Global Guidewires And Catheters Market

Market Size in USD Billion

USD

9.86 Billion

USD

17.32 Billion

2025

2033

USD

9.86 Billion

USD

17.32 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.86 Billion | |

| USD 17.32 Billion | |

| % | |

|

Guidewires & Catheters Market Overview

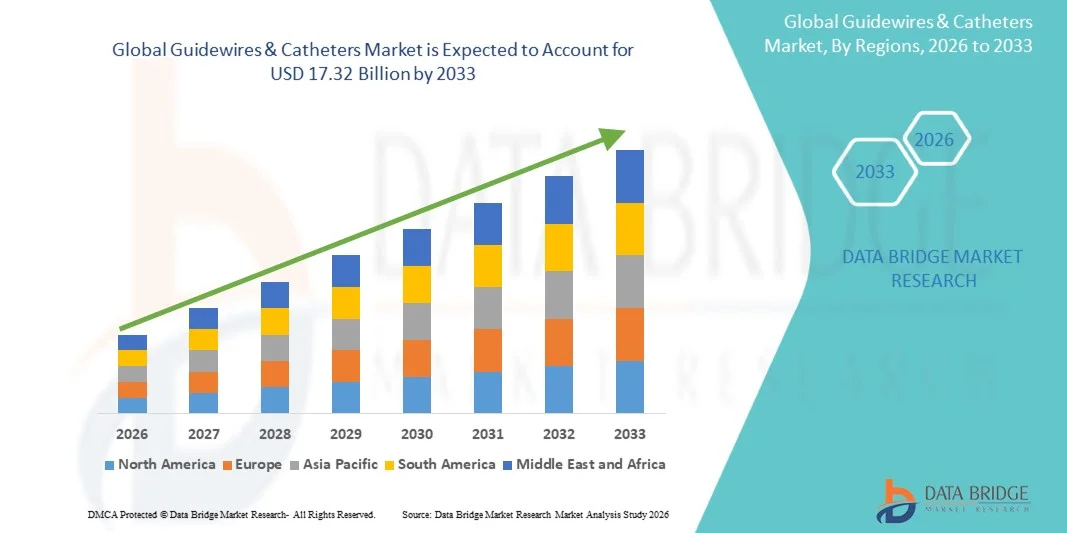

The Guidewires & Catheters Market was valued at USD 9.86 billion in 2025 and is projected to reach USD 17.32 billion by 2033, growing at a CAGR of 7.30% from 2026 to 2033. The market is witnessing steady growth driven by the increasing prevalence of cardiovascular and neurovascular diseases, rising demand for minimally invasive procedures, and continuous advancements in interventional medical technologies.

The growing burden of chronic disorders such as coronary artery disease, peripheral artery disease, and urological conditions, combined with the expanding aging population, is accelerating the adoption of guidewires and catheters across hospitals and specialty care centers. In addition, technological innovations including hydrophilic coatings, steerable guidewires, and advanced catheter navigation systems are improving procedural precision, reducing complications, and enhancing patient outcomes. Increasing investments in healthcare infrastructure, rising surgical volumes, and the growing use of image-guided interventions are further supporting market expansion across developed and emerging economies.

Key Market Trends & Insights

- North America dominated the Guidewires & Catheters Market with the largest revenue share of 38.64% in 2025, supported by a high volume of minimally invasive procedures, advanced healthcare infrastructure, and the strong presence of leading medical device manufacturers.

- The Catheters segment led the market with a 64.38% share in 2025, driven by the increasing number of minimally invasive cardiovascular, neurovascular, and urological procedures performed globally.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by expanding healthcare access, growing medical tourism, and increasing adoption of advanced catheter-based treatments in China, India, and Japan.

- Guidewires are the fastest-growing product type, projected to register a CAGR of 8.2%, reflecting the surge in demand for precision navigation during complex interventional procedures.

- The Stainless Steel segment dominated the material category with a 39.84% revenue share in 2025, led by high strength, durability, cost-effectiveness, and extensive usage across a wide range of interventional devices.

- Cardiology accounted for 34.76% of the market, preferred by the increasing global burden of cardiovascular diseases and rising volumes of angioplasty and cardiac catheterization procedures.

- The Neurology segment is the fastest-growing application category, with a CAGR of 8.7%, driven by the rising incidence of stroke, aneurysms, and other neurovascular disorders globally.

Market Size & Forecast

- Global Market Value (2025): USD 9.86 Billion

- Expected Market Value (2033): USD 17.32 Billion

- Forecast CAGR (2026–2033): 7.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Guidewires & Catheters Market Segmentation

|

Attributes |

Guidewires & Catheters Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Medtronic (Ireland) · Boston Scientific Corporation (U.S.) · Abbott (U.S.) · Terumo Corporation (Japan) · BD (U.S.) · Teleflex Incorporated (U.S.) · Cook (U.S.) · Integer Holdings Corporation (U.S.) · Merit Medical Systems (U.S.) · Asahi Intecc Co., Ltd. (Japan) · Nipro Corporation (Japan) · B. Braun SE (Germany) · Stryker (U.S.) · Cordis (U.S.) · Penumbra, Inc. (U.S.) · MicroPort Scientific Corporation (China) · Biotronik SE & Co. KG (Germany) · AngioDynamics, Inc. (U.S.) · Cardinal Health (U.S.) · Olympus Corporation (Japan) |

|

Market Opportunities |

· Rising adoption of robotic-assisted and image-guided minimally invasive surgeries · Expanding neurovascular intervention procedures for stroke treatment · Increasing healthcare investments and catheterization laboratory expansion |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Guidewires & Catheters Market Trends

Trend: Rising Adoption of Minimally Invasive and Image-Guided Procedures

Healthcare providers are increasingly adopting advanced guidewires and catheters to support minimally invasive procedures that reduce surgical trauma, shorten hospital stays, and improve patient recovery outcomes. The integration of hydrophilic coatings, steerable navigation systems, and enhanced imaging compatibility enables physicians to perform highly precise cardiovascular, neurovascular, and peripheral vascular interventions. Hospitals and specialty centers are similarly expanding catheter-based treatment programs to address rising chronic disease burdens, while robotic-assisted and image-guided technologies create highly controlled procedural environments that closely replicate precision-based interventional workflows.

For instance, in February 2024, Medtronic launched the Cascade Iq aspiration system expansion to strengthen minimally invasive stroke intervention capabilities and improve neurovascular procedural efficiency.

Guidewires & Catheters Market Dynamics

Key Market Driver: Growing Demand for Minimally Invasive Cardiovascular Interventions

The rapid increase in cardiovascular diseases and peripheral vascular disorders has created substantial demand for guidewires and catheters that support minimally invasive diagnostic and therapeutic procedures across healthcare systems worldwide. Hospitals, cardiac centers, and specialty clinics are deploying advanced catheter-based technologies as a core component of interventional treatment pathways, reducing procedural complications, accelerating recovery periods, and improving overall patient outcomes. The growing adoption of angioplasty, electrophysiology, and transcatheter procedures is further driving innovation in steerability, navigation precision, and biocompatible device materials. For instance, in September 2023, Boston Scientific received FDA approval for the AGENT Drug-Coated Balloon, expanding interventional cardiovascular treatment options using catheter-based technology.

Key Restraint/Challenge: High Cost and Complex Regulatory Approval Processes

A significant restraint in the Guidewires & Catheters Market is the high development cost associated with advanced interventional devices and stringent regulatory approval requirements across major healthcare markets worldwide. Modern guidewire and catheter systems integrate specialized coatings, precision-engineered materials, and advanced navigation technologies, demanding substantial investment in research, clinical validation, manufacturing, and long-term quality compliance programs. The total cost burden extends to product testing, physician training, and post-market surveillance obligations, making commercialization difficult for smaller medical device manufacturers and emerging-market suppliers.

For instance, in January 2024, Terumo Corporation expanded investments in interventional device manufacturing and regulatory compliance infrastructure to support global catheter product commercialization initiatives.

Key Market Opportunity: Expansion of Neurovascular and Robotic-Assisted Interventions

The expansion of neurovascular and robotic-assisted intervention platforms presents a significant market opportunity for guidewires and catheters designed for highly precise navigation and complex minimally invasive procedures worldwide. Advanced robotic-assisted systems can improve catheter control, enhance procedural accuracy, and support real-time imaging integration during cardiovascular and neurovascular interventions. The development of AI-assisted navigation technologies and next-generation microcatheters is further expanding access to sophisticated interventional procedures, opening growth opportunities across rapidly developing healthcare markets in Asia-Pacific, Latin America, and the Middle East. For instance, in April 2024, Stryker Corporation expanded its neurovascular product portfolio with advanced catheter technologies to strengthen minimally invasive stroke treatment capabilities.

Guidewires & Catheters Market Scope

The guidewires & catheters market is segmented on the basis of product type, material, application, and end user.

- By Product Type

On the basis of product type, the Guidewires & Catheters Market is segmented into guidewires and catheters. The Catheters segment dominated the market with a 64.38% share in 2025, driven by the increasing number of minimally invasive cardiovascular, neurovascular, and urological procedures performed globally. Catheters are extensively used in diagnostic imaging, drug delivery, electrophysiology, angioplasty, and drainage procedures across hospitals and specialty clinics. Rising prevalence of chronic diseases such as cardiovascular disorders and cancer is significantly boosting demand for advanced catheter-based interventions. Continuous technological advancements including steerable catheters, coated surfaces, and imaging-compatible designs are improving procedural precision and patient safety. The growing expansion of catheterization laboratories and interventional care centers is further strengthening segment growth. Increasing preference for minimally invasive surgeries continues to support the widespread adoption of catheter technologies worldwide.

The Guidewires segment is projected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by increasing demand for precision navigation during complex interventional procedures. Guidewires play a critical role in accessing narrow or blocked vessels during cardiovascular, neurovascular, and peripheral vascular treatments. Advancements in hydrophilic coatings, torque control, and flexible tip technologies are significantly improving maneuverability and procedural outcomes. Growing adoption of robotic-assisted and image-guided interventions is further accelerating the use of high-performance guidewires. Rising incidence of stroke, coronary artery disease, and peripheral artery disease is also contributing to strong segment expansion. Increasing focus on reducing procedural complications and improving minimally invasive treatment success rates continues to create growth opportunities for advanced guidewire products globally.

- By Material

On the basis of material, the Guidewires & Catheters Market is segmented into nitinol, stainless steel, polymer, and hybrid materials. The Stainless Steel segment dominated the market with a 39.84% share in 2025, owing to its high strength, durability, cost-effectiveness, and extensive usage across a wide range of interventional devices. Stainless steel materials provide excellent pushability and torque response, making them highly suitable for cardiovascular and peripheral vascular procedures. Their widespread adoption in standard guidewires and catheter shafts continues to support segment leadership. The material is also preferred due to ease of manufacturing and compatibility with sterilization processes. Strong demand from emerging healthcare markets where affordability remains critical is further supporting market penetration. Continuous improvements in stainless steel device engineering are maintaining its relevance across both diagnostic and therapeutic applications.

The Nitinol segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by increasing demand for highly flexible and kink-resistant interventional devices. Nitinol offers superior shape memory and elasticity properties, enabling improved navigation through complex vascular anatomies. These characteristics make it highly suitable for neurovascular, coronary, and minimally invasive procedures requiring enhanced precision. Growing adoption of advanced microcatheters and steerable guidewires is significantly supporting segment growth. Healthcare providers are increasingly preferring nitinol-based devices due to reduced procedural risks and improved patient outcomes. Rising investments in next-generation interventional technologies and robotic-assisted procedures are further accelerating demand for nitinol materials globally.

- By Application

On the basis of application, the Guidewires & Catheters Market is segmented into cardiology, neurology, peripheral vascular, urology, gastroenterology, oncology, radiology, and electrophysiology. The Cardiology segment dominated the market with a 34.76% revenue share in 2025, driven by the increasing global burden of cardiovascular diseases and rising volumes of angioplasty and cardiac catheterization procedures. Guidewires and catheters are extensively utilized in coronary interventions, diagnostic angiography, electrophysiology mapping, and structural heart procedures. Growing aging populations and lifestyle-related health conditions are significantly increasing demand for interventional cardiology treatments worldwide. Technological advancements in balloon catheters, guiding catheters, and imaging-assisted navigation systems are further enhancing treatment efficiency. Hospitals and cardiac centers continue to expand catheterization laboratory capabilities to manage rising patient volumes. Strong reimbursement support and widespread adoption of minimally invasive cardiac procedures continue to reinforce segment dominance.

The Neurology segment is projected to register the fastest growth at a CAGR of 8.7% from 2026 to 2033, driven by the rising incidence of stroke, aneurysms, and other neurovascular disorders globally. Neurovascular interventions increasingly rely on advanced microcatheters and guidewires capable of navigating highly complex cerebral anatomies. Continuous innovation in flexible catheter systems and steerable guidewire technologies is significantly improving procedural precision and patient safety. Growing awareness regarding early stroke treatment and expanding availability of neurointerventional centers are supporting higher procedure volumes. Increasing adoption of minimally invasive thrombectomy and embolization procedures is further accelerating segment expansion. Government investments in stroke care infrastructure and rapid advancements in neurovascular treatment technologies continue to create strong growth opportunities for this segment.

- By End User

On the basis of end user, the Guidewires & Catheters Market is segmented into hospitals, specialty clinics, ambulatory surgical centers, diagnostic centers, and catheterization laboratories. The Hospitals segment dominated the market with a 54.92% share in 2025, owing to the large volume of interventional procedures performed in hospital-based settings worldwide. Hospitals possess advanced imaging infrastructure, skilled interventional specialists, and comprehensive emergency care capabilities required for complex cardiovascular and neurovascular treatments. Rising patient admissions related to chronic diseases and surgical interventions are significantly increasing utilization of guidewires and catheters. Large hospitals are also investing heavily in catheterization laboratories and minimally invasive surgical programs to improve treatment efficiency. The availability of reimbursement coverage and integrated multidisciplinary care further strengthens hospital-based procedure adoption. Increasing expansion of tertiary healthcare infrastructure continues to support the segment’s leading market position globally.

The Ambulatory Surgical Centers segment is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033, driven by increasing preference for cost-effective and outpatient minimally invasive procedures. These centers offer shorter patient stays, reduced treatment costs, and faster procedural turnaround times compared to traditional hospital settings. Growing advancements in compact imaging systems and portable interventional technologies are enabling wider adoption of catheter-based procedures within ambulatory facilities. Healthcare providers are increasingly shifting suitable cardiovascular and diagnostic procedures toward outpatient environments to improve operational efficiency. Rising patient preference for convenient and same-day treatment options is also supporting segment expansion. Expanding healthcare infrastructure and increasing investments in outpatient surgical care continue to create strong growth opportunities for ambulatory surgical centers worldwide.

Guidewires & Catheters Market Regional Analysis

North America dominated the Guidewires & Catheters Market with the largest revenue share of 38.64% in 2025, supported by a high volume of minimally invasive procedures, advanced healthcare infrastructure, and the strong presence of leading medical device manufacturers. The region also benefits from increasing prevalence of cardiovascular and neurovascular disorders, favorable reimbursement frameworks, and rapid adoption of technologically advanced interventional devices across hospitals and specialty care centers. Growing investments in catheterization laboratories, rising demand for image-guided procedures, and continuous innovation in guidewire and catheter technologies continue to strengthen North America’s leadership position in the global market.

U.S. Guidewires & Catheters Market Insight

The U.S. guidewires & catheters market is witnessing strong growth due to rising prevalence of cardiovascular diseases, increasing adoption of minimally invasive procedures, and growing investments in advanced interventional healthcare technologies. The country’s well-established healthcare infrastructure, along with rapid adoption of image-guided, robotic-assisted, and technologically advanced catheter systems, is driving demand across hospitals, specialty clinics, and cardiac centers. In addition, growing emphasis on improving procedural outcomes and reducing hospital stays is accelerating the adoption of advanced guidewires and catheters across the U.S. healthcare sector.

Europe Guidewires & Catheters Market Insight

The Europe guidewires & catheters market remains a major contributor to global revenue, driven by advanced healthcare systems, strong medical technology innovation, and increasing demand for minimally invasive treatment solutions. The widespread use of guidewires and catheters in cardiovascular, neurovascular, and urological procedures is supporting market expansion across the region. Increasing investments in catheterization laboratories, coupled with rising chronic disease prevalence and favorable healthcare reimbursement systems, continue to enhance the adoption of guidewires and catheters throughout Europe.

U.K. Guidewires & Catheters Market Insight

The U.K. guidewires & catheters market is experiencing steady growth, supported by increasing adoption of minimally invasive procedures, rising healthcare investments, and growing demand for advanced interventional technologies. Expanding use of catheter-based treatments in cardiology, neurology, and radiology applications is contributing significantly to market growth. Furthermore, integration of advanced imaging technologies, robotic-assisted interventions, and precision navigation systems is improving procedural efficiency and patient outcomes, positioning the U.K. as an important innovation center in the guidewires & catheters industry.

Germany Guidewires & Catheters Market Insight

The Germany guidewires & catheters market is expanding steadily due to the country’s advanced healthcare infrastructure, strong medical device manufacturing capabilities, and increasing adoption of next-generation interventional technologies. Hospitals, cardiac centers, and specialty clinics are increasingly utilizing advanced guidewires and catheters for minimally invasive diagnostic and therapeutic procedures. Continuous advancements in catheter design, imaging integration, and neurovascular intervention technologies, along with strong government support for healthcare innovation, are further driving market growth in Germany.

Asia-Pacific Guidewires & Catheters Market Insight

The Asia-Pacific guidewires & catheters market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising prevalence of chronic diseases, and increasing investments in minimally invasive treatment capabilities across countries such as China, India, and Japan. Growing awareness regarding early disease diagnosis, rising adoption of advanced interventional devices, and increasing demand for cost-effective treatment solutions are supporting regional market expansion. In addition, the growing presence of medical device manufacturers and improving access to specialized healthcare services are accelerating guidewire and catheter adoption across the region.

Japan Guidewires & Catheters Market Insight

The Japan guidewires & catheters market is witnessing consistent growth due to rising investments in advanced healthcare technologies, increasing cardiovascular procedure volumes, and growing focus on minimally invasive treatment approaches. Hospitals, research institutes, and specialty care centers are increasingly adopting high-precision guidewires and catheters for interventional cardiology, neurovascular, and radiology procedures. Moreover, increasing integration of robotic-assisted technologies and the country’s emphasis on improving healthcare efficiency and patient safety are further contributing to market growth.

China Guidewires & Catheters Market Insight

The China guidewires & catheters market is growing rapidly, driven by expanding healthcare infrastructure, rising prevalence of cardiovascular diseases, and increasing government focus on improving access to advanced medical treatments. Growing adoption of technologically advanced guidewire and catheter systems across hospitals and specialty centers is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing awareness regarding minimally invasive procedures, and rapid advancements in interventional medical technologies are positioning China as one of the fastest-growing markets for guidewires & catheters globally.

Guidewires & Catheters Market Share

The guidewires & catheters industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific Corporation (U.S.)

- Abbott (U.S.)

- Terumo Corporation (Japan)

- BD (U.S.)

- Teleflex Incorporated (U.S.)

- Cook (U.S.)

- Integer Holdings Corporation (U.S.)

- Merit Medical Systems (U.S.)

- Asahi Intecc Co., Ltd. (Japan)

- Nipro Corporation (Japan)

- Braun SE (Germany)

- Stryker (U.S.)

- Cordis (U.S.)

- Penumbra, Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- Biotronik SE & Co. KG (Germany)

- AngioDynamics, Inc. (U.S.)

- Cardinal Health (U.S.)

- Olympus Corporation (Japan)

Latest Developments in Guidewires & Catheters Market

- In October 2025, Medtronic announced the launch of the Stedi™ Extra Support Guidewire, designed to improve stability, safety, and predictability during transcatheter aortic valve replacement (TAVR) procedures. The guidewire is compatible with all commercially available TAVR systems and enhances deployment performance for patients with severe aortic stenosis. This launch underscores Medtronic’s continued investment in next-generation guidewire technologies aimed at improving minimally invasive cardiovascular intervention outcomes.

- In October 2025, Terumo Corporation announced the launch of the FineCross™ M3 Coronary Micro-Guide Catheter in India to support complex percutaneous coronary intervention procedures. The device features enhanced crossability, guidewire support, hydrophilic coating technology, and improved navigability for challenging coronary lesions. The launch highlights growing demand for advanced microcatheters and precision-based cardiovascular intervention technologies across emerging healthcare markets

- In April 2025, Teleflex announced that it received FDA 510(k) clearance for the AC3 Range™ Intra-Aortic Balloon Pump (IABP), designed to provide reliable cardiac support during patient transport across ambulances and aircraft systems. The device integrates advanced timing algorithms, dual power options, and enhanced mobility features to improve critical cardiovascular care during emergency transfers. The launch strengthens Teleflex’s interventional cardiology portfolio and highlights the growing focus on advanced catheter-based circulatory support technologies in acute care settings

- In February 2025, Boston Scientific announced the first-in-human procedures using its next-generation Faraflex pulsed-field ablation (PFA) and mapping catheter, developed for advanced atrial fibrillation treatment procedures. The investigational catheter combines high-density mapping capabilities with pulsed-field ablation technology to improve procedural precision and workflow efficiency. The development reflects increasing innovation in electrophysiology catheters and growing industry focus on minimally invasive cardiac rhythm management solutions

- In January 2024, Catheter Precision, Inc. announced its participation in the AF Symposium conference to showcase its electrophysiology product portfolio, including the VIVO mapping system and LockeT suture retention device. The event highlighted increasing advancements in catheter-based electrophysiology technologies and growing collaboration between medical device companies and healthcare professionals to improve cardiac arrhythmia treatment procedures. The development also emphasized rising investment in innovation and physician-focused interventional training initiatives

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.