Global Hard Coatings Market

Market Size in USD Billion

USD

1.26 Billion

USD

2.36 Billion

2025

2033

USD

1.26 Billion

USD

2.36 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.26 Billion | |

| USD 2.36 Billion | |

| % | |

|

Hard Coating Market Overview

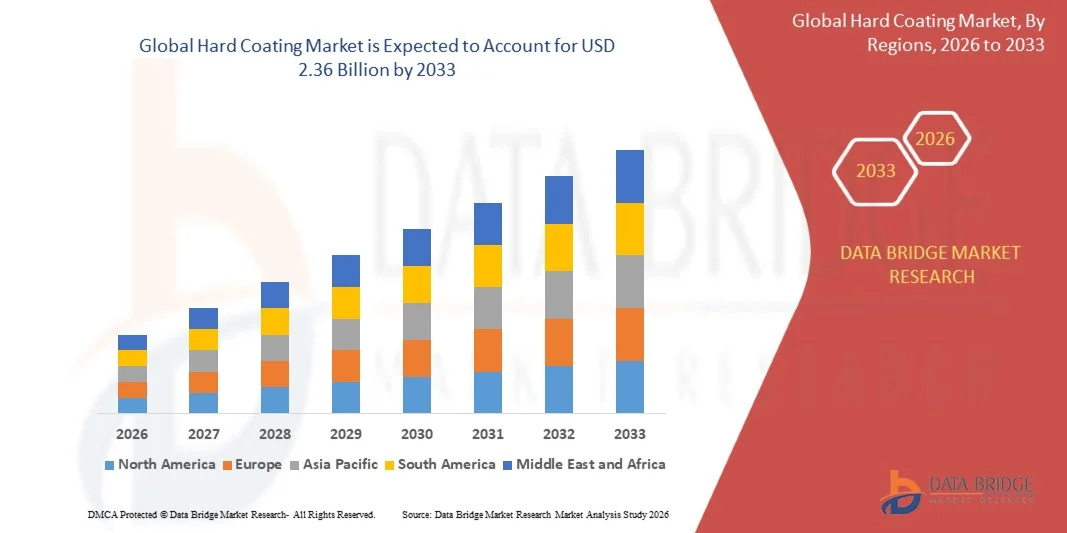

As per Data Bridge Market Research analysis the Hard Coating Market was valued at USD 1.26 billion in 2025 and is projected to reach USD 2.36 billion by 2033, growing at a CAGR of 8.15% from 2026 to 2033. The market is witnessing strong growth driven by increasing demand for wear-resistant, corrosion-resistant, and high-durability surface protection solutions across automotive, aerospace, industrial machinery, electronics, and medical device industries. Rising emphasis on extending product lifespan and improving performance efficiency is further accelerating adoption of advanced hard coating technologies globally.

The growing use of precision engineering components and high-performance materials is significantly boosting demand for hard coatings such as physical vapor deposition (PVD), chemical vapor deposition (CVD), and thermal spray coatings. These coatings are increasingly used to enhance hardness, reduce friction, and improve resistance to extreme operating conditions in automotive engine components, cutting tools, and aerospace parts. In addition, rapid industrialization, expanding manufacturing activities, and increasing focus on energy efficiency and maintenance cost reduction are further supporting global market expansion.

Key Market Trends & Insights

- North America dominated the hard coating market with the largest revenue share of 38.4% in 2025, supported by strong aerospace and automotive manufacturing base, high adoption of advanced coating technologies, and strong R&D investments in surface engineering solutions.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 9.2% from 2026 to 2033. Growth is driven by rapid industrialization, expanding automotive and electronics manufacturing, increasing infrastructure development, and rising adoption of advanced coating technologies in China, India, and Japan.

- The nitrides segment held the largest market revenue share of approximately 34.7% in 2025 driven by its extensive use in cutting tools, automotive components, and aerospace parts due to high hardness, thermal stability, and wear resistance. Nitrides such as titanium nitride are widely preferred for improving tool life and reducing friction in high-performance machining operations.

- The multi-component coatings segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing demand for advanced performance coatings with enhanced corrosion resistance and multi-functional properties. Rising adoption in aerospace turbines, semiconductor equipment, and high-precision industrial tools is further accelerating segment expansion.

- The cutting tools segment held the largest market revenue share of approximately 29.4% in 2025 driven by strong demand from automotive, aerospace, and industrial machining industries. Hard coatings are widely used on drills, milling cutters, and inserts to enhance durability, reduce wear, and improve machining efficiency.

- The bearings and gears segment is projected to register the fastest growth at a CAGR of 8.8% from 2026 to 2033, driven by increasing demand for high-performance automotive systems and industrial machinery requiring reduced friction, improved load capacity, and longer service life under extreme operating conditions.

- The physical vapour deposition segment held the largest market revenue share of approximately 57.9% in 2025 driven by its widespread use in precision coating applications, including cutting tools, electronics, and medical instruments. PVD is preferred due to its ability to produce thin, uniform, and high-hardness coatings at relatively lower processing temperatures.

- The chemical vapour deposition segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for ultra-durable coatings in aerospace, semiconductor, and high-temperature industrial applications. Its superior coating density and adhesion properties are further supporting adoption in advanced engineering applications.

- The automotive and transportation segment held the largest market revenue share of approximately 31.2% in 2025 driven by increasing use of hard coatings in engine components, transmission systems, and wear-resistant parts. Growing production of electric and hybrid vehicles is further strengthening demand for high-performance coatings.

- The medical equipment segment is projected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033, driven by rising adoption of coated surgical instruments, implants, and diagnostic devices requiring high biocompatibility, corrosion resistance, and durability. Expanding healthcare infrastructure and increasing surgical procedures are further accelerating segment growth globally.

Market Size & Forecast

- Global Market Value (2025): USD 1.26 Billion

- Expected Market Value (2033): USD 2.36 Billion

- Forecast CAGR (2026–2033): 8.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Hard coating Market Segmentation

|

Attributes |

Hard coating Key Market Insights |

|

Segments Covered |

· By Material: Nitrides, Oxides, Carbides, Carbon-Based, Borides, and Multi-Component Coatings · By Application: Cutting Tools, Decorative Coatings, Optics, Gears, Bearings, Pistons, Cams, Cylinders, and Hydraulic/Pneumatic Components · By Deposition Technique: Physical Vapour Deposition, and Chemical Vapour Deposition · By End-Use Industry: General Manufacturing, Automotive and Transportation, Buildings and Construction, Medical Equipment, Sporting Goods, Food Manufacturing Equipment, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• IHI HAUZER B.V. (Netherlands) |

|

Market Opportunities |

• Expansion Of Aerospace And Automotive Surface Protection Applications |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hard Coating Market Trends

Trend: Growth In High-Performance Wear Resistant And Multi-Functional Surface Coating Technologies

Increasing demand for durable, corrosion-resistant, and high-hardness surface protection solutions across automotive, aerospace, industrial machinery, electronics, and medical device manufacturing is driving adoption of advanced hard coating technologies. Conventional surface treatments such as electroplating and basic thermal coatings are being replaced due to limited wear resistance, environmental concerns, and shorter service life, encouraging industries to shift toward high-performance coating systems with superior adhesion and thermal stability.

In modern automotive and aerospace applications, hard coatings such as physical vapor deposition (PVD) and chemical vapor deposition (CVD) are widely applied on engine components, turbine blades, and cutting tools, For instance to enhance wear resistance and reduce friction, resulting in improved fuel efficiency and extended component lifespan under extreme operating conditions. In industrial machining, coated cutting tools are increasingly used to achieve higher precision and longer operational cycles, reducing downtime and maintenance costs.

The rapid expansion of semiconductor manufacturing and precision electronics is also increasing demand for ultra-thin, high-hardness coatings that provide electrical insulation, corrosion protection, and thermal resistance in micro-scale components. In addition, medical device manufacturers are adopting hard coatings on surgical instruments and implants to improve biocompatibility and durability. Industry data from 2025 indicates that PVD-coated cutting tools demonstrated up to 30–40% longer tool life compared to uncoated tools in high-speed machining applications, significantly improving production efficiency.

Hard Coating Market Dynamics

Key Market Driver: Rising Demand For Wear Resistance And High-Performance Industrial Components

Industries worldwide are increasingly focused on improving equipment lifespan, reducing maintenance costs, and enhancing operational efficiency, driving strong demand for advanced hard coating solutions. High-performance coatings provide superior hardness, corrosion resistance, and thermal stability, making them essential for demanding applications in automotive engines, aerospace components, and industrial tools.

Automotive manufacturers are increasingly applying hard coatings on engine parts, transmission systems, and brake components, For instance to reduce friction, improve fuel efficiency, and enhance durability under high-temperature and high-pressure operating conditions.

Similarly, aerospace and defense industries are adopting advanced coating systems on turbine blades and structural components to withstand extreme temperatures and mechanical stress. Industrial case studies in Europe and North America during 2024 reported component lifespan improvements of around 25–35% after applying advanced PVD and CVD coatings in heavy-duty machining and aerospace operations.

Key Restraint/Challenge: High Equipment Costs And Complex Deposition Processes

The hard coating market faces challenges due to high capital investment required for coating equipment such as vacuum deposition systems, sputtering units, and CVD reactors. These systems require significant upfront costs, skilled operators, and controlled environments, limiting adoption among small and medium-sized manufacturers.

In addition, complex process parameters such as temperature control, vacuum stability, and material compatibility increase operational difficulty and production costs. Variability in coating quality and limited scalability for large-volume applications further restrict market penetration in cost-sensitive regions.

Industry assessments indicate that advanced PVD and CVD coating systems can increase production costs by approximately 15–25% compared to conventional surface treatment methods, impacting adoption in price-sensitive manufacturing segments.

Key Market Opportunity: Expansion Of Semiconductor, Medical, And Aerospace Applications

Rapid growth in semiconductor manufacturing, precision engineering, and advanced medical devices is creating significant opportunities for hard coating technologies. Increasing demand for miniaturized electronic components and high-performance surgical tools is driving adoption of ultra-thin, high-durability coatings with superior functional properties.

Hard coatings are being widely applied in semiconductor fabrication equipment, medical implants, and aerospace components, For instance to enhance corrosion resistance, improve wear life, and ensure stable performance under extreme operational conditions.

In addition, rising investment in electric vehicles and renewable energy infrastructure is expanding the use of hard coatings in battery systems, wind turbine components, and power electronics. Industry reports from 2025 indicate that coated aerospace components achieved efficiency improvements of around 20–30% in operational durability, supporting longer maintenance cycles and reduced lifecycle costs.

Hard Coating Market Scope

The market is segmented on the basis of material, application, deposition technique, and end-use industry.

- By Material

On the basis of material, the Hard Coating Market is segmented into nitrides, oxides, carbides, carbon-based, borides, and multi-component coatings. The nitrides segment held the largest market revenue share of approximately 34.7% in 2025 driven by its extensive use in cutting tools, automotive components, and aerospace parts due to high hardness, thermal stability, and wear resistance. Nitrides such as titanium nitride are widely preferred for improving tool life and reducing friction in high-performance machining operations.

The multi-component coatings segment is projected to register the fastest growth at a CAGR of 9.6% from 2026 to 2033, driven by increasing demand for advanced performance coatings with enhanced corrosion resistance and multi-functional properties. Rising adoption in aerospace turbines, semiconductor equipment, and high-precision industrial tools is further accelerating segment expansion.

- By Application

On the basis of application, the market is segmented into cutting tools, decorative coatings, optics, gears, bearings, pistons, cams, cylinders, and hydraulic/pneumatic components. The cutting tools segment held the largest market revenue share of approximately 29.4% in 2025 driven by strong demand from automotive, aerospace, and industrial machining industries. Hard coatings are widely used on drills, milling cutters, and inserts to enhance durability, reduce wear, and improve machining efficiency.

The bearings and gears segment is projected to register the fastest growth at a CAGR of 8.8% from 2026 to 2033, driven by increasing demand for high-performance automotive systems and industrial machinery requiring reduced friction, improved load capacity, and longer service life under extreme operating conditions.

- By Deposition Technique

On the basis of deposition technique, the market is segmented into physical vapour deposition and chemical vapour deposition. The physical vapour deposition segment held the largest market revenue share of approximately 57.9% in 2025 driven by its widespread use in precision coating applications, including cutting tools, electronics, and medical instruments. PVD is preferred due to its ability to produce thin, uniform, and high-hardness coatings at relatively lower processing temperatures.

The chemical vapour deposition segment is projected to register the fastest growth at a CAGR of 9.1% from 2026 to 2033, driven by increasing demand for ultra-durable coatings in aerospace, semiconductor, and high-temperature industrial applications. Its superior coating density and adhesion properties are further supporting adoption in advanced engineering applications.

- By End-Use Industry

On the basis of end-use industry, the market is segmented into general manufacturing, automotive and transportation, buildings and construction, medical equipment, sporting goods, food manufacturing equipment, and others. The automotive and transportation segment held the largest market revenue share of approximately 31.2% in 2025 driven by increasing use of hard coatings in engine components, transmission systems, and wear-resistant parts. Growing production of electric and hybrid vehicles is further strengthening demand for high-performance coatings.

The medical equipment segment is projected to register the fastest growth at a CAGR of 9.3% from 2026 to 2033, driven by rising adoption of coated surgical instruments, implants, and diagnostic devices requiring high biocompatibility, corrosion resistance, and durability. Expanding healthcare infrastructure and increasing surgical procedures are further accelerating segment growth globally.

Hard Coating Market Regional Analysis

North America Hard Coating Market Insight

North America dominated the hard coating market with the largest revenue share of 38.4% in 2025, supported by strong demand from automotive, aerospace, industrial manufacturing, and medical device industries along with early adoption of advanced surface engineering technologies. Manufacturers in the region highly value wear resistance, corrosion protection, and extended component life offered by hard coatings across high-performance applications such as cutting tools, engine components, and aerospace parts. This widespread adoption is further supported by strong R&D investments, advanced manufacturing infrastructure, and increasing focus on operational efficiency, establishing hard coatings as a critical solution for high-durability industrial applications.

U.S. Hard Coating Market Insight

The U.S. hard coating market captured the largest revenue share within North America in 2025, driven by rapid expansion of aerospace manufacturing, automotive production, and semiconductor equipment industries. Companies are increasingly prioritizing advanced PVD and CVD coating technologies to enhance product durability and reduce maintenance costs. Growing demand for high-precision machining tools, medical implants, and energy-efficient industrial components is further accelerating market growth. In addition, strong integration of advanced materials science and coating innovation in industrial production is significantly supporting industry expansion across the country.

Europe Hard Coating Market Insight

The Europe hard coating market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by strict environmental regulations, increasing demand for sustainable manufacturing, and strong automotive and aerospace industries. European manufacturers are increasingly adopting eco-efficient coating technologies to reduce emissions and improve material efficiency. Rising demand for high-performance industrial tools and precision engineering components is further supporting adoption. In addition, growth in renewable energy equipment manufacturing and advanced machinery production is accelerating market expansion across the region.

U.K. Hard Coating Market Insight

The U.K. hard coating market is expected to witness steady growth from 2026 to 2033, driven by rising aerospace production, automotive innovation, and increasing demand for advanced industrial machinery. Manufacturers are adopting hard coatings to improve wear resistance, reduce friction, and enhance component longevity in critical applications. In addition, growing focus on sustainable manufacturing practices and high-value engineering exports is further contributing to market expansion across the country.

Germany Hard Coating Market Insight

The Germany hard coating market is expected to witness significant growth from 2026 to 2033, fueled by strong automotive manufacturing, advanced engineering capabilities, and high demand for precision tools and machinery. Hard coatings are widely used in engine components, gears, bearings, and cutting tools to improve performance and durability under extreme conditions. Germany’s focus on industrial innovation and energy-efficient production processes is further accelerating adoption across multiple end-use sectors.

Asia-Pacific Hard Coating Market Insight

The Asia-Pacific hard coating market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding automotive production, and growing electronics manufacturing in countries such as China, Japan, and India. Increasing demand for cost-effective yet high-performance coating solutions is significantly boosting adoption. In addition, rising infrastructure development and strong growth in precision engineering industries are further driving regional market expansion.

Japan Hard Coating Market Insight

The Japan hard coating market is expected to witness strong growth from 2026 to 2033 due to high demand for advanced manufacturing technologies, precision engineering, and automotive innovation. Japanese industries are increasingly adopting hard coatings in electronics, automotive components, and medical devices to enhance durability and performance. Strong focus on miniaturization and high-precision production is further supporting adoption of advanced coating technologies across industrial applications.

China Hard Coating Market Insight

The China hard coating market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid industrial expansion, strong automotive production, and large-scale manufacturing activities. The country’s growing aerospace, electronics, and machinery sectors are significantly driving demand for high-performance coatings. In addition, strong domestic manufacturing capabilities and government support for advanced materials development are further accelerating market growth across China.

Hard Coating Market Share

The Hard coating industry is primarily led by well-established companies, including:

- IHI HAUZER B.V. (Netherlands)

- Sulzer Ltd (Switzerland)

- OC Oerlikon Management AG (Switzerland)

- CemeCon (Germany)

- IHI Ionbond AG (Switzerland)

- Momentive (U.S.)

- ZEISS International (Germany)

- Covestro AG (Germany)

- The Lubrizol Corporation (U.S.)

- Huntsman International LLC (U.S.)

- Solvay SA (Belgium)

- Clariant AG (Switzerland)

- BASF SE (Germany)

- Avient (U.S.)

- Construction Materials Co., Ltd., (China)

- Holcim (Switzerland), CHRYSO GROUP (France)

- GCP Applied Technologies Inc. (U.S.)

- Omnova Solutions Inc. (U.S.)

- DuPont (U.S.)

Latest Developments in Hard Coating Market

- In November 2026, DuPont announced the launch of a new range of bio-based hard coating solutions designed to reduce environmental impact and improve sustainability in surface engineering applications. This development is expected to strengthen its position in eco-friendly coating technologies and attract demand from automotive, aerospace, and industrial manufacturers focusing on low-emission production systems.

- In October 2025, BASF expanded its hard coating production capacity in Asia to meet rising demand driven by rapid industrialization and infrastructure growth. This expansion is expected to enhance supply chain efficiency, strengthen regional market penetration, and support BASF’s competitive position in the fast-growing Asia-Pacific coatings market.

- In September 2025, 3M introduced a new digital platform to optimize the application and performance monitoring of its hard coating solutions. This innovation is expected to improve operational efficiency, enhance customer experience, and accelerate adoption of digitally integrated coating solutions across industrial manufacturing sectors.

- In March 2023, Oerlikon Balzers launched its DiamondShield PVD coating technology, designed to provide superior wear resistance and corrosion protection for high-performance industrial components. This development is expected to enhance product durability, improve machining efficiency, and strengthen Oerlikon’s position in advanced surface coating technologies.

- In 2022, EMAG and HPL Technologies entered a strategic collaboration to develop advanced hard coating systems for automotive disc brakes in compliance with upcoming Euro 7 emission standards. This initiative is expected to support regulatory compliance, reduce brake particle emissions, and accelerate adoption of laser cladding-based coating technologies in the automotive industry.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Hard Coatings Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Hard Coatings Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Hard Coatings Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.