Global Gynecological Examination Chairs Market

Market Size in USD Billion

USD

242.32 Billion

USD

746.43 Billion

2024

2032

USD

242.32 Billion

USD

746.43 Billion

2024

2032

| 2025 - 2032 | |

| USD 242.32 Billion | |

| USD 746.43 Billion | |

| % | |

|

Gynecological Examination Chairs Market Size

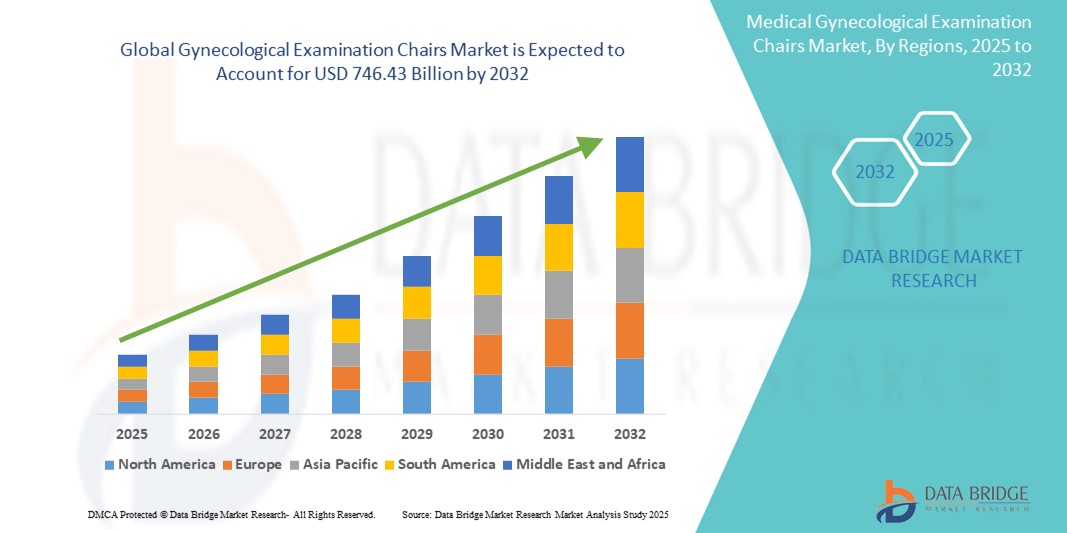

- The global gynecological examination chairs market size was valued at USD 242.32 billion in 2024 and is expected to reach USD 746.43 billion by 2032, at a CAGR of 15.10% during the forecast period

- The market growth is largely driven by the increasing global focus on women’s health, rising awareness of early diagnosis and screening, and expansion of gynecological services in both public and private healthcare sectors

- Furthermore, advancements in medical furniture design, ergonomic innovations, and the demand for enhanced patient comfort and clinician efficiency are establishing modern gynecological chairs as essential clinical tools. These aligned drivers are accelerating adoption across hospitals and specialty clinics, thereby significantly contributing to the market’s expansion

Gynecological Examination Chairs Market Analysis

- Gynecological examination chairs, designed to provide ergonomic positioning and enhanced comfort during pelvic exams and procedures, are increasingly integral to modern gynecological practice in hospitals, clinics, and specialty centers due to their role in improving diagnostic efficiency and patient experience

- The growing demand for gynecological chairs is primarily fueled by rising awareness of women's health, an increasing number of routine screenings, and expanding investments in healthcare infrastructure, especially in emerging economies

- Europe dominated the gynecological examination chairs market with the largest revenue share of 38.1% in 2024, supported by a well-established healthcare system, a growing elderly female population, and favorable government initiatives aimed at preventive women’s healthcare, with countries such as Germany and France witnessing high adoption in both public and private health facilities

- Asia-Pacific is expected to be the fastest growing region in the gynecological chairs market during the forecast period due to increasing healthcare spending, improving hospital infrastructure, and a growing emphasis on maternal and reproductive health

- Electric gynecological chairs segment dominated the market with a market share of 47.3% in 2024, driven by their superior functionality, ease of adjustment, and enhanced patient and clinician comfort during examinations and procedures

Report Scope and Gynecological Examination Chairs Market Segmentation

|

Attributes |

Gynecological Examination Chairs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Gynecological Examination Chairs Market Trends

“Technological Advancements and Enhanced Patient-Centric Design”

- A significant and accelerating trend in the global gynecological examination chairs market is the shift toward technologically advanced and ergonomically designed chairs that enhance both patient comfort and clinical efficiency. Manufacturers are focusing on integrating features such as motorized height adjustment, programmable positioning, and improved cushioning to support longer procedures and minimize patient discomfort

- For instance, companies such as Oakworks Medical and Promotal have introduced electric chairs with remote-controlled multi-positioning capabilities, antimicrobial upholstery, and easy-clean surfaces, facilitating better hygiene and workflow in clinical environments

- The integration of foot-controlled mechanisms and touchless operation has gained traction, especially in the post-COVID-19 context, where minimizing contact and improving sanitization are paramount. In addition, the growing use of portable and modular chairs supports improved space utilization and adaptability in smaller clinics and outpatient centers

- These evolving design trends are helping healthcare providers deliver more personalized care, improve procedural accuracy, and reduce the physical strain on practitioners during examinations

- This trend toward patient-focused, technologically advanced gynecological chairs is significantly elevating expectations in the women’s health diagnostic equipment sector. Consequently, leading players are investing in R&D to enhance comfort, safety, and functionality, aligning with the global emphasis on improving women's healthcare infrastructure and experiences

- The demand for ergonomically advanced and multi-functional gynecological chairs is increasing across hospitals, specialty gynecology centers, and ambulatory clinics, particularly in regions where women’s health initiatives and healthcare modernization efforts are expanding

Gynecological Examination Chairs Market Dynamics

Driver

“Rising Focus on Women’s Health and Expansion of Diagnostic Infrastructure”

- The growing global emphasis on women's health, coupled with increasing awareness around preventive screenings and early diagnosis of gynecological disorders, is a major driver fueling demand for gynecological examination chairs

- For instance, governments and NGOs in both developed and emerging economies are launching cervical cancer screening programs, leading to higher demand for well-equipped gynecology units with advanced diagnostic furniture

- As the volume of gynecological examinations continues to rise, healthcare providers are prioritizing investment in comfortable, reliable, and durable examination chairs to enhance patient care and streamline procedures

- Furthermore, the expansion of outpatient clinics and ambulatory surgical centers (ASCs), particularly in urban areas, is contributing to higher chair demand due to increased footfall and need for efficient patient throughput

- The trend toward modernization of healthcare infrastructure, particularly in Asia-Pacific and Latin America, is creating strong opportunities for gynecological chair manufacturers to offer customized, compact, and technologically integrated products tailored to regional needs.

Restraint/Challenge

“High Cost of Advanced Chairs and Limited Access in Resource-Constrained Regions”

- Despite the clear benefits of modern gynecological chairs, the relatively high cost of advanced electric or motorized models presents a barrier to adoption, particularly in developing countries or underfunded public healthcare systems

- In regions with limited healthcare budgets, providers often rely on outdated or basic equipment, which can limit diagnostic accuracy and patient comfort. This gap is especially significant in rural areas and low-income countries where gynecology units are under-resourced

- Moreover, space constraints in small clinics or older healthcare facilities can make it difficult to accommodate larger, multi-functional examination chairs, leading to hesitance in adopting newer models

- Regulatory approvals and compliance requirements for medical furniture also vary across countries, sometimes slowing down product launch timelines and creating entry barriers for international manufacturers

- Addressing these challenges requires manufacturers to focus on cost-effective product innovation, scalable designs, and targeted distribution strategies that enable broader access and affordability, especially in high-need regions

Gynecological Examination Chairs Market Scope

The market is segmented on the basis of product type, application, end-users, and distribution channel.

- By Product Type

On the basis of product type, the gynecological examination chairs market is segmented into electric gynecological chairs, non-electric gynecological chairs, hydraulic gynecological chairs, manual gynecological chairs, and others. The electric gynecological chairs segment dominated the market with the largest market revenue share of 47.3% in 2024, attributed to their advanced functionality, improved ergonomics, and the ability to offer multiple positioning options. These chairs enhance clinician efficiency and patient comfort, making them highly preferred in hospitals and specialty clinics.

The hydraulic gynecological chairs segment is expected to witness the fastest growth rate from 2025 to 2032, driven by their balance of affordability and functionality. These chairs offer smooth operation, do not require external power sources, and are ideal for mid-sized clinics and healthcare facilities with moderate patient volumes. The rising demand for reliable, durable, and low-maintenance solutions in developing regions is also contributing to the segment’s growth.

- By Application

On the basis of application, the market is segmented into gynecological examinations, diagnostic procedures, minor surgical procedures, and routine check-ups. The gynecological examinations segment accounted for the largest share in 2024, driven by the high frequency of routine pelvic and reproductive health evaluations across a broad patient population. Increased awareness of women’s health, government-led screening programs, and regular check-ups for conditions such as cervical and ovarian cancer are propelling this segment.

The diagnostic procedures segment is anticipated to grow significantly during the forecast period due to the rising demand for early detection and precision diagnostics. The integration of imaging support and patient-positioning aids in examination chairs enhances the effectiveness of procedures such as colposcopy and ultrasound.

- By End User

On the basis of end-users, the market is segmented into hospitals, gynecology clinics, ambulatory surgical centers, and diagnostic centers. The hospitals segment dominated the market in 2024 due to the large patient volumes, presence of specialized gynecological departments, and higher budgets to invest in advanced and multi-functional examination chairs. Public and private hospitals increasingly emphasize modernizing gynecology units to improve patient care and operational efficiency.

The gynecology clinics segment is projected to witness the fastest CAGR through 2032 as standalone women’s health centers continue to expand, particularly in urban areas. Clinics are investing in specialized, compact, and customizable equipment to offer outpatient diagnostics and treatment with greater comfort and personalization.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender, retail sales, and online sales. The direct tender segment held the largest market share in 2024, mainly due to high-volume procurement by hospitals and public healthcare institutions. These entities prefer direct negotiations with manufacturers to acquire bulk, cost-effective, and regulatory-compliant equipment.

The online sales segment is anticipated to grow at the fastest pace during the forecast period, driven by the digitalization of medical procurement and the increasing availability of examination chairs on e-commerce platforms. Small clinics and private practitioners, in particular, are leveraging online channels for cost comparison, convenience, and access to a wider range of models.

Gynecological Examination Chairs Market Regional Analysis

- Europe dominated the gynecological examination chairs market with the largest revenue share of 38.1% in 2024, supported by a well-established healthcare system, a growing elderly female population, and favorable government initiatives aimed at preventive women’s healthcare

- Healthcare providers in the region prioritize advanced, ergonomic medical furniture to enhance patient comfort and improve procedural efficiency, particularly in hospitals and specialty gynecology clinics

- This widespread adoption is further supported by favorable government healthcare policies, increasing healthcare expenditure, and a growing aging female population, establishing gynecological examination chairs as essential equipment across both public and private medical facilities

France Gynecological Examination Chairs Market Insight

The France gynecological examination chairs market is expected to grow steadily during the forecast period, driven by the country’s strong public healthcare system and proactive women’s health initiatives. France has one of the highest rates of gynecological screening in Europe, supported by national cervical and breast cancer programs, which fuels consistent demand for high-quality examination equipment. French hospitals and maternity clinics are increasingly investing in electric and ergonomic chairs that offer improved comfort, hygienic surfaces, and multi-positioning features to enhance both patient experience and clinical workflow.

U.K. Gynecological Examination Chairs Market Insight

The U.K. gynecological examination chairs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by government-backed women’s health initiatives and regular preventive care guidelines. Hospitals and NHS trusts are increasingly modernizing their examination units with electric and hydraulic chairs that meet ergonomic and infection control standards. In addition, the growing prevalence of gynecological disorders and emphasis on outpatient care are encouraging healthcare providers to invest in compact, multi-functional examination furniture.

Germany Gynecological Examination Chairs Market Insight

The Germany gynecological examination chairs market is expected to expand at a considerable CAGR during the forecast period, fueled by its advanced healthcare infrastructure and the presence of leading medical furniture manufacturers. German clinics and hospitals emphasize efficient diagnostics and patient comfort, driving adoption of electric and programmable chairs. In addition, the country’s commitment to hygiene standards and medical innovation supports strong demand for antimicrobial, easy-to-clean chair designs that improve workflow and clinical outcomes.

Asia-Pacific Gynecological Examination Chairs Market Insight

The Asia-Pacific gynecological examination chairs market is poised to grow at the fastest CAGR of 23.4% during the forecast period of 2025 to 2032, due to rising healthcare expenditures, growing maternal health awareness, and rapid hospital expansion in countries such as India, China, and Japan. Government initiatives promoting women’s health and the development of modern outpatient care centers are further accelerating market adoption. The availability of affordable, locally manufactured gynecological chairs tailored to the region’s clinical needs is also expanding access in both urban and semi-urban areas

Japan Gynecological Examination Chairs Market Insight

The Japan gynecological examination chairs market is gaining momentum due to the nation’s focus on preventive healthcare, aging population, and demand for advanced clinical infrastructure. Japanese healthcare facilities prioritize patient-centric technologies, and the integration of electric, space-saving, and multi-functional chairs is increasing, particularly in women’s hospitals and specialty clinics. In addition, the push for digital transformation in healthcare is supporting the adoption of high-tech examination equipment designed for comfort, efficiency, and minimal physical strain on clinicians.

India Gynecological Examination Chairs Market Insight

The India gynecological examination chairs market accounted for the largest market revenue share in Asia Pacific in 2024, attributed to rapid urbanization, expanding hospital networks, and increasing emphasis on maternal and reproductive health. With a growing number of women’s health clinics and diagnostic centers, demand for cost-effective, durable, and adjustable examination chairs is rising. Government programs promoting rural health infrastructure and cervical cancer screening are also boosting adoption across tier 2 and tier 3 cities, supported by domestic manufacturing of affordable gynecology chairs.

Gynecological Examination Chairs Market Share

The gynecological examination chairs industry is primarily led by well-established companies, including:

- SCHMITZ medical GmbH (Germany)

- Promotal SAS (France)

- Oakworks, Inc. (U.S.)

- medifa (Germany)

- Arden Medikal San. Tic. Ltd. Şti. (Turkey)

- Hill-Rom Holdings, Inc. (U.S.)

- Howell Medical (China)

- Malvestio Spa (Italy)

- INMOCLINC S.L.U. (Spain)

- Favero Health Projects Spa (Italy)

- AGA Sanitätsartikel GmbH (Germany)

- BRUMABA (Germany)

- Technomed (India) Private Limited (India)

- Novak M (Slovenia)

- Hidemar S.A. (Spain)

- Taicang Kanghui Technology Development Co., Ltd. (China)

- JMS Co., Ltd. (Japan)

- Ergos (Greece)

- Takara Belmont Corporation (Japan)

- Desco Medical India (India)

What are the Recent Developments in Global Gynecological Examination Chairs Market?

- In April 2024, SCHMITZ u. Söhne GmbH & Co. KG, a leading German manufacturer of medical furniture, launched its latest DIAMOND series of electric gynecological chairs featuring enhanced patient ergonomics, antimicrobial upholstery, and fully automated positioning capabilities. The product aims to support clinicians in improving procedural efficiency and patient comfort, particularly in high-volume hospital environments. This innovation highlights SCHMITZ’s focus on delivering premium, technology-integrated solutions tailored to evolving gynecological care standards

- In March 2024, Promotal, a France-based medical equipment company, introduced a compact, foldable gynecological chair designed specifically for small clinics and mobile healthcare units. This chair addresses space and mobility constraints while maintaining essential features such as adjustable backrests and leg supports. The development reflects the company's commitment to increasing accessibility to quality women’s healthcare, especially in underserved or rural regions

- In March 2024, Oakworks Medical (U.S.) unveiled its new EcoSmart Gynecology Chair, integrating sustainable materials and energy-efficient power systems. With increasing emphasis on environmental responsibility in healthcare, this innovation appeals to institutions prioritizing eco-friendly procurement. The product underscores the growing intersection of green technology and patient-centric medical design in the gynecological equipment segment

- In February 2024, Medifa GmbH & Co. KG, a German medical furniture manufacturer, expanded its distribution agreement with healthcare providers in the Middle East and Southeast Asia, aiming to deliver fully motorized gynecological chairs to regions undergoing rapid healthcare infrastructure development. This strategic expansion is intended to meet the rising demand for advanced examination equipment in international markets with increasing gynecological service needs

- In January 2024, Arden Medikal (Turkey) announced the release of a budget-friendly line of manual and hydraulic gynecological chairs targeted at public hospitals and rural health centers across Eastern Europe and Central Asia. With simplified controls, durable construction, and customizable configurations, the new product line is positioned to address affordability barriers while supporting basic reproductive healthcare needs, demonstrating Arden’s focus on accessible innovation

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.