Global Guidewires For Cardiovascular Procedures Market

Market Size in USD Billion

USD

1.78 Billion

USD

2.75 Billion

2025

2033

USD

1.78 Billion

USD

2.75 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.78 Billion | |

| USD 2.75 Billion | |

| % | |

|

Guidewires for Cardiovascular Procedures Market Size

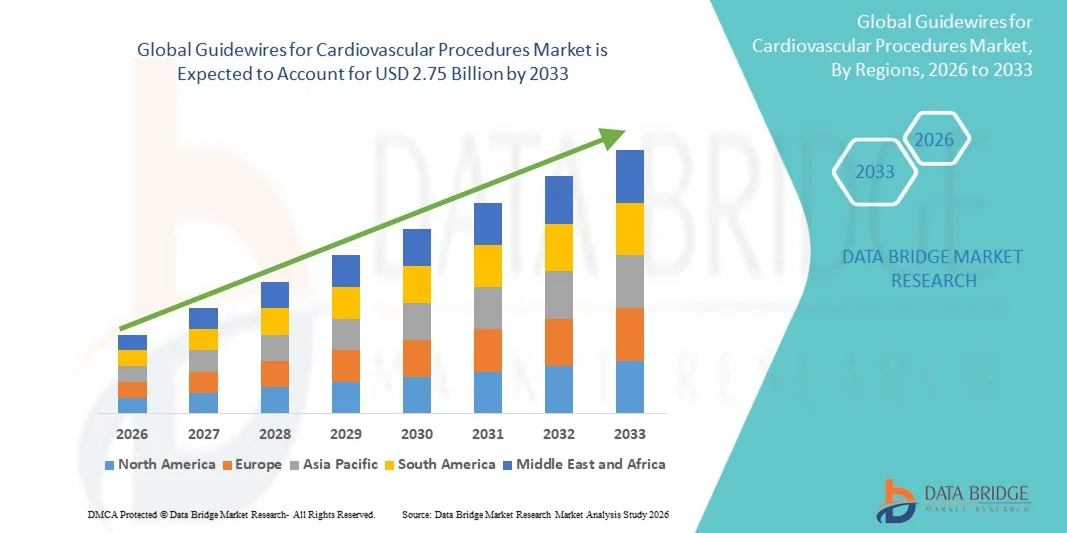

- The global guidewires for cardiovascular procedures market size was valued at USD 1.78 billion in 2025and is expected to reach USD 2.75 billion by 2033, at a CAGR of 5.5% during the forecast period

- Market growth is primarily driven by the rising incidence of cardiovascular diseases (CVDs), increasing adoption of minimally invasive procedures, and continuous advancements in interventional cardiology and neurovascular navigation technologies.

- In addition, the growing geriatric population, expansion of catheter-based procedures, and improved healthcare infrastructure in emerging economies are significantly contributing to sustained demand for advanced guidewire systems worldwide.

Guidewires for Cardiovascular Procedures Market Analysis

- Guidewires are critical components in minimally invasive vascular procedures, enabling precise navigation of catheters through complex vascular anatomy in coronary, peripheral, and neurovascular interventions. Their flexibility, torque control, and tip design significantly influence procedural success and patient safety.

- The increasing burden of coronary artery disease, stroke, and peripheral artery disease is accelerating the use of guidewires across hospitals and interventional centers globally.

- Technological advancements such as hydrophilic coatings, hybrid core materials, and shapeable nitinol-based guidewires are enhancing trackability, lesion crossing ability, and procedural efficiency.

- North America dominated the market with the largest revenue share of 42% in 2025, supported by high procedural volumes, advanced cath lab infrastructure, and strong adoption of innovative interventional devices.

- Asia-Pacific is expected to be the fastest-growing region during the forecast period with a CAGR of 7.8%, driven by increasing healthcare investment, rising cardiovascular disease prevalence, and expanding access to interventional procedures.

- The coronary guidewires segment dominated the market with the largest revenue share of 48% in 2025, driven by the high volume of percutaneous coronary interventions (PCI) performed globally for coronary artery disease management. Coronary guidewires are widely preferred due to their high precision, superior navigability, and compatibility with a broad range of interventional cardiology devices. Increasing prevalence of ischemic heart disease, growing geriatric population, and rising adoption of minimally invasive cardiac procedures further reinforce segment dominance. Continuous innovation in tip design, torque response, and hydrophilic coating technologies is also strengthening clinical adoption across advanced cath labs.

Report Scope and Guidewires for Cardiovascular Procedures Market Segmentation

|

Attributes |

Guidewires for cardiovascular procedures Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of minimally invasive cardiovascular and neurovascular procedures · Rising adoption of advanced hybrid and shapeable guidewire technologies · Growth in ambulatory surgical centers and catheterization labs in emerging markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Guidewires for Cardiovascular Procedures Market Trends

“Shift Toward Advanced, Torque-Controlled, and Hydrophilic Guidewire Technologies”

- A key trend shaping the market is the increasing adoption of high-performance guidewires designed for complex lesion navigation and improved procedural precision.

- Hydrophilic-coated and dual-coated guidewires are gaining strong traction due to reduced friction, better vessel tracking, and improved safety in tortuous anatomies.

- Manufacturers are focusing on hybrid core technologies combining nitinol flexibility with stainless steel strength to improve torque response and pushability.

- Growing demand for neurovascular guidewires is also being driven by rising stroke intervention procedures and expanding mechanical thrombectomy adoption.

- Integration of advanced tip shaping and radiopacity enhancements is improving visualization and procedural control during complex interventions.

Guidewires for Cardiovascular Procedures Market Dynamics

Driver

“Rising Burden of Cardiovascular and Neurovascular Diseases”

- The increasing prevalence of coronary artery disease, stroke, and peripheral artery disease is a major driver of guidewire demand globally.

- Expanding use of minimally invasive procedures such as angioplasty and stenting is accelerating guidewire utilization across hospitals and specialty centers.

- Aging populations and lifestyle-related risk factors such as hypertension, diabetes, and obesity are significantly contributing to higher intervention volumes.

- Growing adoption of catheter-based therapies in both developed and emerging economies is further strengthening market growth.

Restraint/Challenge

“High Cost of Advanced Guidewire Systems and Procedural Complexity”

- Premium guidewires with advanced coatings and hybrid materials are relatively expensive, limiting adoption in cost-sensitive healthcare systems.

- Technical complexity associated with neurovascular and chronic total occlusion (CTO) procedures requires highly skilled operators, restricting broader usage.

- Variability in device performance across anatomical conditions may impact procedural outcomes.

- Limited reimbursement coverage in developing regions can also restrict adoption of advanced interventional guidewire technologies.

Guidewires for Cardiovascular Procedures Market Scope

The market is segmented on the basis of product type, material, coating type, application, and end user.

- By Product

On the basis of product type, the global guidewires for cardiovascular procedures market is segmented into coronary guidewires, peripheral guidewires, neurovascular guidewires, urology guidewires, and others. The coronary guidewires segment dominated the market with the largest revenue share of 48% in 2025, driven by the high volume of percutaneous coronary interventions (PCI) performed globally for coronary artery disease management. Coronary guidewires are widely preferred due to their high precision, superior navigability, and compatibility with a broad range of interventional cardiology devices. Increasing prevalence of ischemic heart disease, growing geriatric population, and rising adoption of minimally invasive cardiac procedures further reinforce segment dominance. Continuous innovation in tip design, torque response, and hydrophilic coating technologies is also strengthening clinical adoption across advanced cath labs.

The neurovascular guidewires segment is expected to witness the fastest growth during the forecast period, fueled by rising stroke incidence and increasing adoption of mechanical thrombectomy procedures. Growing demand for minimally invasive neurovascular interventions, coupled with advancements in micro-navigation technologies and improved device flexibility, is accelerating segment expansion. Expanding stroke care infrastructure and rising awareness regarding early intervention in emerging economies further support growth in this segment.

- By Material

On the basis of material, the market is segmented into nitinol (nickel-titanium alloy), stainless steel, and hybrid materials. The nitinol segment dominated the market in 2025, attributed to its superior flexibility, shape memory properties, and excellent kink resistance, making it highly suitable for complex vascular anatomies. Nitinol guidewires are widely used in both coronary and neurovascular procedures due to their enhanced maneuverability and safety profile.

The hybrid materials segment is expected to grow at the fastest rate, driven by increasing demand for guidewires that combine flexibility, strength, and improved torque control. Hybrid designs are gaining traction in complex interventions requiring high precision and durability across tortuous vascular pathways.

- By Coating Type

On the basis of coating type, the market is segmented into hydrophilic coated guidewires, hydrophobic coated guidewires, dual-coated guidewires, and non-coated guidewires. The hydrophilic coated segment dominated the market in 2025, driven by its superior lubricity, reduced friction, and improved navigation through complex vasculature. These guidewires are widely used in coronary and peripheral interventions where smooth vessel crossing is critical for procedural success.

The dual-coated guidewires segment is expected to witness the fastest growth during the forecast period, supported by rising demand for enhanced performance in complex and chronic total occlusion (CTO) procedures. Dual coatings offer a balance of lubricity and control, improving both pushability and tactile feedback.

- By Application

On the basis of application, the market is segmented into peripheral vascular interventions, neurovascular procedures, urology procedures, gastroenterology, and others. The peripheral vascular interventions segment dominated the market in 2025, driven by the rising prevalence of peripheral artery disease (PAD) and increasing adoption of endovascular treatment approaches. Guidewires are essential in these procedures for accessing and treating blocked or narrowed blood vessels.

The neurovascular procedures segment is expected to grow at the fastest pace, fueled by increasing incidence of stroke and expanding adoption of mechanical thrombectomy and aneurysm repair procedures. Technological advancements in micro-guidewire design are further accelerating procedural success rates in neurovascular interventions.

- By End User

On the basis of end user, the market is segmented into hospitals, ambulatory surgical centers (ASCs), specialty/interventional cardiology centers, and diagnostic centers. The hospitals segment dominated the market in 2025, supported by high patient inflow for cardiovascular emergencies, advanced cath lab infrastructure, and availability of skilled interventional cardiologists. Hospitals remain the primary setting for complex coronary, neurovascular, and peripheral interventions requiring guidewire usage.

The ambulatory surgical centers (ASCs) segment is expected to witness the fastest growth during the forecast period, driven by increasing shift toward outpatient minimally invasive procedures, cost-effectiveness, and shorter recovery times. Rising preference for same-day cardiovascular interventions is further supporting adoption in ASCs globally.

Guidewires for Cardiovascular Procedures Market Regional Analysis

- North America dominated the market with the largest revenue share of 42% in 2025, supported by high procedural volumes, advanced cath lab infrastructure, and strong adoption of innovative interventional devices.

- The region benefits from a well-established reimbursement framework for cardiovascular interventions, encouraging widespread use of advanced guidewire technologies across hospitals and specialty cardiac centers.

- Strong presence of leading medical device manufacturers and continuous product innovation in minimally invasive cardiovascular solutions further reinforce North America’s market leadership.

U.S. Guidewires for Cardiovascular Procedures Market Insight

The U.S. guidewires for cardiovascular procedures market is driven by high procedural volumes for percutaneous coronary interventions (PCI), strong adoption of minimally invasive cardiovascular therapies, and advanced cath lab infrastructure. The country benefits from a robust reimbursement system supporting interventional cardiology procedures and early adoption of innovative guidewire technologies, including hydrophilic and nitinol-based systems. In addition, the strong presence of leading medical device manufacturers and continuous clinical advancements in coronary and neurovascular interventions are further accelerating market growth across hospitals and specialty cardiac centers.

Europe Guidewires for Cardiovascular Procedures Market Insight

The Europe guidewires market is witnessing steady growth, supported by increasing prevalence of cardiovascular diseases, aging populations, and well-established interventional cardiology networks. Hospitals across the region are increasingly adopting advanced guidewire technologies to improve procedural precision and patient outcomes. Strong regulatory standards, combined with rising investments in minimally invasive cardiovascular treatments and growing emphasis on early diagnosis, are further supporting market expansion across major European healthcare systems.

U.K. Guidewires for Cardiovascular Procedures Market Insight

The U.K. guidewires market is expanding due to increasing cardiovascular disease burden and strong national focus on minimally invasive treatment approaches. The National Health Service (NHS) is actively promoting early diagnosis and catheter-based interventions, driving demand for advanced guidewires in coronary and peripheral procedures. Growing adoption of innovative interventional devices, along with improved access to specialized cardiac care centers, is further supporting market growth across the country.

Germany Guidewires for Cardiovascular Procedures Market Insight

The Germany guidewires market is growing steadily, supported by strong healthcare infrastructure and high adoption of precision-driven interventional cardiology techniques. The country’s focus on technologically advanced medical devices and early disease detection is driving demand for high-performance guidewires in coronary and neurovascular procedures. Increasing procedural volumes for cardiovascular interventions, along with a strong emphasis on clinical efficiency and safety, is further reinforcing market expansion.

Asia-Pacific Guidewires for Cardiovascular Procedures Market Insight

The Asia-Pacific guidewires market is expected to grow at the fastest rate, driven by rising cardiovascular disease prevalence, increasing healthcare investments, and expanding access to interventional procedures. Rapid urbanization, improving hospital infrastructure, and growing awareness of minimally invasive treatments are significantly boosting demand. Government initiatives to strengthen cardiac care services and the expansion of catheterization laboratories in emerging economies are further accelerating market growth across the region.

Japan Guidewires for Cardiovascular Procedures Market Insight

The Japan guidewires market is driven by a rapidly aging population and high prevalence of cardiovascular and cerebrovascular diseases. The country’s advanced healthcare system and strong focus on precision medicine are supporting widespread adoption of high-performance guidewires. Increasing use of minimally invasive procedures and continuous innovation in neurovascular and coronary intervention technologies are further strengthening market growth in hospitals and specialized cardiac centers.

India Guidewires for Cardiovascular Procedures Market Insight

The India guidewires market is expanding rapidly due to rising incidence of cardiovascular diseases, increasing healthcare awareness, and improving access to interventional cardiology services. Growing investments in hospital infrastructure and expansion of cath lab facilities are driving procedural volumes across urban and semi-urban regions. In addition, the availability of cost-effective medical devices from domestic manufacturers and government initiatives to strengthen cardiac care are further supporting strong market growth in the country.

Guidewires for Cardiovascular Procedures Market Share

The Guidewires for cardiovascular procedures industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Abbott Laboratories (U.S.)

- Medtronic plc (Ireland)

- Terumo Corporation (Japan)

- B. Braun Melsungen AG (Germany)

- Cook Medical (U.S.)

- Cardinal Health (U.S.)

- Asahi Intecc Co., Ltd. (Japan)

- Teleflex Incorporated (U.S.)

- Merit Medical Systems (U.S.)

- MicroPort Scientific Corporation (China)

- Penumbra, Inc. (U.S.)

- Kaneka Corporation (Japan)

- Lepu Medical Technology (China)

What are the Recent Developments in Global Guidewires for Cardiovascular Procedures Market?

- In October 2025, Boston Scientific Corporation announced the global launch of its Journey Guidewire for peripheral angioplasty procedures, designed to improve torque response, flexibility, and lesion-crossing capability in small and complex vessel anatomies, strengthening its endovascular portfolio for peripheral interventions.

- In April 2025, Boston Scientific Corporation introduced its Kinetix coronary guidewire for PCI procedures, featuring a micro-cut nitinol sleeve that enhances torque control and deliverability, marking a major advancement in coronary guidewire performance and procedural precision.

- In 2025, Abbott Laboratories strengthened its interventional cardiology portfolio with continued advancement of its coronary guidewire systems, focusing on improved lesion-crossing capability and compatibility with complex PCI procedures, reinforcing its leadership in the coronary guidewire segment.

- In 2025, Medtronic plc expanded its cardiovascular guidewire technologies across coronary, peripheral, and neurovascular applications, emphasizing improved navigation efficiency and safety in minimally invasive interventions supported by rising global demand for catheter-based therapies.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.