Global Handheld Ultrasound Imaging Devices Market

Market Size in USD Billion

USD

1.83 Billion

USD

2.80 Billion

2024

2032

USD

1.83 Billion

USD

2.80 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.83 Billion | |

| USD 2.80 Billion | |

| % | |

|

Handheld Ultrasound Imaging Devices Market Size

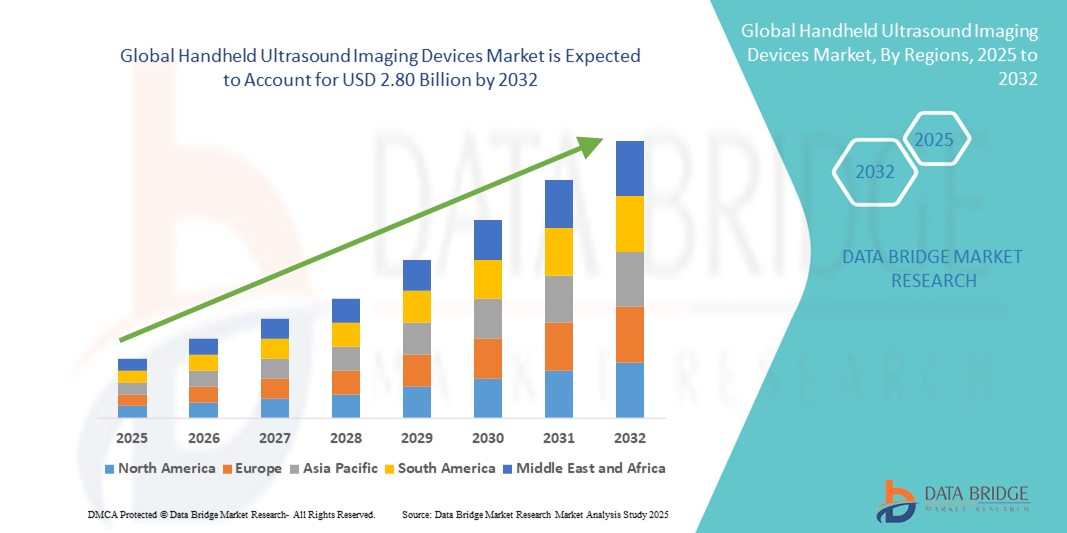

- The global handheld ultrasound imaging devices market size was valued at USD 1.83 billion in 2024 and is expected to reach USD 2.80 billion by 2032, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by the increasing demand for portable and point-of-care diagnostic solutions across healthcare settings, supported by advancements in imaging technology and miniaturization of medical devices

- Furthermore, rising adoption of handheld ultrasound devices among physicians for faster, accurate, and cost-effective diagnostics, coupled with expanding applications in emergency care, primary care, and remote healthcare, is positioning handheld ultrasound systems as a vital diagnostic tool. These converging factors are accelerating market uptake, thereby significantly boosting the industry’s growth

Handheld Ultrasound Imaging Devices Market Analysis

- Handheld ultrasound imaging devices, offering portable and real-time diagnostic capabilities, are becoming increasingly essential in modern healthcare due to their compact design, ease of use, and ability to deliver point-of-care imaging across multiple clinical applications

- The accelerating demand for handheld ultrasound systems is primarily fueled by the growing need for cost-effective and accessible diagnostic tools, rising use in emergency and critical care, and technological advancements in wireless connectivity, AI integration, and probe miniaturization

- North America dominated the handheld ultrasound imaging devices market with the largest revenue share of 39% in 2024, supported by advanced healthcare infrastructure, strong adoption of portable imaging solutions, and high demand in emergency, obstetrics, and primary care settings, with the U.S. leading usage across hospitals and specialty clinics

- Asia-Pacific is expected to be the fastest growing region in the handheld ultrasound imaging devices market during the forecast period due to rapid healthcare expansion, increasing medical expenditures, and growing need for portable diagnostic solutions in rural and underserved regions

- The Smartphone Application segment dominated the handheld ultrasound imaging devices market with a market share of 55.2% in 2024, driven by seamless integration with mobile platforms, enhanced connectivity, and ease of use for physicians across diverse care settings

Report Scope and Handheld Ultrasound Imaging Devices Market Segmentation

|

Attributes |

Handheld Ultrasound Imaging Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Handheld Ultrasound Imaging Devices Market Trends

Rising Adoption of AI-Integrated and Connected Imaging Solutions

- A significant and accelerating trend in the global handheld ultrasound imaging devices market is the growing integration of artificial intelligence (AI), wireless connectivity, and smartphone compatibility, which together enhance diagnostic accuracy, portability, and clinical efficiency

- For instance, Butterfly Network’s Butterfly iQ+ leverages AI and smartphone connectivity to deliver advanced imaging capabilities on a handheld probe, while Philips Lumify connects directly to smart devices, enabling on-the-go diagnostics and remote consultation

- AI integration enables features such as automated image interpretation, anomaly detection, and workflow optimization, reducing operator dependency and improving diagnostic outcomes. GE HealthCare’s handheld ultrasound offerings, for example, incorporate AI to guide less experienced users in capturing optimal images

- The seamless connectivity of handheld ultrasound devices with cloud platforms allows clinicians to securely store, share, and analyze scans in real time, supporting telemedicine and collaborative care. This has proven particularly valuable in rural and resource-limited settings

- This trend towards intelligent, connected, and highly portable imaging solutions is transforming point-of-care diagnostics by making ultrasound accessible beyond traditional hospital settings. Consequently, companies such as Clarius Mobile Health are advancing handheld ultrasound systems with cloud integration, AI-driven features, and app-based platforms for a unified diagnostic experience

- The demand for handheld ultrasound devices that combine AI support, wireless connectivity, and smartphone integration is rapidly growing across emergency medicine, primary care, and remote healthcare, as providers increasingly prioritize efficiency, accuracy, and accessibility

Handheld Ultrasound Imaging Devices Market Dynamics

Drive

Expanding Need for Point-of-Care and Cost-Effective Diagnostics

- The increasing demand for point-of-care diagnostic solutions across healthcare facilities, coupled with the global push for cost-effective imaging, is a significant driver for the growth of handheld ultrasound devices

- For instance, in March 2024, Butterfly Network announced enhancements to its Butterfly iQ+ platform, expanding AI-driven features to assist clinicians in primary care and emergency medicine, underscoring the industry’s shift towards portable, intelligent imaging system

- Handheld ultrasound devices offer clinicians the ability to quickly perform bedside diagnostics, guide procedures, and make rapid decisions in critical scenarios such as trauma, obstetrics, and cardiac emergencies

- Furthermore, their portability and relatively lower cost compared to traditional cart-based ultrasound systems are making them more accessible to smaller clinics, maternity centers, and healthcare providers in emerging markets

- The growing integration of handheld ultrasound with smartphone apps and wireless platforms enhances usability, making it easier for physicians to share scans, consult remotely, and integrate results into electronic health records (EHR). This convenience is propelling adoption in both developed and developing healthcare systems

Restraint/Challenge

Limited Imaging Capabilities and Cost Barriers in Adoption

- Despite their advantages, handheld ultrasound devices face limitations in imaging depth, battery life, and functionality compared to high-end cart-based systems, which can restrict their use in complex diagnostic procedures

- For instance, while devices such as Philips Lumify and Clarius HD3 deliver excellent portability, they may not match the resolution or advanced features of full-scale hospital ultrasound equipment, making some specialists hesitant to fully adopt them

- In addition, the initial cost of advanced handheld ultrasound devices, particularly those integrated with AI or cloud-based platforms, remains relatively high for budget-constrained facilities, particularly in developing regions

- Training requirements also act as a barrier, as less experienced clinicians may find it challenging to use handheld ultrasound effectively without adequate guidance. Although AI-guided imaging is mitigating this, gaps remain in standardization

- Addressing these challenges through further R&D into imaging quality, cost reduction strategies, and broader physician training initiatives will be vital for ensuring the sustained growth and wider adoption of handheld ultrasound imaging devices globally

Handheld Ultrasound Imaging Devices Market Scope

The market is segmented on the basis of application area, type of transducer array, mode of imaging, type of software, connectivity provision, data management feature, and end-users.

- By Application Area

On the basis of application, the handheld ultrasound imaging devices market is segmented into cardiac, emergency medicine, gynecological or obstetrics, musculoskeletal, pulmonary, urological, vascular, and other applications. The Emergency Medicine segment dominated the market with a revenue share of 28.6% in 2024, as handheld ultrasound devices are increasingly vital in trauma care, intensive care units, and critical emergencies. Their ability to provide immediate, real-time diagnostic insights at the bedside allows healthcare professionals to make rapid clinical decisions. Emergency physicians increasingly rely on handheld ultrasound for guiding procedures such as central line placement and detecting internal bleeding. The portability and speed of these devices make them indispensable in emergency departments and ambulance settings. Furthermore, rising global investments in emergency healthcare infrastructure are supporting the segment’s dominance.

The Gynecological or Obstetrics segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing demand for portable solutions in maternity clinics and remote pregnancy monitoring. Handheld ultrasound enables quick, non-invasive imaging for fetal growth, gestational age, and maternal health assessments. As maternal care expands in emerging markets, cost-effective handheld devices offer a viable alternative to traditional cart-based machines. Increasing awareness about prenatal care and rising healthcare access in rural regions also enhance adoption. Integration with smartphone apps for sharing images with specialists remotely further drives growth in this segment.

- By Type of Transducer Array

On the basis of type of transducer array, the handheld ultrasound imaging devices market is segmented into curved, endocavity, linear, phased, and other scanners. The Linear transducer segment held the largest share at 32.4% in 2024, owing to its wide application in vascular, musculoskeletal, and small parts imaging. Its high-frequency range provides superior resolution, making it especially useful for detailed imaging of superficial structures. Clinicians prefer linear probes in emergency care for procedures such as vascular access and in outpatient settings for musculoskeletal diagnostics. In addition, linear probes are easy to integrate with handheld platforms, enhancing their adoption. The rising use of handheld ultrasound in orthopedic and sports medicine further solidifies this segment’s dominance.

The Curved transducer segment is anticipated to grow at the fastest CAGR during the forecast period, primarily driven by its expanding use in abdominal and obstetric imaging. Its deeper penetration capabilities make it essential for examining internal organs and fetal monitoring in pregnancy care. With rising prevalence of chronic liver and kidney diseases, curved transducers are gaining traction in point-of-care settings. Their compatibility with handheld systems is improving with advances in miniaturization and connectivity. Moreover, demand from maternity clinics and rural healthcare centers is driving adoption in both developed and emerging markets.

- By Mode of Imaging

On the basis of mode of imaging, the handheld ultrasound imaging devices market is segmented into brightness (B-mode), color Doppler, motion (M-mode), power Doppler, pulsed wave, tissue harmonic, and others. The Brightness (B-Mode) imaging segment dominated the market with a 35.8% share in 2024, as it is the most widely adopted imaging mode for general diagnostics. B-mode provides two-dimensional grayscale images that are essential for visualizing anatomical structures in real-time. Its simplicity and versatility make it the first choice for point-of-care examinations across emergency, obstetrics, and primary care. Clinicians value B-mode for rapid assessments of organ size, soft tissue abnormalities, and fluid accumulation. Its fundamental role in diagnostic imaging ensures steady demand across all healthcare environments.

The Color Doppler imaging segment is expected to witness the fastest CAGR from 2025 to 2032, supported by its ability to visualize blood flow and detect vascular abnormalities. This functionality is critical in cardiology, vascular medicine, and obstetrics, where monitoring blood supply is crucial. Handheld ultrasound devices with Doppler capabilities empower clinicians to detect conditions such as deep vein thrombosis and monitor fetal circulation. As handheld devices continue to integrate advanced Doppler features with minimal power usage, adoption is expected to accelerate significantly.

- By Type of Software

On the basis of type of software, the handheld ultrasound imaging devices market is segmented into smartphone application-based scanners and customized software-based scanners. The Smartphone application-based scanners dominated the market with a 55.2% share in 2024, driven by the seamless integration of ultrasound probes with mobile platforms. These devices offer physicians the convenience of connecting directly to iOS or Android systems for real-time imaging. Smartphone-based scanners also allow instant sharing of results via cloud storage or telemedicine platforms. Their lower cost compared to customized solutions makes them attractive for smaller clinics and individual practitioners. The ease of portability and user-friendly interface are key drivers of adoption. The growth of digital health ecosystems further cements this segment’s leadership.

The Customized software-based scanners are projected to grow at the fastest CAGR during the forecast period, as hospitals and diagnostic centers increasingly require advanced functionality. These systems provide tailored features, integration with electronic health records (EHR), and support for AI-driven image analysis. They are particularly suited for specialized applications such as cardiology, gynecology, and oncology imaging. As demand for more advanced handheld solutions rises, customized software platforms will play an increasingly important role in meeting clinical needs.

- By Connectivity Provision

On the basis of connectivity provision, the handheld ultrasound imaging devices market is segmented into USB, cellular or Wi-Fi, and Bluetooth. The Cellular or Wi-Fi segment accounted for the largest share at 46.2% in 2024, owing to its ability to provide real-time connectivity for telemedicine and cloud storage. Clinicians can instantly transmit images for remote consultations, improving accessibility in rural and underserved areas. Wi-Fi-enabled handheld devices are highly preferred in hospitals and clinics due to seamless integration with IT systems. Cellular connectivity expands the utility of handheld ultrasound in mobile healthcare services and ambulances. This connectivity ensures patient scans can be reviewed by specialists regardless of location, boosting adoption.

The Bluetooth segment is expected to grow at the fastest CAGR from 2025 to 2032, driven by its low energy consumption and secure, short-range connectivity. Bluetooth-based handheld ultrasound devices are popular for their portability and ease of pairing with smartphones and tablets. They are especially suitable for point-of-care use in smaller clinics and home healthcare settings. With rising focus on compact, energy-efficient designs, Bluetooth-enabled ultrasound systems are gaining traction among practitioners seeking convenient, wireless solutions.

- By Data Management Feature

On the basis of data management feature, the handheld ultrasound imaging devices market is segmented into internal, external, and cloud or remote monitoring. The Cloud or remote monitoring segment held the largest share of 41.5% in 2024, as cloud integration has become central to modern medical imaging. Cloud-enabled handheld ultrasound devices allow secure storage, retrieval, and sharing of patient data across multiple providers. This feature supports collaboration among healthcare professionals and facilitates AI-driven analytics for enhanced diagnosis. Cloud solutions are also vital for telemedicine and remote patient monitoring applications. The ability to integrate with EHR systems enhances workflow efficiency, making this segment dominant in both developed and emerging healthcare systems.

The External data management segment is projected to record the fastest CAGR during 2025–2032, as healthcare providers increasingly demand portable and cost-effective data storage options. External drives and portable storage devices allow clinicians to maintain control over patient data without relying entirely on internet connectivity. This is particularly beneficial in areas with poor internet infrastructure. The affordability and simplicity of external storage solutions ensure continued growth alongside cloud-based models.

- By End-Users

On the basis of end users, the handheld ultrasound imaging devices market is segmented into ambulatory surgical centers, diagnostic imaging centers, hospitals, maternity clinics, specialty clinics, and other end-users. The Hospitals segment dominated the market with a 39.8% share in 2024, due to widespread adoption of handheld ultrasound across multiple departments. Hospitals use these devices in emergency medicine, cardiology, obstetrics, and intensive care units, making them essential for everyday operations. The availability of skilled healthcare professionals and IT infrastructure further supports adoption in hospitals. Moreover, increasing investments in advanced diagnostic technologies strengthen hospitals’ role as primary adopters. Their central role in healthcare delivery ensures this segment remains the largest contributor to revenue.

The Maternity Clinics segment is expected to grow at the fastest CAGR during 2025–2032, driven by the rising demand for portable fetal monitoring and maternal health assessments. Handheld ultrasound devices allow quick, safe, and cost-effective imaging for pregnancy care, even in remote or rural areas. The increasing number of specialized maternity clinics in emerging economies is expanding demand further. Integration with mobile apps for sharing images and reports enhances utility for both patients and providers. As maternal and neonatal care becomes a global priority, this segment is poised for strong growth.

Handheld Ultrasound Imaging Devices Market Regional Analysis

- North America dominated the handheld ultrasound imaging devices market with the largest revenue share of 39% in 2024, supported by advanced healthcare infrastructure, strong adoption of portable imaging solutions, and high demand in emergency, obstetrics, and primary care settings

- Physicians in the region highly value the portability, real-time imaging capabilities, and seamless connectivity of handheld ultrasound devices, which are increasingly used across emergency medicine, primary care, and maternal health settings

- This widespread adoption is further supported by high healthcare spending, a technologically advanced clinical workforce, and growing demand for point-of-care diagnostics, establishing handheld ultrasound systems as a vital imaging solution for both hospitals and specialty clinics

U.S. Handheld Ultrasound Imaging Devices Market Insight

The U.S. handheld ultrasound imaging devices market captured the largest revenue share of 79% in 2024 within North America, fueled by the rapid adoption of point-of-care diagnostics and a strong demand for portable imaging solutions across emergency, cardiac, and obstetric applications. Physicians and healthcare providers increasingly prefer handheld ultrasound systems for their affordability, ease of use, and integration with smartphones and tablets. The trend toward value-based care and home-based monitoring is further accelerating adoption. Moreover, the presence of leading companies such as Butterfly Network, GE HealthCare, and Philips significantly contributes to market expansion.

Europe Handheld Ultrasound Imaging Devices Market Insight

The Europe handheld ultrasound imaging devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare quality regulations and the push for more accessible diagnostic imaging. Rising investments in telemedicine and remote healthcare services are fostering handheld ultrasound adoption across both urban and rural settings. European clinicians are also drawn to the cost-effectiveness and mobility of these devices. Growth is significant across hospitals, specialty clinics, and maternity centers, with handheld ultrasound increasingly used in both primary care and emergency medicine.

U.K. Handheld Ultrasound Imaging Devices Market Insight

The U.K. handheld ultrasound imaging devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the National Health Service (NHS) initiatives supporting early diagnostics and home-based healthcare solutions. The growing need for quick, non-invasive diagnostic tools is encouraging adoption in maternity, cardiac, and musculoskeletal care. In addition, the U.K.’s strong digital health ecosystem and ongoing integration of AI-enhanced imaging software are expected to accelerate market penetration. The affordability and efficiency of handheld devices make them attractive for both public healthcare and private practices.

Germany Handheld Ultrasound Imaging Devices Market Insight

The Germany handheld ultrasound imaging devices market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s emphasis on medical innovation and sustainable healthcare practices. German healthcare providers are increasingly adopting handheld ultrasound for bedside diagnostics, reducing reliance on bulky imaging systems. The integration of these devices with advanced imaging software and secure data-sharing platforms aligns with the country’s strong focus on digital healthcare infrastructure. Growing demand is evident across cardiology, obstetrics, and musculoskeletal applications, particularly within hospitals and specialty clinics.

Asia-Pacific Handheld Ultrasound Imaging Devices Market Insight

The Asia-Pacific handheld ultrasound imaging devices market is poised to grow at the fastest CAGR of 23.8% during the forecast period of 2025 to 2032, driven by increasing healthcare access, rising disposable incomes, and rapid digital transformation in countries such as China, Japan, and India. The region’s emphasis on affordable healthcare, combined with government initiatives to expand rural diagnostic coverage, is accelerating adoption. APAC also benefits from being a major manufacturing hub for medical devices, enhancing affordability and accessibility. Rising prevalence of cardiovascular and maternal health conditions further fuels demand for portable ultrasound systems.

Japan Handheld Ultrasound Imaging Devices Market Insight

The Japan handheld ultrasound imaging devices market is gaining momentum due to the nation’s advanced healthcare ecosystem and strong preference for high-precision diagnostic technologies. Clinicians are increasingly using handheld ultrasound in emergency medicine, maternity care, and chronic disease monitoring. The integration of AI-driven imaging, alongside the compatibility of devices with telehealth platforms, is fueling adoption. Moreover, Japan’s aging population is such asly to spur further demand for easy-to-use, portable imaging systems that support point-of-care diagnosis in both clinical and homecare settings.

India Handheld Ultrasound Imaging Devices Market Insight

The India handheld ultrasound imaging devices market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding middle class, increasing focus on maternal and child health, and government-backed healthcare initiatives. Handheld ultrasound devices are becoming essential for rural and semi-urban regions where access to traditional imaging infrastructure is limited. The affordability and portability of these systems, coupled with the rise of local manufacturers and startups, are accelerating adoption. In addition, the rapid growth of telemedicine and mobile health applications further strengthens India’s leadership position in the APAC market.

Handheld Ultrasound Imaging Devices Market Share

The handheld ultrasound imaging devices industry is primarily led by well-established companies, including:

- Butterfly Network, inc (U.S.)

- Clarius Mobile Health Corp. (Canada)

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- FUJIFILM Sonosite, Inc. (U.S.)

- EchoNous, Inc., or its affiliates (U.S.)

- Exo Imaging, Inc (U.S.)

- Healcerion Co., Ltd. (South Korea)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- CHISON Medical Technologies Co., Ltd. (China)

- SonoScape Medical Corp. (China)

- Shantou Institute of Ultrasonic Instruments Co., Ltd. (China)

- ALPINION MEDICAL SYSTEMS Co., Ltd. (South Korea)

- EDAN Instruments, Inc. (China)

- Interson Corporation (U.S.)

- Pulsenmore Ltd. (Israel)

- Biim Ultrasound AS (Norway)

- Vave Health, Inc. (U.S.)

- Vinno Corporation. (China)

- Shenzhen Wisonic Medical Technology Co., Ltd (China)

What are the Recent Developments in Global Handheld Ultrasound Imaging Devices Market?

- In June 2025, Clarius Mobile Health received FDA clearance for Clarius OB AI, its eighth AI model for handheld ultrasound. This innovation automates fetal biometric measurements (e.g., fetal age, weight, growth), enabling even less experienced users such as midwives and nurses to confidently obtain accurate prenatal imaging using the Clarius C3 HD3 scanner

- In December 2024, SuperSonic Imagine introduced PocketVu, a new fleet of handheld ultrasound devices offering multiple scanning modes, AI-powered automatic image quality adjustments, DICOM 3.0 compatibility, long battery life, and support for applications across abdominal, cardiac, musculoskeletal, vascular, and obstetric imaging

- In June 2024, Esaote unveiled the AI-powered MyLab E80 ultrasound system at the SIRM Congress in Milan the first in its new "E" Series offering AI-driven workflow automation, fusion imaging, intuitive touch-control, and battery-powered portability for advanced diagnostics

- In February 2024, GE HealthCare launched its next-generation LOGIQ ultrasound portfolio at ECR 2024, integrating the Vscan Air CL wireless handheld probe with curved and linear transducers, along with AI-enhanced workflow tools, as part of their LOGIQ E10 Series, LOGIQ Fortis, and the newcomer LOGIQ Totus

- In January 2024, Butterfly Network announced FDA clearance of its next-generation handheld point-of-care ultrasound system, Butterfly iQ3, featuring advanced semiconductor technology with new digital imaging modes (iQ Slice and iQ Fan), enhanced image resolution, ergonomic design, and faster 3D capabilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.