Global Gynecological Cancers Market

Market Size in USD Billion

USD

18.50 Billion

USD

42.63 Billion

2025

2033

USD

18.50 Billion

USD

42.63 Billion

2025

2033

| 2026 - 2033 | |

| USD 18.50 Billion | |

| USD 42.63 Billion | |

| % | |

|

Gynecological Cancers Market Size

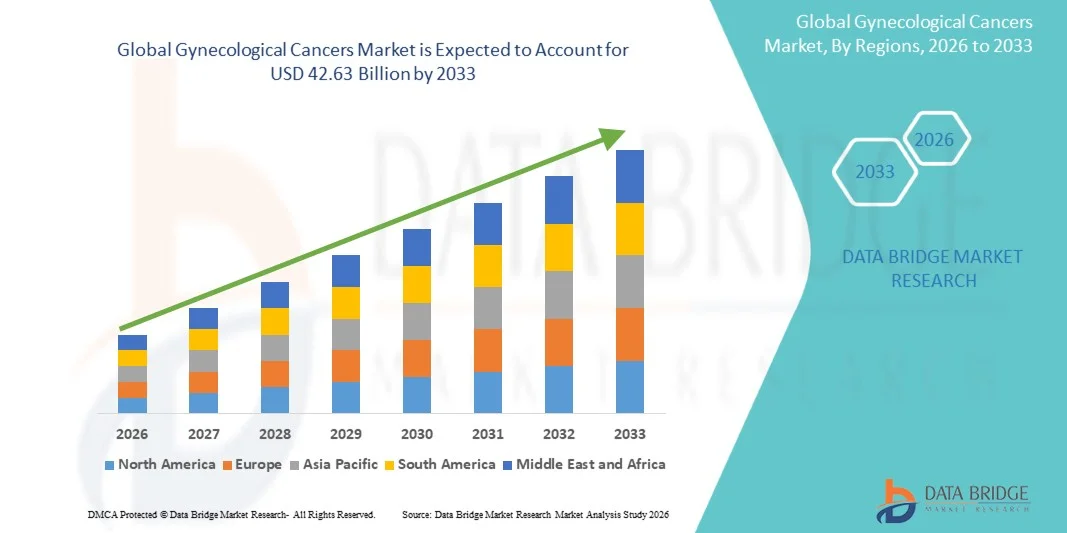

- The global gynecological cancers market size was valued at USD 18.50 billion in 2025 and is expected to reach USD 42.63 billion by 2033, at a CAGR of 11.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of gynecological malignancies such as ovarian, cervical, and uterine cancers, along with continuous advancements in oncology therapeutics, including targeted therapy, immunotherapy, and precision medicine approaches

- Furthermore, rising awareness regarding early cancer screening, improving healthcare infrastructure, and growing demand for effective, patient-centric treatment solutions are establishing gynecological cancer therapies as a critical component of modern oncology care. These converging factors are accelerating the adoption of advanced treatment options, thereby significantly boosting the industry's growth

Gynecological Cancers Market Analysis

- Gynecological cancers, including ovarian, cervical, uterine, vaginal, and vulvar cancers, represent a significant segment of the global oncology landscape, with growing importance in healthcare systems due to rising incidence rates and the need for advanced, targeted treatment approaches across both developed and emerging economies

- The escalating demand in the gynecological cancers market is primarily fueled by the increasing global burden of cancer, advancements in diagnostic technologies, and the rapid development of innovative therapies such as immunotherapy, targeted drugs, and personalized medicine, improving patient outcomes and survival rates

- North America dominated the gynecological cancers market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong adoption of novel therapeutics, with the U.S. witnessing substantial growth driven by robust research activities, favorable reimbursement policies, and the presence of major pharmaceutical companies focusing on oncology innovation

- Asia-Pacific is expected to be the fastest growing region in the gynecological cancers market during the forecast period due to increasing healthcare expenditure, improving access to cancer screening programs, and a rising patient population across countries such as China and India

- The ovarian cancer segment dominated the gynecological cancers market with a market share of 41.8% in 2025, driven by its high prevalence, severity, and the increasing focus on developing targeted therapies and early detection methods to improve clinical outcomes

Report Scope and Gynecological Cancers Market Segmentation

|

Attributes |

Gynecological Cancers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Gynecological Cancers Market Trends

“Advancement of Targeted Therapies and Precision Oncology”

- A significant and accelerating trend in the global gynecological cancers market is the increasing adoption of targeted therapies and precision medicine approaches, supported by advancements in molecular diagnostics and genomic profiling technologies. This integration is significantly improving treatment outcomes and patient-specific care strategies

- For instance, PARP inhibitors such as olaparib and niraparib are widely used in ovarian cancer treatment, offering targeted action based on BRCA mutation status. Similarly, pembrolizumab is utilized in advanced cervical and endometrial cancers, enhancing survival outcomes through immunotherapy-based approaches

- The integration of precision oncology enables clinicians to tailor treatment plans based on genetic mutations and tumor characteristics, improving therapeutic efficacy and reducing adverse effects. For instance, biomarker-driven therapies are increasingly used to identify patients who are most likely to benefit from specific drugs, thereby optimizing clinical outcomes and resource utilization. Furthermore, advancements in immunotherapy are providing durable responses in certain cancer subtypes

- The growing incorporation of advanced diagnostics and targeted treatments facilitates a more personalized and efficient cancer care pathway. Through integrated healthcare systems, patients can access early detection, molecular testing, and tailored therapies, creating a more comprehensive oncology care framework

- This trend toward more precise, patient-centric, and technologically advanced treatment solutions is fundamentally transforming gynecological cancer management. Consequently, companies such as Roche and AstraZeneca are developing innovative targeted therapies and companion diagnostics to enhance treatment effectiveness and expand therapeutic options

- The demand for advanced targeted therapies and precision medicine solutions is increasing rapidly across both developed and emerging markets, as healthcare providers prioritize improved survival rates and personalized treatment approaches

Gynecological Cancers Market Dynamics

Driver

“Rising Disease Burden and Increasing Adoption of Advanced Therapies”

- The increasing prevalence of gynecological cancers worldwide, coupled with the growing adoption of advanced therapeutic solutions, is a significant driver for the heightened demand for effective treatment options

- For instance, in recent years, pharmaceutical companies such as GlaxoSmithKline and Merck & Co. have expanded their oncology pipelines with innovative drugs targeting ovarian and cervical cancers, supporting improved treatment accessibility and outcomes

- As awareness regarding early diagnosis and treatment continues to rise, patients and healthcare providers are increasingly opting for advanced therapies, including immunotherapy and targeted treatments, which offer improved efficacy compared to conventional chemotherapy

- Furthermore, the expansion of cancer screening programs and government initiatives aimed at reducing cancer burden are contributing to increased diagnosis rates and timely intervention, supporting market growth

- The growing investments in oncology research and development by pharmaceutical and biotechnology companies are significantly driving innovation and expanding the availability of novel treatment options in the market

- The rising adoption of combination therapies, which integrate chemotherapy, immunotherapy, and targeted treatments, is improving clinical efficacy and boosting demand for advanced gynecological cancer therapeutics

- The availability of novel treatment options, improved healthcare infrastructure, and the integration of digital health technologies are key factors propelling the adoption of gynecological cancer therapies across hospitals and specialty clinics. The growing focus on personalized medicine and patient-centric care further strengthens market expansion

Restraint/Challenge

“High Treatment Costs and Limited Access in Developing Regions”

- The high cost associated with advanced gynecological cancer treatments, including targeted therapies and immunotherapies, poses a significant challenge to widespread market adoption. These treatments often require substantial financial resources, limiting accessibility for patients in low- and middle-income regions

- For instance, the cost of PARP inhibitors and immunotherapy drugs can be significantly higher than traditional chemotherapy, making them less accessible in regions with limited healthcare funding and insurance coverage

- Addressing these cost-related challenges through pricing strategies, government support, and expansion of insurance coverage is essential for improving patient access. Companies such as Bristol Myers Squibb and AstraZeneca are focusing on expanding access programs and partnerships to improve affordability and availability of advanced therapies

- In addition, disparities in healthcare infrastructure and limited availability of specialized oncology services in developing regions further restrict timely diagnosis and treatment. While developed markets benefit from advanced medical facilities, many emerging economies still face challenges in providing comprehensive cancer care

- The lack of awareness and limited participation in regular screening programs in developing regions continues to hinder early diagnosis, leading to late-stage detection and reduced treatment effectiveness

- Stringent regulatory approval processes and the complexity of clinical trials for oncology drugs can delay product launches, thereby restricting the timely availability of innovative therapies in the market

- Overcoming these challenges through cost optimization, improved healthcare access, and strengthening oncology care infrastructure will be critical for ensuring sustainable growth in the gynecological cancers market

Gynecological Cancers Market Scope

The market is segmented on the basis of type, treatment type, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the gynecological cancers market is segmented into uterine cancer, ovarian cancer, cervical cancer, vaginal cancer, and others. The ovarian cancer segment dominated the market with the largest market revenue share of 41.8% in 2025, driven by its high mortality rate and increasing focus on advanced therapeutic development. Ovarian cancer often presents at a late stage, leading to a higher demand for effective treatment options such as targeted therapies and immunotherapies. The segment also benefits from growing research investments and the availability of novel drugs, including PARP inhibitors. In addition, the rising incidence of ovarian cancer globally and increasing awareness regarding early diagnosis are further supporting segment growth. The availability of combination treatment approaches and personalized medicine is also strengthening its dominance in the market.

The cervical cancer segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing awareness programs and expanding screening initiatives across developing regions. Government-led vaccination campaigns for HPV prevention are significantly contributing to early detection and reduced disease burden. The segment is also benefiting from advancements in immunotherapy and targeted treatment options, improving patient outcomes. Increasing healthcare access and improving diagnostic infrastructure in emerging economies are further driving growth. In addition, global initiatives by health organizations to eliminate cervical cancer are expected to accelerate the demand for effective treatment solutions.

- By Treatment Type

On the basis of treatment type, the gynecological cancers market is segmented into chemotherapy, targeted therapy, and others. The chemotherapy segment dominated the market with the largest revenue share in 2025, primarily due to its widespread use as a standard treatment option across multiple gynecological cancers. Chemotherapy remains a first-line treatment, especially in advanced-stage cancers, due to its broad applicability and established clinical efficacy. The segment is supported by its relatively lower cost compared to advanced therapies and its availability across healthcare settings. In addition, chemotherapy is often used in combination with other treatment modalities, further sustaining its demand. The continued use of platinum-based drugs in ovarian and cervical cancer treatment significantly contributes to segment dominance.

The targeted therapy segment is expected to witness the fastest CAGR from 2026 to 2033, driven by increasing adoption of precision medicine and advancements in molecular diagnostics. Targeted therapies offer improved efficacy with fewer side effects compared to traditional chemotherapy, making them highly preferred in modern oncology practices. The development of drugs such as PARP inhibitors and angiogenesis inhibitors is significantly boosting segment growth. In addition, the growing focus on biomarker-based treatment selection is enhancing clinical outcomes. Rising investments in oncology R&D and regulatory approvals of novel targeted drugs are further accelerating segment expansion.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest revenue share in 2025, driven by the widespread use of intravenous therapies in hospital settings. Most chemotherapy and biologic drugs are administered through parenteral routes, ensuring rapid drug delivery and controlled dosing. This route is particularly preferred for advanced-stage cancers requiring immediate and intensive treatment. The dominance of hospital-based cancer care and the availability of skilled healthcare professionals further support segment growth. In addition, the increasing use of injectable targeted therapies and immunotherapies is strengthening the segment’s position.

The oral segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing patient preference for convenient and non-invasive treatment options. Oral therapies enable at-home treatment, reducing the need for frequent hospital visits and improving patient compliance. The growing availability of oral targeted therapies and hormonal treatments is significantly contributing to segment expansion. In addition, advancements in drug formulation technologies are enhancing the efficacy of oral medications. The shift toward patient-centric care and home-based treatment models is further accelerating the adoption of oral therapies.

- By End-Users

On the basis of end-users, the gynecological cancers market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the availability of advanced diagnostic and treatment facilities. Hospitals serve as primary centers for cancer diagnosis, surgery, chemotherapy, and radiation therapy, making them a key contributor to market revenue. The presence of skilled oncology professionals and access to multidisciplinary care further strengthen the segment. In addition, hospitals are often equipped with advanced technologies required for complex cancer treatments. Increasing patient inflow and rising hospitalization rates for cancer care are also supporting segment dominance.

The homecare segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the growing preference for home-based treatment and supportive care services. Advances in oral therapies and remote patient monitoring technologies are enabling effective cancer management at home. Homecare reduces treatment costs and improves patient comfort, making it an attractive option for long-term care. In addition, the increasing aging population and rising burden of chronic diseases are driving demand for home-based healthcare solutions. The shift toward decentralized healthcare delivery models is further boosting segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2025, driven by the high volume of cancer treatments administered in hospital settings. Hospital pharmacies play a crucial role in dispensing specialized oncology drugs, including chemotherapy and biologics. The availability of prescription-based high-cost drugs and controlled distribution channels further support segment growth. In addition, hospitals ensure proper storage and handling of sensitive medications, maintaining treatment efficacy. The strong integration between hospitals and pharmacies enhances patient access to required therapies.

The online pharmacy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing digitalization and the growing adoption of e-commerce platforms in healthcare. Online pharmacies offer convenience, home delivery, and access to a wide range of medications, making them increasingly popular among patients. The rise in internet penetration and smartphone usage is further driving segment growth. In addition, online platforms often provide competitive pricing and discounts, attracting cost-sensitive consumers. The shift toward digital healthcare ecosystems is significantly accelerating the expansion of online pharmacy channels.

Gynecological Cancers Market Regional Analysis

- North America dominated the gynecological cancers market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong adoption of novel therapeutics

- Patients in the region highly benefit from the availability of innovative therapies, early screening programs, and access to specialized oncology care, improving survival rates and treatment outcomes across various gynecological cancers

- This widespread growth is further supported by favorable reimbursement policies, strong presence of leading pharmaceutical companies, and continuous research and development activities, establishing advanced cancer therapies as a preferred treatment approach for both patients and healthcare providers

U.S. Gynecological Cancers Market Insight

The U.S. gynecological cancers market captured the largest revenue share of 80% in 2025 within North America, fueled by the high prevalence of cancer cases and the strong presence of advanced healthcare infrastructure. Patients are increasingly prioritizing early diagnosis and access to innovative treatment options, including targeted therapy and immunotherapy. The growing preference for precision medicine approaches, combined with robust clinical research and oncology drug pipelines, further propels the market. Moreover, the increasing integration of advanced diagnostics, such as genomic testing and biomarker analysis, is significantly contributing to the market's expansion.

Europe Gynecological Cancers Market Insight

The Europe gynecological cancers market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing cancer awareness and well-established screening programs. The rise in aging population, coupled with improved access to healthcare services, is fostering the demand for effective cancer treatments. European patients are also benefiting from advancements in oncology therapies and government-supported healthcare systems. The region is experiencing steady growth across hospitals and specialty clinics, with increasing adoption of innovative treatment options and personalized medicine approaches.

U.K. Gynecological Cancers Market Insight

The U.K. gynecological cancers market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising incidence of gynecological cancers and strong public health initiatives. In addition, increasing participation in cervical cancer screening programs and HPV vaccination campaigns are encouraging early diagnosis and prevention. The country’s advanced healthcare system, along with ongoing research in oncology, is expected to continue to stimulate market growth.

Germany Gynecological Cancers Market Insight

The Germany gynecological cancers market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of cancer prevention and the demand for advanced therapeutic solutions. Germany’s well-developed healthcare infrastructure, combined with its focus on innovation and clinical research, promotes the adoption of targeted therapies and immunotherapies. The integration of modern diagnostic technologies is also becoming increasingly prevalent, with a strong preference for high-quality, effective treatment solutions aligning with patient expectations.

Asia-Pacific Gynecological Cancers Market Insight

The Asia-Pacific gynecological cancers market is poised to grow at the fastest CAGR of around 12% during the forecast period of 2026 to 2033, driven by increasing population, rising cancer incidence, and improving healthcare infrastructure in countries such as China, Japan, and India. The region's growing focus on early diagnosis and treatment, supported by government initiatives and healthcare investments, is driving market growth. Furthermore, as APAC strengthens its pharmaceutical manufacturing capabilities, the accessibility and affordability of cancer treatments are expanding to a wider patient population.

Japan Gynecological Cancers Market Insight

The Japan gynecological cancers market is gaining momentum due to the country’s advanced healthcare system, aging population, and increasing focus on early cancer detection. The Japanese market places significant emphasis on precision medicine, and the adoption of targeted therapies is driven by continuous innovation in oncology research. The integration of advanced diagnostic technologies, such as molecular testing, is fueling growth. Moreover, Japan's aging demographic is likely to spur demand for effective and long-term cancer management solutions in both hospital and specialty care settings.

India Gynecological Cancers Market Insight

The India gynecological cancers market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large population base, rising cancer burden, and improving access to healthcare services. India stands as one of the fastest-growing markets for oncology treatments, with increasing awareness regarding early screening and diagnosis. The push towards strengthening healthcare infrastructure, along with the availability of cost-effective treatment options and expanding pharmaceutical sector, are key factors propelling the market in India.

Gynecological Cancers Market Share

The Gynecological Cancers industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- Pfizer Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Gilead Sciences, Inc. (U.S.)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- AstraZeneca PLC (U.K.)

- GSK plc (U.K.)

- Sanofi (France)

- Bayer AG (Germany)

- Boehringer Ingelheim International GmbH (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Eisai Co., Ltd. (Japan)

- Astellas Pharma Inc. (Japan)

- Daiichi Sankyo Company, Limited (Japan)

What are the Recent Developments in Global Gynecological Cancers Market?

- In May 2025, the U.S. Food and Drug Administration approved the combination therapy avutometinib and defactinib (Avmapki Fakzynja) for KRAS-mutated recurrent low-grade serous ovarian cancer, marking the first-ever FDA-approved treatment specifically for this rare cancer type and significantly advancing targeted therapy options in gynecologic oncology

- In May 2025, the U.S. FDA approved the Teal Wand, the first at-home vaginal self-collection device for cervical cancer screening, enabling more accessible and convenient early detection and potentially increasing screening participation rates among women

- In June 2024, the U.S. Food and Drug Administration approved pembrolizumab (Keytruda) in combination with chemotherapy for patients with primary advanced or recurrent endometrial carcinoma, enhancing treatment outcomes and expanding the role of immunotherapy in gynecological cancers

- In April 2024, the U.S. FDA granted full approval to tisotumab vedotin (Tivdak) for recurrent or metastatic cervical cancer, demonstrating a significant reduction in the risk of death compared to chemotherapy in late-stage clinical trials

- In March 2024, the U.S. FDA granted full approval to mirvetuximab soravtansine (Elahere) for FRα-positive platinum-resistant ovarian cancer, based on clinical trials showing improved survival and fewer side effects compared to standard chemotherapy

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.