Global Glucose Meters Market

Market Size in USD Billion

USD

14.00 Billion

USD

30.44 Billion

2025

2033

USD

14.00 Billion

USD

30.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.00 Billion | |

| USD 30.44 Billion | |

| % | |

|

Glucose Meters Market Size

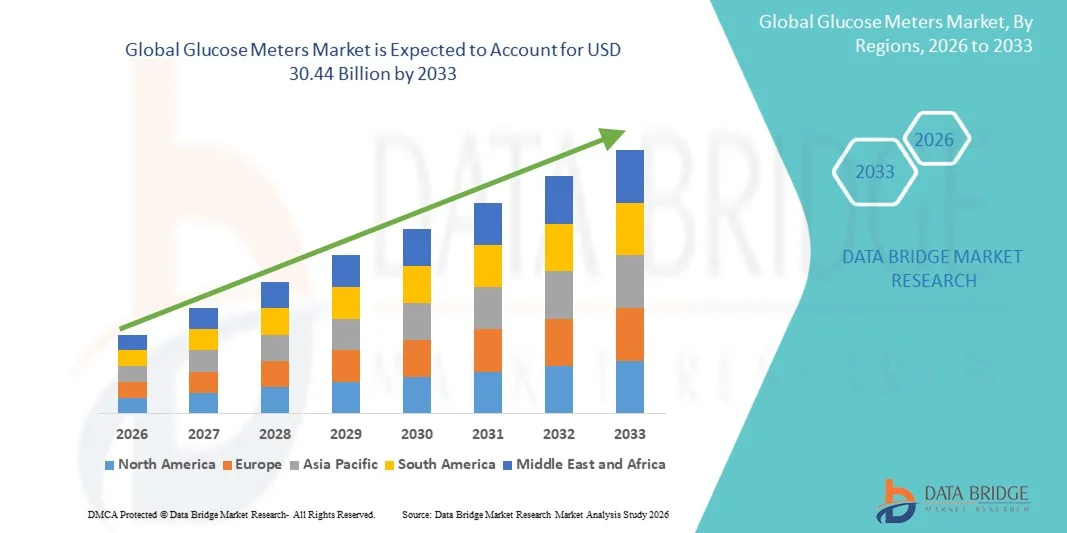

- The global Glucose Meters market size was valued at USD 14.00 billion in 2025 and is expected to reach USD 30.44 billion by 2033, at a CAGR of 10.20% during the forecast period

- The market growth is largely fueled by the increasing prevalence of diabetes and other blood glucose-related disorders, coupled with growing awareness among patients about the importance of regular blood sugar monitoring. Technological advancements in portable, digital, and continuous glucose monitoring devices are further driving adoption across both homecare and clinical settings

- Furthermore, rising consumer demand for accurate, easy-to-use, and connected glucose monitoring devices is positioning glucose meters as a preferred solution for proactive diabetes management. These converging factors are accelerating the uptake of Glucose Meters solutions, thereby significantly boosting the industry's growth

Glucose Meters Market Analysis

- Glucose meters, providing rapid and accurate blood glucose measurement, are increasingly essential tools for diabetes management in both home and clinical settings due to their convenience, portability, and integration with digital health platforms

- The escalating demand for glucose meters is primarily fueled by the growing prevalence of diabetes worldwide, rising awareness about self-monitoring, and the adoption of connected healthcare devices that allow patients to track and manage their blood sugar levels efficiently

- North America dominated the glucose meters market with the largest revenue share of 39.6% in 2025, driven by high diabetes prevalence, strong healthcare infrastructure, widespread adoption of advanced glucose monitoring devices, and the presence of leading market players in the U.S.

- Asia-Pacific is expected to be the fastest growing region in the glucose meters market during the forecast period due to the rapidly increasing diabetic population, improving healthcare access, rising awareness of glucose monitoring, and growing adoption of cost-effective diagnostic devices in emerging economies

- The invasive segment dominated the largest market revenue share of around 72.1% in 2025, driven by its proven accuracy and long-standing clinical acceptance

Report Scope and Glucose Meters Market Segmentation

|

Attributes |

Glucose Meters Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Glucose Meters Market Trends

“Enhanced Convenience and Accuracy in Home Glucose Monitoring”

- A significant and accelerating trend in the global glucose meters market is the growing emphasis on accuracy, ease of use, and seamless integration with personal health management routines. This trend is significantly enhancing patient self-monitoring and disease management capabilities

- For instance, modern glucose meters now feature rapid test results, smaller blood sample requirements, and user-friendly interfaces, allowing individuals to efficiently monitor their blood sugar levels at home or on the go

- The integration of digital record-keeping and mobile app connectivity allows users to track trends, set reminders, and share data with healthcare providers, enhancing proactive disease management and personalized care

- Advancements in sensor technology and test strip design have improved the precision and reliability of glucose meters, making them essential tools for both Type 1 and Type 2 diabetes management

- The market is witnessing the development of compact, portable, and ergonomic designs that cater to diverse user needs, promoting regular and consistent monitoring

- Companies are also focusing on affordability and accessibility, ensuring that glucose meters are available across different regions and income groups, thereby expanding the user base

- The growing awareness of diabetes, coupled with the rise in lifestyle-related health issues, continues to drive demand for home-based glucose monitoring solution

- The market’s expansion is supported by continuous product innovations, regulatory approvals, and partnerships between device manufacturers and healthcare providers, ensuring that users have access to reliable and convenient monitoring solutions

Glucose Meters Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Diabetes and Home Monitoring”

- The increasing prevalence of diabetes worldwide, coupled with rising awareness of the importance of regular blood glucose monitoring, is a significant driver for the heightened demand for home glucose meters

- For instance, in April 2024, major healthcare companies launched updated home glucose monitoring kits with enhanced accuracy, faster readings, and mobile connectivity features. Such innovations are expected to drive Glucose Meters market growth in the forecast period

- As patients seek more convenient and reliable ways to monitor their blood sugar levels, modern glucose meters provide easy-to-use interfaces, rapid test results, and integration with mobile applications, enabling proactive diabetes management at homeFurthermore, the trend of self-care and home-based healthcare has increased the adoption of these devices, as patients prefer avoiding frequent hospital visits for routine glucose checks

- The ability to track trends, set reminders, and share readings directly with healthcare providers enhances patient compliance and supports personalized treatment plans, driving market growth

- The demand for compact, portable, and user-friendly glucose meters that require minimal blood samples has further contributed to market expansion, particularly among elderly patients and individuals with limited mobility

Restraint/Challenge

“Concerns Regarding Accuracy, Cost, and Regulatory Compliance”

- Concerns regarding measurement accuracy and reliability of certain glucose meters can pose challenges to broader market adoption, as patients rely heavily on precise readings for insulin dosing and lifestyle adjustments

- In addition, high-quality glucose meters with advanced features such as Bluetooth connectivity, memory storage, or integration with health apps often come at a premium price, which can be a barrier for price-sensitive consumers in developing regions

- Regulatory approvals, quality certifications, and adherence to medical device standards are critical to gaining consumer trust, and any delays in these processes can slow product launches and market penetration

- Despite decreasing prices for basic glucose meters, the perceived premium for technologically advanced models can still limit widespread adoption among certain population segments

- Overcoming these challenges through enhanced accuracy, affordable pricing strategies, and regulatory compliance, along with increased awareness campaigns about the benefits of home glucose monitoring, will be vital for sustained market growth

- Integration with telehealth platforms and mobile health applications can further enhance user experience, supporting adherence, and long-term market expansion

Glucose Meters Market Scope

The market is segmented on the basis of product, type, technique, ergonomics, distribution channel, application, and end-user.

• By Product

On the basis of product, the Glucose Meters market is segmented into continuous glucose monitoring (CGM) devices and self-monitoring blood glucose (SMBG) systems. The SMBG systems segment dominated the largest market revenue share of around 58.4% in 2025, driven by its affordability, ease of use, and widespread adoption across both developed and emerging economies. SMBG devices remain the first-line monitoring tool for diabetic patients due to their reliability and accessibility. Rising global diabetes prevalence is strongly boosting demand. Increasing awareness of self-care management is supporting growth. Hospitals and homecare users widely prefer SMBG systems. Availability of low-cost test strips is further strengthening adoption. Expanding pharmacy and retail penetration is improving access. Technological improvements are enhancing accuracy and usability. Growing elderly diabetic population is contributing significantly to demand. Strong physician recommendation continues to support market dominance. Government screening programs are increasing usage rates.

The CGM devices segment is expected to witness the fastest CAGR of around 11.9% from 2026 to 2033, driven by rising demand for real-time and continuous glucose monitoring solutions. Increasing adoption of wearable healthcare technologies is boosting expansion. CGM systems eliminate frequent finger-prick testing, improving patient compliance. Growing preference for digital health ecosystems is accelerating adoption. Rising Type 1 diabetes cases are supporting demand. Integration with smartphones and insulin pumps is enhancing functionality. Advancements in sensor accuracy and miniaturization are improving performance. Expanding telehealth and remote monitoring trends are driving usage. Increasing healthcare digitization is strengthening adoption. Rising awareness of preventive diabetes management is further fueling growth.

• By Type

On the basis of type, the glucose meters market is segmented into photoelectric blood glucose meters and electrode-type blood glucose meters. The electrode-type segment dominated the largest market revenue share of around 64.7% in 2025, driven by its high accuracy, fast response time, and strong clinical reliability. These devices are widely used in hospitals and homecare environments. Rising diabetes prevalence globally is supporting strong demand. Electrochemical sensing technology ensures precise glucose measurement. Ease of use and portability are boosting adoption. Strong compatibility with widely available test strips is enhancing usage. Expanding healthcare infrastructure is improving accessibility. Increasing patient awareness about glucose monitoring is driving demand. Continuous technological innovation is strengthening product efficiency. Cost-effectiveness compared to advanced systems is further supporting dominance.

The photoelectric segment is expected to witness the fastest CAGR of around 10.8% from 2026 to 2033, driven by advancements in optical and non-invasive glucose sensing technologies. Rising demand for painless monitoring solutions is fueling growth. Increasing R&D investment is improving device accuracy and reliability. Growing adoption in wearable health devices is supporting expansion. Integration with mobile applications is enhancing usability. Rising preference for non-invasive testing methods is accelerating demand. Expanding digital health ecosystem is boosting adoption. Increasing focus on patient comfort is driving usage. Technological innovation in biosensors is strengthening market growth.

• By Technique

On the basis of technique, the glucose meters market is segmented into invasive and non-invasive methods. The invasive segment dominated the largest market revenue share of around 72.1% in 2025, driven by its proven accuracy and long-standing clinical acceptance. Finger-prick testing remains the most widely used glucose monitoring method globally. Increasing diabetic population is boosting demand. Low cost and easy availability of devices are supporting adoption. Strong physician trust in invasive methods is reinforcing usage. High reliability in real-time readings is driving preference. Expanding home-based monitoring is supporting growth. Widespread availability of SMBG systems is strengthening dominance. Government health programs are increasing awareness and usage.

The non-invasive segment is expected to witness the fastest CAGR of around 13.2% from 2026 to 2033, driven by rising demand for painless and continuous glucose monitoring solutions. Increasing adoption of wearable biosensors is fueling growth. Technological advancements in optical and sweat-based detection are improving feasibility. Growing preference for needle-free monitoring is accelerating adoption. Expanding investment in R&D is enhancing device development. Rising digital healthcare transformation is supporting demand. Increasing patient awareness is boosting acceptance. Integration with AI-based health platforms is strengthening growth.

• By Ergonomics

On the basis of ergonomics, the glucose meters market is segmented into wearable and non-wearable devices. The non-wearable segment dominated the largest market revenue share of around 61.3% in 2025, driven by widespread use of traditional handheld glucose meters. These devices are cost-effective and widely accessible across global markets. Rising diabetes prevalence is boosting demand. Strong presence in hospitals and homecare settings is supporting usage. Ease of operation is driving patient preference. Availability in retail pharmacies is improving access. Continuous improvements in accuracy are supporting growth. Government diabetes screening programs are increasing adoption.

The wearable segment is expected to witness the fastest CAGR of around 14.5% from 2026 to 2033, driven by rising demand for continuous and real-time glucose monitoring. Increasing adoption of smart wearable devices is fueling growth. Integration with smartphones and health apps is boosting usability. Growing preference for remote patient monitoring is accelerating adoption. Advancements in sensor miniaturization are improving comfort. Rising digital health trends are strengthening expansion. Increasing focus on preventive healthcare is supporting demand.

• By Distribution Channel

On the basis of distribution channel, the glucose meters market is segmented into institutional sales and retail sales. The retail sales segment dominated the largest market revenue share of around 57.6% in 2025, driven by strong availability of glucose monitoring devices through pharmacies, drug stores, and online platforms. Increasing preference for self-monitoring among diabetic patients is significantly boosting demand. Rising global diabetes prevalence is further supporting market growth. Expanding e-commerce penetration is improving product accessibility across urban and rural regions. Affordable pricing of SMBG devices is encouraging widespread adoption. Frequent availability of test strips and consumables is supporting continuous usage. Growing awareness of home-based glucose monitoring is strengthening consumer preference. Rising health consciousness among patients is driving regular monitoring habits. Strong presence of retail pharmacy chains is enhancing distribution reach. Convenience of over-the-counter purchase is supporting segment dominance. Increasing digital health platforms are further improving accessibility and adoption.

The institutional sales segment is expected to witness the fastest CAGR of around 9.6% from 2026 to 2033, driven by rising hospital-based diabetes management and diagnostic programs. Increasing patient admissions due to diabetes-related complications is boosting demand. Government healthcare initiatives are strengthening institutional procurement of monitoring devices. Expanding hospital infrastructure is improving access to advanced glucose monitoring systems. Strong requirement for accurate clinical monitoring is driving adoption in healthcare facilities. Rising focus on early diagnosis and preventive care is supporting growth. Increasing integration of glucose monitoring in hospital protocols is enhancing usage. Growing number of specialty diabetes clinics is contributing to demand. Rising healthcare expenditure in emerging economies is supporting expansion. Development of advanced institutional monitoring systems is further accelerating adoption.

• By Application

On the basis of application, the glucose meters market is segmented into Type 1 diabetes, Type 2 diabetes, and gestational diabetes. The Type 2 diabetes segment dominated the largest market revenue share of around 68.9% in 2025, driven by the high global prevalence of lifestyle-related metabolic disorders. Sedentary lifestyles and poor dietary habits are major contributing factors. Increasing elderly population is significantly boosting demand. Rising awareness about regular blood glucose monitoring is supporting adoption. Strong dependence on SMBG devices is driving continuous usage. Expanding healthcare access is improving diagnosis rates globally. Growing healthcare expenditure is supporting market penetration. Government diabetes awareness programs are increasing early detection. High recurrence and chronic nature of Type 2 diabetes are sustaining demand. Increasing obesity rates are further fueling market growth.

The Type 1 diabetes segment is expected to witness the fastest CAGR of around 10.4% from 2026 to 2033, driven by increasing reliance on continuous glucose monitoring (CGM) systems. Rising pediatric and adolescent diabetes cases are contributing to demand growth. Technological advancements in insulin delivery and monitoring systems are boosting adoption. Growing awareness of early disease management is accelerating usage. Expanding availability of CGM devices is supporting segment growth. Increasing focus on precision diabetes care is enhancing adoption. Rising digital health integration is improving patient compliance. Strong clinical recommendation for continuous monitoring is driving demand. Expanding healthcare infrastructure is supporting accessibility. Increasing research into advanced diabetes management solutions is further strengthening growth.

• By End-User

On the basis of end-user, the glucose meters market is segmented into hospitals and home care. The home care segment dominated the largest market revenue share of around 62.8% in 2025, driven by increasing preference for self-monitoring and decentralized healthcare management. Rising global diabetes prevalence is significantly boosting demand. Easy availability of user-friendly glucose monitoring devices is supporting adoption. Growing awareness of preventive healthcare practices is encouraging regular usage. Expanding retail and online distribution channels are improving access. Technological advancements are enhancing ease of operation and accuracy. Increasing patient empowerment in chronic disease management is driving growth. Rising healthcare costs are pushing patients toward home-based care. Strong availability of SMBG systems is reinforcing segment dominance. Increasing digital health awareness is further strengthening adoption.

The hospital segment is expected to witness the fastest CAGR of around 9.8% from 2026 to 2033, driven by increasing hospital-based diagnosis and management of diabetes. Rising complications associated with uncontrolled diabetes are boosting demand. Expanding healthcare infrastructure is supporting adoption of advanced monitoring systems. Strong clinical requirement for accurate and real-time glucose tracking is driving usage. Increasing government investments in hospital healthcare systems are supporting growth. Rising number of inpatient diabetes cases is contributing to demand. Growing focus on early diagnosis and disease management is strengthening adoption. Integration of glucose monitoring into hospital workflows is enhancing efficiency. Expanding specialty diabetes care units is further accelerating growth. Continuous improvement in hospital diagnostic capabilities is supporting segment expansion.

Glucose Meters Market Regional Analysis

- North America dominated the glucose meters market with the largest revenue share of 39.6% in 2025, driven by high diabetes prevalence, strong healthcare infrastructure, widespread adoption of advanced glucose monitoring devices, and the presence of leading market players in the U.S.

- The region benefits from well-established diabetes care management systems, high patient awareness regarding blood glucose monitoring, and strong access to both traditional and digital glucose monitoring solutions

- This dominance is further supported by favorable reimbursement policies, continuous technological advancements in self-monitoring devices, and strong integration of glucose meters into routine clinical and homecare diabetes management programs

U.S. Glucose Meters Market Insight

The U.S. glucose meters market captured the largest revenue share in North America in 2025, driven by a high burden of diabetes, strong adoption of self-monitoring blood glucose devices, and advanced healthcare infrastructure. The country has a well-developed diabetes care ecosystem with widespread availability of both basic and advanced glucose monitoring systems, including connected and smart-enabled devices. In addition, strong presence of key medical device manufacturers and continuous product innovation are further supporting market growth in the U.S.

Europe Glucose Meters Market Insight

The Europe glucose meters market is projected to expand at a substantial CAGR throughout the forecast period, driven by increasing diabetes prevalence, well-established public healthcare systems, and rising awareness of early disease management. Strong emphasis on preventive healthcare and routine glucose monitoring is supporting widespread adoption of glucose meters across hospitals, clinics, and homecare settings in the region.

U.K. Glucose Meters Market Insight

The U.K. glucose meters market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing diabetes cases and strong NHS-led screening and monitoring programs. Rising awareness of lifestyle-related disorders and growing emphasis on self-monitoring of blood glucose levels are further supporting market growth.

Germany Glucose Meters Market Insight

The Germany glucose meters market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong healthcare system, high adoption of advanced diagnostic devices, and increasing prevalence of diabetes. Germany’s focus on precision healthcare and structured disease management programs supports steady use of glucose monitoring devices in both clinical and home settings.

Asia-Pacific Glucose Meters Market Insight

The Asia-Pacific glucose meters market is expected to be the fastest growing region during the forecast period due to the rapidly increasing diabetic population, improving healthcare access, rising awareness of glucose monitoring, and growing adoption of cost-effective diagnostic devices in emerging economies. Expanding healthcare infrastructure and government initiatives for chronic disease management are further driving market growth across the region.

Japan Glucose Meters Market Insight

The Japan glucose meters market is gaining momentum due to its aging population, high healthcare standards, and increasing prevalence of diabetes-related conditions. The country’s strong healthcare system and emphasis on preventive care are driving consistent adoption of glucose monitoring devices in both hospital and homecare settings.

China Glucose Meters Market Insight

The China glucose meters market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to a large diabetic population, rapid urbanization, and increasing awareness of diabetes management. Expanding healthcare infrastructure, rising availability of affordable diagnostic devices, and strong domestic manufacturing capabilities are key factors driving market growth in China.

Glucose Meters Market Share

The Glucose Meters industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Roche Diagnostics (Switzerland)

- Dexcom, Inc. (U.S.)

- Medtronic plc (Ireland)

- Ascensia Diabetes Care (Switzerland)

- LifeScan, Inc. (U.S.)

- Bayer AG (Germany)

- Arkray, Inc. (Japan)

- B. Braun SE (Germany)

- Terumo Corporation (Japan)

- Sinocare Inc. (China)

- i-SENS, Inc. (South Korea)

- AgaMatrix, Inc. (U.S.)

- Omron Healthcare (Japan)

- Ypsomed AG (Switzerland)

- Trividia Health, Inc. (U.S.)

- Nipro Corporation (Japan)

- Microtech Medical (China)

- Rossmax International Ltd. (Taiwan)

- Sanofi (France)

Latest Developments in Global Glucose Meters Market

- In May 2022, Abbott announced that its FreeStyle Libre 3 system received U.S. FDA clearance, featuring the world’s smallest, thinnest, and most accurate 14-day glucose sensor. This advancement was aimed at enhancing diabetes management by providing continuous glucose monitoring with improved precision, convenience, and user experience

- In October 2022, Dexcom launched its G7 Continuous Glucose Monitoring System across the United Kingdom, Ireland, Germany, Austria, and Hong Kong, marking the initial phase of its global rollout. The G7 system was designed to provide real-time glucose readings every five minutes, offering superior accuracy and usability for patients managing diabetes

- In April 2023, Medtronic announced that its MiniMed780G system received FDA approval, introducing the world’s first insulin pump with meal detection technology and five-minute auto-corrections. This innovation aimed to deliver more precise insulin management and improve glycemic outcomes for patients with diabetes

- In July 2023, Senseonics received FDA approval for its Eversense E3 Continuous Glucose Monitoring System, allowing for continuous glucose monitoring for up to six months. This system was developed to reduce the frequency of sensor replacements, providing patients with enhanced convenience and long-term usability

- In September 2024, Senseonics announced FDA clearance for the Eversense 365 Continuous Glucose Monitoring System, which enables continuous glucose monitoring for up to one year. This development aimed to offer long-term convenience and reduce costs for patients using implantable sensors, representing a significant step forward in diabetes management technology

- In April 2025, Dexcom received FDA clearance for the G7 15-Day Continuous Glucose Monitoring System, extending the sensor wear period from 10 to 15 days. This advancement provided patients with greater convenience, fewer sensor replacements, and sustained accuracy for continuous glucose monitoring, further enhancing diabetes care

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.