Global Haematology Market

Market Size in USD Billion

USD

2.51 Billion

USD

3.48 Billion

2025

2033

USD

2.51 Billion

USD

3.48 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.51 Billion | |

| USD 3.48 Billion | |

| % | |

|

Haematology Market Overview

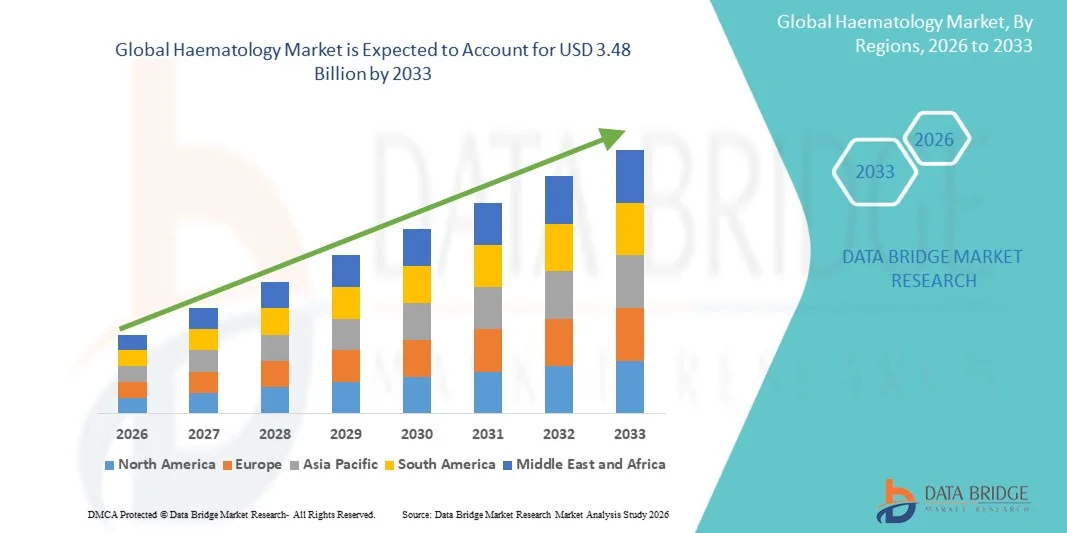

The Haematology Market was valued at USD 2.51 billion in 2025 and is projected to reach USD 3.48 billion by 2033, growing at a CAGR of 4.20% from 2026 to 2033. The market is witnessing steady expansion driven by the rising global burden of blood disorders such as anemia, leukemia, hemophilia, and other hematological malignancies, along with increasing demand for advanced diagnostic testing and targeted therapies. Growth in routine blood screening and the adoption of automated hematology analyzers across clinical laboratories is further supporting market development.

The increasing prevalence of chronic diseases, aging population, and growing awareness regarding early disease detection are accelerating the adoption of hematology diagnostics and treatment solutions worldwide. In addition, advancements in flow cytometry, molecular hematology, and next-generation sequencing are improving diagnostic accuracy and enabling personalized treatment approaches. Expanding healthcare infrastructure, coupled with rising investments in laboratory automation and precision medicine, is expected to further drive the adoption of advanced hematology technologies across hospitals, diagnostic centers, and research institutions.

Key Market Trends & Insights

- North America dominated the Haematology Market with the largest revenue share of 38.92% in 2025, supported by advanced diagnostic infrastructure, high prevalence of blood disorders, and strong adoption of automated hematology analyzers and molecular testing platforms.

- The Haematology Analyzers segment led the market with a 44.15% share in 2025, driven by their widespread use in routine complete blood count testing and high-throughput diagnostic workflows across hospitals and clinical laboratories

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising healthcare expenditure, expanding diagnostic laboratory networks, and increasing awareness of early disease detection in countries such as China, India, and Japan.

- Flow Cytometers are the fastest-growing product type, projected to register a CAGR of 7.3%, reflecting the surge in demand for advanced cellular analysis in oncology, immunology, and hematological malignancies

- The Coagulation Reagents segment dominated the reagent category with a 39.87% revenue share in 2025, led by high demand for blood clotting tests in the diagnosis and monitoring of bleeding disorders, liver diseases, and cardiovascular conditions

- Cancer accounted for 41.62% of the market, preferred by the rising global burden of leukemia, lymphoma, and other hematological malignancies.

- The Autoimmune Disease segment is the fastest-growing application category, with a CAGR of 7.1%, driven by increasing prevalence of disorders such as lupus and rheumatoid arthritis affecting blood parameters.

Market Size & Forecast

- Global Market Value (2025): USD 2.51 Billion

- Expected Market Value (2033): USD 3.48 Billion

- Forecast CAGR (2026–2033): 4.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Haematology Market Segmentation

|

Attributes |

Haematology Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Roche Diagnostics (Switzerland) · Abbott (U.S.) · Siemens Healthineers AG (Germany) · Danaher (U.S.) · Sysmex Corporation (Japan) · BD (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · Beckman Coulter, Inc. (U.S.) · HORIBA, Ltd. (Japan) · Mindray Medical International Limited (China) · PerkinElmer Inc. (U.S.) · F. Hoffmann-La Roche Ltd (Switzerland) · Agilent Technologies, Inc. (U.S.) · QuidelOrtho Corporation (U.S.) · Illumina, Inc. (U.S.) · GSK plc (U.K.) · Novartis AG (Switzerland) · Amgen Inc. (U.S.) |

|

Market Opportunities |

· Expansion of precision hematology diagnostics using next-generation sequencing (NGS) and molecular profiling · Growing integration of AI-driven hematology analyzers in clinical laboratories · Rising demand for point-of-care (POC) hematology testing in emerging healthcare systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Haematology Market Trends

Trend: Growth in Molecular Diagnostics & Precision Hematology

Clinical laboratories are increasingly adopting molecular diagnostics and precision hematology techniques to improve early detection and classification of blood disorders such as leukemia, anemia, and lymphoma, enabling more targeted and personalized treatment approaches. The integration of next-generation sequencing, flow cytometry, and digital pathology is enhancing diagnostic accuracy and allowing detailed genetic and cellular profiling of hematological diseases. Hospitals and diagnostic centers are also leveraging automated analyzers and AI-assisted interpretation tools to streamline workflows and reduce turnaround time for large-scale blood testing. For instance, expanding use of NGS-based leukemia profiling in reference laboratories is improving risk stratification and treatment planning.

Haematology Market Dynamics

Key Market Driver: Rising Burden of Blood Disorders & Routine Screening Demand

The increasing global prevalence of hematological conditions such as anemia, hemophilia, and blood cancers is driving strong demand for routine blood testing and advanced diagnostic solutions across hospitals and diagnostic laboratories. Aging populations, nutritional deficiencies, and chronic disease comorbidities are further contributing to higher testing volumes and sustained utilization of hematology analyzers. Healthcare systems are also expanding preventive screening programs, encouraging early detection and continuous monitoring of blood-related abnormalities. For instance, large-scale national anemia screening initiatives are significantly increasing the adoption of automated complete blood count testing platforms.

Key Restraint/Challenge: High Cost of Advanced Hematology Technologies

A major challenge in the Haematology Market is the high cost associated with advanced diagnostic platforms such as molecular testing systems, flow cytometers, and fully automated hematology analyzers. These systems require substantial capital investment, specialized laboratory infrastructure, and skilled personnel, making adoption difficult for small and mid-sized diagnostic centers. Ongoing expenses related to reagents, maintenance, and software upgrades further increase the total cost of ownership. Limited reimbursement coverage in certain emerging healthcare markets also restricts widespread adoption of high-end hematology diagnostics. For instance, adoption of high-throughput flow cytometry systems remains concentrated in large tertiary care hospitals due to budget constraints.

Key Market Opportunity: Expansion of AI-Driven Hematology Diagnostics & Digital Laboratories

The integration of artificial intelligence and digital pathology platforms in hematology presents a significant opportunity for improving diagnostic accuracy, automation, and workflow efficiency in clinical laboratories. AI-enabled systems can assist in abnormal cell detection, predictive disease modeling, and automated report generation, reducing manual interpretation errors and enhancing productivity. The rise of cloud-based laboratory information systems is also enabling remote access to diagnostic data and centralized analysis across multi-site healthcare networks. For instance, AI-assisted blood smear analysis tools are increasingly being deployed in large diagnostic chains to support faster and more consistent hematology reporting.

Haematology Market Scope

The haematology market is segmented on the basis of product, reagent, application, and end user.

- By Product

On the basis of product, the Haematology Market is segmented into haematology analyzers, flow cytometers, coagulation analyzers, slide stainers, centrifuges, hemoglobinometers, and others. The Haematology Analyzers segment dominated the market with a 44.15% share in 2025, owing to their widespread use in routine complete blood count testing and high-throughput diagnostic workflows across hospitals and clinical laboratories. These systems are essential for rapid and accurate detection of blood disorders, enabling efficient screening of large patient populations. Increasing automation in diagnostic laboratories and integration with laboratory information systems is further strengthening adoption. Continuous technological advancements such as AI-based cell classification and digital morphology analysis are improving diagnostic precision. Growing demand for standardized, cost-efficient blood testing in both developed and emerging healthcare systems is further reinforcing dominance. The segment also benefits from high replacement demand in established hospital laboratories.

The Flow Cytometers segment is expected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing demand for advanced cellular analysis in oncology, immunology, and hematological malignancies. These systems enable multi-parameter analysis of individual cells, making them critical for leukemia and lymphoma diagnosis. Rising adoption of precision medicine and targeted therapies is further accelerating usage. Continuous improvements in laser technology and software analytics are enhancing accuracy and speed. Expanding applications in research institutes and pharmaceutical development are also supporting growth. Increasing investments in cancer diagnostics infrastructure is further boosting demand globally.

- By Reagent

On the basis of reagent, the Haematology Market is segmented into coagulation reagents, flow cytometry reagents, immuno-haematology reagents, and others. The Coagulation Reagents segment dominated the market with a 39.87% share in 2025, owing to high demand for blood clotting tests in the diagnosis and monitoring of bleeding disorders, liver diseases, and cardiovascular conditions. These reagents are widely used in hospitals and diagnostic laboratories for routine and emergency testing. Increasing prevalence of anticoagulant therapies and surgical procedures is further driving usage. Strong adoption in critical care and trauma settings supports continuous demand. Standardized testing protocols and automation in coagulation analyzers are improving efficiency. Rising focus on patient safety and perioperative care is reinforcing segment leadership.

The Flow Cytometry Reagents segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by rising use in advanced immunophenotyping and cancer diagnostics. These reagents are essential for identifying and characterizing abnormal cell populations in hematological malignancies. Increasing research in immuno-oncology and personalized medicine is further boosting demand. Expanding clinical trials and drug development activities are supporting reagent consumption. Continuous innovation in antibody panels and fluorescent markers is enhancing diagnostic capabilities. Growing adoption of high-throughput testing in research laboratories is further accelerating growth.

- By Application

On the basis of application, the Haematology Market is segmented into drug testing, autoimmune disease, cancer, diabetes mellitus, infectious disease, and others. The Cancer segment dominated the market with a 41.62% share in 2025, driven by the rising global burden of leukemia, lymphoma, and other hematological malignancies. Increasing demand for early detection and precise disease classification is boosting adoption of advanced hematology diagnostics. Expanding use of molecular and flow cytometry-based testing is improving cancer profiling accuracy. Growing investment in oncology research and targeted therapies is further supporting segment dominance. Hospitals and diagnostic centers are increasingly integrating multi-modal diagnostic platforms. Rising awareness of early cancer screening is also contributing to growth.

The Autoimmune Disease segment is expected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing prevalence of disorders such as lupus and rheumatoid arthritis affecting blood parameters. Advanced hematology testing is being widely used to monitor immune response and disease progression. Growing adoption of personalized treatment approaches is further boosting demand. Expanding research into immune system disorders is enhancing diagnostic innovation. Improved awareness and early diagnosis initiatives are supporting testing volumes. Increasing use of hematology analyzers in chronic disease monitoring is further accelerating growth.

- By End User

On the basis of end user, the Haematology Market is segmented into hospitals, clinical testing institutes, patient self-testing, and others. The Hospitals segment dominated the market with a 46.28% share in 2025, owing to high patient inflow, established laboratory infrastructure, and availability of skilled healthcare professionals. Hospitals serve as primary centers for diagnosis and treatment of blood disorders, driving consistent demand for hematology analyzers and reagents. Integration of automated laboratory systems is improving operational efficiency. Increasing emergency and inpatient care cases further supports high testing volumes. Strong investment in hospital-based diagnostic expansion is reinforcing market dominance. Government healthcare programs are also strengthening hospital diagnostic capabilities.

The Clinical Testing Institutes segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, driven by increasing outsourcing of diagnostic services and rising demand for specialized laboratory testing. These institutes offer cost-effective and high-throughput testing solutions compared to traditional hospital laboratories. Expanding diagnostic networks in emerging economies are supporting rapid growth. Adoption of advanced automation and digital reporting systems is improving efficiency and scalability. Increasing demand for preventive screening and routine blood testing is further boosting volumes. Growing private-sector investment in diagnostic chains is also accelerating segment expansion.

Haematology Market Regional Analysis

North America dominated the Haematology Market with the largest revenue share of 38.92% in 2025, supported by advanced diagnostic infrastructure, high prevalence of blood disorders, and strong adoption of automated hematology analyzers and molecular testing platforms. The region also benefits from high prevalence of blood disorders, well-established reimbursement frameworks, and widespread adoption of routine blood screening programs across hospitals and diagnostic centers. Increasing investments in precision medicine, molecular diagnostics, and AI-driven laboratory automation continue to strengthen North America’s leadership position in the global market.

U.S. Haematology Market Insight

The U.S. haematology market is witnessing strong growth due to rising prevalence of blood disorders, high adoption of advanced diagnostic technologies, and robust healthcare infrastructure. The country’s well-established hospital and clinical laboratory network, along with widespread use of automated hematology analyzers and molecular diagnostic platforms, is driving demand across routine testing and oncology applications. In addition, increasing investments in precision medicine, AI-driven laboratory automation, and large-scale screening programs are accelerating adoption across hospitals, diagnostic centers, and research institutions.

Europe Haematology Market Insight

The Europe haematology market remains a major contributor to global revenue, driven by strong healthcare systems, high awareness of early disease detection, and widespread adoption of advanced diagnostic solutions. The region benefits from established laboratory infrastructure, strong regulatory frameworks, and increasing use of flow cytometry and molecular hematology techniques in clinical practice. Growing investments in personalized medicine, cancer diagnostics, and automated laboratory systems continue to support market expansion across hospitals and diagnostic networks.

U.K. Haematology Market Insight

The U.K. haematology market is experiencing steady growth, supported by strong public healthcare infrastructure, rising demand for early disease diagnosis, and increasing adoption of automated laboratory systems. Expansion of national screening programs and growing use of advanced hematology analyzers in NHS hospitals are contributing to market development. Furthermore, integration of AI-based diagnostic tools, digital pathology, and molecular testing technologies is improving diagnostic accuracy and efficiency across clinical laboratories.

Germany Haematology Market Insight

The Germany haematology market is expanding steadily due to its advanced healthcare system, strong diagnostic capabilities, and increasing focus on precision medicine. Hospitals and diagnostic laboratories are increasingly adopting automated hematology analyzers, flow cytometry systems, and molecular testing platforms for accurate disease detection and monitoring. Continuous investments in laboratory modernization, cancer research, and digital healthcare technologies, along with strong pharmaceutical and biotech presence, are further driving market growth in Germany.

Asia-Pacific Haematology Market Insight

The Asia-Pacific haematology market is expected to witness rapid growth, driven by increasing healthcare expenditure, rising prevalence of blood disorders, and expanding diagnostic laboratory networks across countries such as China, India, and Japan. Growing awareness of early disease detection, improving access to advanced diagnostic technologies, and government initiatives supporting healthcare infrastructure development are fueling regional market expansion. In addition, increasing adoption of automated hematology analyzers and molecular diagnostic solutions is accelerating market penetration across hospitals and clinical laboratories.

Japan Haematology Market Insight

The Japan haematology market is witnessing consistent growth due to rising demand for advanced diagnostic technologies, strong healthcare infrastructure, and increasing focus on early disease detection. Hospitals and research institutions are increasingly adopting automated hematology systems, flow cytometry, and molecular diagnostics for accurate blood disorder analysis. Moreover, Japan’s emphasis on precision medicine, aging population, and integration of AI-based diagnostic tools are further contributing to market growth.

China Haematology Market Insight

The China haematology market is growing rapidly, driven by expanding healthcare infrastructure, increasing prevalence of hematological disorders, and rising demand for advanced diagnostic solutions. Government initiatives to improve early disease screening and strengthen hospital laboratory capabilities are significantly boosting adoption of hematology analyzers and molecular testing platforms. In addition, growing investments in biotechnology, rising awareness of blood-related diseases, and rapid expansion of diagnostic networks are positioning China as one of the fastest-growing markets globally.

Haematology Market Share

The haematology industry is primarily led by well-established companies, including:

- Roche Diagnostics (Switzerland)

- Abbott (U.S.)

- Siemens Healthineers AG (Germany)

- Danaher (U.S.)

- Sysmex Corporation (Japan)

- BD (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Beckman Coulter, Inc. (U.S.)

- HORIBA, Ltd. (Japan)

- Mindray Medical International Limited (China)

- PerkinElmer Inc. (U.S.)

- Hoffmann-La Roche Ltd (Switzerland)

- Agilent Technologies, Inc. (U.S.)

- QuidelOrtho Corporation (U.S.)

- Illumina, Inc. (U.S.)

- GSK plc (U.K.)

- Novartis AG (Switzerland)

- Amgen Inc. (U.S.)

Latest Developments in Haematology Market

- In September 2023, the U.S. FDA approved Ojjaara (momelotinib), developed by GSK, for the treatment of myelofibrosis in patients with anemia. This marked an important advancement in addressing both disease symptoms and anemia-related complications in hematologic malignancies. The drug provides a differentiated mechanism by inhibiting JAK1, JAK2, and ACVR1 pathways. It offers a targeted option for patients with limited treatment alternatives. The approval strengthens the JAK inhibitor segment within the hematology therapeutics landscape

- In August 2023, the U.S. FDA approved Talvey (talquetamab-tgvs), developed by Johnson & Johnson (Janssen), for the treatment of relapsed or refractory multiple myeloma. This bispecific antibody targets both GPRC5D and CD3, enabling immune-mediated destruction of cancer cells. The approval expanded innovative immunotherapy options in late-line hematologic malignancies. It supports improved survival outcomes in heavily pretreated patient populations

- In May 2023, the U.S. FDA approved Omisirge (omidubicel-onlv), developed by Gamida Cell, for use in patients undergoing allogeneic hematopoietic stem cell transplantation. This development improved stem cell transplant outcomes by reducing time to neutrophil recovery and infection risk. The therapy addresses a critical unmet need in blood cancer and bone marrow transplant procedures. It enhances transplant accessibility, especially for patients lacking matched donors

- In October 2022, the U.S. FDA approved Tecvayli (teclistamab-cqyv), developed by Johnson & Johnson (Janssen), as the first bispecific T-cell engager therapy for multiple myeloma. This approval introduced a new class of off-the-shelf immunotherapy in hematologic cancer treatment, reducing dependence on individualized cell manufacturing. The therapy enhances immune system targeting of malignant plasma cells through dual antigen binding. It has significantly influenced treatment pathways for heavily pretreated patients

- In March 2021, the U.S. FDA approved Abecma (idecabtagene vicleucel), developed by Bristol Myers Squibb and bluebird bio, as the first BCMA-targeted CAR-T cell therapy for relapsed or refractory multiple myeloma. This marked a major breakthrough in hematologic oncology, offering a novel personalized immunotherapy approach for patients with limited treatment options. The therapy strengthens the CAR-T segment within the hematology market by enabling highly targeted cancer cell destruction. It also accelerated global investment in cell and gene therapies for blood cancers

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.