Global Graves Disease Treatment Market

Market Size in USD Million

USD

418.50 Million

USD

590.60 Million

2024

2032

USD

418.50 Million

USD

590.60 Million

2024

2032

| 2025 - 2032 | |

| USD 418.50 Million | |

| USD 590.60 Million | |

| % | |

|

Graves Disease Treatment Market Size

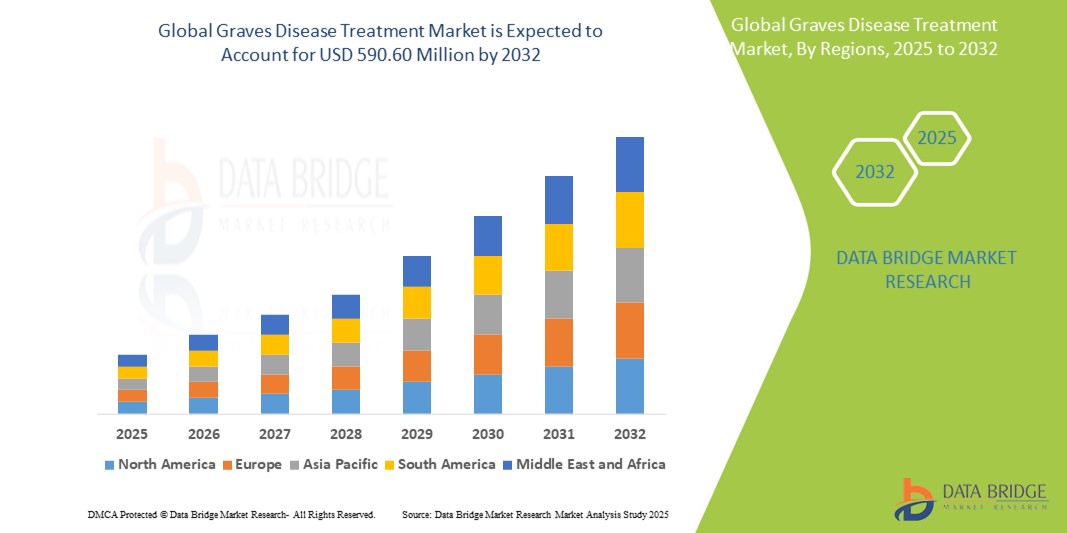

- The global Graves Disease Treatment market size was valued at USD 418.5 million in 2024 and is expected to reach USD 590.60 million by 2032, at a CAGR of 4.50% during the forecast period

- This growth is driven by factors such as increasing prevalence of autoimmune thyroid disorders, advancements in diagnostic tools, and rising patient awareness.

Graves Disease Treatment Market Analysis

- Graves disease is an autoimmune disorder that causes hyperthyroidism by overstimulating the thyroid gland. The treatment options include anti-thyroid medications, radioactive iodine therapy, and surgery, which aim to reduce thyroid hormone production.

- The demand for Graves disease treatment is significantly driven by the rising number of thyroid disorder cases, improved diagnostic capabilities, and increasing availability of treatment options globally.

- North America dominates the Graves disease treatment market due to high healthcare spending, early diagnosis rates, and robust reimbursement frameworks.

- Asia-Pacific is anticipated to witness the fastest growth due to increasing healthcare access and awareness campaigns in countries like China and India.

- Anti-thyroid drugs are expected to hold the largest market share of 41.32% in 2025 due to their effectiveness as a first-line treatment option. Increased preference for non-invasive therapies and wide availability are expected to drive segment growth.

Report Scope and Graves Disease Treatment Market Segmentation

|

Attributes |

Graves Disease Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Graves Disease Treatment Market Trends

"Shift Towards Personalized Thyroid Management Protocols"

- A key trend shaping the Graves disease treatment market is the increasing emphasis on personalized medicine. Clinicians are adopting individualized treatment plans that consider age, gender, severity of hyperthyroidism, underlying autoimmune profiles, and comorbidities.

- This approach aims to improve clinical outcomes, reduce side effects, and enhance patient adherence by using targeted diagnostics such as hormonal and genetic profiling.

- For instance, Increased availability of genetic and hormonal profiling tools is supporting the implementation of personalized thyroid care models across North America and Europe.

- The adoption of personalized thyroid management protocols is transforming Graves' disease treatment by enabling tailored therapies, which enhance efficacy and patient satisfaction while reducing adverse effects.

Graves Disease Treatment Market Dynamics

Driver

"Rising Incidence of Autoimmune Thyroid Disorders"

- There is a global rise in autoimmune diseases, with Graves disease being one of the most prevalent. Increased awareness, routine screening, and enhanced diagnostic capabilities have contributed to early detection and growing patient volumes seeking treatment.

- The burden is particularly high in urban regions with rising stress, iodine intake fluctuations, and genetic predisposition.

- For instance, In January 2024, a CDC report highlighted a 12% increase in newly diagnosed thyroid dysfunction cases in North America. In April 2023, global thyroid awareness campaigns accelerated early testing, leading to increased treatment initiation.

- The rising incidence of autoimmune thyroid disorders, fueled by improved diagnostics and awareness, is driving demand for Graves' disease treatments, creating a robust market for innovative solutions.

Opportunity

"Launch of Monoclonal Antibody-Based Therapies"

- A significant opportunity in the Graves disease treatment landscape is the introduction of monoclonal antibody therapies designed to inhibit autoantibody stimulation of the thyroid-stimulating hormone receptor

- These biologics are especially valuable for patients with contraindications to conventional treatments or recurrent disease

- For instance, In March 2024, the U.S. FDA granted Orphan Drug Designation to a monoclonal antibody therapy targeting TSH receptor stimulation. In June 2023, clinical trials began for an anti-CD20 therapy to reduce autoantibody production in Graves disease.

- The development of monoclonal antibody therapies presents a promising opportunity to address unmet needs in Graves' disease treatment, offering targeted and effective options for complex cases

Restraint/Challenge

"Side Effects and Long-Term Risks of Conventional Therapies"

- Despite being effective, standard treatment modalities such as radioactive iodine and anti-thyroid drugs come with significant risks including permanent hypothyroidism, relapse after remission, and adverse effects ranging from agranulocytosis to hepatotoxicity. These limitations hinder long-term compliance and encourage demand for safer alternatives

- For instance, In August 2023, a meta-analysis published in JAMA indicated a 28% relapse rate within five years post-radioactive iodine treatment. In October 2024, patient advocacy groups raised concerns regarding side effects of methimazole in pediatric populations.

- The significant side effects and long-term risks associated with conventional therapies pose a challenge to patient compliance and market growth, underscoring the need for safer, innovative treatment options

Graves Disease Treatment Market Scope

The market is segmented on the basis of treatment type, route of administration, end user, and distribution channel.

|

Segmentation |

Sub-Segmentation |

|

By Treatment Type |

|

|

By Route of Administration |

|

|

By End User |

|

|

By Distribution Channel

|

|

In 2025, the Anti-thyroid Drugs segment is projected to dominate the market with a largest share in treatment type segment

In 2025, the Anti-thyroid Drugs segment is projected to dominate the market with the largest share of 41.32% reflecting their longstanding position as the first-line treatment for Graves' disease. These medications, primarily methimazole and propylthiouracil, are widely utilized due to their oral administration, well-established efficacy, and manageable safety profile. Anti-thyroid drugs allow for non-invasive management of hyperthyroidism and are particularly favored in pediatric, pregnant, and mildly symptomatic patients. Their cost-effectiveness, accessibility, and capability to restore euthyroidism without the risks associated with surgery or radioiodine therapy further contribute to their market dominance.

The Hospital segment is expected to account for the largest share during the forecast period in indication market

In 2025, the Hospitals segment is expected to dominate with the largest share of 50.6%, driven by its comprehensive infrastructure for diagnosis, intensive care, and interdisciplinary management of Graves’ disease. Hospitals are central to the delivery of multimodal therapies, including anti-thyroid drugs, radioiodine therapy, and surgical interventions. They also serve as referral centers for complex cases involving thyroid storm, orbitopathy (thyroid eye disease), and cardiac complications associated with hyperthyroidism. Additionally, hospital-based care facilitates access to endocrinologists, ophthalmologists, and nuclear medicine specialists, ensuring a coordinated treatment approach and ongoing monitoring for disease relapse or progression.

Graves Disease Treatment Market Regional Analysis

“North America Holds the Largest Share in the Graves Disease Treatment Market”

- North America is projected to dominate the global Graves' disease treatment market in 2025, accounting for an estimated 41.7% of the total market share. This dominance is attributed to the region's well-established healthcare infrastructure, higher disease awareness, and early screening programs.

- North America holds the largest share of the global Graves disease treatment market, primarily due to its well-established healthcare infrastructure, higher disease awareness, and early screening programs.

- The United States leads within North America, holding a 65.12% of the share. The country's robust pharmaceutical industry, extensive clinical trial activities, and favorable reimbursement frameworks contribute to its leading position. Additionally, initiatives by organizations like the American Thyroid Association, which updated its clinical practice guidelines in 2023 to encourage early and accurate diagnosis, have enhanced treatment uptake.

- The region benefits from the presence of leading pharmaceutical companies, robust clinical trial activities, and favorable reimbursement frameworks, particularly in the U.S. Moreover, initiatives by government agencies and medical societies to enhance thyroid disorder diagnosis and management contribute to market growth.

- For instance, in 2023, the American Thyroid Association updated its clinical practice guidelines to encourage early and accurate diagnosis, enhancing treatment uptake. Canada and Mexico also demonstrate growth due to public health outreach programs and rising adoption of advanced therapeutics.

“Asia-Pacific is Projected to Register the Highest CAGR in the Graves Disease Treatment Market”

- The Asia-Pacific region is expected to register the highest compound annual growth rate during the forecast period. This growth is attributed to improving healthcare infrastructure, expanding government health schemes, and increasing awareness about autoimmune thyroid diseases.

- The Asia-Pacific region is anticipated to register the highest compound annual growth rate (CAGR) during the forecast period, with an estimated 15.32% market share by 2025. This growth is driven by improving healthcare infrastructure, expanding government health schemes, and increasing awareness about autoimmune thyroid diseases.

- Countries such as India, China, and South Korea are investing heavily in diagnostic technologies and public health education, resulting in improved early detection rates.

- India is witnessing a surge in thyroid disorder screenings through national health campaigns, while China is focused on rural healthcare expansion and incorporation of endocrinology units in regional hospitals. South Korea benefits from a growing private healthcare sector and government incentives for rare disease management. Additionally, lower treatment costs and increasing penetration of biologics in these markets are expected to fuel rapid expansion.

Graves Disease Treatment Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- AbbVie Inc. (U.S.)

- Mylan N.V. (U.S.)

- Merck & Co., Inc. (U.S.)

- Pfizer Inc. (U.S.)

- GlaxoSmithKline plc (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Amgen Inc. (U.S.)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Allergan (Ireland)

- AstraZeneca (U.K.)

- Eli Lilly and Company (U.S.)

- Sling Therapeutics, Inc. (U.S.)

Latest Developments in Global Graves Disease Treatment Market

• In January 2025, Sanofi launched a Phase II clinical trial for its novel biologic therapy targeting thyroid-stimulating immunoglobulins (TSI) in patients with Graves disease. This initiative marks a significant milestone in the advancement of monoclonal antibody-based therapies for autoimmune thyroid disorders. By directly neutralizing TSIs, the therapy aims to prevent hyperthyroid flares and minimize relapse rates, offering a targeted treatment alternative to standard antithyroid medications and surgery.

• In August 2024, Novartis entered a strategic collaboration with a leading AI diagnostics firm to jointly develop early screening tools for autoimmune thyroid diseases, including Graves disease. The initiative focuses on leveraging machine learning algorithms and clinical biomarker integration to enhance the accuracy and speed of diagnosis. The partnership is expected to support data-driven therapeutic planning, paving the way for more personalized and predictive approaches in thyroid disease management.

• In November 2023, Merck announced that the European Medicines Agency (EMA) granted approval for its extended-release pediatric formulation of methimazole, a frontline antithyroid drug. This innovation addresses a critical need in pediatric endocrinology by offering improved dosing flexibility, once-daily administration, and enhanced treatment adherence for children living with Graves disease. It also helps reduce the risk of side effects associated with fluctuating drug levels.

• In October 2023, Teva Pharmaceuticals commenced clinical trials for a biosimilar version of propylthiouracil (PTU), a widely used antithyroid medication. The biosimilar is designed to increase global affordability and accessibility, particularly in emerging markets where treatment costs and drug availability remain barriers. If approved, this biosimilar could improve therapy equity and reduce dependence on expensive branded drugs.

• In July 2023, Pfizer announced its investment in a cross-border collaborative project involving academic institutions in the Asia-Pacific region to explore genetic biomarkers linked to Graves disease susceptibility and treatment responsiveness. This study supports Pfizer’s broader strategy in precision medicine, with the goal of identifying genotype-based predictors for optimal therapeutic responses. The project may unlock new insights into the pathophysiology of Graves disease across diverse populations.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.