Global Glucose Sensors Market

Market Size in USD Billion

USD

5.10 Billion

USD

21.71 Billion

2025

2033

USD

5.10 Billion

USD

21.71 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.10 Billion | |

| USD 21.71 Billion | |

| % | |

|

Glucose Sensors Market Size

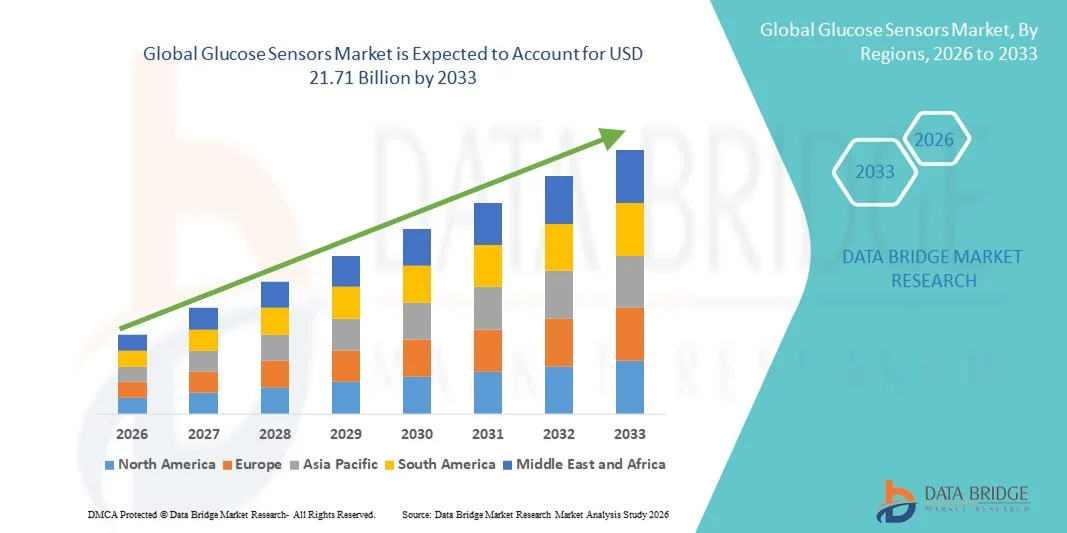

- The global glucose sensors market size was valued at USD 5.10 billion in 2025 and is expected to reach USD 21.71 billion by 2033, at a CAGR of 19.85% during the forecast period

- The market growth is largely fueled by the rising prevalence of diabetes worldwide, increasing adoption of continuous glucose monitoring (CGM) technologies, and growing awareness regarding proactive disease management, leading to greater integration of glucose sensors across hospitals, clinics, and homecare settings. Advancements in sensor accuracy, wireless connectivity, and real-time monitoring are further driving adoption and improving patient outcomes in both developed and emerging markets

- Furthermore, the growing preference for minimally invasive and wearable health monitoring solutions, along with the increasing demand for personalized diabetes management, is establishing glucose sensors as essential tools for modern healthcare. Expansion of healthcare infrastructure, rising smartphone penetration, and supportive reimbursement policies are accelerating the uptake of innovative glucose sensor technologies, thereby significantly boosting overall industry growth

Glucose Sensors Market Analysis

- Glucose sensors, including continuous glucose monitoring (CGM) systems and blood glucose meters, are increasingly vital components of modern diabetes management due to their ability to provide accurate, real-time blood glucose readings, enhance patient compliance, and reduce complications associated with uncontrolled diabetes. Advancements in wearable devices, non-invasive monitoring, and integration with mobile apps are further accelerating adoption across clinical and homecare settings

- The escalating demand for glucose sensors is primarily fueled by the rising prevalence of diabetes globally, growing awareness about proactive disease management, and increasing preference for personalized and minimally invasive monitoring solutions. Technological innovations such as AI-enabled predictive analytics, smartphone connectivity, and hybrid closed-loop systems are further driving market adoption and improving patient outcomes

- North America dominated the Glucose Sensors market with the largest revenue share of approximately 41.5% in 2025, supported by advanced healthcare infrastructure, strong reimbursement policies, high prevalence of diabetes, and early adoption of wearable and continuous monitoring technologies. The U.S. continues to witness substantial growth in CGM adoption, particularly among type 1 and type 2 diabetic patients, driven by technological innovations and increasing healthcare awareness programs

- Asia-Pacific is expected to be the fastest-growing region in the Glucose Sensors market during the forecast period, projected to register a CAGR of approximately 12.2% driven by rising diabetes prevalence, improving healthcare infrastructure, increasing affordability of advanced glucose monitoring devices, and growing awareness of diabetes management in countries such as India, China, and Japan

- The Adult Population segment dominated the largest market revenue share of 60.2% in 2025, driven by the higher prevalence of type 2 diabetes, lifestyle-related disorders, and regular hospital monitoring needs

Report Scope and Glucose Sensors Market Segmentation

|

Attributes |

Glucose Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Glucose Sensors Market Trends

Shift Towards Continuous, Minimally Invasive, and Connected Glucose Monitoring

- A key trend in the global glucose sensors market is the growing adoption of continuous glucose monitoring (CGM) systems that allow real-time tracking of blood glucose levels without frequent finger-prick testing. These devices provide better glycemic control, improve patient adherence, and reduce the risk of hypoglycemia

- For instance, Dexcom, Inc. has developed advanced CGM systems that transmit glucose data directly to smartphones or wearable devices, enabling both patients and clinicians to track trends and make timely adjustments in therapy

- Wearable and minimally invasive sensors are becoming increasingly preferred, particularly among pediatric and elderly populations, as they reduce discomfort and improve compliance

- The integration of sensors with digital health platforms and cloud-based data storage is enhancing patient monitoring, remote care, and personalized diabetes management

- Advances in sensor accuracy, longer sensor lifespan, and reduced calibration requirements are further improving clinical outcomes and patient convenience. In addition, the development of implantable glucose sensors that provide extended monitoring periods is gaining traction, particularly in hospital and high-risk patient settings. These innovations, combined with the increasing demand for real-time data analytics in diabetes care, are reshaping patient expectations and creating opportunities for new market entrants

Glucose Sensors Market Dynamics

Driver

Rising Prevalence of Diabetes and Increasing Awareness of Self-Monitoring

- The primary driver for the glucose sensors market is the rapid increase in the global prevalence of diabetes, driven by factors such as aging populations, sedentary lifestyles, and obesity

- Type 1 and Type 2 diabetes patients increasingly require reliable, accurate, and continuous glucose monitoring to manage their condition effectively.

- For instance, according to the International Diabetes Federation, the number of adults living with diabetes worldwide continues to grow, reaching over 600 million by 2030, creating a significant demand for glucose monitoring solutions

- Growing awareness about the benefits of self-monitoring, coupled with patient education programs, is encouraging the adoption of advanced sensors over traditional glucometers

- Expanding healthcare infrastructure and rising affordability of glucose monitoring devices in emerging economies such as India, China, and Brazil are also fueling market growth. The increasing prevalence of gestational diabetes and the focus on maternal health further drive demand for reliable glucose monitoring solutions

- In addition, integration of glucose sensors with insulin pumps and telemedicine platforms is providing comprehensive diabetes management options, making these devices essential tools in both clinical and home-care settings

Restraint/Challenge

High Device Costs and Regulatory Barriers

- Despite strong growth, the glucose sensors market faces challenges related to high device costs, reimbursement limitations, and regulatory complexities

- Advanced continuous and implantable sensors are often more expensive than traditional glucometers, which can limit adoption in low- and middle-income regions

- For instance, hospital-grade or long-term CGM systems from companies such as Medtronic plc require ongoing maintenance, sensor replacements, and subscription-based monitoring software, which increases the overall cost for patient

- Stringent regulatory requirements for medical device approval, including safety, efficacy, and accuracy testing, can extend product launch timelines and increase compliance costs for manufacturers

- Technical challenges such as sensor calibration, signal interference, and short lifespan of disposable sensors may also impact patient satisfaction and adoption

- In addition, some patients may experience skin irritation or discomfort from wearable sensors, posing barriers to long-term use

- Addressing these issues through improved device accuracy, cost-effective manufacturing, patient education, and streamlined regulatory pathways is essential for sustained market growth and broader adoption globally

Glucose Sensors Market Scope

The market is segmented on the basis of product, technology, component, demographics, and end-user.

- By Product

On the basis of product, the Glucose Sensors market is segmented into Invasive Glucose Monitoring, Non-Invasive Glucose Monitoring, Self-Glucose Monitoring, and Lab-Based Glucose Monitoring. The Invasive Glucose Monitoring segment dominated the largest market revenue share of 42.8% in 2025, driven by its high accuracy, reliability, and clinical acceptance across hospitals and diabetes care centers. Hospitals and home care providers prefer invasive sensors for critical patient monitoring, continuous glucose tracking, and insulin delivery integration. Rising prevalence of diabetes globally, coupled with established reimbursement frameworks in developed markets, supports adoption. Clinical trials and physician recommendations also drive confidence in invasive devices. Integration with insulin pumps and mobile applications further strengthens demand. Patients value real-time alerts, trend analysis, and automated data sharing with healthcare providers. The segment is supported by strong R&D investments, frequent product launches, and favorable regulatory approvals. Growth is particularly strong in North America and Europe, where infrastructure for continuous monitoring is well-established. Hospitals, clinics, and home care setups form the core end-users for invasive glucose monitoring.

The Non-Invasive Glucose Monitoring segment is expected to witness the fastest CAGR of 21.4% from 2026 to 2033, fueled by rising consumer preference for pain-free monitoring solutions. Innovations such as optical coherence tomography, near-infrared spectroscopy, and fluorescence-based detection are enabling non-invasive sensors for home and ambulatory care. Convenience, avoidance of finger pricks, and integration with wearable devices appeal to tech-savvy and pediatric populations. Emerging economies are adopting non-invasive technologies due to increasing diabetes awareness and government healthcare initiatives. Companies are focusing on miniaturization, sensor accuracy, and continuous monitoring capabilities. The adoption in home care and outpatient settings is rapidly increasing. Patient compliance and comfort are significant growth drivers, supported by smartphone connectivity and cloud-based data analytics. Partnerships with digital health providers further accelerate growth. Rising demand in Asia-Pacific and Latin America is contributing to faster CAGR.

- By Technology

On the basis of technology, the Glucose Sensors market is segmented into Photo Acoustic Spectroscopy, Optical Coherence Tomography, Polarimetry, Fluorescence, MIR Spectroscopy, NIR Spectroscopy, Impedance Spectroscopy, Skin Suction Blister Technique, Sonophoresis, and Reverse Iontophoresis. The Optical Coherence Tomography (OCT) segment held the largest market revenue share of 39.6% in 2025, owing to its high accuracy, non-invasive capabilities, and suitability for continuous glucose monitoring in clinical and home care environments. OCT devices are widely adopted in hospitals and specialized clinics, particularly for high-risk diabetic patients. Advantages include rapid measurements, integration with smartphones, and compatibility with wearable monitoring systems. Continuous innovation and regulatory approvals support OCT adoption. High accuracy, patient convenience, and seamless integration with digital health platforms strengthen market dominance. Increasing collaborations with device manufacturers and healthcare providers drive clinical use. Expansion in Europe and North America remains a key factor. Patients benefit from enhanced data analytics and trend tracking. Hospital adoption is reinforced by insurance coverage and physician recommendation. Continuous monitoring capabilities further boost demand.

The Photo Acoustic Spectroscopy segment is expected to witness the fastest CAGR of 22% from 2026 to 2033, supported by growing R&D focus and consumer demand for non-invasive, continuous monitoring. Its rising adoption is driven by accuracy, portability, and minimal discomfort. Integration with wearable devices and insulin pumps enhances usability. The technology is gaining traction in home care, ambulatory settings, and remote patient monitoring programs. Emerging markets are investing in cost-effective spectroscopy-based devices to expand accessibility. Rising awareness of diabetes management and digital healthcare solutions further fuels adoption. Adoption in Asia-Pacific is growing rapidly due to technological innovation and government support. Pediatric and adult populations benefit from pain-free monitoring. Manufacturers are launching compact, user-friendly devices. High compatibility with mobile apps strengthens adoption.

- By Component

On the basis of component, the Glucose Sensors market is segmented into Sensors, Transmitters & Receivers, and Integrated Insulin Pumps. The Sensors segment dominated the largest market revenue share of 45.3% in 2025, as it forms the core of glucose measurement and continuous monitoring systems. Sensors provide accurate, real-time glucose readings, critical for hospitals, clinics, and home care patients. High reliability, ease of integration with insulin pumps, and compatibility with mobile applications drive demand. Rising adoption of continuous glucose monitoring systems (CGMS) and increasing prevalence of diabetes globally boost sensor usage. Clinical trials and favorable reimbursement policies reinforce dominance. Technological advancements and miniaturization increase patient compliance. Integration with cloud platforms allows for remote patient monitoring. Strong adoption is seen in North America and Europe. Continuous innovation in sensor design and connectivity strengthens market position. Hospitals, clinics, and private care facilities form the core end-users.

The Integrated Insulin Pumps segment is expected to witness the fastest CAGR of 23% from 2026 to 2033, fueled by the demand for closed-loop systems that automate insulin delivery based on real-time glucose readings. Adoption is driven by convenience, reduced risk of hypoglycemia, and improved patient quality of life. Growing awareness, digital integration, and rising investment in smart devices enhance market growth. Emerging economies are increasingly adopting insulin pumps due to affordability and government awareness programs. Integration with wearable and remote monitoring solutions further accelerates adoption. High adoption in home care and outpatient clinics drives rapid CAGR. Pediatric and adult users benefit from automated alerts. Collaboration with digital health platforms strengthens functionality.

- By Demographics

On the basis of demographics, the Glucose Sensors market is segmented into Adult Population (>14 years) and Children Population (≤14 years). The Adult Population segment dominated the largest market revenue share of 60.2% in 2025, driven by the higher prevalence of type 2 diabetes, lifestyle-related disorders, and regular hospital monitoring needs. Adults prefer continuous glucose monitoring, self-monitoring devices, and integration with smartphone apps. Corporate wellness programs and remote monitoring solutions increase adoption. Rising awareness campaigns, insurance coverage, and advanced healthcare infrastructure reinforce dominance. Adults benefit from devices integrated with insulin pumps, cloud platforms, and trend analysis tools. Hospitals and home care setups form the primary end-users. Adoption is particularly high in North America and Europe. Technological adoption and affordability support sustained growth. Continuous innovation enhances adult patient compliance.

The Children Population segment is expected to witness the fastest CAGR of 19.5% from 2026 to 2033, fueled by innovations in pain-free, non-invasive monitoring and wearable-friendly designs. Pediatric patients and parents increasingly adopt continuous glucose monitoring solutions to improve compliance. Integration with mobile apps for parental monitoring, gamification features, and remote alerts drive growth. Government initiatives for early diabetes detection enhance adoption. Pediatric care units and clinics are investing in child-friendly, accurate monitoring systems. Home care adoption is rising rapidly. Advanced sensors and mobile connectivity facilitate usage. Asia-Pacific and Latin America are emerging markets for pediatric adoption.

- By End-User

On the basis of end-user, the Glucose Sensors market is segmented into Hospitals, Private Clinics, Home Care, Ambulatory Settings, and Others. The Hospitals segment dominated the largest market revenue share of 47.5% in 2025, due to high patient volume, clinical reliance on continuous and lab-based monitoring, and integration with hospital EMRs. Hospitals prioritize devices with accuracy, reliability, and interoperability with other monitoring systems. Clinical trials, physician recommendations, and insurance reimbursement drive hospital adoption. Continuous monitoring, automated data sharing, and integration with insulin delivery systems reinforce hospital dominance. Adoption is strongest in North America and Europe. Hospitals continue to invest in advanced technologies for critical patient care.

The Home Care segment is expected to witness the fastest CAGR of 21% from 2026 to 2033, driven by rising diabetes prevalence, increasing patient preference for self-monitoring, and adoption of wearable and non-invasive glucose sensors. Smartphone connectivity, cloud integration, and personalized data management enhance patient compliance. Rising awareness campaigns, telemedicine adoption, and digital healthcare initiatives accelerate growth. Integration with smart insulin pumps and mobile alerts strengthens adoption. Emerging markets such as Asia-Pacific show high growth potential. Patient convenience and remote monitoring are major drivers.

Glucose Sensors Market Regional Analysis

- North America dominated the glucose sensors market with the largest revenue share of approximately 41.5% in 2025, supported by advanced healthcare infrastructure, strong reimbursement policies, high prevalence of diabetes, and early adoption of wearable and continuous monitoring technologies. The U.S. continues to witness substantial growth in CGM adoption, particularly among type 1 and type 2 diabetic patients, driven by technological innovations and increasing healthcare awareness programs

- Consumers and healthcare providers in the region highly value real-time glucose tracking, integration with insulin pumps, and seamless connectivity with mobile and cloud platforms. High disposable incomes and robust digital health frameworks further encourage adoption. The presence of leading device manufacturers and continuous product innovation strengthens market dominance. Integration with telemedicine and remote patient monitoring supports hospital and home care applications

- Insurance coverage and government health initiatives facilitate accessibility and affordability. Hospitals, private clinics, and home care services remain the major end-users. Rising awareness programs and increasing patient compliance reinforce market growth. North America remains a hub for R&D and technological advancement in glucose monitoring solutions

U.S. Glucose Sensors Market Insight

The U.S. glucose sensors market captured the largest revenue share in 2025 within North America, fueled by the rapid uptake of connected devices, continuous glucose monitoring systems (CGMS), and mobile health integration. Patients increasingly prefer wearable sensors that provide accurate, real-time glucose readings and automated alerts. Strong healthcare infrastructure, high diabetes prevalence, and favorable reimbursement policies further drive adoption. Hospitals, ambulatory care centers, and home care setups are increasingly incorporating advanced glucose sensors into patient care programs. Technological innovations such as non-invasive monitoring, integration with insulin pumps, and cloud-based analytics enhance usability. Growing awareness through government programs and diabetes education campaigns supports consumer adoption. Telemedicine integration allows remote monitoring and trend analysis. Increasing demand for pediatric and adult CGM solutions accelerates growth. Home-based self-monitoring devices complement clinical use. Smartphone connectivity and app-based data management improve patient compliance.

Europe Glucose Sensors Market Insight

The Europe glucose sensors market is projected to expand at a substantial CAGR throughout the forecast period, driven by stringent healthcare regulations, rising diabetes prevalence, and increasing adoption of connected medical devices. Hospitals and clinics are increasingly incorporating continuous and non-invasive glucose monitoring technologies. Urbanization and technological awareness encourage adoption of wearable sensors for both adult and pediatric populations. Consumers value accuracy, convenience, and integration with digital health platforms. Demand is strong in residential care, private clinics, and ambulatory care settings. High healthcare spending and insurance coverage facilitate penetration. Europe witnesses rapid growth in home care adoption for diabetes management. Technological advancements, telemedicine adoption, and physician recommendation further drive market expansion. Regulatory approvals for new devices accelerate innovation. End-users increasingly prefer connected devices with real-time alerts. Diabetes awareness campaigns enhance patient compliance and adoption.

U.K. Glucose Sensors Market Insight

The U.K. glucose sensors market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing diabetes prevalence, rising awareness of self-monitoring solutions, and growing adoption of home-based monitoring devices. Consumers are motivated by convenience, integration with digital health apps, and improved patient compliance. The country’s robust e-commerce and healthcare infrastructure supports widespread availability of advanced glucose sensors. Hospitals and private clinics are incorporating continuous glucose monitoring systems into routine care. Rising government initiatives for diabetes management further stimulate adoption. Home care adoption is also growing among adult and pediatric patients. Telemedicine integration and smartphone connectivity enhance remote monitoring. Regulatory approvals for innovative monitoring technologies accelerate market growth. Consumer preference for non-invasive and wearable devices continues to rise. Pediatric diabetes care adoption is improving. Insurance coverage and reimbursement policies contribute to accessibility and adoption.

Germany Glucose Sensors Market Insight

The Germany glucose sensors market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of diabetes management, technological innovation, and advanced healthcare infrastructure. Hospitals, clinics, and home care setups are increasingly adopting continuous and non-invasive monitoring solutions. Integration with insulin pumps, mobile apps, and cloud platforms enhances usability and patient compliance. Germany’s emphasis on precision healthcare and innovation encourages adoption of advanced glucose sensors. Rising prevalence of type 1 and type 2 diabetes supports strong market demand. Telemedicine and remote monitoring solutions are being integrated into care programs. Regulatory approvals facilitate adoption of new monitoring technologies. Emerging home care and outpatient segments offer significant growth potential. Consumers favor wearable, pain-free, and accurate monitoring devices. Pediatric and adult populations benefit from continuous glucose tracking. Reimbursement schemes and healthcare funding further support adoption.

Asia-Pacific Glucose Sensors Market Insight

The Asia-Pacific glucose sensors market is poised to grow at the fastest CAGR of approximately 12.2% during the forecast period, driven by rising diabetes prevalence, improving healthcare infrastructure, increasing affordability of advanced glucose monitoring devices, and growing awareness of diabetes management. Countries such as India, China, and Japan are witnessing rapid adoption of continuous and non-invasive monitoring solutions. Government initiatives promoting diabetes awareness and digital health integration boost adoption. Rising medical tourism, expanding hospital infrastructure, and enhanced reimbursement policies further support growth. Adoption is increasing across hospitals, clinics, home care, and ambulatory settings. Technological innovation, integration with mobile and wearable devices, and patient education drive acceptance. Pediatric and adult populations are adopting devices for self-monitoring and management. Telemedicine and cloud-based monitoring accelerate data-driven care. Emerging economies show high growth potential due to increasing accessibility. Manufacturers are introducing cost-effective, user-friendly solutions for diverse patient needs. Continuous innovation and partnerships with healthcare providers strengthen regional growth.

Japan Glucose Sensors Market Insight

The Japan glucose sensors market is gaining momentum due to the country’s high-tech healthcare culture, increasing diabetes prevalence, and growing demand for convenient self-monitoring solutions. Adoption is driven by integration with wearable devices, mobile applications, and insulin pumps. Hospitals, clinics, and home care setups are adopting continuous and non-invasive monitoring solutions. The aging population fuels demand for easy-to-use and reliable devices. Telemedicine and remote monitoring initiatives enhance accessibility. Government programs and awareness campaigns support patient education and compliance. Pediatric and adult populations are adopting connected monitoring solutions. Technological innovation and product miniaturization drive adoption. High-income population segments favor advanced, non-invasive glucose sensors. Integration with digital health platforms facilitates trend analysis and alerts. Home care and outpatient adoption continue to rise. The market benefits from robust healthcare infrastructure and high consumer purchasing power.

China Glucose Sensors Market Insight

The China glucose sensors market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding middle class, increasing diabetes prevalence, rapid urbanization, and high rates of technological adoption. Hospitals, clinics, and home care setups are rapidly integrating continuous and non-invasive monitoring systems. Government initiatives promoting diabetes awareness and smart healthcare infrastructure facilitate adoption. Wearable and connected devices are gaining traction among adult and pediatric populations. Integration with mobile applications, insulin pumps, and cloud platforms improves patient compliance. Emerging smart cities and increasing healthcare investments support market expansion. Manufacturers are introducing cost-effective, user-friendly monitoring solutions. Rising awareness of diabetes management and telemedicine adoption accelerate growth. The market is strengthened by domestic production capabilities and strong distribution networks. Hospitals and home care facilities are adopting advanced devices. Technological innovation and continuous product development sustain market expansion.

Glucose Sensors Market Share

The Glucose Sensors industry is primarily led by well-established companies, including:

- Dexcom, Inc. (U.S.)

- Abbott (U.S.)

- Medtronic plc (Ireland)

- Roche Diabetes Care (Switzerland)

- Senseonics Holdings, Inc. (U.S.)

- Insulet Corporation (U.S.)

- GlucoMe Ltd. (Israel)

- Ascensia Diabetes Care (Switzerland)

- Ypsomed AG (Switzerland)

- Arkray, Inc. (Japan)

- LifeScan, Inc. (U.S.)

- Nipro Corporation (Japan)

- Tandem Diabetes Care, Inc. (U.S.)

- Bayer AG (Germany)

- i-SENS, Inc. (South Korea)

- GlucoTrack Ltd. (Israel)

- AllMed, Inc. (U.S.)

- Nova Biomedical Corporation (U.S.)

- Becton Dickinson and Company (U.S.)

- Medisana AG (Germany)

Latest Developments in Global Glucose Sensors Market

- In February 2023, Dexcom, Inc. announced that its G7 continuous glucose monitoring (CGM) system received FDA approval and began availability in the U.S., offering real‑time glucose readings that update every five minutes and connecting directly to mobile apps and insulin pumps without requiring traditional finger‑stick calibrations

- In September 2024, Abbott Laboratories launched its Lingo continuous glucose monitoring system available for over‑the‑counter purchase, designed for adults to conveniently monitor glucose levels without a prescription and tailored for everyday wellness tracking beyond traditional diabetic management

- In August 2024, Dexcom introduced Stelo by Dexcom, the first FDA‑cleared over‑the‑counter CGM that offers up to 15‑day sensor wear and real‑time glucose tracking via smartphone, expanding glucose sensor access to broader consumer segments including non‑insulin users

- In June 2024, Abbott Laboratories received U.S. FDA clearance for two over‑the‑counter continuous glucose monitoring systems, Lingo and Libre Rio, both based on its FreeStyle Libre platform, expanding consumer access to glucose monitoring tools outside clinical settings

- In August 2024, Medtronic secured U.S. FDA approval for the Simplera CGM, its first fully disposable, all‑in‑one glucose monitoring sensor that is significantly smaller and designed for streamlined daily wear, marking Medtronic’s entry into simplified CGM offerings

- In July 2024, Roche received CE mark approval for its Accu‑Chek SmartGuide AI‑enabled continuous glucose monitoring system, which provides predictive hypoglycemia alerts, real‑time readings, and glucose trend forecasts to enhance diabetes self‑management and digital health integration

- In April 2025, Dexcom, Inc. announced U.S. FDA approval of the Dexcom G7 15 Day CGM system for adults aged 18 and older, offering extended sensor wear capability (up to 15.5 days) and improved accuracy, setting a new benchmark in wearable glucose monitoring technology

- In June 2025, Tracky, an Indian medtech startup by DrStore Healthcare Services, launched India’s first Bluetooth‑enabled continuous glucose monitor, featuring automatic syncing via a mobile app, real‑time glucose alerts, and a cost‑effective design aimed at expanding access to modern glucose sensing technology

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.