Setting segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by increasing adoption of self-monitoring devices and rising demand for remote healthcare solutions. Growing diabetic population is encouraging home-based glucose monitoring. Expansion of telemedicine platforms is supporting connected glucose devices. Rising healthcare costs are shifting care toward home settings. Technological advancements in portable analyzers are improving usability. Increasing awareness of self-care management is boosting adoption. Integration with mobile apps and cloud platforms is enabling real-time tracking. Elderly population growth is further supporting demand. COVID-era healthcare behavioral shifts continue to influence adoption. Insurance support for home monitoring devices is expanding usage. Convenience and affordability are key drivers. Overall, digital health integration is accelerating growth in this segment.

Glucose Analyzer Devices Market Regional Analysis

North America dominated the Glucose Analyzer Devices market and accounted for the largest revenue share of 39.48% in 2025, supported by advanced healthcare infrastructure, high prevalence of diabetes, strong adoption of point-of-care (POC) glucose monitoring devices, and widespread availability of home-based and hospital-integrated diagnostic solutions. The region also benefits from high healthcare expenditure, strong reimbursement frameworks, and increasing integration of digital diabetes management systems, including connected glucose monitoring platforms and AI-enabled glucose tracking applications that improve real-time disease monitoring and patient outcomes.

U.S. Glucose Analyzer Devices Market Insight

The U.S. Glucose Analyzer Devices market is witnessing strong growth due to rising diabetes prevalence, increasing investments in point-of-care diagnostics, and rapid adoption of digital health technologies. The country’s advanced healthcare system, strong presence of leading diagnostic device manufacturers, and growing use of continuous and self-monitoring glucose analyzers are driving demand across hospitals, clinics, and home care settings. In addition, increasing focus on preventive healthcare and early disease detection is accelerating the adoption of advanced glucose monitoring solutions across both urban and rural populations.

Europe Glucose Analyzer Devices Market Insight

The Europe Glucose Analyzer Devices market remains a major contributor to global revenue, driven by strong healthcare systems, government-supported diabetes screening programs, and high awareness regarding early disease diagnosis. The region benefits from widespread use of advanced diagnostic devices in hospitals and specialty clinics, along with increasing adoption of portable glucose analyzers for outpatient and home-based monitoring. Rising investments in digital healthcare infrastructure and growing integration of connected medical devices continue to strengthen market expansion across Europe.

U.K. Glucose Analyzer Devices Market Insight

The U.K. Glucose Analyzer Devices market is experiencing steady growth, supported by increasing diabetes prevalence, strong National Health Service (NHS) screening programs, and growing adoption of point-of-care testing devices. Rising demand for rapid diagnostic solutions in primary care settings and increasing use of portable glucose analyzers for home monitoring are contributing to market growth. Furthermore, integration of digital health platforms and remote patient monitoring solutions is improving diabetes management efficiency across the country.

Germany Glucose Analyzer Devices Market Insight

The Germany Glucose Analyzer Devices market is expanding steadily due to its strong healthcare infrastructure, high adoption of advanced diagnostic technologies, and increasing burden of diabetes and metabolic disorders. Hospitals, diagnostic laboratories, and specialty clinics are increasingly using automated and portable glucose analyzers for accurate and rapid testing. Continuous advancements in biosensor technologies and strong focus on precision medicine are further driving market growth in Germany.

Asia-Pacific Glucose Analyzer Devices Market Insight

The Asia-Pacific Glucose Analyzer Devices market is expected to witness rapid growth, driven by a rising diabetic population, improving healthcare infrastructure, and increasing awareness of early disease detection across countries such as China, India, and Japan. Expanding access to affordable diagnostic devices, growing government-led diabetes screening initiatives, and rising adoption of point-of-care glucose monitoring systems are supporting regional market expansion. In addition, increasing investments in healthcare modernization and digital health technologies are accelerating market growth across both urban and rural areas.

Japan Glucose Analyzer Devices Market Insight

The Japan Glucose Analyzer Devices market is witnessing consistent growth due to a rapidly aging population, increasing prevalence of diabetes, and strong healthcare system adoption of advanced diagnostic technologies. Hospitals and clinics are increasingly integrating automated glucose monitoring systems to improve chronic disease management. Moreover, rising adoption of home-based glucose monitoring devices and digital health solutions is supporting long-term market expansion.

China Glucose Analyzer Devices Market Insight

the China glucose analyzer devices market is growing rapidly, driven by increasing diabetes prevalence, expanding healthcare infrastructure, and rising government focus on chronic disease management. growing adoption of point-of-care glucose analyzers in hospitals and clinics, along with increasing availability of affordable home-use monitoring devices, is significantly boosting market demand. in addition, rising healthcare investments, improved diagnostic accessibility, and rapid technological advancements in medical devices are positioning China as one of the fastest-growing markets globally.

Glucose Analyzer Devices Market Share

The Glucose Analyzer Devices industry is primarily led by well-established companies, including:

- Moog Inc. (U.S.)

- Dallara (Italy)

- Exail (France)

- IPG Automotive GmbH (Germany)

- aiMotive (Hungary)

- VI‑grade GmbH (Germany)

- Cruden B.V. (Netherlands)

- Dynisma Ltd. (UK)

- Applied Intuition Inc. (U.S.)

- rFpro (rFpro Limited) (England)

- Siemens AG (Germany)

- Dassault Systèmes SE (France)

- MTS Systems Corporation (U.S.)

- CAE Inc. (Canada)

- NVIDIA Corporation (U.S.)

- AB Dynamics PLC (U.K.)

- Forum8 (Japan)

- Mitsubishi Precision Co., Ltd. (Japan)

- FAAC Incorporated (U.S.)

- DriveSafety (U.S.)

- Simtec Simulation Technology GmbH (Germany)

- MB Dynamics Inc. (U.S.)

- Sanlab Simulation (India)

- SimCraft (U.S.)

- CXC Simulations (U.S.)

- XPI Simulation (United Kingdom)

- Tecknotrove Simulator Systems Pvt. Ltd. (India)

- Zhejiang Kechi Intelligent Technology Co., Ltd. (China)

- Shenzhen Zhongzhi Simulation (China)

- Hindustan Simulators (India)

- DriveSimSolutions (U.S.)

- Teksim Technologies (India)

- iMVR Inc. (U.S.)

- SimXperience (U.S.)

Latest Developments in Glucose Analyzer Devices Market

- In February 2022, Senseonics announced that the Eversense E3 continuous glucose monitoring (CGM) system received FDA approval in the United States, featuring an implantable long-term sensor with up to 180-day wear time. The system was designed to improve long-term glucose monitoring accuracy and reduce the need for frequent sensor replacements. This approval strengthened innovation in minimally invasive glucose monitoring technologies and expanded options for diabetes management

- In April 2022, Abbott received U.S. FDA clearance for its FreeStyle Libre 3 system, the world’s smallest and thinnest continuous glucose monitoring device. The system delivers real-time glucose readings directly to smartphones every minute without scanning. This launch significantly advanced wearable glucose monitoring technology by improving accuracy, comfort, and digital integration for diabetic patients

- In December 2022, Dexcom announced U.S. FDA clearance for its Dexcom G7 CGM system, featuring a smaller, more accurate, and fully disposable design. The device offers faster warm-up time and improved connectivity with digital health platforms. This development marked a major advancement in real-time glucose monitoring and strengthened Dexcom’s position in the global CGM market

- In April 2023, Medtronic received FDA clearance for expanded interoperability of its Guardian 4 CGM sensor as part of its MiniMed 780G automated insulin delivery system ecosystem. The update improved algorithm-driven insulin dosing accuracy and reduced the need for fingerstick calibration. This development enhanced closed-loop diabetes management and strengthened integration between glucose monitoring and insulin delivery systems

- In June 2023, Roche announced enhancements to its Accu-Chek SmartGuide predictive glucose monitoring ecosystem, focusing on digital connectivity and improved data analytics for diabetes management. The system integrates predictive algorithms to help patients anticipate glucose fluctuations. This advancement supported Roche’s strategy to expand digital diabetes care solutions and improve patient self-management

- In January 2024, Abbott expanded global availability of its FreeStyle Libre continuous glucose monitoring portfolio, including Libre 2 and Libre 3 systems across additional international markets. The expansion focused on increasing access to affordable CGM technology and strengthening digital diabetes care adoption in emerging economies. This move further reinforced Abbott’s leadership in wearable glucose monitoring technologies

- In March 2025, Dexcom expanded its next-generation CGM ecosystem with enhanced AI-driven glucose insights and predictive analytics integration across connected health platforms. The update focused on improving personalized diabetes management through real-time data interpretation and mobile health integration. This development highlighted the increasing role of AI and digital ecosystems in glucose monitoring innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.