Global Gynecological Devices Market

Market Size in USD Billion

USD

18.89 Billion

USD

33.43 Billion

2025

2033

USD

18.89 Billion

USD

33.43 Billion

2025

2033

| 2026 - 2033 | |

| USD 18.89 Billion | |

| USD 33.43 Billion | |

| % | |

|

Gynecological Devices Market Overview

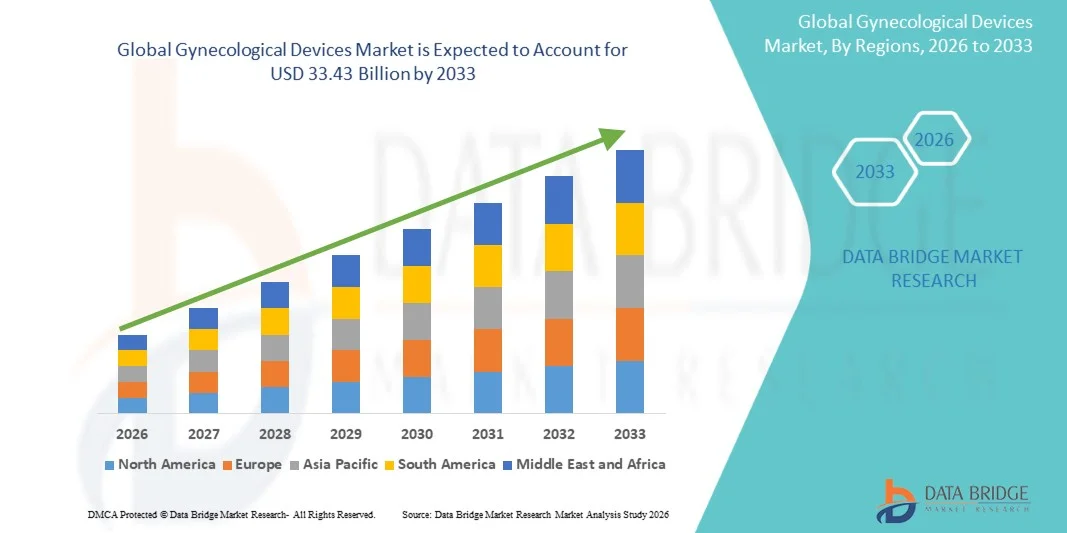

The Gynecological Devices Market was valued at USD 18.89 billion in 2025 and is projected to reach USD 33.43 billion by 2033, growing at a CAGR of 7.40% from 2026 to 2033. The market is experiencing steady growth driven by increasing prevalence of gynecological disorders, rising awareness of women’s health, and continuous advancements in minimally invasive surgical and diagnostic technologies.

The growing burden of conditions such as uterine fibroids, endometriosis, cervical cancer, and ovarian disorders, along with expanding demand for early diagnosis and effective treatment options, is significantly boosting the adoption of gynecological devices. Additionally, increasing emphasis on preventive healthcare, rising healthcare expenditure, and improving access to gynecological care in emerging economies are further supporting market expansion.

Key Market Trends & Insights

- North America dominated the Gynecological Devices Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong presence of leading medical device companies.

- The Gynecological Endoscopy Devices segment led the market with a 35.48% share in 2025, driven by increasing adoption of minimally invasive surgical procedures such as hysteroscopy and laparoscopy across hospitals and specialty clinics.

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033 at a CAGR of 7.6%, fueled by improving women’s healthcare access, rising awareness of reproductive health, and increasing healthcare investments in countries such as India and China.

- Diagnostic Imaging Systems are the fastest-growing product type, projected to register a CAGR of 7.6%, reflecting the surge in demand for early and accurate detection of gynecological diseases such as cervical cancer and uterine abnormalities.

- The Uterine Fibroids segment dominated the application category with a 32.14% revenue share in 2025, led by the high global prevalence of fibroids among women of reproductive age.

- Hospitals accounted for 66.35% of the market, preferred by the high patient inflow, availability of advanced surgical infrastructure, and presence of skilled gynecological specialists.

- The Cervical Cancer segment is the fastest-growing application category, with a CAGR of 7.8%, driven by the expanding global screening programs and rising emphasis on early detection.

Market Size & Forecast

- Global Market Value (2025): USD 18.89 Billion

- Expected Market Value (2033): USD 33.43 Billion

- Forecast CAGR (2026–2033): 7.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Gynecological Devices Market Segmentation

|

Attributes |

Gynecological Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Hologic, Inc. (U.S.) · Medtronic (Ireland) · CooperSurgical, Inc. (U.S.) · Olympus Corporation (Japan) · Karl Storz SE & Co. KG (Germany) · Richard Wolf GmbH (Germany) · Stryker (U.S.) · Boston Scientific Corporation (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · BD (U.S.) · Cook (U.S.) · Intuitive Surgical, Inc. (U.S.) · GE HealthCare (U.S.) · Siemens Healthineers AG (Germany) · FUJIFILM Holdings Corporation (Japan) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Smith & Nephew (U.K.) · Teleflex Incorporated (U.S.) · B. Braun SE (Germany) · Zimmer Biomet (U.S.) |

|

Market Opportunities |

· Rapid expansion of minimally invasive gynecological procedures · Increasing adoption of AI-enabled diagnostic imaging and digital colposcopy systems · Growing penetration of outpatient and ambulatory gynecology care models |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Gynecological Devices Market Trends

Trend: Growth in Minimally Invasive Gynecological Procedures

Gynecological care is increasingly shifting toward minimally invasive surgical techniques such as laparoscopy, hysteroscopy, and endometrial ablation, driven by reduced patient recovery time, lower complication risks, and improved clinical outcomes. The adoption of advanced visualization systems, energy-based surgical devices, and robotic-assisted platforms is enhancing procedural precision and expanding outpatient treatment capabilities. Hospitals and specialty clinics are increasingly integrating these technologies into standard gynecological care pathways, while digital imaging and AI-assisted tools are improving diagnostic accuracy and workflow efficiency. For instance, rising use of advanced hysteroscopic systems in fibroid and polyp removal procedures demonstrates this shift toward less invasive treatment approaches.

Gynecological Devices Market Dynamics

Key Market Driver: Rising Prevalence of Gynecological Disorders and Screening Demand

The increasing global burden of gynecological conditions such as cervical cancer, uterine fibroids, endometriosis, and ovarian disorders is significantly driving demand for diagnostic and surgical gynecological devices. Expanding awareness of women’s health, along with government-led cervical cancer screening programs and preventive healthcare initiatives, is boosting early diagnosis rates. Healthcare providers are increasingly adopting advanced imaging, colposcopy, and biopsy devices to improve detection accuracy and treatment outcomes. For instance, growing adoption of HPV screening programs combined with colposcopy-based diagnostics highlights the rising emphasis on early intervention and disease management.

Key Restraint/Challenge: High Cost of Advanced Gynecological Surgical Systems

A major restraint in the gynecological devices market is the high cost associated with advanced surgical systems, including robotic-assisted platforms, high-end imaging devices, and minimally invasive surgical instruments. These technologies require significant capital investment, along with ongoing maintenance, training, and consumable costs, which can limit adoption in low- and middle-income healthcare settings. Smaller hospitals and clinics often rely on conventional surgical tools due to budget constraints and limited reimbursement support. For instance, limited deployment of robotic gynecological surgery systems in resource-constrained public hospitals reflects the affordability challenges restricting broader market penetration.

Key Market Opportunity: Expansion of AI-Enabled Diagnostics and Outpatient Gynecology Care

The integration of artificial intelligence and digital imaging technologies into gynecological diagnostics presents a significant market opportunity by enabling earlier, faster, and more accurate detection of conditions such as cervical cancer, fibroids, and endometriosis. At the same time, the shift toward outpatient and ambulatory surgical center-based care is creating strong demand for portable, single-use, and cost-efficient gynecological devices that reduce hospital burden and improve patient accessibility. Device manufacturers are increasingly focusing on smart colposcopy systems, AI-assisted ultrasound platforms, and minimally invasive disposable instruments to address evolving clinical needs. For instance, the rising deployment of AI-based cervical screening tools in community health programs highlights the growing role of digital transformation in expanding access to women’s healthcare.

Gynecological Devices Market Scope

The gynecological devices market is segmented on the basis of product type, application, and end user.

- By Product Type

On the basis of product type, the Gynecological Devices Market is segmented into gynecological endoscopy devices, endometrial ablation devices, fluid management systems, female sterilization and contraceptive devices, hand instruments, diagnostic imaging systems, and software. The Gynecological Endoscopy Devices segment dominated the market with a 35.48% share in 2025, owing to increasing adoption of minimally invasive surgical procedures such as hysteroscopy and laparoscopy across hospitals and specialty clinics. These devices provide high precision visualization, reduced surgical trauma, and faster patient recovery, making them the preferred choice for treating fibroids, endometriosis, and ovarian disorders. Continuous technological advancements in imaging resolution and instrument miniaturization are further strengthening adoption. Rising demand for outpatient gynecological surgeries is also contributing to market expansion. Increasing integration with digital imaging and AI-assisted surgical guidance is enhancing procedural accuracy. Strong preference for minimally invasive techniques continues to reinforce this segment’s dominance.

The Diagnostic Imaging Systems segment is projected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising demand for early and accurate detection of gynecological diseases such as cervical cancer and uterine abnormalities. Advanced ultrasound systems, colposcopes, and AI-enabled imaging platforms are improving diagnostic precision and reducing false detection rates. Growing awareness of preventive healthcare and government-led screening programs is significantly boosting adoption. Expanding access to women’s healthcare services in emerging economies is further supporting growth. Integration of AI and digital pathology tools is enhancing workflow efficiency in diagnostic centers. Increasing shift toward non-invasive diagnostic techniques is also accelerating demand for imaging-based solutions.

- By Application

On the basis of application, the market is segmented into uterine fibroids, ovarian disorders, cervical cancer, endometriosis, fertility & pregnancy care, and contraception. The Uterine Fibroids segment dominated the market with a 32.14% share in 2025, driven by the high global prevalence of fibroids among women of reproductive age. Increasing use of minimally invasive surgical devices and ablation technologies is significantly improving treatment outcomes. Rising hospitalization rates and surgical interventions for fibroid management are further supporting segment growth. Advancements in hysteroscopic and laparoscopic procedures are enabling effective and less invasive treatment options. Growing awareness and early diagnosis are also contributing to higher treatment adoption. Strong clinical focus on fertility preservation is reinforcing demand for advanced treatment devices.

The Cervical Cancer segment is expected to witness the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by expanding global screening programs and rising emphasis on early detection. Increasing adoption of HPV testing, colposcopy, and biopsy devices is improving diagnostic accuracy and early intervention rates. Government initiatives promoting cervical cancer awareness and vaccination programs are further accelerating demand. Technological advancements in diagnostic imaging and AI-assisted screening tools are enhancing detection efficiency. Growing healthcare investments in developing regions are improving access to diagnostic infrastructure. Rising mortality reduction targets are also pushing adoption of advanced screening solutions.

- By End User

On the basis of end user, the market is segmented into hospitals, diagnostic centers, and others. The Hospitals segment dominated the market with a 66.35% share in 2025, due to high patient inflow, availability of advanced surgical infrastructure, and presence of skilled gynecological specialists. Hospitals remain the primary centers for complex gynecological surgeries and diagnostic procedures. Increasing adoption of minimally invasive surgical systems is further strengthening hospital-based utilization. Availability of integrated diagnostic and treatment facilities enhances procedural efficiency. Strong reimbursement frameworks in developed regions are also supporting hospital dominance. Continuous investments in upgrading gynecology departments are reinforcing their leadership position.

The Diagnostic Centers segment is projected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by rising demand for early disease detection and preventive screening services. Increasing use of advanced imaging systems and AI-enabled diagnostic tools is improving accuracy and turnaround time. Growing preference for outpatient diagnostic services is reducing dependency on hospital-based care. Expanding healthcare infrastructure in emerging economies is further supporting segment growth. Rising awareness of women’s health screening programs is boosting patient participation. Cost-effective and accessible diagnostic services are making this segment increasingly attractive.

Gynecological Devices Market Regional Analysis

North America dominated the Gynecological Devices Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive procedures, and strong presence of leading medical device companies. The region also benefits from well-established screening programs, favorable reimbursement policies, and strong awareness of women’s health and preventive care. Increasing utilization of robotic-assisted surgery, advanced imaging systems, and AI-enabled diagnostic tools continues to strengthen clinical outcomes across hospitals and specialty clinics. Rising incidence of gynecological disorders and continuous technological innovation further reinforce North America’s leadership position in the global market.

U.S. Gynecological Devices Market Insight

The U.S. gynecological devices market is witnessing strong growth due to advanced hospital infrastructure, high adoption of robotic-assisted and minimally invasive gynecological procedures, and strong presence of leading global medical device manufacturers. The country benefits from well-established cervical cancer screening programs, favorable reimbursement policies, and high awareness of preventive women’s healthcare. Increasing integration of AI-enabled diagnostic imaging, hysteroscopy systems, and laparoscopic technologies is improving clinical accuracy and treatment outcomes. Rising prevalence of uterine fibroids, endometriosis, and other gynecological disorders is further driving demand. Continuous innovation and strong R&D investments continue to position the U.S. as the most influential market in the region.

Europe Gynecological Devices Market Insight

The Europe gynecological devices market remains a major contributor to global revenue, driven by strong healthcare systems, supportive government initiatives for women’s health, and high adoption of minimally invasive surgical technologies. The widespread use of advanced diagnostic imaging systems, colposcopy devices, and endoscopic surgical tools is supporting market expansion across hospitals and specialty clinics. Increasing investments in digital health infrastructure and AI-assisted diagnostics are enhancing early disease detection and treatment outcomes. Strict regulatory standards and a strong focus on patient safety further drive technology adoption. Continuous innovation in surgical techniques and rising demand for outpatient procedures continue to strengthen Europe’s position in the market.

U.K. Gynecological Devices Market Insight

The U.K. gynecological devices market is experiencing steady growth, supported by rising adoption of advanced diagnostic and surgical technologies in public and private healthcare systems. Increasing investments in women’s health programs and early cancer screening initiatives are driving demand for colposcopy, ultrasound, and hysteroscopy devices. The integration of AI and digital imaging in diagnostic workflows is improving accuracy and efficiency in clinical decision-making. Growing preference for minimally invasive procedures and outpatient care is further supporting market expansion. Strong presence of skilled healthcare professionals and continuous NHS-driven modernization efforts are enhancing overall market growth.

Germany Gynecological Devices Market Insight

The Germany gynecological devices market is expanding steadily due to its strong medical device manufacturing base, advanced hospital infrastructure, and high focus on clinical innovation. Hospitals and specialty clinics are increasingly adopting robotic-assisted surgery systems, endoscopic devices, and advanced imaging technologies for gynecological treatments. Growing emphasis on precision medicine and minimally invasive procedures is further accelerating device adoption. Strong research and development activities in medical technology and favorable healthcare reimbursement policies are supporting market growth. Continuous innovation in surgical and diagnostic systems continues to position Germany as a key European market.

Asia-Pacific Gynecological Devices Market Insight

The Asia-Pacific gynecological devices market is expected to witness rapid growth, driven by improving healthcare infrastructure, rising awareness of women’s health, and increasing access to diagnostic and surgical care in countries such as China, India, and Japan. Expanding government initiatives for cervical cancer screening and maternal healthcare are significantly boosting device adoption. Growing penetration of minimally invasive surgical technologies and increasing investments in hospital modernization are supporting regional expansion. Rising medical tourism and expanding private healthcare facilities are further accelerating demand. Additionally, increasing burden of gynecological disorders is driving strong market growth across emerging economies.

Japan Gynecological Devices Market Insight

The Japan gynecological devices market is witnessing consistent growth due to advanced healthcare systems, strong focus on early disease detection, and high adoption of innovative medical technologies. Hospitals and clinics are increasingly utilizing advanced imaging systems, hysteroscopic devices, and robotic-assisted surgical platforms for gynecological treatments. Integration of AI-enabled diagnostics and precision medicine approaches is improving clinical outcomes. The country’s aging female population is also contributing to higher demand for gynecological care. Continuous technological innovation and strong regulatory standards are further supporting market development.

China Gynecological Devices Market Insight

The China gynecological devices market is growing rapidly, driven by expanding healthcare infrastructure, rising awareness of women’s reproductive health, and increasing government focus on early disease screening programs. Growing adoption of advanced diagnostic imaging systems, minimally invasive surgical devices, and AI-powered healthcare solutions is significantly boosting market demand. Rapid urbanization and increasing access to specialized gynecological care are further supporting growth. Strong investments in hospital modernization and domestic medical device manufacturing are enhancing market availability. Rising prevalence of gynecological disorders continues to position China as one of the fastest-growing markets globally.

Gynecological Devices Market Share

The gynecological devices industry is primarily led by well-established companies, including:

- Hologic, Inc. (U.S.)

- Medtronic (Ireland)

- CooperSurgical, Inc. (U.S.)

- Olympus Corporation (Japan)

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Stryker (U.S.)

- Boston Scientific Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- BD (U.S.)

- Cook (U.S.)

- Intuitive Surgical, Inc. (U.S.)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- FUJIFILM Holdings Corporation (Japan)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Smith & Nephew (U.K.)

- Teleflex Incorporated (U.S.)

- Braun SE (Germany)

- Zimmer Biomet (U.S.)

Latest Developments in Gynecological Devices Market

- In June 2023, DYSIS Medical received expanded regulatory recognition for its DYSIS Colposcopy System, an advanced digital colposcopy platform used in cervical cancer screening and detection of precancerous lesions. The system combines digital imaging with automated analysis to improve accuracy and standardization in cervical examinations. This advancement supports early detection programs and strengthens global cervical cancer screening initiatives. It also highlights growing adoption of AI-assisted diagnostic tools in women’s health

- In March 2022, Olympus Corporation continued the global expansion of its advanced endoscopy and imaging platforms used in gynecological procedures such as hysteroscopy and laparoscopy. These systems feature high-definition visualization and improved ergonomics designed to enhance diagnostic accuracy and surgical precision. The advancements support minimally invasive interventions and improve workflow efficiency in hospitals and specialty clinics. This development reflects increasing innovation in imaging technologies for women’s healthcare

- In December 2021, Hologic, a global leader in women’s health diagnostics and medical imaging, announced the completion of its acquisition of Gynesonics, the developer of the Sonata® System for transcervical fibroid ablation. The Sonata system enables incision-free treatment of uterine fibroids using intrauterine ultrasound guidance and radiofrequency energy. This acquisition expanded Hologic’s minimally invasive gynecological treatment portfolio and strengthened its position in uterine fibroid management technologies. It also reinforced the shift toward outpatient gynecological procedures

- In November 2021, CooperSurgical, a subsidiary of CooperCompanies, announced the acquisition of AEGEA Medical, the developer of the Mara™ water vapor ablation system used for treating heavy menstrual bleeding caused by uterine fibroids. The system offers a minimally invasive, in-office treatment option for women’s health care. This acquisition strengthened CooperSurgical’s portfolio in minimally invasive gynecological treatment solutions and expanded its presence in the uterine care segment. The deal highlighted growing consolidation in women’s health technologies

- In October 2021, Medtronic, a leading medical technology company, announced that its Hugo™ Robotic-Assisted Surgery (RAS) system received CE Mark approval in Europe for use in gynecological and other minimally invasive surgical procedures. The system is designed to support complex laparoscopic surgeries with enhanced precision, 3D visualization, and modular architecture, enabling broader adoption of robotic surgery across hospitals and surgical centers. This milestone marked Medtronic’s entry into the soft-tissue robotic surgery market, including gynecological applications such as hysterectomy and endometriosis treatment. It also strengthened competition in the global surgical robotics space

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.